The Reserve Bank (RBNZ) estimates the reintroduction of high loan-to-value ratio (LVR) restrictions will shave between one and four percentage points off house price inflation over the next year.

So, if house prices were to increase by say 20% without LVR restrictions, they might increase by between 16% and 19% with LVR restrictions in place.

The RBNZ included these estimates, based on research it did in 2018, in its just-published Regulatory Impact Assessment on the reinstatement of LVR restrictions.

The RBNZ last week announced that from March 1, at least 80% of new bank lending to owner-occupiers will need to go to borrowers with deposits of at least 20%.

Meanwhile, at least 95% of new bank lending to residential property investors will need to go to borrowers with deposits of at least 30%.

From May 1, this minimum for investors will be bumped up to 40% - a tougher restriction than was in place before the RBNZ removed LVR restrictions from May 2020.

The RBNZ said that while LVRs should dampen house price growth over about a year, addressing longer-term pressures on the housing market are beyond the scope of its macro-prudential tools.

The RBNZ stressed it's reinstating LVR restrictions to support financial stability, not cool the housing market.

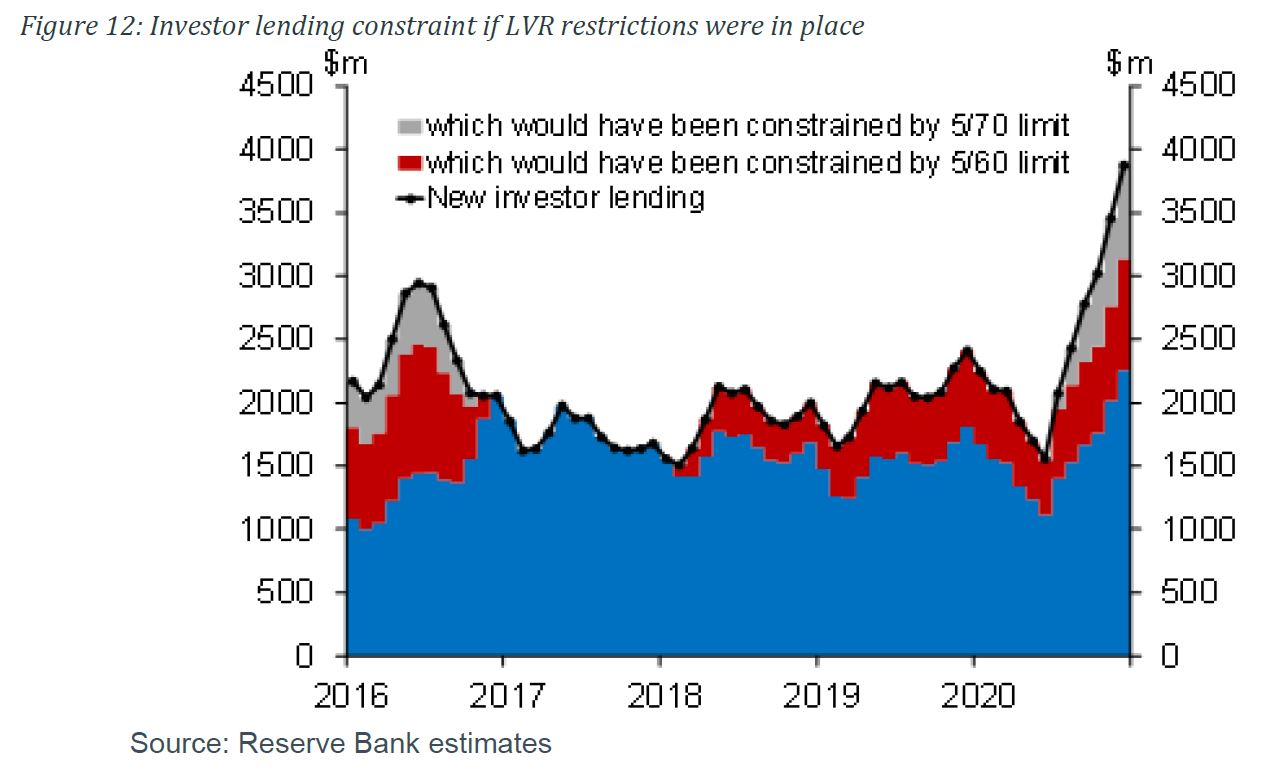

Keeping LVRs in place could’ve reduced investor lending by 15%

The RBNZ expected LVR restrictions to have the greatest impact on investors.

Had it not removed restrictions last year, it believed bank lending to investors could've been 15% lower. Had the tougher 40% deposit requirement been in place, it estimated lending could've been 40% lower.

The RBNZ cautioned: "This is likely to be an over estimate of the true impact, since some lending would have moved to ‘compliant’ LVR buckets (e.g. via investors increasing cash deposits and/or purchasing less expensive properties) and some lending would have been exempt from the restrictions.

