The COVID-19 health crisis, which morphed into an economic crisis, is not at this stage showing signs of turning into a credit crisis.

The string of interventions the Reserve Bank (RBNZ) has made in the financial system has left banks cashed-up and ready to lend.

Yet with businesses and households being cautious about borrowing, and banks needing to be sure borrowers can repay their loans, a lot of that cash is sitting there, waiting to be deployed.

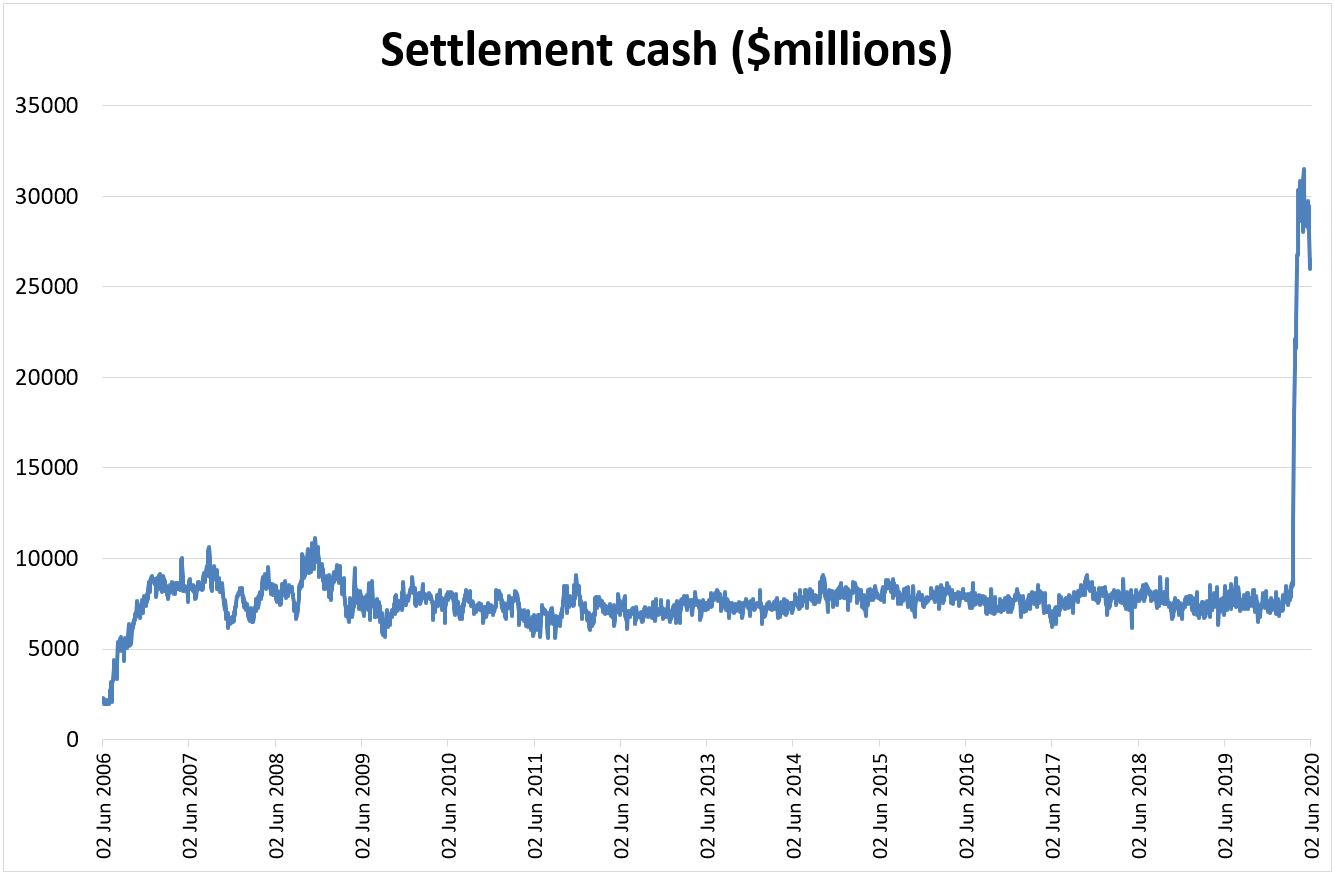

In fact, the amount of settlement cash held by the RBNZ has increased more than three-fold since before COVID-19.

