ANZ economists see house prices remaining "on ice" for the foreseeable future with a number of "opposing forces" applying in the market to balance things out.

In the bank's latest Property Focus publication chief economist Sharon Zollner and senior economist Philip Borkin have a look at the various factors influencing the residential property market this year. They don't have a detailed look at how the new Government's policies might affect the market, having done this in a previous Property Focus edition in November 2017.

In summing up the current situation they note that net migration is cooling, but should stay historically strong. Loan to value ratio (LVR) restrictions are being eased, but only gradually. Short-term mortgage rates are likely stable, although there is potential for some modest falls, but longer-term mortgage rates look set to rise in line with global reflationary forces.

"As is often the case with housing market drivers, there are plenty of moving parts. But even though house prices continue to look well out of whack with incomes, especially in Auckland, and the new Government intends to introduce policies targeting speculative housing demand, we still do not see a sharp downward correction as likely," they say.

"That would require a sharp deterioration in debt serviceability and a lift in forced sales, which is not on our horizon. Certainly if the economy was sideswiped by some particularly nasty shock from offshore, that could change the picture, but at this stage we are still of the view that with a number of opposing forces will simply see house prices remaining ‘on ice’ for the foreseeable future."

The economists say regional disparities in the housing market are likely to persist, which will come down to "the idiosyncrasies of various regions".

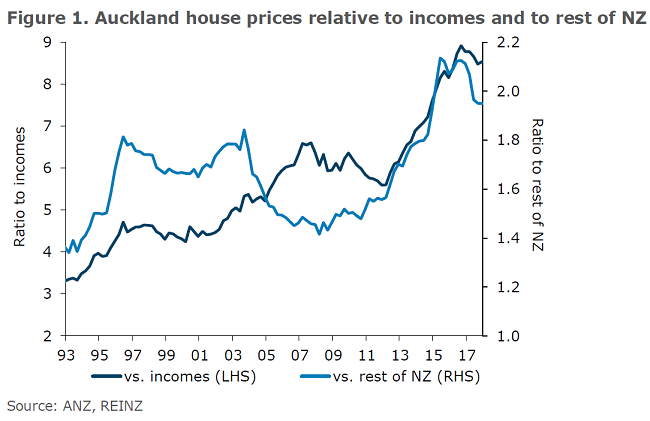

"Figure 1 below shows that while the relativities between Auckland house prices and the rest of the country have come back a little, they are still roughly twice the price of the rest of New Zealand. Relative population pressures and housing shortages will see a wedge maintained."

On migration, Zollner and Borkin say they believe net migrant inflows have peaked, given possible tweaks in government policy, a New Zealand economic backdrop that is perhaps not outperforming to the degree it was, especially relative to Australia, and due to natural cycling effects.

"While any migration forecast contains a great deal of uncertainty, we assume annual net inflows will ease to 45k by the end of 2019. While not necessarily a headwind for the housing market, it will be less of a positive influence."

On Interest rates, they continue to see the Reserve Bank keeping the Official Cash Rate on hold for the foreseeable future.

"That will help anchor short-term mortgage rates at historically low levels."

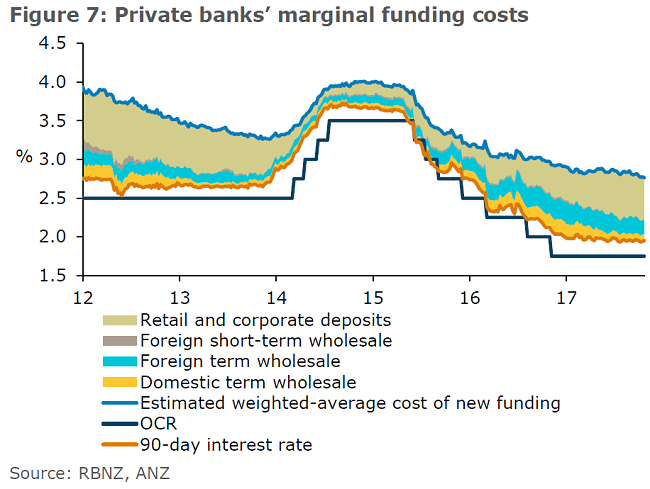

The economists say that over recent times, what has actually had the biggest influence on bank funding costs has been the ease (or not) with which banks could raise local term deposits (figure 7).

"Up until around 18 months ago, that was a relatively simple exercise, as domestic deposit growth was rising at a similar pace to loan growth."

But they say deposit growth (in this case household deposit growth) began to decelerate sharply – perhaps as the RBNZ cut the OCR and term deposit rates fell.