"However, it gives an indication of the potential impact of reinstating LVR restrictions on investor lending flows going forward."

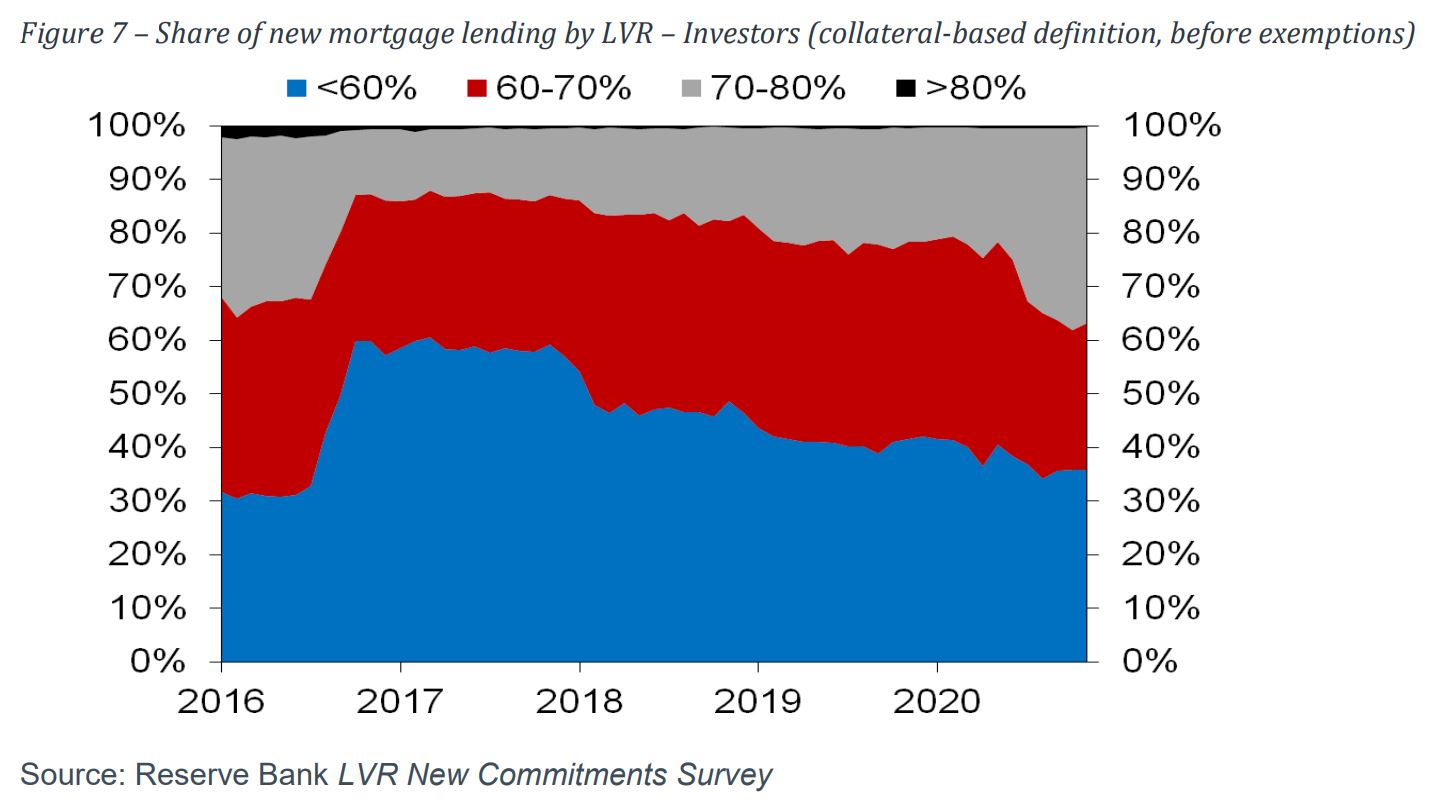

Looking at changes to high-risk lending, the share of investor lending to borrowers with deposits of less than 30% increased to 35% after LVR restrictions were removed last year, from around 15% (see the increase of the grey area in the graph below).