As at Tuesday, the value of settlement cash, or the value of cash effectively in the RBNZ’s own bank account, sat at $27 billion. Settlement cash hit a record high of nearly $32 billion in May - a huge jump from the $7 billion to $8 billion mark it usually hovers around, and the $11 billion mark reached at the 2008 Global Financial Crisis (GFC).

RBNZ data

RBNZ deputy governor Geoff Bascand said retail banks have had a lot of money flow into their own accounts, so haven’t really needed to borrow from the RBNZ.

Banks’ accounts have had a boost as the RBNZ has printed money to buy mainly New Zealand Government Bonds from bondholders including banks.

It has committed to buying up to $60 billion of these bonds in the next year through its quantitative easing (QE) or Large Scale Asset Purchase programme. To date, the RBNZ has bought nearly $15 billion of bonds under the programme.

The Government has also effectively injected $11 billion into banks’ accounts by paying businesses the wage subsidy.

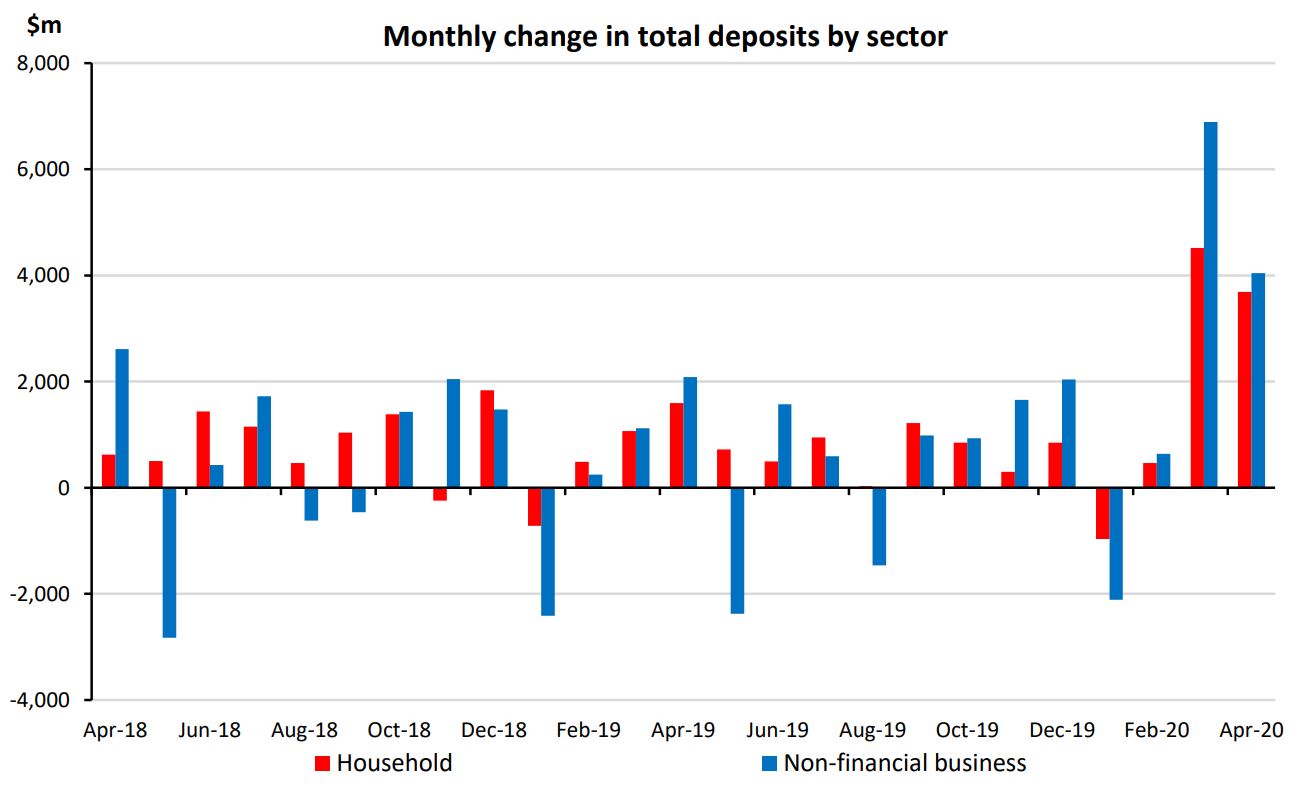

Furthermore, nervous investors have opted to put their money in the bank rather than invest it elsewhere - once again boosting the amount of cash held by banks and reducing the need for them to borrow from the RBNZ.

