The Reserve Bank (RBNZ) says banks can’t use higher bond yields globally and domestically as an excuse to not lower lending rates.

Speaking to media after releasing the RBNZ’s quarterly Monetary Policy Statement on Wednesday, Governor Adrian Orr recognised improved growth and inflation outlooks around the world were contributing to rising yields.

The worry is that if banks’ funding costs go up, they’ll pass that cost onto their customers by charging them higher lending rates.

Yet with the RBNZ making up to $28 billion of cheap funding available to banks through its Funding for Lending Programme (FLP), Orr said: “They can’t just point to the rising wholesale interest rate to explain why they are not passing through the rates.”

Since the onset of COVID-19, the RBNZ has thrown a lot at lowering interest rates to try to boost inflation and employment. It has cut the Official Cash Rate to 0.25%, committed to buying up to $100 billion of mostly New Zealand Government Bonds on the secondary market via its Large-Scale Asset Purchase Programme (LSAP), and offered to lend banks newly created money at the OCR through its FLP.

A difficult balance

Assistant Governor Christian Hawkesby said the RBNZ couldn’t “completely stand in the way” of the factors driving up long-term interest rates.

He and Orr recognised the optimism underpinning rising bond yields was a good thing.

The RBNZ revised up its CPI inflation and Gross Domestic Product forecasts fairly substantively since its last Monetary Policy Statement in November.

Yet Orr said if monetary conditions tightened “unnecessarily”, the RBNZ would act.

“What we’ve talked about very openly there is we expect more pass-through from the banks because of our Funding for Lending Programme,” Orr said.

“And of course, as I mentioned before, the Official Cash Rate can go lower.”

Orr also noted banks are no longer as reliant on wholesale funding from offshore. Unlike before the 2008 Global Financial Crisis, a higher portion of their funding now comes from customers’ deposits.

“We have a lot more optionality to achieve, or sustain, the conditions necessary to meet our remit,” Orr said.