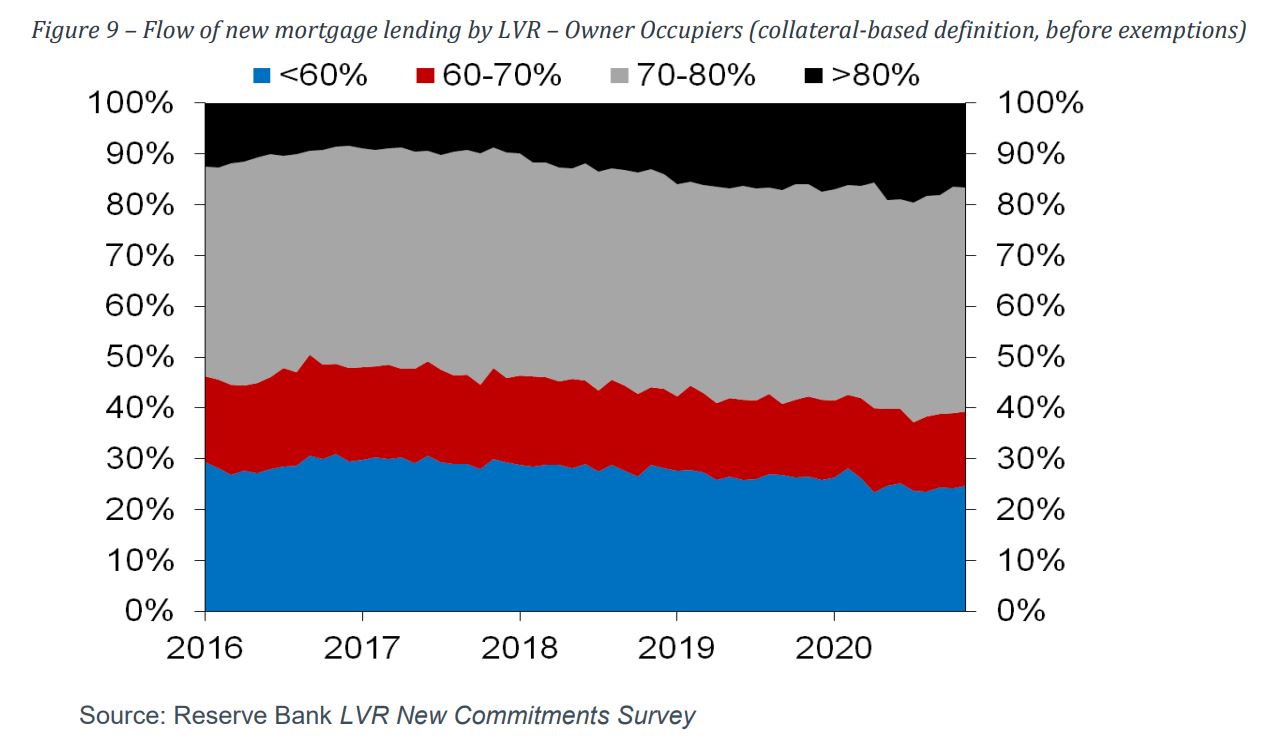

Owner-occupiers relatively unaffected

The RBNZ expected the reinstatement of LVR restrictions to have no effect on owner-occupiers.

It noted banks generally kept within previous limits without being required to do so by their regulator.

It said reimposing restrictions would keep the level of high-LVR, or high-risk, lending to owner-occupiers stable.

First-home buyers don't need exemptions

The RBNZ noted that during its consultation some submitters requested looser LVR restrictions for first-home buyers.

It overlooked this suggestion, pointing out first-home buyers already make up the majority of the 20% of owner-occupier lending banks are allowed to provide to borrowers with deposits of less than 20%.

The RBNZ worried this portion would grow, increasing risks to financial stability, if there was a first-home buyer exemption.

What’s more, it noted there are already exemptions for new builds and Kāinga Ora’s First Home Loans scheme, which enables eligible first-home buyers to secure loans with small deposits.

Investors pose the highest risk

The RBNZ summarised its position: “We are concerned at the recent rapid rise in house price inflation combined with growth in high-LVR lending, particularly to investors.

“If these trends continue, there is an increasing risk of a sharp correction in the housing market, which could be exacerbated by a ‘fire sale’ dynamic whereby highly leveraged borrowers default and/or sell property to raise capital, driving prices down further.

“International evidence suggests that highly-leveraged investors - particularly ‘late stage’ entrants to the property market - play an outsize role in both the ‘boom’ and ‘bust’ phases of housing market cycles.

“These developments also need to be considered against the background of continued economic uncertainty due to COVID-19. While New Zealand’s economy is currently performing much better than expected, if there were another outbreak of the virus requiring further lockdowns, the situation could deteriorate quickly - putting highly leveraged borrowers under significant financial pressure.

“We also note that in the absence of LVR restrictions, competitive dynamics could drive banks with more conservative lending policies to relax these in order to maintain market share, leading to a self-reinforcing cycle of increased risk.

“Prior to our announcement in November that we would be consulting on reinstating LVR restrictions, we saw divergence between banks with some banks remaining within the previous speed limits while others significantly increased their high-LVR lending shares.”

Banks can justify reining themselves in if their competitors are made to do the same

The RBNZ said all respondents to its consultation supported reinstating LVR restrictions in some form (aside from one submitter whose view was unclear).

Around half of respondents said restrictions on investors should be tougher than the restrictions that were in place last year.