RBNZ data

Kiwibank treasurer Tim Main acknowledged, “There’s been a bit of a switch in flows - more money in, less money out. We are holding more cash than we would normally hold.

“Over time, we do expect that to eventually flow out as the economy recovers and people are more willing to take out loans.”

Bascand said the RBNZ was at the onset of COVID-19 worried about banks’ liquidity positions, so made a lot of liquidity available to them.

For example, it offered them loans with terms of up to a year through a Term Auction Facility similar to that it used in the GFC.

“But then in fact what has happened is that they had actually quite strong deposit growth and very little credit demand for a period of time. So actually, banks have become quite cashed-up… the amount of liquidity is very strong,” Bascand said.

Accordingly, banks have only drawn down $1.2 billion via the RBNZ’s Term Auction Facility.

“Hopefully we’ll see credit demand pick up over the next few months; we’ll see those wage subsidies finish; we’ll see a bit of a wind down in the deposit story,” Bascand said.

He was pleased the RBNZ had so much settlement cash, saying “we’re allowing it to increase, or increasing it directly, because we want short-term interest rates to be lower”.

Main said, “The whole theory of QE is that it pushes interest rates so low that it pushes banks to change their asset allocations towards higher risks investments…

“We’ve got enough bonds ourselves. Everyone I think has plenty of liquid assets. We would just really like to see credit growth increase so that we can reallocate some of that cash into higher earning lending assets.”

Main said Kiwibank wasn’t “deliberately holding back money”.

“We’re still living with our [responsible] lending requirements. And that hasn’t changed. It’s more a demand problem in that there’s a reluctance by people to commit right now to lending because of the uncertain employment conditions and economic outlook.”

