ANZ economists foresee prices rising more aggressively than expected, so believe the Reserve Bank (RBNZ) will respond by hiking interest rates in larger increments than usual.

ANZ economists now see the RBNZ’s Monetary Policy Committee hiking the Official Cash Rate (OCR) by 50 points when it meets in both April in May.

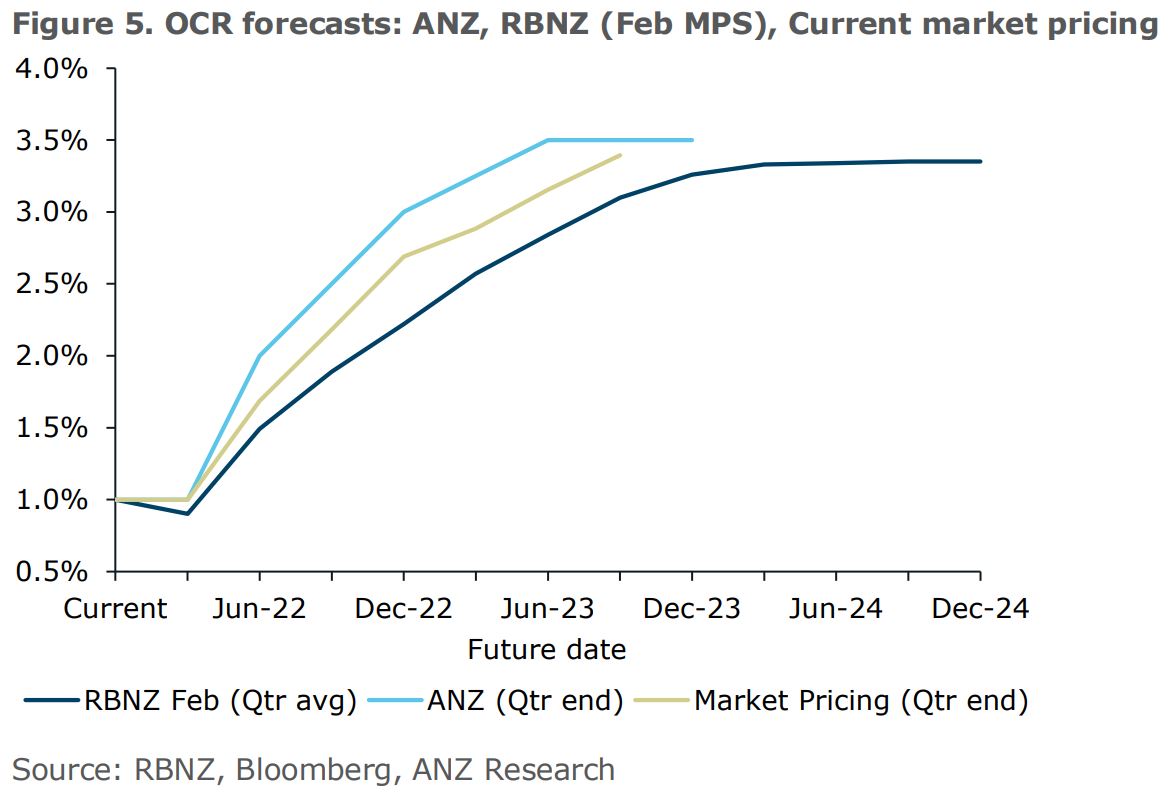

This would bring the OCR up from 1% to 2%.

ANZ economists previously thought there was a 50% chance the Committee would hike by 50 points.

The Monetary Policy Committee typically changes the rate in 25-point increments, but when it last met on February 23, it said it was “willing to move the OCR in larger increments if required over coming quarters”.

ANZ chief economist Sharon Zollner and senior strategist David Croy expect the OCR to reach a peak of 3.5% in April 2023. Previously they forecast it peaking at 3%.

Their change in outlook comes as they now see consumer inflation peaking at 7.4% in the June quarter - above the RBNZ’s forecast peak of 6.6% in the March quarter. The Consumers Price Index rose 5.9% year-on-year in the December 2021 quarter.