RBNZ Deputy Governor Geoff Bascand, at a Finance and Expenditure Committee meeting last week, told Members of Parliament he didn’t regret removing LVR restrictions last year.

The RBNZ reiterated its thinking in its Regulatory Impact Assessment: “The removal aimed to ensure that banks continued to provide support to borrowers against a backdrop of uncertainty, and continued to provide access to credit for credit-worthy borrowers.

“Moreover, lifting the LVR restrictions removed a risk these might discourage banks from offering mortgage deferrals to their customers.”

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

100 Comments

Aware of house price jumping by 20% to 50% annually still RBNZ is and was slow to act unlike last year in April when just the fear of panademic affecting the house price growth prompted them to jump instantly and than think.

This shows the mindset and intent of RBNZ and Government- still waiting from government of measures to control the ponzi specially now when house prices are going up in multiple on a weekly basis.

Exactly. They couldn't be any more obvious

I sorry, I can't give you any meaningful action on the housing crisis that we have made worse. The best I can do is tampons.

Aroha.

Team of five million.

Free tampons.

Good for nose bleeds from excessive banging of heads against walls and facepalming.

Nzdn...if you venture into West Akld a tampon might come in handy.....they are one of the best things to plug a bullet hole with.

The tampon story did the rounds on Reddit and the comments about Jacinda are enough to make you vomit. The international audience have no idea of the her policies, and even less about her failed policies. Every now and then you see a comment from a Kiwi pointing out the increasing inequality, housing crisis, child poverty, domestic abuse and suicide rates. But they're drowned about by hundreds of "Jacinda for world PM!" and "I love her she's great!".

Her PR team are earning their keep. Though less so with those who matter.

Truly sickening...

Might be time to build a Jacinda meme generator to help get the facts out.

Brainwashed en masse

There was a similar phenomenon with John Key initially - "everyday bloke" (multi-millionaire lol), good to have a yarn to at a BBQ etc. Jacinda - Nice and caring, compassionate and will listen to people etc.

Both apparently too gutless to actually do what's right and address the major issues, yet somehow the public votes for these personalities. Just like John, I'm sure the gloss with come off Jacinda if inequality continues to increase and more of the young are shut out of any future in NZ.

'Hospital at the bottom of the cliff' policy, same goes for lunch in schools. Why are we even at that stage to start with?

Actually, I think lunches in schools is a good idea. School lunches are a nightmare for working parents and many kids get nothing or rubbish. My tax dollars going on school lunches is fine with me, as long it comes off the accommodation supplement, which has simply jacked up rents. What really irks me is schools providing breakfast. Any parent who can't make toast or a bowl of weetbix is not fit for purpose. Breakfast is the easiest and cheapest meal of the whole day.

Agreed - school lunches to me seem like a great idea just from the perspective of efficiency. It's nuts that parents make individual lunches when it would be so much more efficient to prepare them in bulk. I don't think breakfast is such a bad idea though - for a lot of people it wouldn't be the prep that's a problem, but the time crunch. Especially if you have a long commute.

Yeah it's good, but why is the Government in a position where they need to supply lunches? Shouldn't they focus on the cause? It seems like a band aid on a worsening situation.

'Shouldn't they focus on the cause' is code for parent-blaming, then doing nothing. The 'cause' is 30 years of the neoliberal marginalisation of the bottom third of society that began with Ruthanasia. Part of the solution will be implementing all the recommendations of the Welfare Expert Advisory Group. Ultimately the gap between rich and poor must be narrowed by taxing wealth, especially landed wealth, rather than income and consumption, and using those taxes for wraparound social security.

In the meantime, school-based, state-provided, free, healthy breakfasts and lunches for all kids is a must, not only on school days, but for those who need it, during weekends and holidays as well.

Sounds a bit extreme, comrade.

How about we just remove them from their crappy parents and put them up for adoption to good homes? Far cheaper. And we would stop the cycle of intergenerational benefit abuse.

I work and love providing healthy lunches for my son (he's put them together in his lunchbox since he was little - independance). School lunches are just another feel good tactic and way to 'create jobs' and dependance

Why do so many schools around the world provide school lunches?

Because parents wanting to spend their benefit money on drugs, alcohol and gambling is a world wide problem. The real solution is not paying these people in cash but vouchers for the supermarket.

The world media latching on the fluff pieces is understandable. Its the local media that are sickening ones. When she ruled out capital gains taxes based on having that policy during the years they didn't get in, nothing but crickets from the media. Did they rule out all their other policies from those years too or just the one they didn't want to do once in power?

PMs seem to get an easy ride in NZ. Key had a fairly easy ride too.

Maybe it's because they are generally likeable and popular.

Doesn't matter if their policies suck.

And a new public holiday. Dont forget that!