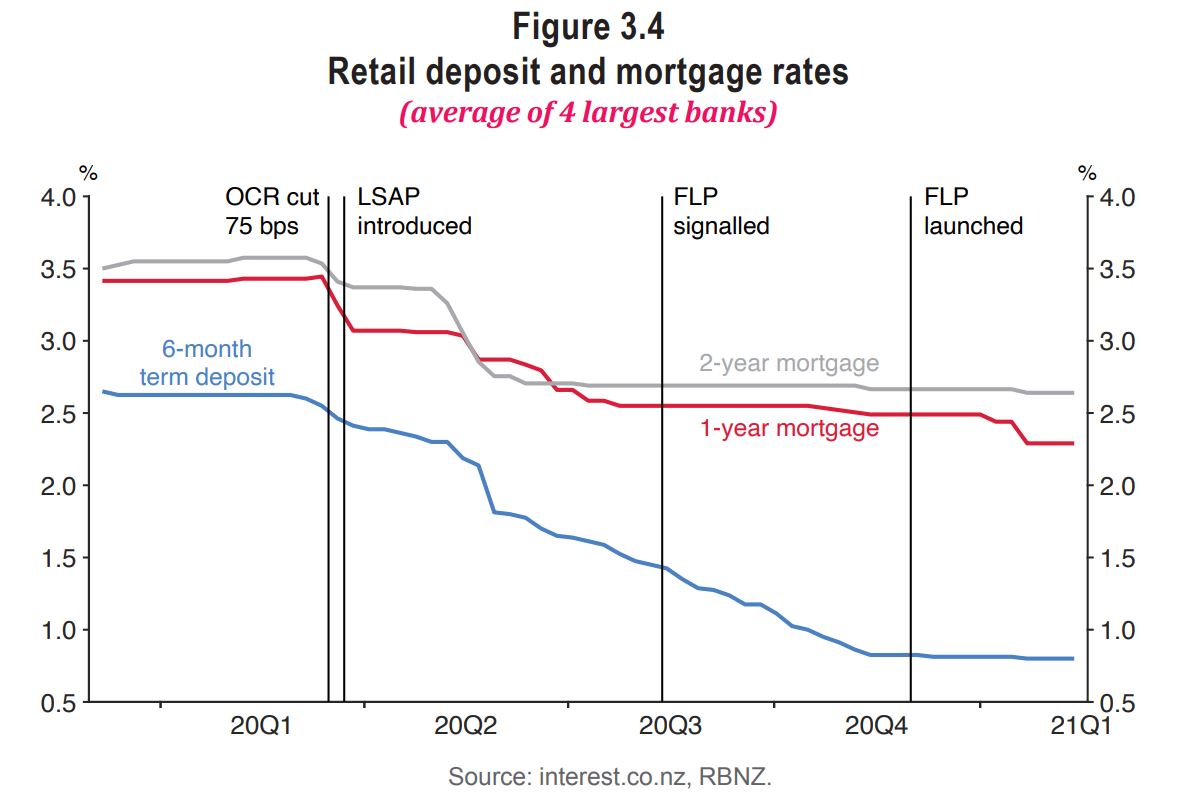

Banks lower deposit rates more than lending rates

Since the RBNZ started aggressively loosening monetary policy last year, banks have lowered term deposit rates more than they’ve lowered mortgage rates.

The RBNZ explained in its Monetary Policy Statement: “Mortgage rates fell immediately following the reduction of the OCR to 0.25 percent, and have continued to drift lower in response to further monetary easing. Lending rates to businesses have also declined.

“Deposit rates fell steadily throughout the second half of 2020.

“Declines in deposit rates partly reflect the anticipation of the FLP, consistent with international evidence that monetary policy has significant ‘announcement effects’. That is, market participants react to the prospective implementation of a policy before it is operational.

“More recently, there have been small declines in mortgage rates. Declines have been most prevalent in the 1-year mortgage rate, for which competition between banks appears to be strongest.

“Strength in the housing market led to record volumes in new mortgage commitments in late 2020, which may have dampened competitive pressure for further reductions in lending rates.”

“With highly accommodative financial conditions expected to remain for some time, we expect banks will pass through lower funding costs to lending rates over time.”

Hawkesby told media he wasn’t surprised uptake of the FLP had been “modest” to date, at $1.14 billion.

Orr added: “The mere fact it’s in the room, changes behaviours. And that’s what we will be watching.”

Asked whether he was satisfied banks were passing lower costs on to businesses - not just property buyers - Orr said there was more banks could do.

Yet he reiterated what the RBNZ has said in the past - that it can’t control who banks lend to. In other words, whether they choose to lend more to property buyers than to businesses.

Orr also noted the RBNZ can’t make businesses want to borrow.

A matter of bedding in inflation

Orr said the RBNZ didn’t provide more explicit forward guidance in the Monetary Policy Statement, as its counterparts overseas have, around future OCR movements.

He said the RBNZ couldn’t pinpoint a date when it believed “confidence will magically arise”.

He stressed the RBNZ’s view that it would take time to attain and sustain this confidence.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

22 Comments

Orr is like King Canute commanding the tide not to come in. However, he is not prepared the suffer the slings & arrows of a normalising economic cycle, and is now building a dam made of QE cash.

He is a clear & present danger to economic stability and the monetary system we all live under. All central bankers are, because they are all following the same flawed and failing gameplan. Nothing but wreckers whose gross distortions in the market just cause cascading issues. They've killed price discovery, they've consipated the functing of the market so that it is clogged up with excess debt and malinvestment.

Rearrange the letters in Canute minus the 'a' and the 'e', and that's what Orr is behaving like.

Thanks, now I've spilt coffee on my laptop after reading that

Beautifully written, and so true.

Assistant Governor Christian Hawkesby said the RBNZ couldn’t “completely stand in the way” of the factors driving up long-term interest rates. He and Orr recognised the optimism underpinning rising bond yields was a good thing.

I don't think so. Higher oil price expectations in the Northern Hemisphere have caused 5 year US Treasury Inflation Protected Securities yields (TIPS) to trade as low as negative 1.86%.