“The RBNZ would prefer to look through oil price shocks, but right now, with inflation expectations so high and rising, they just can’t,” Zollner and Croy said.

While consumer inflation is running hot, and there are “clearly mounting downside growth risks, both in New Zealand and globally”, they expect house prices to fall 10% in 2022. Previously they expected a 7% fall.

“Evidence continues to mount that the housing market is slowing more rapidly than their forecast, and things could get a little messy there,” Zollner and Croy said.

They noted back-to-back 50-point OCR hikes seem risky when double-digit house price falls are forecast.

“But there aren’t any low-risk policy options anymore,” they said.

“The fact is, it’s just no longer true that mild downside growth surprises will derail OCR hikes.”

Drivers of inflation

Zollner and Croy noted a lot has changed since the Monetary Policy Committee last met (and hiked the OCR by 25 points).

Crude oil soared to nearly US$140 a barrel at one point this week, rather than start its journey back to US$80, as the RBNZ assumed it would a couple of weeks ago.

“There seems little hope of the Ukraine situation being resolved quickly, and we do know sharply increasing fuel prices will be particularly visible,” Zollner and Croy said.

“Indeed, analysis shows that petrol prices have a much bigger impact on household inflation expectations than their weight in the Consumers Price Index alone would suggest.”

They said rising inflation expectations could also feed into a wage spiral, “given the extreme tightness in the labour market”.

Furthermore, commodity prices have jumped. Dairy commodities are trading at an average price of US$5,065 per tonne versus the RBNZ assumption of a moderation to US$3,500 over the forecast period.

And, a net 74% of firms surveyed as a part of ANZ’s Business Outlook survey intend to raise prices over the next year.

End of low inflation era

Zollner and Croy questioned, "If inflation risks are so severe, then why won’t the RBNZ just carry on and raise the OCR to 5% or 6%?

"The OCR may well get there, in the fullness of time, given our sense that climate change and de-globalisation spell the definitive end of the very-low inflation era.

"But it seems more likely to be in the next cycle - we’ve got the aftermath of a housing boom to tidy up first."

Zollner and Croy believed a 10% fall in house prices, from the elevated levels they're at, would constitute a "soft landing".

They said concerns around the impact of a larger fall would be a greater impediment to the RBNZ lifting the OCR more quickly, than concerns around the impact of higher debt servicing costs.

The latest from the RBNZ

Interest.co.nz spoke to RBNZ Deputy Governor Christian Hawkesby on February 28 - five days after the release of the Monetary Policy Statement, and just as Russia's invasion of Ukraine was really kicking off.

He said, "If oil prices stay where they are at the moment, that’s higher than where we projected in our Monetary Policy Statement.

“So, the very near-term implication is that we’ll have higher CPI outturns over the next quarter or so than we had factored into our statement.

“The key judgement for the Monetary Policy Committee will be - we can’t control that. It’s happened, it’s come from overseas, what does that then mean for the outlook for inflation going forward?"

130 Comments

50 bps increases are still too little too late. The OCR should be hitting 3% by May, not 2%, if the RBNZ wants to retain some hope and credibility to combat inflation and try to unwind the results of its stupidly ultra-loose monetary policy of the recent past.

100 bps increases are necessary, to make any difference.

Not increasing the OCR quickly and aggressively now will result in the RBNZ being forced to go even higher later on.

Even if the RBNZ acts timely, the OCR peak of 3.5% predicted by ANZ is still too low - the peak will have to go between 4% and 5% in order to rein in a potentially runaway inflation surge.

. 25 she goes, slow and steady. Banks have got it wrong every step of the way

I disagree, RBNZ is too far behind the curve, needs to go big to make a statement.

Can't continue to let it run or we'll be 3rd world, fortunately our dollar hasn't tanked as yet so we can still rescue the situation

Needs to? Maybe.

What will they do? 0.25 steps.

With stagflation its a catch 22... Whatever you do its hitting the fan anyway.