No amount of sense or logic will help as both reserve bank as well as Jacinda Arden wants ponzi to continue.

They all are too smart and knows when to switch on their Dementia and mute mode. Thick Skin @%$

"The RBNZ said that ... addressing longer-term pressures on the housing market are beyond the scope of its macro-prudential tools."

All of this "It's not my problem, it's yours" is rubbish. For all intents and purposes the Government is the RBNZ and visa-versa. Anyone who thinks they are "arm's length", independent institutions is being simplistic.

The RBNZ does have the macro-prudential tools at its disposal, even if they are in the Government's toolbag. It doesn't matter who has the hammer at any one time, but that they have one - and that's the real problem. They both think the other one will use it, so it's left lying idle on the bench.

And of course, the real problem is that they have both been told by Powers far bigger than them that "they are not to touch that hammer, or else". What was implied to NZ all those years back? "Let our battleships in to your ports, or we'll blow your currency out of the water", and that will still apply today.

The only things to do for those softy Kiwis? is just waves upon waves of essential workers strike, in every corner - Then magically? you'll see those; rent freeze bill, xyz bill to control this madness. So far? it's about keeping the lid for painful few (as so they/govt thought) - Look at other binge; Nicotine, Alcohol, Gambling.. it's all about? vested interest & introduce 'delay=time=money' the last one? money to flow.. well basically to the clever OZ Banks for sure, in case of anyone blinks? - region down, no work, can't pay rent, no wowies; hand-out, subsidy.... straight to rental, landlord mortgage payment.... voila.. Banks! - in gambling/casino, the house is always win, same with Banks, they always .. win! - bankrupt you said? - well even it's so then govt will bail them out, UBR etc.

The govt can change the legislation governing the Reserve Bank.

They can...if theyre willing to row against the tide....do you think they are keen to risk their preferential access to capital markets? I very much doubt it, and the RBNZ have the same problem....they may be central bankers with a conscience but they are central bankers with sweet FA clout.

.

The NZ dollar really is a shitcoin with these simpletons calling the shots.

There is a simple message for the Government here: ban all bank lending to property investors wanting to buy existing homes, and encourage those investors to build new houses. Don't waste time fiddling with LVRs.

Saturday, 20 February: Stuff's Janine Starks gets it: https://www.stuff.co.nz/business/opinion-analysis/300233796/investor-ba…

On the contrary, you can rely on the government to continue pumping our property bubble (also known as NZ's economy).

INZ has clearly been a major party in these efforts. The tens of thousands of multi-year work visas handed to cleaners and kitchen-hands since the lockdowns to keep wages low and demand for accommodation elevated across the country.

The latest is further kicking the can down the road to delay the exodus of thousands of tourists from NZ.

We have also listened to New Zealand’s business sector, including tourism ventures, which say foreign visitors who are still here can help our local economies .

Has the 'business sector' ever stopped calling the shots on migration in this country?

https://www.stuff.co.nz/travel/124299668/covid19-tourists-to-get-two-mo…

Advisor.. exactly right. Time to force businesses to pay what they need to in order to get Kiwi staff.

Building a new home $ 85,000.00 GST.......

If Cindy is motivated to create new rental dwelling then perhaps look at this also ?

(Fat Chance).

Well you know, if they took away GST on new builds do you really think the price will go down?

Developers need lending to buy the existing home, put a bulldozer thru it, and replace it with 3+ new houses.. how does your plan work with that?

Where will all the renters live if a rental cannot be sold to another landlord? Are we giving them all free money for house deposits so they can buy them? And who is going to want to rent a brand new home to the solo mum with 6 kids and a gang member boyfriend? New homes are more expensive than existing ones, so rents will skyrocket. You must work for the Labour Govt because this sounds like yet another plan to reduce the supply of rental housing and force the price of rents up, that the Labour Govt is so good at.

So makes a marginal difference. Still, better than nothing I guess.

But just to make sure there were no unintended consequences, and any price falls, following all of that research we cut the OCR in 2019 and have dropped it by 150bps since 2018, or a reduction of 90 percent, giving the same investors significantly larger deposits by default.

The RBNZ reiterated its thinking in its Regulatory Impact Assessment: “The removal aimed to ensure that banks continued to provide support to ponzi-pushers against a backdrop of the super leveraged toxic asset pyramid, and continued to provide access to credit for credit-worthy parasites

Beautifully written, I agree 100%.

Did I see that ASB reversed their investor LVR decision?

For new builds.

Ah ok. Thanks.

Some of their language, "exacerbated by a fire sale dynamic", in particular, hints at what I have thought (and said) for a while. The powers that be are very worried (and rightly so IMO) that a (not too worrying) drop of 15% or 20% would be more likely than not to feed on itself and quite likely to cause a much bigger drop. My guess is that if we see a drop of 15% then it is better than even money that the drop ends up to be 35%+ before things trend upwards again.

