Giant dairy co-operative, Fonterra, has raised its forecast milk price for farmers, paid 40 cents in dividends and increased its full-year forecast earnings.

This is all on top of lifting half-year profits after tax to $750 million from $729 million a year ago.

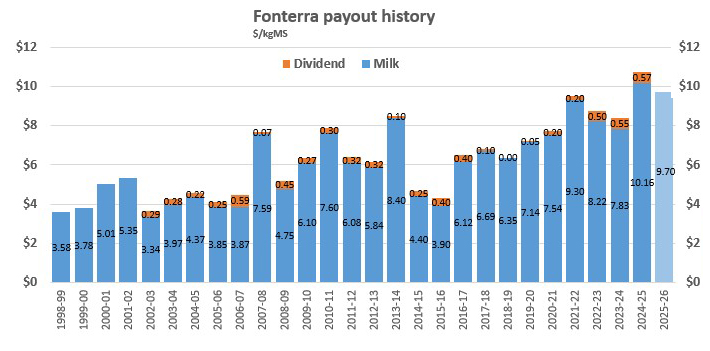

The forecast farmgate milk price is now $9.70 per kilogram of milk solids (midpoint of a $9.40-$10 range), up from a forecast of $9.50 made only last month ($9.20-$9.80 range). If achieved, $9.70 would be the second highest pay out ever behind the $10.16 achieved last year.

The dividend to be paid is made up of 24c ordinary dividend and a 16c 'special dividend' from the Mainland assets, which are in the midst of being sold to French group Lactalis for $4.22 billion. Fonterra says that sale, which is unconditional, is proceeding and expected to be completed by the end of this month.

Previously Fonterra had forecast earnings from continuing operations in the range of 45c to 65c. Its now lifted the bottom of this range and is now targeting 50c to 65c.

In terms of the outlook, Fonterra CEO Miles Hurrell - soon to leave Fonterra - said the conflict in the Middle East "is having an impact on our supply chain and has the potential to increase Fonterra’s inventory levels and costs over the course of the second half of the year. There’s also the potential for further volatility in global commodity prices".

The conflict is a complex and dynamic situation that is changing daily, "but we are confident that we’re on the right track to get product to customers", he said.

"Our business is designed to manage volatility. Our scale and strong relationships with customers and logistics provider Kotahi will help us to navigate through these challenges better than most. With this in mind, we remain focused on delivering on our strategic targets," Hurrell said.

This is the half-year highlights as listed by Fonterra:

- Total Group revenue: NZ $13.9 billion, up by NZ $1.3 billion

- Operating profit: NZ $1,231 million, up from NZ $1,107 million

- Profit after tax: NZ $750 million, up from NZ $729 million

- Earnings per share: 45 cents per share, up from 44 cents last year

- Normalised earnings per share: 51 cents per share, up from 47 cents last year

- Continuing Operations return on capital: 11.2% up from 10.4%

- Interim dividend, fully imputed: 24 cents per share

- Special Mainland dividend, fully imputed: 16 cents per share

- Forecast Farmgate Milk Price range: NZ $9.40 - $10.00 per kgMS, with a midpoint of $9.70 per kgMS

- Forecast milk collections: 1,565m kgMS, up 4%

- FY26 full year forecast earnings range for continuing operations: 50-65 cents per share

This is the full release from Fonterra:

Fonterra Co-operative Group Ltd has today released its FY26 interim results, showing continued momentum in its performance with revenue of $13.9 billion in the first half of the financial year.

Fonterra announced an interim dividend of 24 cents per share, fully imputed from continuing operations and confirmed a special Mainland dividend of 16 cents per share, fully imputed, representing 100% of Mainland Group’s FY26 earnings while under Fonterra ownership.

The Co-op has also lifted its forecast Farmgate Milk Price midpoint for the season from $9.50 per kgMS to $9.70 per kgMS, with the range changing from $9.20 - $9.80 per kgMS to $9.40 - $10.00 per kgMS.

Given the strength of these interim results, and our contracted commitments for the second half of the year, we have also adjusted our full year earnings guidance for continuing operations from 45-65 cents per share to 50-65 cents per share.