"At a time of still-strong demand for credit and increased scrutiny of banks’ offshore borrowing by the regulator and credit rating agencies, that forced banks to compete more aggressively for domestic deposits, forcing term deposit rates higher (despite wholesale interest rates and the OCR not moving).

"But as credit growth has cooled and deposit growth has lifted, those funding pressures are no longer as intense. As such, we have already seen some term deposit rates (and hence fixed mortgage rates) begin to ease modestly. As long as that ‘funding gap’ – the gap between overall deposit and loan growth – remains steady, a return of bank competition in the mortgage space could actually see mortgage rates begin to ease off modestly again.

"...In fact, with bank funding pressures subsiding a little, as the ‘gap’ between deposit and loan growth has closed, there is even potential for competitive pressures in the market to step up a degree triggering modest mortgage rate falls," they say.

"However, longer-term mortgage rates are at the whims of global forces and on the back of these, look to be biased higher."

On the RBNZ's loan to value ratio restrictions (LVRs), which were eased as from January 1, the two economists say they think these are likely to be eased further, "but only if the market shows signs of ongoing independent cooling (which may or may not be due to the policies of the new Government)".

"In that regard, we don’t see any changes having a large influence over market activity and prices over the next couple of years."

60 Comments

They would say that would they not? Its the last thing they would want!

They are absolutely correct

Yvil, how can anyone trust this ANZ forecast when their very own CEO forecasted a messy ending; https://www.nbr.co.nz/article/anz-boss-warns-property-market-calls-furt…

"Overcooked" was how he described Auckland property on July 20, 2016. Being that he will have been briefed by his own economists, what's changed since? Has there already been a price correction, a severe reduction of interest only lending or even a period of deleveraging so to return house prices to healthier fundamentals? Short answer - no.

The outcome of years of folly is yet to play out in some form and ANZ are just trying to calm skittery customers. What else can we expect ANZ economist to say?

R-P, I agree, we should not trust them, they will mostly state what suits themselves. Still in this article, they are absolutely correct

Never take any notice of any opinion put forward by an "employed" economist!

It really depends who they are employed by whether you'll get truth out of them.

It's not what you can see but what you can't see coming that matters ( the unknown unknowns). You pays your many you takes your chance - in other words you will never get certainty so take a chance based on your risk profile. .

In other words they, the ANZ, are saying "roll up roll up! get your 1 million dollar mortgages now so when the rates increase in a couple of years we'll make more money our of you"

Its like a passive bait and switch.

The only thing that will trigger a sudden fall in house prices is a sudden sharp and steep increase in the cost of borrowed money .

And every indication is that interest rates will remain low for some time to come .

So their prognosis is right ............... for now

Boatman, I have new respect for you, for you have quoted the most important sentence of the article. A great majority of people (including David Hargreaves who "tries to make sense of the various conflicting factors influencing the housing market" in his article of yesterday) cannot see this clearly.

If you look at the housing corrections in other major countries in last 2/3 years they are all tending to be gradual and that is probably what will happen here with a few developers going bust along the way and a few individuals quite a lot poorer due to failed property speculation.

There remains the supply side problem that isn't going to be fixed for several years yet.

Can you elaborate on some figures? You mean the 150k+ homes nationwide that aren't occupied by tenants? Oh that oversupply issue! Gotcha

Meanwhile equities are falling and long term bond yields are rising. Who knows what the future holds but I for one would not be liking to be holding big debts

Steer clear of any asset class where there is strong evidence of stretched valuations and existing "vulnerabilities". There is limited central bank buffers to protect the financial system from the next global shock. The QE boom has run its course.

If an indebted speculator hangs on hoping for better they must be prepared to lose all equity and more. That's just the life and times of a speculator. If there is price stagnation for the longer term then thats a chance outcome in itself. For many a spruiker its more of a self protecting wish rather than a fundamentally sound forecasted outcome. There is simply too many things that could go wrong, turning price stagnation into a freefall.

We know that global financial shocks are a more regular occurrence nowadays. So when ANZ forecast sounds a bit like Ben Bernanke from Jan 10, 2008 "'The Federal Reserve is not currently forecasting a recession" then best to prepare your finances for the unforeseeable.

The "experts" in the game never see the crisis coming - as this will spook the horses and ruin their game. Ben Bernanke; December 5, 2010 "'I wish I'd been omniscient and seen the crisis coming" The red flags were popping up everywhere, much like they are today.

This asset class where 85% of bank lending is secured - is simply too big to let fail. We all agree on THAT point.

I think the battered can is set to roll into the drain.