Real yields say, ‘The real economy is AWFUL!’ So what is driving inflation expectations higher? Fuel. Oil prices are up – but the economy isn’t. Link

Furthermore, the floating Secured Overnight Financing Rate is just 1bps above the Fed's Reverse Repo 0.0% interest rate floor, while interest on excess reserves is set at 10bps.

Yet with the RBNZ making up to $28 billion of cheap funding available to banks through its Funding for Lending Programme (FLP), Orr said: “They can’t just point to the rising wholesale interest rate to explain why they are not passing through the rates.”

Only for selected investment securities already held on account via money less repurchase agreements-exhibit 2:

Eligible Securities: Tier 1 securities (New Zealand Government Securities, acceptable Kauri issues), and Residential Mortgage Backed Securities (RMBS).

FLP is only up to 6% of a bank loan book and only if they behave. How are banks supposed to hold more capital if the RB is determined to drive depositors elsewhere demanding lower rates which will effect depositors as well.

Bank have retained earnings, which presently cannot be distributed to their shareholders, to bolster capital to meet regulatory risk weighted asset expansion requirements.

Banks swap IOUs with borrowers to generate unsecured deposits for so called savers who have exchanged assets or commodities etc in return for them.

Exactly! Does Orr know what he is talking about, or is he just being disingenuous ?

"Yet he reiterated what the RBNZ has said in the past - that it can’t control who banks lend to. In other words, whether they choose to lend more to property buyers than to businesses." - Yes they can just make it a requirement that if they draw down on FLP it can only be loaned out to business.

"Orr also noted the RBNZ can’t make businesses want to borrow." -- ha - I am sure they are sick of the rejection of trying from banks

You just shuffle your money around and so ring-fencing has no effect.

Who needs banks Adrian? Everyone can bank with central bank with dictated rates for everything? 'Tis the socialists dream.

That's it Adrian, we have been too gentle on society. Forget sending house prices to the moon, let's send them to the Kuiper belt.

Yes. And I for one are not going to sit there with my large retirement funds earning next to nothing in a scam TD account. All my money is currently being taken out of NZ banks and headed overseas. Since I split my time between two countries I have that advantage. I know all about fx risk. To think people are going to put up with such pathetic TD returns over the long term in order to continue in bubbling up real estate...find yourself another sucker.

The RBNZ is on a path to no good! They are the architects of destruction. None of their objectives are admirable. A few decide for all. And these few are usually the most insulated from the misery their policies are causing for your children, the aged, and generally for all those whose oncomes are not adjusting to the asset inflation that is being willfully created. Mr Orr, you are not working in the interests of the people at large and I have one thing to say to you, "karma"!!

Orr must be sacked. And he must go now, before it's too late.

"Orr also noted banks are no longer as reliant on wholesale funding from offshore. Unlike before the 2008 Global Financial Crisis, a higher portion of their funding now comes from customers’ deposits."

Total BS from Orr, again. Customers' term deposits are evaporating at a fast pace. If I remember well, every month 2 billions disappear from the term deposit pool of NZ banks. And I think that this monthly hemorrhaging will increase. I personally would not establish a new term deposit with a NZ bank at the current levels of interest rates, not even a single dollar.

Yes, on-call accounts amounts are increasing, but is this what we want the NZ banks to rely on, in the future ? On call-accounts and the RBNZ funding ?

It's interesting that Grunty asked Ariana to jump across a hurdle without actually jumping and Ariana now asks the Banksy to do the same.

An epic disaster in the making.

.

Orr tells banks to lend without pricing in risk.

Orr tells banks to lend without pricing in risk.

Orr can hand banks as much cheap money as he likes, but is deluded to think he can then stand back and they will pass on the rates. Banks have a legal duty to make a profit for shareholders. So its easy money for banks to be handed cheap money for their shareholders. Customers are their source of revenue and not people to help out because Orr thinks so. Orr has not appreciate customers are the market and so must impose laws on banks to lend and force banks to on lend the low rates. Instead banks are tightening their security levels with LVRs etc. to protect and secure their already mega profits so that there is more equity in a mortgage that they own and can use to sell-up everyones home. The banks own your home if things go belly up.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.