This would put enormous stress on our financial system especially the banks and I think this is why the decision makers are becoming so concerned. I believe they think the only way to prevent the likelihood of a huge correction is to try to prevent even a small downturn. I am not saying we will see that initial drop, what I am saying is that if we do, LOOK OUT!

Agree, but the thing is that they've stoked the fire in the property market for over a decade with low interest rates, banks risk weightings favouring property, easy credit etc and made that scenario more dangerous as a result. Now their solution to mitigate that scenario is more of the same?

You see the same idiotic behaviour with forest management.

They prevent all the small fires for years and end up with the mother of all fires down the track.

Great analogy.

And the long term answer is not:

"Let's make the problem worse"

Which is exactly what increasing the leverage needed to undertake any property transaction is doing

It's not the cost of finance (the interest rate; the LVR or the DTI) that matters but the size of the debt.

Property Bubbles have burst before. Yes, they hurt, but it's not the End of Civilisation as we know it!

The tragedy of all of this is that they knew/know what they were doing; did it anyway and hoped for a solution to magically arrive.

In the absence of their hope being justified is their acceptance of the inevitable (your, 'Look out!") and their giving our populations a bit more time in the economic sunlight before it gets Dark.

Having stupidly hoped for that Miracle to arrive with the election results last year, I have to accept that Darkness, real Darkness is inevitable. The only question we all have to ask ourselves is :

"How do I and my family survive what's inevitable?"

They will devalue the currency before they let property prices drop.

Seeking "maximum employment" will be the excuse.

The unsustainable house price inflation has gone on so long people believe it is inevitable and will go on indefinitely ... but they fail to realise how much house prices rises have relied on progressively lower interest rates. The problem being there is a floor to how low interest rates can go. People say "but the OCR can go negative" ... which it can, but nowhere in the world have retail deposit rates ever gone negative. Why? because they can't. The minute a retail deposit COSTS people money, people will stop keeping money in the bank and will instead hold cash. The whole idea behind "creating" money through bank lending, requires that the money lent stays in the banking system - if this breaks down, we are in real trouble - not just the housing market, but our whole financial system.

Better we address things before it gets to that point .... but given how gutless our politicians have proven to be, I'm not hopeful.

Ban cash, digital only currencies cost less to maintain.

then the money goes offshore into other currencies further devaluating our currency

Of course gold is an option too

Yes, this is the endgame of central bankers, the IMF even stated recently that negative interest rates won't work without the ban of physical currency.

It will crash one day Miguel. Contrary to property spruikers, it is inevitable.

Who knows whether it's this year, 5 years or 10 years.

I have put myself out on a limb for the last year, I am picking a financial crisis 2022 that collapses all the cards....

But rental returns are still reasonable. To me that indicates it's not too much of a bubble and that there is a genuine supply issue underlying it.

Maybe they are to you but the rental prices are anything but reasonable in most places in NZ.

Just because someone can charge and profit from people being forced into living in rental properties because houses are now out of reach to buy by the majority of income earners, doesn't mean they should.

Maybe these people should stop to think about the future for once rather than their own greedy pockets.

Nup it's a demand issue, and it's the demand for future 'wealth' underpinning it not the demand for a home.

Plus the banks demand for printing debt - without it they'd just be a money storage house again.

We deserve our servitude for being so damned ignorant.

Who'd have thunk it - money (debt) IS free!

https://youtu.be/fOj_xp2jHl0

The RBNZ said that while LVRs should dampen house price growth over about a year, addressing longer-term pressures on the housing market are beyond the scope of its macro-prudential tools.

Banks will always look to maximise return on capital on behalf of shareholders, hence lending priorities will be determined by the asset class that demands the least capital and provides the most liquid collateral.

RBNZ residential property standard capital risk weights can be reduced by implementing 'the internal models based approach'. ANZ has reported a figure as low as 27%.

{kind=link}

Banks have migrated away from lending to productive business enterprises because the risk weights can be as high as 150%.

Thus around 60% of NZ bank lending is dedicated to residential property mortgages held by one third of households.

Bank lending to housing rose from $50,788 million (48.36% of total lending) as of Jun 1998 to $292,645 million (59.71% of total lending) as of November 2020 - source.

Watch out for rates increases, Market watch 10yr today

U.S. 10yr 1.298 up: 0.0244

Germany 10yr -0.343 up: 0.0257

Italy 10yr 0.662 up: 0.0735

Spain 10yr 0.336 up: 0.0460

U.K. 10yr 0.626 up: 0.0508

Japan 10yr 0.094 dn: -0.0044

Indeed: Nonetheless, residential property punters seem unaware that the long persistent rise in discounted present values of future cash flows associated with assets may have pivoted the other way.