The experts will never make it known that they see it coming, it’s good to have it on record that they “don’t know”.

"Look out of whack"? Statement of a one who knows... but just can't say it. 'Are' not 'looks'.

Does "out of whack" have a rigorous economic definition?

If out of whack than either incomes have to go up to meet affordabily or prices down I suspect the later. A long way down to the lobby.

There is a 3rd option but unbelievably nobody seems to see it.

@Stealth Out of whack with incomes is not synonymous with out of whack with affordability.

Oh yes it does.

@PocketAces $1,000 @ 10% vs $1,000 @ 5%, affordability is filtered through interest rates, income to debt ratios are not, im confident that clarifies this for you.

Affordability by interest rate is your preferred measure?

NZ's measure of housing affordability is a bit different, not quite that simplistic:

http://www.mbie.govt.nz/info-services/housing-property/sector-informati…

https://www.stuff.co.nz/national/politics/92446194/new-ham-measure-is-p…

An affordability measure that only looks at the interest cost right now - and factors in neither changes in interest nor the time it takes to save a deposit - seems a tad simplistic.

While the Economist noted in March that NZ has the least affordable housing in the world:

http://www.newshub.co.nz/home/money/2017/03/new-zealand-housing-most-un…

@RickStrauss I am explaining that affordability and income to debt ratios are not equivalent terms. Your post is accurate and supports my point nicely.

Deposit growth slowing was not from low interest yield offerings. It was from slowing property volumes, there is a major major correlation that appeared after 2008.

It means the market after 2009 became simply a function of credit. And means that the deposit growth at banks, is actually loan growth at another bank.

The other thing, there is a major correlation between money supply growth in NZ and capital gains. Another major indicator of credit only activity. As property is now falling, it means the money supply will contract. RKerr hasn’t factored that in to his major inflation banana republic models I don’t believe, but to be fair to the guy, neither has anyone else

For the record, this all sheds light on the road the RBNZ is on. The RBNZ is on the road to QE within 18 months, they don't have a say in the matter unless they enjoy headline deflation, which I think is safe to say they don't. We aren't talking rate hikes here, its not even about rate cuts, because they won't expand the money supply to spur new lending, it is also why LVR removal, excuse my French, won't do anything, banks aren't even hitting LVR limits, nor will it stop the crowd from running, or change the demographic and credit forces at play. QE is not only necessary and completely warranted, but imminent.

You state: "property is now falling", which country are you referring to Lalaland?

New Zealand. Volumes and prices in nominal and inflation adjusted terms.

...the relativities between Auckland house prices and the rest of the country have come back a little

This will be an interesting watch over the coming decades. I anticipate the current Auckland Council policy of high sprawl development will mean a less valuable city. The more traditional compact city forms of Tauranga and Hamilton could provide increasing value.

David, I really enjoy your writing and think you are a quality journalist, but I wonder why these days everyone seems to insist on breathing life into the National Party leadership's top colloquialism, 'have a look at'? Might I suggest alternatives such as: analyse, gauge, examine or assess - to name a few? Next you'll be telling us the budget has 'dropped' (please, please no).

Sincerely, future grumpy old man, tongue not quite so firmly in cheek as perhaps it should be.

So the bank could be worried about a property bubble and so they issue a statement saying everything is fine?

Didnt Nat say overseas buyers were almost nothing. Then why are the agents and lawyers all kicking up a stink....?

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=119…

Every day it lools more and more like Nats lied their arses off on this. Shame on them.

Yes exactly Averageman - National & Real Estate machine:

1st breath: “Foreign/non-resident/nontaxpaying semi residents have had no influence on housing market”

.

2nd breath “ if you make it difficult for foreign buyers, the whole housing market will crash, all new developments will fold, it will be an economic disaster”

.

Which one?? Lol

The actual quote is "Banning foreign investors .."

Definition of ‘foreign’ and ‘investor’ is debatable.

Plenty of options for non NZ tax paying people to keep buying NZ property.

Hey - if you are a lawyer the word Definition is up for debate.

And I suspect the Auckland District Law Society and Real Estate Institute are allowed their view too.

The words investor and owner/buyer seem to be interchangeable these days. Dictionaries ain't what they used to be.

No. No they didn't.

But now that foreigners will be banned can we expect housing prices to halve?

At least, I'd say they'll drop about 150%

Cool, ....When?? ....cos apparently all sale prices and volumes now seem to be " insignificant" ...... the real reduction effects will come April/May .... No , Wait, Maybe July/ August sales will be more significant and show the real trend of this market - Actually the real crash will start in 2019, surely .! ..Best bet, Don't buy until we see properties back to 2003 prices ....