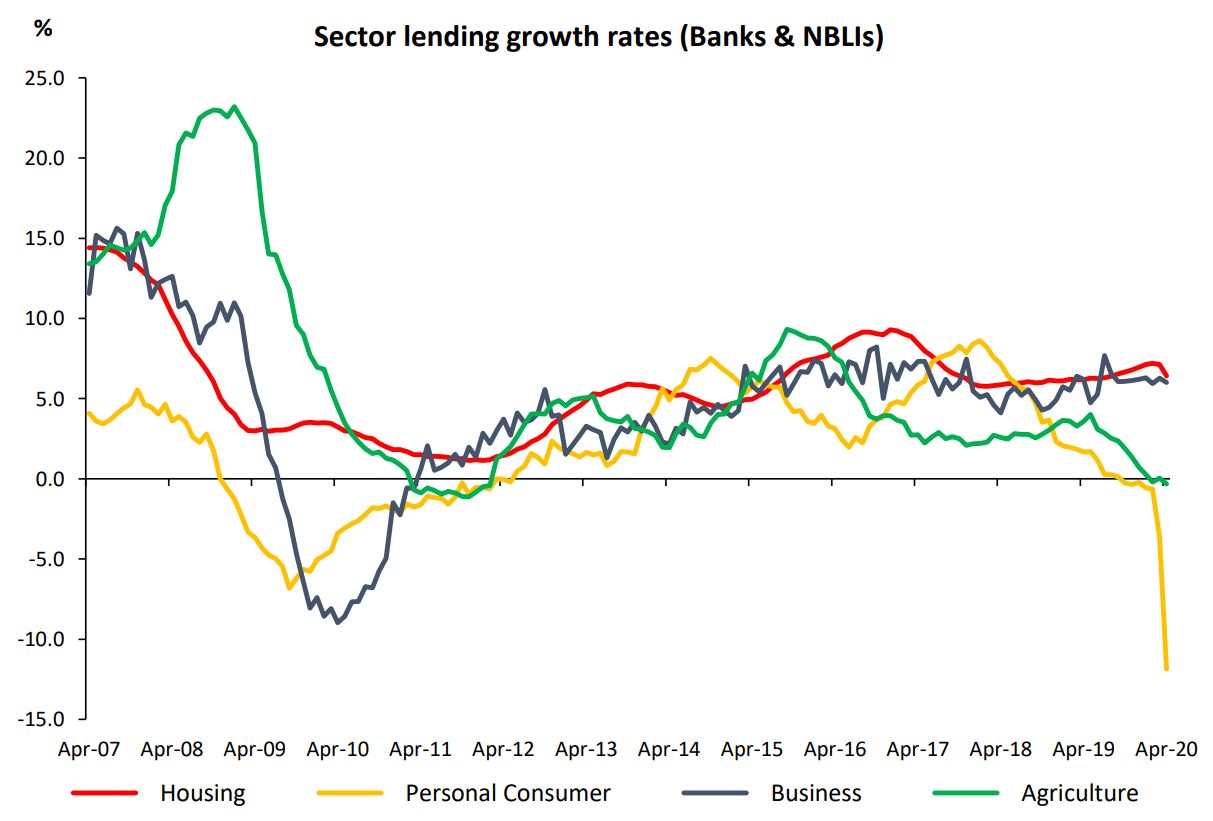

RBNZ data

Bascand said the process of withdrawing cash from the system was one “we have ahead of us a long time out, when we do face the pleasant challenge of having to raise interest rates again or slow the economy”.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

41 Comments

“Hopefully we’ll see credit demand pick up over the next few months; we’ll see those wage subsidies finish; we’ll see a bit of a wind-down in the deposit story,” Bascand said."

Way to go, Geoff! More debt and less household income.

That'll spur those animal spirits on.

(Did these guys all do the same Harvard course on 'How to Run an Economy' or something? Oh, that's right! They did)

'How to Run an Economy'

They missed the 'i' in ruin.

They obviously skipped Clay Christensen's very worthy course: how MBAs and overfinancialisation results in governance by ratios and loss of innovation / productivity.

@bw ....dont worry ..........credit demand will NOT pick up anytime soon, even if money was free . Many of those of us able to borrow and spend don't want for anything , and many of the rest are a poor credit risk.

We are a professional practice, all the partners are Boomers .

We had a partners meeting on Monday at one's home and ALL non-contracted spending is frozen for the rest of 2020.

Budgeted Capex on computers and software , new flooring and some fitout work is cancelled . Motor vehicles are to be sold to staff using them for book value, we will no longer provide Company cars . They were never part of our employment agreements , and specifically excluded . We have simply condoned the private use of fleet cars .

In fact we are going further to cut operating costs dramatically, including :-

Negotiate a new lease with our landlord

Stop all paper consumption and reduce consumables spend by at least 50 %

Reduce staffing

Exit our vehicle fleet leases , and sell the paid up vehicles to the users ( the fleet leases have always been a waste in my view ) . We will no longer be providing company vehicles .

There is evidence that many of our clients are , or are about to become, financially stressed .

We need to prepare for this new normal where we expect revenues to fall , by having plans in place to ride the storm .

And that is not just one company.

(Late PS)

So, (Geoff), you’re convinced that low rates are a powerful stimulus. You believe, like any good standing Economist, that reduced interest costs can only lead to more credit across-the-board. That with more credit will emerge more economic activity and, better, activity of the inflationary variety. A recovery, in other words.

What happens, however, if you also believe you’ve been responsible for bringing rates down all across the curve…and then no recovery. Just as the textbook said, lower yields as far as the eye can see. And yet, nothing.

Any normal, rational person requiring nothing more than common sense would see this situation and realize the faulty premise; and the stark implications, therefore, needed to rectify the matter (that Economics might need to just start over). Maybe low rates aren’t always stimulus?

Economists have constructed “laws” out of their dogma, therefore they instead seek out plausible-sounding answers by diving back into ceteris paribus. They are absolutely certain, despite the mountains of contrary planetary evidence, that low rates are indeed the trick – but, taking things one step forward, the world won’t always be attached to those low rates.

https://alhambrapartners.com/2020/06/03/from-qe-to-eternity-the-backdoo…

Banks’ accounts have had a boost as the RBNZ has printed money to buy mainly New Zealand Government Bonds from bondholders including banks.

It has committed to buying up to $60 billion of these bonds in the next year through its quantitative easing (QE) or Large Scale Asset Purchase programme. To date, the RBNZ has bought nearly $15 billion of bonds under the programme.

