The wait continues for those interested in whether or not the Reserve Bank (RBNZ) will go further to restrict bank mortgage lending.

The RBNZ plans to respond in late-May to the Government’s request for more information on restricting interest-only mortgages and lending to people seeking large mortgages compared to their incomes.

Some observers may have expected the RBNZ to release this advice at the same time it publishes its biannual Financial Stability Report on May 5, to effectively kill two birds with one stone.

But, the RBNZ told interest.co.nz: “We will be providing advice on policy options for responding to the Government’s section 68B direction on housing-related matters late next month.

“This will be released separately to the publication of the May Financial Stability Report.”

Finance Minister Grant Robertson on February 25 asked the RBNZ to provide advice on debt-to-income (DTI) and interest-only restrictions. He did so as he issued a direction under section 68B of the Reserve Bank Act, requiring the Bank to have regard for the Government’s housing policy in the work it does to ensure the financial system is stable.

Once the RBNZ provides advice on DTI and interest-only mortgage restrictions, the Government will need to decide whether or not to add these tools to the RBNZ’s “macro-prudential” toolkit.

Should it do so, and should the RBNZ decide it needs to use these tools, it would need to publicly consult on the matter. This could take some time. For example, there was a three-month gap between the RBNZ starting consultation on reinstating loan-to-value ratio (LVR) restrictions and these actually coming into force.

There a number of complicating factors underpinning this situation:

1. Robertson has repeatedly said he would only want DTI restrictions imposed on investors. But RBNZ Governor Adrian Orr has said this would be difficult.