Recent news that the RBNZ may no longer take action to move the OCR to a negative setting and in fact the term discount factor in the form of the government 10 year note has risen from a 0.50% yield last May to 1.50% today are being ignored.

The opposite is true in the short end of the interest rate curve - The RBNZ FLP scheme has implemented a new 3 year wholesale benchmark rate set at OCR, currently 0.25%.

The US has a similar, but lower interest rate structure out to the 2 year note tenor, due to pristine near cash collateral demand - US Tbills.

As long as the government continues to support Byzantine zoning/approval legislation (which, given the RMA will soon be a three ring circus, appears inevitable) and New Zealand's immigration policy remains unchanged I think the tailwind will remain with investors.

..Just don't wake the IRD and mentioned much to the investors, they hated the guts of those IRD bunch. Simple more probing power/authority given to IRD, including necessary logistics, that alone enough to disturb the tailwind. But don't expect it coming from govt, they think they've found the solution to the formulae.. stimulus, subsidy, borrow more.

I'm actually getting a bit tired of property stories at the moment, we seem to be locked into a death spiral with RBNZ and Government. It seems that until the system completely stops functioning we are going to continue to pursue the policies that got is here at any cost.

I'm picking Green's pick up a bunch of disillusioned Labour voters by next election. Market will start to get shaky in late 2022 when players realise a wealth tax is on the table.

Forget about a wealth tax. Just means test national super. Start with a high threshold. Say 2 million in assets or Income over $200,000. Let that settle in and then gradually lower the limits.

You have obvioulsy never tried to asset test somebody. You would need an army of forensic accoutants and sub-branches of NZS in India, USA,China, Pakistan, Australia,Portugal.......and on and on.

There is a reason we don't. The reason is we can't.

We can ony asset test ma and pa with their kiwibank account who were born here.

Yeah would be absolute can of worms with trusts with multiple trustees & beneficiary's etc. Land tax or Capital gains is way to go. Though the greens arn't financially literate enough to understand this so might give wealth tax a crack.

Thirty years too late for a capital gains tax, unless property prices crash. But an annual land tax added to every property-owner's rates bill would be simple to implement, and effective. It would provide a nice piggybank for building state rental housing for all those who will never be able to afford to buy their own home.

I suspect their reason to give that option a crack? - coz' no one dare to touch the other thing you've mentioned in NZ, including the green.

NZ is full of kindy kids that all able to held their ECE teachers as a hostage, more lollies? yip, more soda? yip, we would like to breath that crack+vape sweet vapour.. please?, err yip sure.

Income test them then!!! Either you're retired or you're not retired. Taking a pension at 65 while still working (withholding a job from somebody else) and probably owning a couple of rentals (withholding home ownership from somebody else) is ridiculous.

Nzdan, the problem is that they can't really make any changes to super immediately - they need to be phased in. And what does that mean? The people who will really bear the brunt of super changes are not those boomers who have already benefited from rapidly rising property prices. It will instead be yet another kick in the guts for those who had to take out student loans, and are either renting or in massive mortgage debt. It's just like saying, oh, you're a millennial? Congrats, that's a 250k penalty for being born at the wrong time (lucky you! Student loans and ridiculous accommodation costs!) Oh, and as a cherry on top, we'll take an extra 80k off you by means testing super because you had to take out a 30 year mortgage (and so work way beyond 65) so you could pay the boomer you bought your house off a couple of hundred k extra to supplement THEIR super.

Of course they can. Sorry Boomer on $250k p.a. salary, if you want to go on the benefit then you need to quit your job like everyone else under the age of 65. Just amend the NZ Superannuation and Retirement Income Act:

Insert under 7 - Age Qualification for New Zealand superannuation

(4) However, a person is not entitled to receive New Zealand superannuation while employed in full time work.

Full time work is defined as....blah blah blah and income greater than...blah blah blah.

No, the triumph of NZ Superannuation is that it is universal and nonjudgmental, as long as you have 10 years' residency up your sleeve. You get it regardless of whether you are an 80-year-old workaholic who's been slaving away happily since the age of 15, or you've never worked day in your life.

A better solution, as Susan St John has suggested, is to keep NZ Super universal, but put those who sign up for it on a special tax scale for other income that would claw much or all of the Super back, reflecting the fact that NZ super is a social welfare benefit. That would still not deal with the tax inequity between aged property owners and non-property-owners, however.

https://www.interest.co.nz/personal-finance/81629/susan-st-john-says-al…

Know what you are saying.

But at least every story and opinion and attack from the opposition puts the government on the spot.

It's going to be fascinating what policy they come out with in the next few months. I expect to be underwhelmed.

This system has been architected as a solution for poor GDP. It has not been built to deliver affordable housing. What is happenning is the intention of the government and not a problem they are trying to solve. Look at the policy settings.

1) if you sell a house in five years the government will tax the gains

2) If you are going to get taxed on the sale of a property, dont sell it and use equity release to buy another property tax free.