QE, the wage subsidy and nervous investors see banks sit with more cash to lend, than borrowers to lend to

I think not in respect of QE!!!

Three structural features of monetary systems form the starting point for this paper. They include (1) a two-layer structure comprising a private sector agent deposit system with commercial banks, parallel to a commercial bank deposit (reserve) system with central banks, with the two being separate and not allowing transfers between the two, that is, reserves cannot be “lent out” to the private sector (Sheard 2013); (2) the fact that money is created upon the creation of bank loans (Werner 2014/16) while repayment implies money destruction, both of which are an accounting reality, and implying that banks would better not be called “intermediaries”; and (3) the fact that the money stock is endogenously and elastically driven by demand and constrained loosely by regulation. The constraints to the provision of new credit include capital regulation, banks’ conditionality on an incremental profit prospect, and, eventually, demand (McLeay et al. 2014)1. Link

A recent Bloomberg article described central bank easing with the phrase “pumping money into the economy.” That’s a misconception. Monetary easing is actually an asset swap. The public was holding savings in one form, and now it holds it in another. The Fed buys Treasury securities from the public, and replaces them with currency and bank reserves (base money) that someone has to hold, at every point in time, until the Fed sells its bonds and retires the cash. All monetary policy does is to change the mix of government obligations held by the public. Only fiscal policy – specifically deficit spending – changes the total amount of those obligations.Link

I'm not sure we can write off a credit crisis just yet. Just because fewer borrowers are willing to borrow right now, doesn't say anything about banks willingness to lend now or in the near future.

I think you will find that the 'social contract' of the holy nexus between commercial banks and the central banks / govts means that credit should be delivered to the great unwashed to keep them under control. That's their obligation.

I don't think so - only the creditworthy are eligible for bank loans to engage in leveraged asset speculation activities.- solid income and preferably assets in addition to that being purchased with loan funds, are often a prerequisite.

I don't think so - only the creditworthy are eligible for bank loans to engage in leveraged asset speculation activities.- solid income and preferably assets in addition to that being purchased with loan funds, are often a prerequisite.

OK, that make sense; but my point is that the ruling elite want that speculation to be happening. They don't want funding to be idle. And if the definition of creditworthy applies to fewer brorrowers now than 6 months ago, they may possibly want the 'creditworthy' to speculate in greater volume.

Like when the OCR was being cut but only a fraction of each cut was being passed on?

OCR cuts are passed on to customers in varying degrees but normally a majority is passed, see;

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

OCR cuts do what the RBNZ expects, see:

https://www.interest.co.nz/bonds/101245/rbnz-modelling-finds-economys-r…

With strong kiwi dollar, and money to borrow, RBNZ could go into the negative range sooner than the schedule.

Strong NZD? Slightly less weak, maybe.

In other news, down is up, black is white, and you can get away with whatever you desire.

May be is not a Credit Crisis but will definitely lead to Credit Crisis along with many other crisis.

Yet......

What the RBNZ forget to tell everyone on purpose is that this new phase QE is whats called in simple terms, waking up one morning and while having a coffee decide to go to work at the RBNZ and make up new amounts of money to whatever volume they chose and then deposit it with the banks. Of course the banks are flush with cash because the government is filling peoples pockets with grants etc and buying bonds. The OCR will be going negative about September I believe it has too and interest rates will have a 1 in them by December and stay low for 10 years. The government cant raise the OCR if it does its doubling its debt ratio its at .25% so if it raised the OCR to .50% its doubled so this will never happen for years so there is only one way for it to go and thats down baby.

Why isn't there a credit crisis? Well nobody had to pay interest on loans if they couldn't and the government paid everyones wages...

Free markets are a thing of the past. Never worry about risk again people because there is none - hence risk free rates are near zero and governments will come to the rescue if there is ever any downside. Get reckless because you can never be burnt. And if you're prudent, well make sure you keep paying your PAYE and RWT so the government (or you the tax payer) can carry the risk of the risk takers.

Totally agree with you IO ( for once lol)

Its an unfortunate, unethical and immoral environment we've created.

Comment of the day mate!

I find myself always in strong agreement with you, IO.

I can only add that it is frankly quite incredible that the powers to be seem to be so ignorant or simply culpably neglectful of the catastrophic longer term impacts of such mis-pricing of risk and killing of any price-signal.