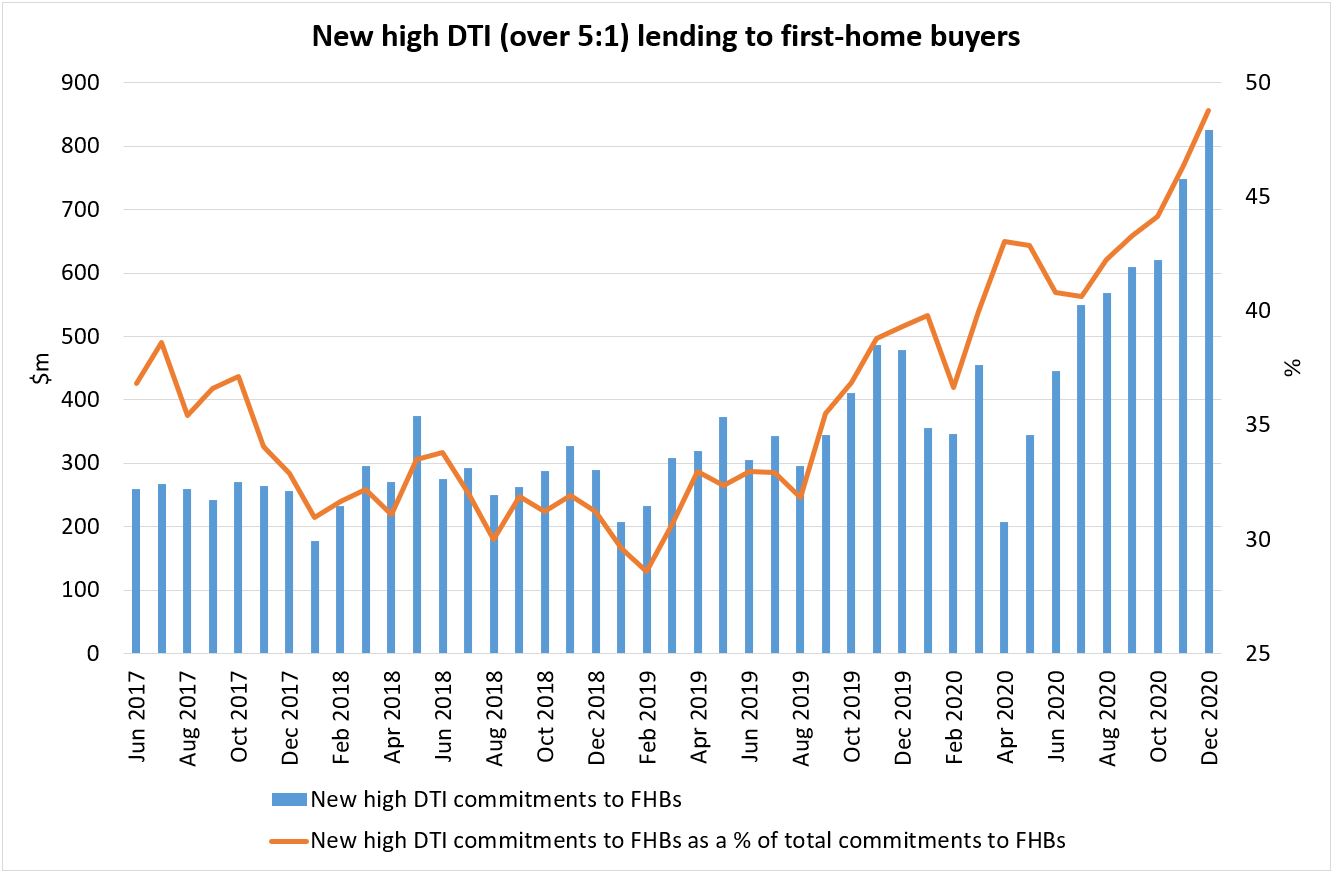

The RBNZ doesn’t even publish data on investors’ DTI ratios. The data it publishes shows first-home buyers - the group Robertson is trying to protect - have been taking out increasingly risky mortgages, as house price growth shoots ahead of wage/salary growth.

Source: RBNZ

2. The effects of tax changes aimed at reducing demand for property by investors are yet to be seen.

As this reporter suggested in an opinion piece published earlier this month, the RBNZ may want to consider the impacts of a proposed law change to remove the ability for investors to deduct interest as an expense for tax purposes, before taking another step to curb demand for property.

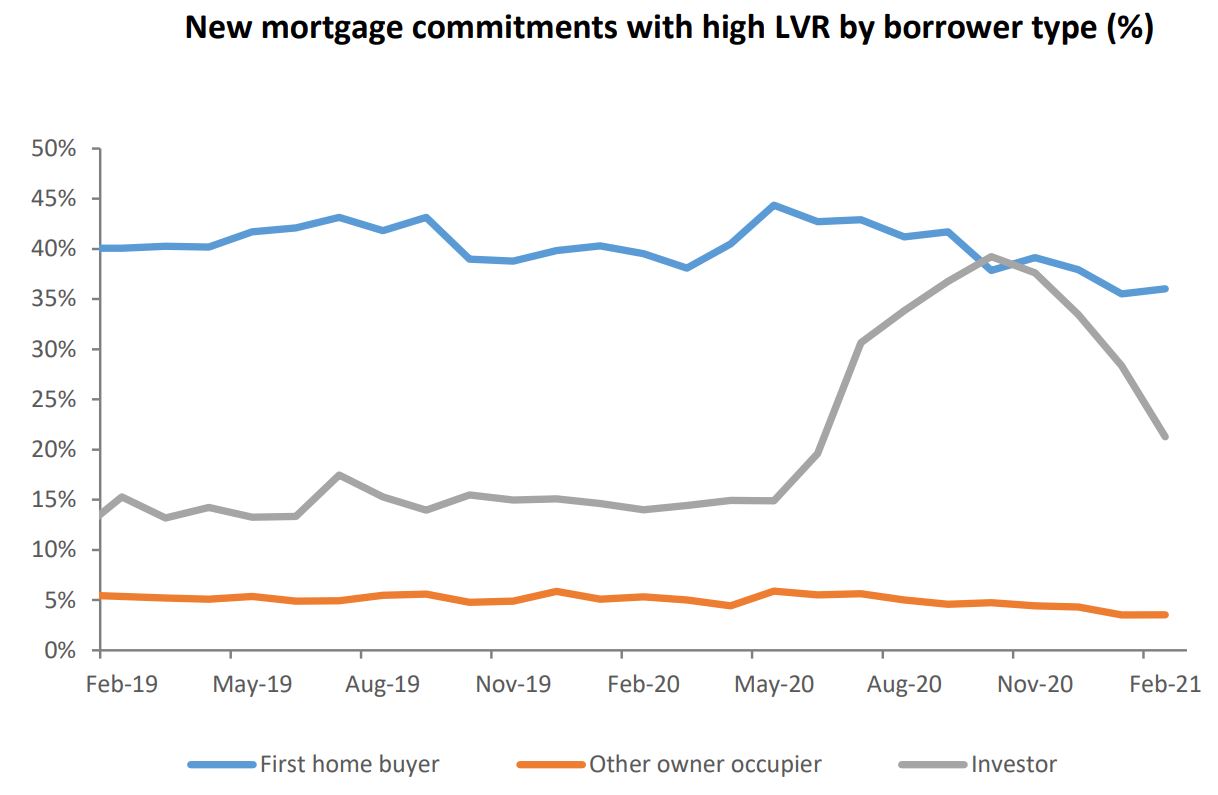

The RBNZ may also want to sit tight and consider the impact of LVR restrictions reimposed in March.