3) if the housing market looks like falling.. raid tax payers accounts for 64billion to ensure it doesn't.

In short if everyone owned a house there would be be no investors. Pointless owning a house you cannot rent. To ensure that you have renters you have to ensure some people have multiple houses and keep it so expensive that some people will never afford it.. It is very sick system indeed.

Exactly, I thought I heard a politian the other day, say 'high house prices are good thing, because it creates a strong rental market'. 'Plus at the end of the day, you need someone to pay your mortgage'. Now we know why all politicians are also landlords. Rigged system. Life will suck for a lot of our people because of this behaviour.

Don't forget the $1.5b annually in accommodation supplements paid to landlords via renters to underwrite the whole system. Over 300,000 households need AS in order to pay their rent. Average of 5k per year from the crown accounts direct to landlords pockets per household .

While this is a move in the right direction is still not pushing the wealthiest investors out of the market. We need a total ban on speculative behavior on housing and we need it yesterday.

The root cause of the housing debacle has been the uncontrolled immigration into NZ. As an ExPatKiwi I look back at a country I barely recognize now.

An article in stuff today about how NZ should reinvigorate the immigration programme once borders are open. No mention about the impact this would have on housing.

Nice analysis/prediction, out of...staggering, stellar performance in short period of time for .. NZ darling house inflation by how much? ha ha, gullible Kiwis. OZ will always get the upper hands to squeeze you.

At least that graph shows who's been buying lately.

People leveraging up to and over 70% loan to portfolio value often only possible for mum and dad investors buying their 1st IP ... I.e people with out a clue caught up in the excitement.

Speculative demand is a tap that can go from full bore to off very quickly and is always never given the respect it deserves in driving prices.

That 4% reduction in price could easily turn into 10, 20, 30% as the power of human nature again magnifies market moves by x10

This is what it was really about, “Moreover, lifting the LVR restrictions removed a risk these might discourage banks from offering mortgage deferrals to their customers.” Orr was shit scared of deferrals because people were already too leveraged, so he let those who could, leverage some more ... OMG

"RBNZ Deputy Governor Geoff Bascand, at a Finance and Expenditure Committee meeting last week, told Members of Parliament he didn’t regret removing LVR restrictions last year."

How does he still have a job after such a demonstration of incompetence and lack of awareness?

That's a shocker.

I do actually see the rationale and benefits of cutting the OCR.

I don't at all on LVRs.

They seem like a really arrogant bunch.

Yes, his and RBNZ governor (who decided he was right) should have lost their jobs. Unfortunately they are unelected officials who report to nobody, not the public that's for sure, and they only have to self rate their performance. Which of course is always "stellar".

They should have been rolled late last year when it was clear they completely screwed up. Unfortunately neither the finance minister nor the PM have the slightest bit of backbone to actually do it. They all just trundle along believing their own self affirming rhetoric.

It didn't take long for Grant and Jacinda to get arrogant did it. Probably 1 year into their first term.

RBNZ says ....' will shave between one and four percentage points off house price inflation over the next year.'

Amazing, they can tell what the saving will be without knowing how much it will go up by, But whatever the figure is, it will be up to 4% less.

It's a nonsense meaningless prediction.

If they could control how much things come back by, why don't they enact policy that causes no further increase or a reversal of the last few months increases? We know why.

One day we will look at central banks, like we look at communism today. Looks ok on paper, rotten once you understand it.

Brr.nz

Cool username

December 2020 lending to Investors 2454 million. December 2019 1298 million

December 2020 lending FHB 1686 million. December 2019 1209 million.

So LVR for FHB will go ahead after this month.

Average FHBs have exactly 9 days before a hurdle is being thrown at them- be quick!

How do you define average?

LVRs were removed because the widely expected price falls might have seen some owners having their loans called in, particularly if they had borrowed against businesses that also got into trouble. I thought it was a good move, however they should have been reinstated before summer when the situation improved.

Make it 100% and you got a deal

So now that property investors are selling up due to the new tenancy regulations, if you remove 40% of investors from the market, that means less rental properties available to be rented. I thought there was a rental property shortage as well? So new landlords cant take the place of old landlords, and the ex-rental now sits empty while it waits for an owner occupier to buy it. Do people actually think any of these policies through?

There should be a punitive tax on every unoccupied dwelling of not less than 100% of the estimated or actual capital gain for every day it is unoccupied, so that nothing can be gained by owning it.

Speculator investors actually keep all the properties rented so that the costs of loan are paid by the renters. By introducing your rule, you're only end up hurting the non-speculative holiday bach owners. :D

The hidden power of the law of unintended consequences.

It's a shame my tenants weren't featured- it would had made it a more interesting read.

https://www.stuff.co.nz/life-style/homed/housing-affordability/12429765…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.