Meanwhile other CBs cant make their minds when or if they will make a first move up vis a vis RBA and ECB. Or we could do a Russian move and go vertical in a single bound to 20 percent :)

A lot of the assumptions around the housing bubble being "iron clad" was based on the assumption the vested interests would always be willing and able to step in an arrest any correction.

It is looking increasingly likely this is the event - from outside influences - that forces their hand and they are unable to effectively intervene.

Ironically it has come about largely due to the RBNZ's inaction in failing to raise rates to try and get on top of inflation early - simply to protect the housing bubble. They had 9+ months of clear data that showed the aggressive stimulatory monetary policies needed to be gradually withdrawn. Instead they may now be forced to move very quickly and creating a minsky moment.

They actually need to drive non-tradable inflation down now to counteract tradable inflation. A reduction in rents, rates, utilities etc. is required to offset increases in commodities. If consumers are hung out to high inflation the economy will crash as spending declines in real terms.

It's cute that these ANZ economists still cling to the belief that Orr's woke tree cult will do anything more than pay lip service to their inflation mandate.

Rational minds gave up believing in fairy tales long ago.

The RBNZ are way behind the inflation curve. Real interest rates are still loosening and will continue to do so while they claim to be "tightening".

Certain government policies couldn't have come at a worse time such as the planned phase out of low-user power plans that will make 40% of NZ's households worse off by up to $126 in annual fixed user charges.

https://www.mbie.govt.nz/building-and-energy/energy-and-natural-resourc…

The worst part is MBIE claims the remaining 60% households may not necessarily be better off from this phase-out exercise, since there is uncertainty over how power companies will choose to structure their pricing plans once the phase-out begins, and therefore what the impact on households will be.

Not just oil, most commodities have been moving upwards in tandem.

Don't see it though, if they where going to do the 50 they'd have done it last time they reviewed the OCR. If anything, the fact the Russians haven't cut energy exports despite the war, means inflation is likely more subdued than it could have been at the last meeting.

along with wheat, soy beans, rice and oats ...

scroll down for yoy increases https://tradingeconomics.com/commodity/oat

If so, have ANZ recalibrated their house price and economic growth forecasts?

If the RBNZ does this, then we'll be in a recession by mid year and house prices would likely have dropped at least 10-15%.

Edit: I see they have in fact changed their forecast of house price declines from 7 to 10%. I think the declines will be greater if the OCR is 2% by June.

there may well be recession ahead and that is probably the safer option than letting inflation erode our collective wealth and further impoverishing the poor.

Besides if inflation causes massive increases in living costs, the result is the same, no discretionary spend = recession

Our collective wealth?

Haven't we been inflating our "wealth" for the past two decades and now it's going to erode with inflation?

Forgive me for being a little confused.

Given that Auckland prices may already be down close to 10% in 3 months (waiting for REINZ HPI figures) it seems pretty hard to believe the total drop won’t exceed 10%.

Completely agree. At the current rate there's every chance we're looking at a 15% or so decline by June. If that happens the second half of 2022 will be very interesting.

On an anecdotal note, I've never seen so many for sale signs pop un in such a short amount of time around my neighbourhood.

You are welcome to believe anything and many do.

100bp of hikes in next two months … and OCR peak of 3.5% and forecasting house prices to ONLY drop 10% this year?!? … Sorry ANZ but either you’re just trying to be dramatic and get some click bait or your model of house prices vs interest rates is broken… down 20-30% is the more likely outcome if your OCR path is correct.

Yep totally agree - 20 to 30% falls if their OCR predictions are correct / close to correct.

That would be roughly a 10% fall for every 1.00 increase in OCR... so a 32.5% fall if their estimate of an OCR increase from .25% to a peak of 3.5% is correct... which sounds about right

OCR at 3.5, retail rates would be circa 6.5-7%?

Definitely house price crash, as well as a house building crash, big recession, and soaring unemployment.

All of which may end up being the lesser of two evils.

"The path of least regret"

And yet the extreme measures the RBNZ went to in 2020 to avoid that outcome (a house price crash) by removing things like LVR's that were put in place to protect buyers from overextending themselves....and yet it would appear that if we do have a crash now, that Orr and the team used the buyers as collateral in order to kick the can down the road a few years after encouraging banks to go out and lend, lend, lend.