CEO Miles Hurrell says these changes to the forecast Farmgate Milk Price and earnings reflect improvement in global commodity prices and the Co-op’s strong underlying margins and cost control, but notes that

significant volatility remains, particularly as the conflict in the Middle East continues. “The underlying performance of Fonterra’s continuing business is stable, allowing the Co-op to return all earnings associated with the Mainland Group business and lift our forecasts for the remainder of the year ahead. Demand for our products is strong, and we’re

focused on our plan to maximise both the Farmgate Milk Price and earnings,” says Mr Hurrell. The record date for the two dividend payments will be 30 March, and the payment date will be 14 April. This is also the date Fonterra is targeting for payment of the $2.00 per share capital return from the Mainland Group divestment, based on the transaction completing at the end of March.

Business performance

Total Group reported operating profit increased to $1,231 million from $1,107

million the year prior. Reported profit after tax is $750 million, equivalent to earnings per share of 45 cents and up on 44 cents last year. When excluding the costs associated with the Consumer divestment, Fonterra’s normalised earnings per share is 51 cents.

The Co-op delivered a Return on Capital of 11.2%, up on this time last year and in line with the target range of 10-12%.

“The first half of the year has been shaped by strong milk flows, with the Co-op collecting record milk volumes in the South Island so far this season. When combined with several adverse weather events, these conditions have put pressure on the operations of all New Zealand milk processors.

"We have been able to navigate through these challenges due to the resilience of our network," says Mr Hurrell. "Our performance shows that we are growing the high-value parts of our business through optimal allocation of milk solids across our product mix, which is driving a strong return on capital for shareholders and unit holders."

Fonterra’s market performance has been strong, with the Ingredients business delivering a return on capital of 11% and Foodservice a return on capital of 12.6%.

These results have been driven by our protein portfolio in the Ingredients channel

and improved pricing in Foodservice to successfully recover the lift in butter and cream input costs seen last year. Mainland Group performance improved during the first half of this year, primarily due to a favourable commodity price cycle.

Progress on strategy

Over the course of FY26, Fonterra has made significant progress on the divestment of its global consumer and associated businesses, Mainland Group, to Lactalis for $4.22 billion. The transaction is unconditional and expected to complete at the end of March 2026.

“Our focus now is firmly on our strategy to grow value for farmers as a global B2B dairy nutrition provider, working closely with customers through our high-performing Ingredients and Foodservice channels.

“The foundation of our Co-op is our New Zealand milk supply. Fonterra has made it easier for new farmer suppliers to join the Co-op and share up over time through changes to our shareholding requirements, with greater flexibility in the level of investment required.

“We are focused on maximising value from farmers’ milk and are building new manufacturing capacity across several New Zealand sites to help meet growing demand for our high-value proteins, butters and creams,” says Mr Hurrell.

Projects underway include:

- Studholme - construction of the new advanced protein hub is now complete, with first trial products off the line in February 2026.

- Clandeboye - commenced build of our butter plant expansion in January 2026, with product expected off the line in April 2027.

- Edendale – construction underway of new UHT cream plant and remains on track for first products to come off the line in late 2026.

- Edgecumbe – today announcing a $35 million investment in expanding our pastry butter sheet line, to support continued demand through Foodservice for butter products. Site works began in March 2026, with product off the line expected in April 2027.

In addition, the Co-op's decarbonisation

programme continues across key sites at Whareroa, Edgecumbe, Waitoa, and Edendale to help secure energy supply, reduce emissions, and support future processing growth. Underpinning our business operations is the Co-op's Enterprise Resource Planning system1

implementation, which has been deployed successfully at our first three locations. The five-year programme remains on track and on budget and is expected to wrap up in late 2028 with spend peaking across FY26 and FY27. Outlook

Looking ahead, the conflict in the Middle East is having an impact on our supply chain and has the potential to increase Fonterra’s inventory levels and costs over the course of the second half of the year. There’s also the potential for further volatility in global commodity prices.

“The conflict is a complex and dynamic situation that is changing daily, but we are confident that we’re on the right track to get product to customers.

“Our business is designed to manage volatility.

Our scale and strong relationships with customers and logistics provider Kotahi will help us to navigate through these challenges better than most. With this in mind, we remain focused on delivering on our strategic targets,” says Mr Hurrell.

This is the dairy industry payout history.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.