Source: RBNZ

3. Robertson is proposing to change the roles of both the Government and the RBNZ when it comes to setting restrictions on bank lending.

He published proposals last week outlining what the new process could look like, further to a long-standing RBNZ and Treasury-led review of the Reserve Bank Act.

Robertson suggested the RBNZ would still decide how to regulate bank lending. It might even have more macro-prudential tools, including DTI restrictions, at its disposal.

But the Finance Minister would specify which types of lending (IE residential property, commercial property, agricultural, business) restrictions could be imposed on.

The proposed regime is complex and includes a number of grey areas that need to be worked through before it takes effect in 2023.

92 Comments

Current bank lending style is a systemic risk to the tax payer. So by mid year we could have Dti and and end to interest only. Speculators will wail, but their and the banking sectors greed, have caused this.

If your a fhb I would absolutly wait until the back half of the year.

I am actually quite scared to suggest that an FHB can have the liberty to wait a bit. I have been so wrong on this many times and have watched the prices sky rocket to epic levels.

From the article though, all the huff and puff is about DTI, so removing interest only loan is a no brainer? So can the RBNZ and the government at least do that while they mull, contemplate and have a wait and see approach, back and forth, indecision on DTI?

DTI should be on all not just investors. DTI's aim is to regulate the household debts to a sane level. FHBs should also be protected.

Also just seal the immigration tap. With all of this, if you do not negate the influx, nothing matters. The team of 5 million should ideally be the team of 4.5 million, then down to 4million and sustain it at 4 million. Everyone will prosper.

Just look at what investors are doing now, wait and see. You would be taking a huge risk jumping into the market right now.

Yes. FHBs need protecting from themselves as much as investors do. How FHBs can be so contempt taking on so much debt is mind boggling. I was a FHB 2yrs ago in Wellington and had a 40% deposit and DTI of 2 (two income household). Yet I still worry about owing over $300k of debt and how I can clear that asap.

Well Spectators, I couldn't sleep if I owed so little at your stage.

Why did you wait so long to buy man?

'Buy! Buy! Buy! Buy! Mad if you don't!'

This is what it's like living through a speculative mania, where irrational exuberance is off the chain and running wild. Historic times indeed.

You couldn't be more wrong, timing the market is speculative. Time in the market is what leads me to ask why they waited so long to buy. The longer you wait, the more you have to pay on average.

If you aren’t careful people here will start accusing you of being Warren Buffet.

You guys made my day! :)

And is that what happened with the US, Japanese, and Irish housing markets in the lead up to their crashes?

Same with equities: look at the epic crashes that have happened on a regular basis throughout history.

After every credit fuelled 'boom' there is always a bust. Please don't get in at the top Laminar.

Everything you are saying is speculative my dude. I get in at tops and bottoms and everything in between.

My investment portfolio was running faster than houses so I was happy to keep my deposit in equities. Only bought when we found out that we were soon to be a family of three and didn't fancy raising a child in a central city Wellington apartment.

I don't think you have done your maths right there bud. Did you account for leverage?

You can leverage shares as well. ASB securities publishes a list of pre approved securities and the LVR they will take on them. I seem recall lending against some bonds being as high as 95%

Yes you can leverage shares but the leverage you can achieve against financial assets is generally a lot lower and more expensive relative to housing assets and you are also on the hook for margin calls . I am sceptical you can borrow 95% of the value of a bond as a retail punter and if you could, it would be a bond that yields less than the cost of margin loan e.g. a government bond.

My investment portfolio was (now less so) aggressively leveraged. My leveraged returns plus small savings in rent vs mortgage and owner expenses outweighed the house price appreciation of the neighbourhood I bought in. Disclaimer: I work in financial markets so I do appreciate that most won't be utilising leverage in their investing and therefore your point is true.