Such a crazy situation and set of actions by the central bank.

Adrian Orr: Banks must be 'courageous' and continue lending to customers in the tough times. September 6, 2020

Which would imply there's something structurally/fundamentally wrong with The Economy.

My first and only mortgage was @7.5% in 2000 and it was a non issue. 100% financed on a reasonably priced home.

Rome's burning.... again.

And that’s nominal terms…and a few years of inflation at 5-10% to that…assuming the recession doesn’t cause near immediate deflation.

Be Quick!

Where is the clown? He now realises he was fatally wrong?

Hi DDDDebt.

Another way to look at it , for every 1.00% increase in OCR is about $100,000 off the value of the average kiwi home.

https://www.rnz.co.nz/news/national/459095/million-dollar-homes-average…

Brilliant... that's a much easier way to look at it and explain it.

Agree - clickbait. Look at Bryan Easton's review of banks' forecasts when the pandemic hit - he was particularly scathing of ANZ

Yes that looks like a 30% decrease in property values by December.

Don't worry guys. Jacinda assured the nation on the news last evening that this period of high inflation isn't here to stay.

Then again, the woman didn't know the difference between GDP numbers and Crown accounts after serving as PM for more than 12 months.

We are learning the folly of a leader elected on the back of performative caring instead of intelligence. What's even worse is that she installed a finance minister with a Dunning-Kruger level of macro-economic competence.

Nationals no better

they are trying to retrain Bridges from law into economics.....

Why waste effort training a numpty when your entire manifesto could fit on a sticky note: more migration, less construction, more roads, more utes, less taxes on the rich, remove environmental regulations, deregulate tenancies and employment, and cut back spending on education & health.

As I've said before, the longer RBNZ wait, the higher OCR they need to hike. Do it now avoid more pain in future.

This would happen in an ideal world. However, recent purchasers also need to settle with their loan approvals so it would make sense that the lenders and the RBNZ should keep things relatively loose in meantime until such time and if the narrative changes.

Here comes the pain.

"The Depelter Turbo ... prepare for a lot of stinging !"

Sudden short shocks will decimate consumer spending but they're basically inevitable after leaving things too low and arguing about transitory this and temporary that.

We're heading for a very, very dark time that may well see recent FHBs wiped out without housing becoming any easier to buy for those currently on the sidelines. And that's before contemplating the effect a collapse in discretionary spend would have on employment numbers. Everyone assumes their job would be safe if interest rates suddenly spiked and house prices dropped. That's a bold assumption to make.

As I have said many times, the house building sector would collapse. Directly and indirectly it comprises about 20% of employment in NZ.

Nasty feedback loops then build and it's a downward spiral.

Yup. Some of us here have been arguing stagflation for a while and it looks like we now have target fixation. Inflationary wage growth spirals can't save us but it might help ease the pain, but will only reward those who are prepared to job-hop. NZ employers generally won't meet a market rate to keep staff, so they deserve everything they get.

maybe the govt could finally get to starting that kiwibuild project they promised but never delivered

Wouldn't a slowdown in construction present the government the opportunity to have social housing built? i.e. pick up the slack? It would solve two issues at once.

Maybe, but that's dependent on them having their act together...

And they don't. So the lag times in getting failing firms contracts will be too great.

It would be the perfect chance to be ready to ramp up construction of social housing. But Labours track record of converting plans into action (or even having a coherent plan) doesn’t leave me with much hope.

Correct.

And they aren't set up to suddenly engage a whole lot of failed builders. Their whole system is too traditional, top heavy and clunky for that.

Let's be clear it's the public sector system that is not set up for this with numerous "Offices of" playing go between ministers and those public servants doing the actual work and the only value add is to slow things down. That doesn't change under National

I think we are already getting very close. Having recently been quoted at $4700 per sq m for a standard spec dwelling, up from $3000 the year before, it's quickly becoming impossible to build.

Paying around $1500 in Australia give or take.

