Welcome to 2026. It's early in the year, but the main drivers for the tax year seem already set. With $9.3 billion of tax interest and penalties outstanding as of 30th June 2025 Inland Revenue's crackdown on debt will continue. It will also ramp up its investigation activities, with holders of crypto-assets under particular scrutiny.

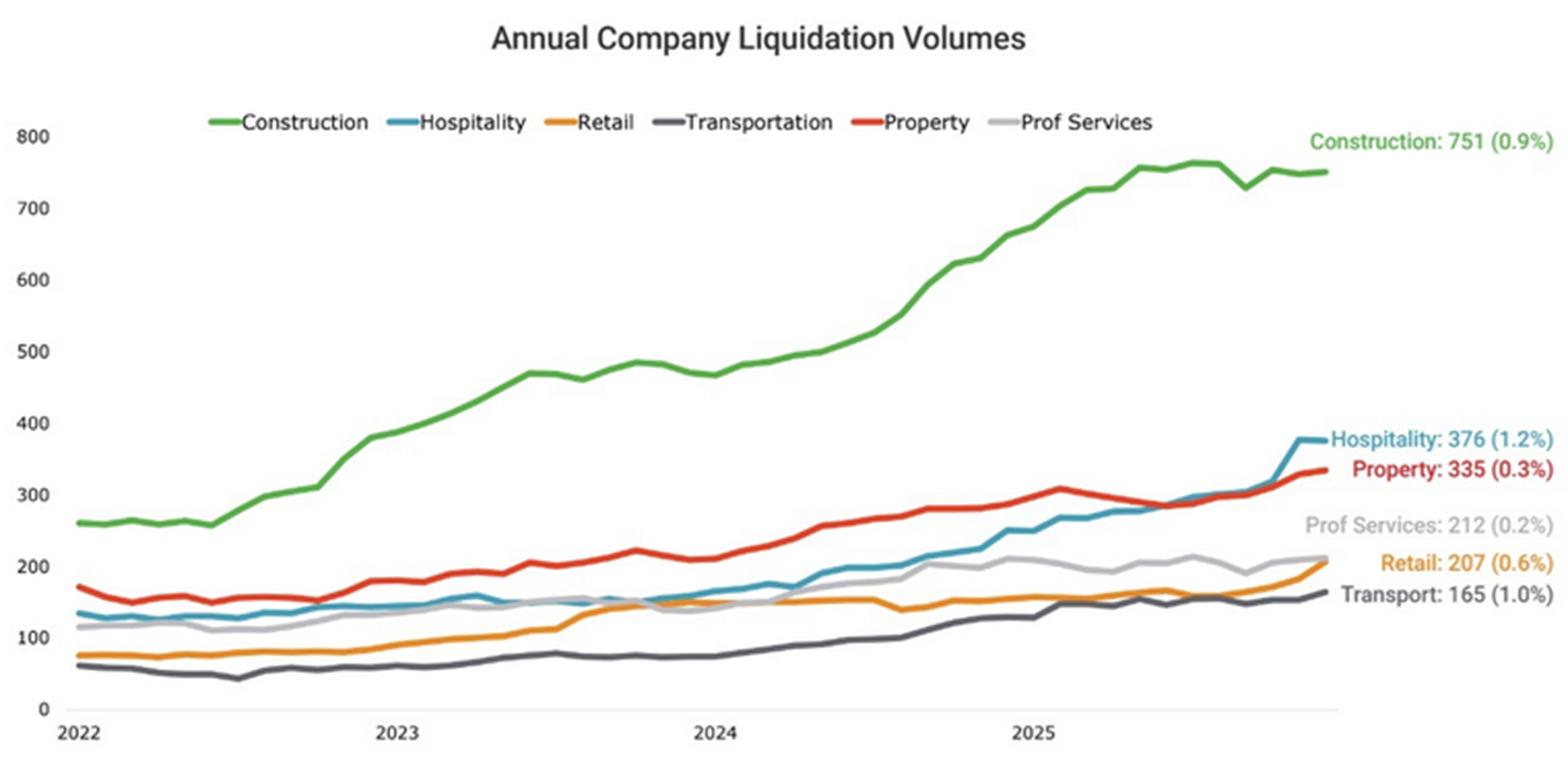

Inland Revenue is working hard to get the overdue tax debt down. However, the economy isn't in great shape, with a recent story pointing out that liquidations have been the highest since the global financial crisis in 2008-2010. The construction sector in particular is struggling.