If you have only local money in the market, then yes prices should fall back to levels that people can afford on local wages, also more likely now investor leverage is less in play with no rampant CG to use

.,

https://list.juwai.com/news/2017/07/juwai-releases-chinese-global-prope…

Says it all really. The foreign ownership ban will have a significant impact. NZ ranked 6th most popular property market by Juwai. NZs share of 80 billion USD last year and 100billion in 16 must be significant....with majority flooding into Akl. Spin some more BS National. In the absence of being able to be proven wrong I'd guess Chinese $$ accounts for 30% or more of Akl market. Interesting how the ramp up of Chinese foreign investment correlates with our rapid rise to property wealth nirvana. Hearing the REs, lawyers & Radio Live blue bloods squeal is the final confirmation.

Squealer in chief being Ashley Church, heard him yesterday on Ali Mau's show and he admitted, almost sheepishly that property investors' number one driver was capital gain in properties they bought, how being a landlord was just secondary. That about confirms what I've thought for a long time, that renting in this country is little better than people farming or a by product of the speculation game. We have to do something about it and it's going to require the govt to step in and build masses of social houses and houses for fhbs

Unfortunately the foreign buyers will still find a way to use some form of legal proxy to buy property.

The ban may slow things down for a while.

Forfeiture if they are caught out would make a few think twice. That is what I would do.

Then do it

Perhaps apply a new rule of thumb: "What would Augustine Lau do?"

Agreed. Proposed $20k fine on lawyers has them hand wringing already.

Just like people find ways of committing fraud, burglaries etc. When you make something illegal, then there is always a consequence behind it.

Yep. Looks like the only way out of this feck-up so that we have houses as affordable accommodation rather than houses as non-functional speculative tokens and money-laundering vehicles is to flood the market with state houses that remain in state ownership. Just because some landlords and property managers have developed this revolting sense of bloated entitlement to exploit and punish their customers doesn't mean the rest of society has to indulge them.

That's what I reckon with the state housing.

Actually I take that back re the lawyers, they're rightfully complaining because they are tasked with determining the legitimacy of residency by purchasers. Trying to decipher the money behind a Trust, Partnership or Smurfing group won't be easy. Perhaps the RE's job should be to prove it, considering the fees charged and ability to stop the deal before it starts.

Auckland investors always overshoot in the regions at the end of each cycle. They make the mistake of thinking the regions have the same dynamics as Auckland. Simply... they do not. All direct quotes from Tony Alexander at BnT " please dont stop the buying frenzy (read in comission) seminar.

Agree that Awk tends to flatten vs drop. Will this time be different due to external influences pumping a bigger bubble this cycle will be well covered in future reporting.

Pick your fork in the road a) fluffy unicorns it can only go up....or b) maths so broken and twisted by external influences some sort of correction is inevitable.

The real skill is to hedge both outcomes I guess

Averageman, X2 - Well said

its interesting that the articles that attract the most comments from left wing labour voters are on housing. I can almost feel there gut wrenching fear as they monitor the price of houses and rage against those nasty bad evil banks and the grand puppet master john keys... yes who took my dreams away...

Hmmm im pretty right of center and have a property portfolio as well. Just not levereged to crazy levels didling my tax waiting for speculative gains. Just saying the factors driving the ponzi have and are changing. Been a golden run but the next 5 years wont be like the last 5.

All this political polarising and bating is getting really old.

I'm not a left or right fanatic. Like a great many people, i'm fairly centrist and vote both ways. However, you would have to be deluded or a short sighted fool not to see the housing affordability and rising inequality issue as a serious issue for the long term health of NZ society.

Its also to be expected that there is more interest in the housing market then other topics. Both the banks, and majority of households have most of their wealth in that market. And then consider all the people under 40 who have been locked out of the housing market, desperately hoping to be able to own their own home one day, and praying for prices to return to something sane. Obviously that will be the hot topic.

Preach it, sister! It's just mindless tribalism.

I'm not a member of any political party, don't particularly care whether the blue team or the red team is in to bat, but will absolutely judge them on factors such as results, honesty, corruption, pandering to cronies, punitive policies, and how much time they waste on political machinations rather than getting things done for the benefit of the citizens.

I was pretty easy about National winning 2008, wished them well, but they've been bad news for everybody but the donors and lobbyists, and will remain on my shit list until they've cleaned up the corruption.

the ban on foreign buyers will be massive. Labour have gone further than Australia in effectively banning foreign buyers from new builds. The effects on the economy may very well be dire.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.