Something is very very wrong in New Zealand.

Perhaps Fletchers supply business is trying to make up for the Casino and Christchurch precinct losses.

Yeah I see a lot of 2nd tier lenders ending up in strife.....where are they getting their funds?

many from supposedly sophisticated investors chasing higher yields.....finance co debacle no 2 on the way?

how many developers are going to get squeezed between cost overruns and falling finished product prices??

The answer to your last question is 'an awful lot'.

Not to mention workers coming down with Covid meaning already delayed builds are slower to complete, generating cashflow problems caused by the payment structures of new builds.

This recent housing boom has lured in a lot of property investors to become first time property developers. There are a high number of inexperienced first time developers that have popped up in the last few years. Including in my own extended family. Zero experience in building or running a building project in uncertain times, just the belief that if you can leverage up, you can’t lose.

Very true. There is a lot of people who assume prices can’t fall as owner occupiers will just hold and can eat the rising cost of debt servicing. I agree that owner occupiers will just hunker down.

Its the specuvestors and the highly leveraged developers that will likely be the hardest hit. They can’t just hold on. Interest only loans, high leverage, rising interest rates, evaporating capital and capital gains turning to capital losses could quickly become untenable.

Top comment GV27 !

So the spruikers are going to be spooked!!!

The cowboys will be spooked. Unfortunately, the seasoned spruikers will just wait out the tide for our housing-led national economy to topple over and RBNZ to then cut interest rates aggressively in an attempt to pump liquidity into our "markets".

Obviously, the only markets that matter to the RBNZ and Labour-National are REA auction rooms.

Unfortunately, far too many people listen to spruikers like Ashley Church... who now tells us the only thing we have to fear is fear itself

OECD have been warning of this for years

We topped their list of countries with highest risk of a correction

https://www.newshub.co.nz/home/money/2021/06/new-zealand-tops-bloomberg…

Bloomberg are clearly doom gloom merchants so their views should be ridiculed and dismissed (sarc)

Church is going to soon be looking like a total moron.

I hope very few FHBs have listened to him.

Church is usually a sacred word, except when it's preceded with 'Ashley'

Quite a few people are going to come to regret listening to these self-interested charlatans.

While banks so called stress tested mortgage applications at 6 or 7 % they didn't also allow for cost inflation of 7% plus , combined this will be a fatal combination for highly mortgaged households.

The banks and more than happy to massage figures to pass the stress test.

Yes, just see their shrieking when personal responsibility for directors was added into the picture.

Correct, the banks stress test only cares if they get paid at 7%, not if you have to skip a meal to fill the tank to get to work.

Fortunately I think the whole game will have collapsed long before we get there, anything above 6% is 'Danger Will Robinson' stuff.

You know, to ordinary working people. Probably not to cabinet ministers or senior governors at financial institutions that will remain nameless.

Highly mortgaged will find it difficult to sell when buyers are stress tested at 9-10% which will need to happen if rates go back to 6-7%

The RBNZ does indeed need to hike in 50bps increments but no matter what they do, it's going to get very messy. Inflation will persist and a recession is coming late 2022 early 2023. There is now a good chance for housing values to drop by 20%

There is now a good chance for housing values to drop by 20%

I like the way you described a house price crash while skirting around an utterance the dreaded c-word. This is a good strategy if you want to avoid the class clowns dogpiling you for doom and gloom.

Speaking of which, where are they? They've been surprisingly quiet these last few days.

What?

20% is where a correction becomes a crash. Proper doom and gloom.

Hi Yvil.

Did you just say CRASH ?

Quite a turnaround for ole Yvil, who has been pretty much an advocate of 'you can't lose with property'.

Yvil, honorary membership of the DGM crowd granted.

I don't quite adhere to the idea of people's position having to be black or white, for or against, "spruikers" or "DGM", in my opinion, the world is more nuanced and the world changes. Indeed for about 30 years, house prices have mostly gone up and they have been an outstanding way of making money. Today I see so many headwinds pushing against property all at the same time, headwinds that didn't exist only a year ago, so yes, I think house prices are going to go down, I also think inflation and interest rates are going to continue to increase significantly, which will hurt many less wealthy people and a recession will follow. When the mess is over in a few years? time, I might well become bullish again, I don't see a problem with adapting my views and strategy to changing conditions.