"How FHBs can be so contempt taking on so much debt is mind-boggling"; well likely for the same reason you'd run a bond portfolio 20:1, or a stock portfolio 10:3. You made the same style bet as the FHBs you are casting shade on. Even so, why a 40% deposit when you could have held more stocks rather than saving some minuscule amount of interest?

The issue is what happens when you wait. Anyone who was thinking about buying 1-2 years ago and didn’t will be wishing they had.

Not me - I'd be pooing myself if I'd ploughed 700k into a shitbox (that is now, on paper, worth 850k) with the massive risks sloshing around.

Was the same with tulips bulbs. Prices just kept rising and rising, they were still jumping in at the top and were being advised to do so by astute family & friends and tulip bulb dealers. And look where they are today, I can only dream of owning a tulip bulb.

Friends of ours put an unconditional offer in today on a house - 400K (40%) over RV (on a 2019 RV) top of the valuation - Real estate agent said - that price wont be high enough - you will need to up it. Apparently they looked at her and said no thanks - not playing that game anymore. they are happy to wait than pay too much. There are a lot of stupid prices out there but also lots of real estate agents trying the old FOMO tricks too. Really this sort of behaviour should be banned in the industry.

Removing interest only may well be a no brainer...

So it'll be a good litmus test for intent for the RBNZ and government.

Agree with you RickStrauss and it is for this very reason is been delayed as reality is that both Robertson and Orr is happy for the ponzi to run = NZ economy.

Thick skin @#$& - do not care so to expect anything from them on time is asking them to go against their breed.

There is a chance that a supply squeeze starts to become apparent later this year (November / December) as supply that was expected to come on stream does not (due to some developers holding off on converting their building consents into dwellings whilst they wait on the definition of a new build and information as to if new builds will be exempt from the new interest deductibility rules. There is also a chance that the prime minister was being too definitive when she said new builds would be exempt).

A supply squeeze may push up prices, especially if it happens to coincide with reduced existing stock coming to market due to investors not selling courtesy of the bright line rules or looking to consume the whole benefit of the tax deductibility of interest on their existing holdings over the next 5 years.

That is the real damage when we get just words, then no action.

Kiwibuild being a good example. Lulling FHB into maybe waiting on the sidelines (and registering their interest, remember those stats?) in the hope this would be their chance to get into a home. Then finding themselves high and dry when delivery came to virtually nothing. And house prices had continued to race even further ahead in the meantime.

Seems to be helping them now. I know people with Kiwibuild houses who purchased in the last year.

Agreed. If I didn't know any better I'd say it is planned that way

Watch and wait!!!11one

Averageman, they have no intent to act but as are forced both are playing a scripted scene to buy time to avoid taking action and if they are not able avoid than try to delay as much as and this exactly what is happening.

Mr Orr should be asked, why is he waiting till end of week ...to be transperent, would he enlighten us, who are ignorant, what data/information is he waiting between now and end or May before advising Mr Robertson....unless it is a part of the game plan to delay as no intent.

You may be right. Who is running NZ again...?

Another 4 weeks of waiting....why doesn't Orr show some courage and take action rather than continue with his interminable waiting game.

#SnailsPace

Have any of you really thought this through? The more macro-prudential restrictions on lending, the harder it is for first time buyers, or those without asset rich parents, the deeper the moat between the haves and have-nots. These policy changes will not be the panacea for affordable housing nor lead to lower prices and it is likely to necessitate other stimulus packages. If any new restrictions are introduced it also makes low interest rates for longer a lot more likely.

Sure but what you call being harder for buyers is just not taking into account that a mortgage the size is required these days will be even harder to handle when rates will go up even by a little bit.

Why would it be harder for FHB? How many investors are rocking out interest only loans and 40% deposit recycled from equity? Many many investors are also likely to be "have nots", if it weren't for such ridiculous lending conditions.

If you knock out investor property purchases overnight, then you have effectively halved demand in the FHBer market if RBNZ C31 numbers are anything to go by.

Why would it be harder - because a FHB will be able to borrow less. So unless prices fall, they are locked out. Also you won't remove property investors from the market, many have already accumulated enough to be able to deal with whatever changes eventuate. You also lock out the current young from getting ahead by investing in property. You may think that's a price worth paying, but that's the moat.

That's precisely the point. The hope indeed is that prices fall because house prices are the problem. We back ourselves into a low interest rate forever hole the more we let household debt climb. The answer is not to allow people to borrow more and more to purchase houses that are increasing in price, it is to reduce house prices so that buyers don't have to borrow eye watering amounts that threaten financial stability. Housing is a basic human need and therefore should be affordable. As to locking out the current young from getting ahead, if only there were other assets available to invest in other than property to get ahead?! You know, ones that don't render some of your fellow countrymen homeless.