If you are behind with tax debt contact Inland Revenue

I cannot stress this enough, if you are in trouble with your tax debt, the first and best thing you should do, is to approach Inland Revenue. So long as you are realistic and open with, you will probably find it is prepared to work with you on an instalment plan. And in some cases where the debt is relatively small, say under $20,000, you can set up your own instalment plan, or your tax agent can help you do it.

The key thing is you have got to make the initial approach because Inland Revenue's attitude hardens if it feels that a tax debtor is not making realistic attempts to address the scenario.

The 80:20 rule in reverse

An interesting feature about the composition of tax debt is that although the bulk of tax is paid by the very largest companies in the form of PAYE, GST, and company income tax, the majority of tax debt comes from SMEs, micro-businesses and individuals. As of 30th June 2025, over 527,000 taxpayers owed tax. For many of those small businesses, the owners are under enormous stress and it’s difficult to address the issue of tax debt. Perhaps surprisingly, my experience has been that many clients are relieved when they eventually do contact Inland Revenue as it’s often not as bad as feared and a plan is now in place.

Don’t expect the Election to change anything

We can also expect to see Inland Revenue ramping up activities. I would not be surprised if this year’s Budget has more funds for investigation and debt collection activities on top of the $35 million per annum boost it received in last year’s Budget. And by the way, this will be something that will remain the same even if there's a change in government after the Election. Inland Revenue will still be expected to crank up its enforcement activities.

Cryptoasset investors targeted

On investigations, I'm hearing noises that transfer pricing reviews are increasing, but a key focus area is cryptoassets. Inland Revenue noted in its last annual report that it had several cases going through its dispute process, which involved “tens of millions of dollars”. It seems to be taking a fairly aggressive approach.

A client has shown me a letter where Inland Revenue have said, “if you do not make a voluntary disclosure or contact me directly, I will assume that you have deliberately failed to correctly declare your cryptoasset income.”

The tone of this letter was really quite surprising to me. Generally speaking, when Inland Revenue is considering investigations and audits, it is never as aggressive as that. More often the questions/letters that come in are along the lines of “Are you sure about that? Maybe you might want to check and come back to us.” Whatever Inland Revenue’s tone cryptoasset investors and traders should expect enquiries.

Wrapping, bridging, lending, borrowing and staking cryptoassets

Still on crypto, Inland Revenue has released a 30 pages issues paper for discussion setting out its view on the income tax treatment of wrapping, bridging, lending, borrowing, and staking cryptoassets, or decentralised finance (DeFi) transactions.

The basic position Inland Revenue has adopted with crypto is that it is property, and therefore the general rules apply that the disposals of crypto will be taxable if they were acquired for a main purpose of disposal or as part of a profit-making activity.

The paper refers to increases in crypto arising from DeFi transactions as “rewards”. Inland Revenue's view is these are money's worth and usually taxable when received. The analogy would be these rewards are like a dividend or an interest payment and should therefore be taxed. Submissions on the paper are open until 12th March.

Expect some crypto related court decisions

Last November I discussed the Technical Discussion Summary TDS 25/23 on the taxation of cryptoassets. As previously noted, Inland Revenue is currently involved with several similar cases involving “tens of millions of tax” so I expect some cases to appear in the courts this year perhaps either before the Taxation Review Authority, or the High Court.

As an aside it's worth noting one of the interesting (and I don't think it's entirely healthy to be frank) issues with our tax system at present is that we don't actually get an awful lot of tax cases coming through, partly because the dispute process is designed to try and resolve most issues before they get to court.

But I do wonder if it's gone too far the other way. Supreme Court Justice Susan Glazebrook has publicly remarked on the decline in tax cases in the courts. Is that entirely healthy, given that tax is a fairly litigious topic? It is a little surprising when you step back and reflect that we don't see many tax cases coming through. That said, I expect we will see some crypto related cases this year.

International tax – America goes its own way

Moving on, the year has been quite frantic with international developments. One of the features of the new second Trump administration is its withdrawal from many international agreements, and it has also made it very clear that it will view unfavourably what it regards as discriminatory tax practices.