All good :)

It's still a big turnaround though.

Good for you. We should all be fitting our opinions to the data and not the other way round, but it is very easy to become stuck in your ways when you have money invested.

Yes good on Yvil.

For a long time he certainly seemed to be a believer in the religion of 'House Prices in NZ can never crash'.

It's a shrinking religion, a shrinking Church of believers, but there's still plenty out there. In fact A. Church is one of the few high priests still publicly saying there's no house price crash, not even a 'correction'!

Meanwhile, CWBW still hasn't come out of the basement / dungeon with the boys. Too much fun?

I've re-read my post, I'm pretty sure I didn't say "crash"

I think the common view is that -20% is a crash rather than correction. So people are calling it a crash for you :)

It's silly and petty. Actually if you want semantics, a drop of over 20% is referred to as a bear market.

I think most people would say 20% is a crash in terms of property market declines.

10-15% a significant correction.

You may wish for it however context matters, 20 percentage in the context of the prior years increase is a correction…no crash. inflation is the real issue here and in real terms what asset/investment class is looking good….

A 20% is a crash, especially in a high inflation environment where the real fall is closer to 30%.

You over reach..so many NZX shares, inflation adjusted, have also already crashed by your measure. It a relativity situation, have you ever experience an economic cycles...

Yes, many cycles, and got hit quite hard by the 2007/2008 crisis. What's your point?

I sold my share portfolio last October after having a pretty good run for 5 or so years.

I'm happy enough with cash in the bank for now in addition to the house I live in, I might buy some shares after they tank even more.

There are a few C words out there that appear to be taboo. Jacinda and John Key both had trouble with the word crisis as well. Sadly this crash seems baked in however you describe it.

I said the RBNZ should have gone 100bps last review but no. They are falling further and further behind but refuse to acknowledge it. What do I think now ? They are clearly in total denial so expect tiny 25bps rises for the rest of the year. External pressures are mounting, can they continue to ignore them now ?

Hang on, this inflation is transitory right???

.25 all the way, Mr. Orr has shown time and time again he is more than comfortable to watch and wait.

They noted back-to-back 50-point OCR hikes seem risky when double-digit house price falls are forecast.

“But there aren’t any low-risk policy options anymore,” they said.

Why would the RBNZ be worried about house price falls? Surely they have ensured the banks would be safe under those circumstances (its not exactly something unexpected), and they shouldn't be worried about the economic outcomes as that is not in their remit (there is always an economic downside to raising interest rates to curb inflation). The only reason would be the stupid full employment target, but considering we have very low unemployment and very high inflation, that doesn't seem like a good reason.

I suspect we are going to see how good their stress tests actually were.

If the banks fail that would be incompetency in the extreme considering the market has looked bubbly for years.

Economists strike again with crap, the raise will be 0.25 bps again.

.50 will only happen if the fed goes for bigger raise on 16th March.

I agree its clear that the RBNZ intends to sit on its hands for as long as possible. Unfortunately for them the outside influences that are outside of their control are starting to mount. Oil predicted to hit as high as $200 a barrel and we will have $4 a liter petrol in no time flat. This flows into transport costs of food so even official inflation is going to go double digits and we already know its actually already double digits.

Realistically the RB will try to ensure the currency doesn’t drop, the only way they can try to mitigate that is stay in step with the fed…everything else will be just collateral damage.

I just read these articles now as either banks asking for more free money (interest payments) from Govts, the wealthy demanding a higher return on their wealth, or business leaders demanding action that increases unemployment so that their labour costs don't go up.

Also worth noting that some of the products with large price increases (e.g. oil) are not substitutable in the short-term. Higher prices for these products will therefore have a similar demand-side deflationary impact as changes to OCR / mortgage rates - i.e. they both reduce disposable incomes, aggregate demand in the economy, and unemployment. I personally don't think demand-side measures will make any difference to prices - but, hey ho. Sometimes I think economists just love a good recession.