The time there was such an environment was in Soviet Russia. And we all know what sort of economy resulted from it.

Thanks for this article Jenée, about time someone focused on the increasing credit available. I would love you to delve further in to the consequences on the NZ economy, housing, business of this excess of funds

Explanation: defaults prev by printing and gov largesse worldwide so now is no consequence to stupid investor risk taking. Plus can’t get folk to spend. 2008 plus

Banks do not lend out the reserves that they hold, banks create all of the money that they lend. They are not reserve constrained but capital constrained in the amount of lending that they can do.

This Bank of England bulletin from 2014 explains how banking operates, and how banks create money.

https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

Thanks for the link.

Adrian Orr is making a bloody mistake ...........and I suspect he knows it .

He knows all too well from the Japanese experiment , that reducing interest rates to zero does NOT stimulate spending .

Perversely , it has the reverse effect , it increases the propensity to pay down debt and save even more.

As an example , I personally have more disposable income that ever before in my entire life , and I am simply putting it away .

Why you may ask ?

Well in light of uncertainty around interest rates , I am going to need way more capital for my retirement than if my capital was generating some yield in excess of inflation and tax .

Basically I will be living off my capital from day 1 when I stop working , because interest earned will be close to zero .

So the net effect is I am saving more cash than ever before, and I happen to know I am not the only person doing this

Bingo - liquidity trap. Monetary policy no longer stimulates the economy. Further interest rates drops will only make our financial position worse. But if we raise rates our ponzi will collapse.

Orr has been fenced in by a Bollard before him, and by reckless speculators infesting NZ.

Yip and I think Orr knows that - I think he's known that from the start. I was listening closely when he was saying things like 'we need to stop this short term thinking'. But I guess like J Powell, he realises that it is now too late, the system has too much momentum to reverse out of, or if you did try to reverse out of it, you'd need to cause quite a lot of short term pain (which it appears there is no appetite for - it would appear everyone would rather just head into a massive train smash together sometime in the future, but probably inside the next 10 years). Watching the Fed try to raise rates a few years back and it couldn't, they can't. But at some point we will need to and something will have to give, probably asset prices and debt defaults.

They're all hoping the can offload their portfolios first, perhaps.

In Japan household income deflated at a faster rate than their prices. So in reality their QE has been inflationary (as with diminishing income and consumption, surely priced should have fallen in line with income).

I am not sure if Japanese people are saving more. They are earning less and less, while prices are not reducing as fast, therefore they have less to save. I am no expert on Japan economy, but it does look like the QE money is not ending up in household pockets. It ends up with corporate and investors who cannot do much with it (as the household income prospect is gloomy, what can they invest in?).

Jenee , please change the teaser headline to........... " Why the Covid crisis is not a credit crisis ......... just yet "

Its not a credit crisis , but it looks like it may become one as we tumble into a severe recession where both sovereign and private debt defaults rocket , banks write off bad debts thus wreaking havoc with their Balance Sheets and stability is threatened

A government deficit equals a private sector surplus, that is what allows the private sector to pay down its own debt and increase savings. (Sectoral Balances). Money is either created by the banks or by the government only, when we have a current account deficit. Not all sectors can be in surplus together.

Hold on a moment ..............a Government deficit = a Private sector surplus ?

I dont see that at all .

I have tried to understand this idea , but I cant figure it out

The rate we are going we are all going to be in deficit

There is plenty of information online about sectoral balances, here is a link here.

https://gimms.org.uk/fact-sheets/sectoral-balances/

You are assuming that all the deficit is spent to buy locally produced stuff. No mate, the other side of the deficit can be private sectors of other countries as we give money people to consume fuel (imported) food (some imported) cars (imported) medical supplies (imported) etc etc.

The foreign sector is one of the three sectors accounted for in sectoral balances. We run a current account deficit ( foreign sector surplus). All financial flows must net to zero ,it is a simple accounting identity. Look it up.

Not yet a credit crisis, in NZ is more accurate.

Remember there is a world banking system and its in hock to its eyeballs to third world in USD loans and corporate debt. What do you think will happen to all that debt when 3rd world begins defaulting: many of the biggest banks will implode. Central banks like Fed will not have enough to stop that. Central banks hold up equity markets, they cannot save the bond market

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.