As a result, the international two-pillar agreement that the OECD/G20 been working on for close to a decade now has hit a big speed bump, with the Americans making it very clear they don't believe or consider that its multinationals (we're talking particularly the tech companies) should be subject to those rules.

Now the end result of that is that there's been a development called the side-by-side package which the OECD released in early January. l It's convoluted as always with international tax, but at the moment, there's only one country that qualifies for the side-by-side system, and you'll not be surprised to hear that's the United States. Basically, the idea is to allow Pillar Two to continue to coexist with the American tax regime and in theory deliver comparable minimum tax outcomes. In theory everyone is still progressing towards the 15% minimum corporate income tax rate globally.

Incidentally, the Pillar Two rules were effective for 2025 from a New Zealand perspective which means some multinationals may be subject to these rules. As I mentioned earlier, there's been reports coming out from the Big Four that more transfer pricing reviews are happening. Anyway, we'll keep our eyes on what's going on in the global tax space. We expect to see more developments in that area. And it'd be interesting to see how Inland Revenue approaches its audit work in relation in this space.

“What's in a name? That which we call a rose by any other name would smell as sweet”

Finally, it's an election year and tax seems set to play a major part of the debate this year. So far Labour has proposed a capital gains tax on residential properties (excluding the family home) and commercial properties.

Meanwhile, echoing Juliet’s question in Romeo and Juliet, a sharp debate broke out last week, in relation to the Government’s gas levy to help pay for the proposed LNG facility in New Plymouth. Is it a tax or “just” a levy? We can expect to see more of this verbal jousting in the months ahead of the election.

Last week, the Finance Minister Nicola Willis was one of the speakers at a two-day economic forum at Waikato University. Interestingly, she brought up the question of tax policy, which is often a matter that's debated at tax conferences although usually it’s the Revenue Minister discussing the topic.

The Finance Minister hasn’t exactly gone outside her lane because tax is a key part of her portfolio, but it is unusual to see her discuss it publicly.

She noted “tax policy certainty needs to span successive governments.” And that's very true. The issue she was driving was a hope that Labour would support the Investment Boost package that was renounced as part of last year's budget.

Investment Boost is an interesting initiative, one of what we call accelerated depreciation, which the OECD suggests we should be doing if we want to boost productivity. It’s an interesting mix of reactions to it, mostly positive.

I've had clients who are in the business financing sector report that it hasn't had the booster effect that they were expecting.

So anyway, the Finance Minister was saying she hopes that Labour in the interests of consistent tax policy would keep Investment Boost. That remains to be seen. It's an election year and to possibly; to borrow a rugby phrase, she's getting her retaliation in first.

A bank taxation review?

In her speech the Finance Minister also raised the question of whether the four main big Australian-owned banks are paying enough tax. This seems a classic example of Bettridge's law of headlines, that is, any headline that ends in a question mark can be answered by the word no. There's a great deal of commentary around how much tax is paid by the big four banks and whether it is appropriate. They seem to have higher margins than their Australian parents and a higher margin compared with many other countries.

Australian introduced its Major Bank Levy in 2017 and there has been a long-running bank levy in the UK. Infamously, as the Green Party pointed out, Margaret Thatcher introduced a bank levy on excessive profits in the early 1980s. Anyway what the Finance Minister has apparently put on the radar is some form of review of the tax treatment or what's happening with the tax and the big four banks. It will be interesting to see what comes out of the review.

Budget date announced

Finally, this year’s Budget will be on Thursday 28th May, a little later than I anticipated. We’ve been told it won’t be a “lolly scramble”, but being an election year, I expect we may see some surprise announcements.

Meanwhile the main themes for the year are set, more Inland Revenue debt recovery and investigation activity, an international tax picture in flux and finally because of the forthcoming election we’re going to be hearing a lot about tax. Whatever eventuates we will keep you up to date with developments.

And on that note, that’s all for this week, I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

3 Comments

Good article thanks Terry. I'm interested in any updates regarding the abatements issue as noted in your previous article here given the implications for families of young kids and the seemingly silly disincentive to work harder and earn more for those in certain income brackets.

Thanks Mr T Baucher for todays article I can easily understand. In the past I have mostly got bogged down in complexities and technical detail so have ended up no wiser from reading them.

So NZ has half a million people owing tax and half a million people in arrears on credit........ but business confidence is high. This doesn't seem to compute

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.