What is your alternative to avoiding recessions?

It would be like having life with no death, reward with no risk. Where would the balance in that be?

The avoidance of recession the last 10+ years has caused many investors to believe markets are risk free (it has also severely distorted prices of assets like property, shares and bonds to unsustainable levels). That simply isn’t true. People are behaving irrationally because they haven’t been hurt for their excessive risk taking. Many lessons are to be had from a recession…a chance to learn what is true and what is not…a time to renew and rebuild…removing excess risk and inefficiency

That's a great question.

We have operated an economic model since the 70s that incentivises boom and bust - particularly in the financial markets where the unchecked creation of credit, leveraging off that credit, and a frankly wild west derivative market create wild swings, over-valued companies, and rampant speculation (gambling).

We need much stronger stabilisers than wiggling the OCR up and down in an attempt to (a) control the quantity of credit fuelling the economy, and (b) keep 'just enough' people unemployed.

Those stabilisers would include going back to the future and re-focusing central banks on controlling the quality and quantity of credit. Whilst I buy the need for some leveraging and even the limited use of some derivatives (e.g. hedging), making cheap credit easily available for speculative purposes has to stop. I would also end involuntary unemployment and run a bank of locally run 'transition jobs' that people could take-up instead of welfare to stay in work, stay job ready, get training, and return to better paid normal employment when the market picks up. Planting natives, fencing off streams, or teaching music or te reo to kids would all be good examples in NZ. Note that this scheme is not a socialist dream - it is a strong fiscal stabiliser. Govt would invest more in these jobs during a downturn (providing fiscal stimulus to the economy) and less in the upturn (withdrawing stimulus).

Have you read much on Ray Dalio's long debt cycle and where we are at in that? It might clarify a few of the areas you touch on above.

Removal of the gold standard in the 70's perhaps explains a lot of what you describe above. Its only a matter of time before the USD loses its reserve currency status and given the amount they are printing and the conditions that now face us - it could be the only option they have is to print more $$ when they should be doing the reverse if the dollar had a sustainable future.

I am familiar with Dalio's views on the debt cycle - I would say he built heavily on Minsky's work, which had a bit more nuance, not least because Minsky was heavily critical of financial speculation and the parasitical tendencies of the finance industry (which is basically Dalio's job!)

The gold standard was regularly bypassed. I would point the finger of blame for over-financialisation at the rise of neoclassical monetarism, the cocaine fueled Wall St culture of the 1980s, and the unchecked introduction of technology and trading tools that have left us with algorithms in charge of sucking gains out of the economy, with ridiculously over-leveraged derivatives driving boom and bust cycles in the very commodity prices they were originally set-up to smooth!

Thank you both Jfoe and Observer for this little thread. +1 for your time taken to post these considered comments.

Great comment IO !

Expect nothing but a weak response from Orr...

Agree that 50 bps is to little to late and that 6-7% here we come. Regardless of RBNZ action/inaction the banks will lift rates at the behest of their overseas owners to continue their super profit extraction on the NZ economy. Tenants can double their rents to catch up....fat chance of that In the inflationary firestorm of 2022.

Time for patience and keep building the vulture fund. Yield math loves higher interest rates...

50bps twice in a row? Wishful thinking. 25bps it is.

RBNZ doesn't have the balls to burst the bubble.

The bubble is already leaking air without any further change in OCR due to the credit tightening.

If investors start cashing up and getting out to avoid further losses in capital gains then this will accelerate the downturn without any intervention from Orr. Another OCR hike will just be more oxygen to the raging fires already burning.

This is going to get very real, very fast.

When the Nanny Herald is pumping this info out you know things are looking BAD.

https://www.nzherald.co.nz/business/interest-rates-to-soar-house-prices…

Have my popcorn. I owe not a cent, large mortgage free house, earn $10k pm and investing in WW2 German stuff. Life is good.

The amount of doom and gloom on here is outstanding!

Yes discretionary household spending will decrease as a result of increased mortgage interest payments. However your average household will just tighten their budget.

But remember we are in a tight labour market and households will seek to change their employment for a 10%+ increase in salary.

Property investors will feel the pinch. But every investment holds risk, and they've made huge paper gains, which will likely remain positive even with a 10 / 15% decrease in property this year. They can always sell.

I accept developers will be in a spot of trouble with high debt, increasing cost to service, and supply constraints pushing project deadlines.

Re interest rates, how much impact do you guys think an increased OCR is really going to have? It won't materially impact demand for fuel. And increasing costs of supply are a key driver of increasing / inflating product costs.

You forgot to mention a couple of things that are the main driving force behind house prices:

1. The already abysmal rental yields will tank (unless mortgage-free) due to higher interest rates. People won't be paying an extra 100-200 per week for a shitty 3br. Who's gonna buy rentals that have net yields lower than your average TD?

2. Tighter lending conditions will cut off the stream of buyers at the low-to-mid tiers. One might be able to afford a million dollar mortgage at 3%, but not at 5-6-7%. (Stress-test doesn't mean anything)

3. Sentiment is key. When most investors and wannabe FHB's think that prices will keep going up and up and up, people are ready to overpay just to "get on the ladder". House flippers won't be so eager to bid at auctions now, and a well-positioned FHB won't be rushing to buy that mouldy shack in Papakura for 1 mil.

Sorry Jester, we all know landlords can pass on any cost they want, it’s one of the Church’s 10 commandments.

Bold to assume that people can realistically change employment and just add 10% onto their salary just like that. Many of us are not in a position where we want to spin the roulette wheel and a being last on board with a new employer with a significant period of economic uncertainty looming may not work out for people if things get uncomfortably tight.

And unfortunately, 10% has to come from somewhere, and with business inputs rising many will simply say it's too hard to increase pay at this time. As usual, those in a position to take advantage will do well, but for those who aren't, they will take a big squeeze with no sign of relief.

And bold to assume PIs can just sell. That might be true at a very reduced price, but that may then require them to also pay back their loss to the bank.

More to that point, we have such a labour shortage in this country, employers are crying out for workers. If you can't make a decent living and afford a decent home working an average job, that shortage is just going to get worse.

I live in a provincial capital. My daughter put an offer on a bigger home for her family but was beaten by Aucklanders who offered $300k more than my daughter subject to selling their home in Auckland. The agent said the Aucklanders had an element of fomo in their offer. My daughter has taken it on the chin which is admirable. She did make an unconditional offer as she needed to be competitive. How is the Auckland market going currently? Is it as strong as it was late last year?

I'm expecting bigger house price falls percentage wise in Auckland than anywhere else. I'm hearing that people are bailing out of Auckland and many are heading North. I expect an Auckland exodus, sell while you can at stupid money and it buys so much more in the regions. There appears to be many seeking early retirement.

An agent from another firm thinks the vendor will come back to my daughter but that depends on what the purchaser is selling in Auckland and whether they get what they want for it. Where I live the agents are brutally honest. Less houses selling, less inquiry, fear of paying too much and mainly very hard to get finance.

Wonder how many might regret that when they're needing more and more medical care in the regions.

Thames is a hidden gem, yes it is a pun on it being founded on gold mining. The local hospital, first built in 1868 and since refurbed, there is no lack of health care in close proximity. Has plenty of shops and eateries and popular coastal environments. Surprisingly cheap houses being snapped up

My current thinking is that the market will simply dry up for a few months . Very few people have to sell and very few have to buy. House construction will also slow down and banks will be very cautious about financing new property developments.

KeithW

True, as long as everyone hangs onto their jobs. If unemployment takes off then everything changes as people are forced to sell. The longer this war lasts the worse it will get. I don't have a good feeling going forward.

Developers have no option but to sell.

Expect a fire sale on new 2 bedroom shitboxes in the coming months.

Very weird, seeing developers trying to sell two bedroom townhouses in the sticks for a million dollars.

Entitlement Mentality has taken Auckland pricing to madness.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.