"That's precisely the point. The hope indeed is that prices fall because house prices are the problem."

Hoping that prices fall by addressing the demand side is a really poor strategy, look at the hole that has got some commentators here in over recent years. The best bet is addressing the supply side - council planning etc etc. Rates are low forever, you're kidding yourself if you ever think they go back up. Look at Switzerland - their 50 year bond is -10bp.

I'm not sure you understand Adrian's job. He warned the govt in Nov 2019 and Feb 2020 that his response to an economic downturn may include UCM and that could be reasonably expected to drive housing prices up, he went on to say the government has the tools to manage those externalities and the use of those tools is warranted. It is Robertson who doesn't know what he's doing and said he was sceptical of the link between interest rates and house prices, he went on to do absolutely nothing until it was far too late, and what he did doesn't even make any sense. Say it with me, build more houses and tax capital gains.

Agreed Laminar, Robertson has been exposed here.

People forget, Robertson was the one who added the full employment mandate in 2017, leading to interest rates that were lower than they otherwise would have been. Then he didn't like the results on house prices, and chucked in another mandate. He is pretty culpable to be honest.

Plenty of central banks have dual targets including employment. They all however, have a capital gains tax on resi property investment. I've been calling for this for 4 years here. Instead we are going to tie ourselves in knot's making up policy on the run.

Laminer. You have got the handle on this. Adrian Orr knows what he is doing. Robertson does not. Orr is steering clear of Politics, Robertson trying to pull him to control the Reserve Bank into Labours objectives!!!

We wouldn't want to be accused of moving too fast would we?

When they were afraid house prices might reflect reality the LVR's were gone by lunchtime.

Trying to actually do something about the cancer eating this country. Endless foot dragging.

Going on past form, there will be 1 year of consultation with "stakeholders" and then a 3 year implementation timeline.

Is it May this year or next year, please be specific in your article..

Good point. A working group will be assembled to make a decision in the next 6 months if the announcement was meant for May this year or next year.

Or is it 2023

Slooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooooow

Almost half of new lending to FHBs over 5-to-1 DTI? Christ. I assume that's household income too.

Two incomes, no kids for the most part. Things like that be put off... until suddenly they can't.

Given that the bright line assumes an intention to resell for profit, will any (unrealised) gains on property subject to the bright line constitute income for the investor? If so an investor DTI would essentially be meaningless in any sort of rising market?

Will companies that are setup as investment vehicles include the income of every shareholder when calculating DTI? Will companies need to list the income of every shareholder when buying property. What if a

Someone buys into the company after the property was purchased? Will individuals be prevented from buying into companies if doing so would cause their own or the company’s DTI to be in breach?

What is the expected impact on aggregate housing supply of DTI / “non deductibility of interest expenses” impacting bank servicing calculations and thus preventing those who wish to densify from buying existing properties that they can demolish to make room for multiple new dwellings?

Looks like apartments and units are heading towards a boom in the next few years.

Time to take stock.

Is that a boom in leaky buildings claims or mortgagee sales?

Looks like you'd never bought a house before. There's something called "due diligence" and "insurance".

Due diligence and insurance only gets you so far.

Looks like you've never done any due diligence if you think apartments in New Zealand are a good thing to buy.

I just don't understand how DTI would work in FHB favour. All it does is make a cutoff point like the current home subsidy that was on the news the other night based on your income and the lower quartile median house price, which the Government are yet again using the wrong numbers. You end up either earning to much and the houses are non existent anyway in that price bracket. DTI looks like a tool to simply stop risky bank lending to me so even more FHB will be locked out of the market. How FHB think it will magically reduce house prices is beyond me.

Maybe FHB are of the impression that they have higher cashflow than investors ;p

They certainly pay more in tax.

Many investors will also have day jobs at a senior level or in specialist fields. Only the retired investors pay less tax.

House prices are a function of the credit available to bid them up. What happens if there is less credit available?

Unfortunately for you, you only saw 1 out 3 possibilities on the impact on house prices. Your single variate assumption on house price doesn't hold water. Does gold ever fall in prices because people couldn't find funding to buy in bars? No. The prices never fall due to funding, instead gold buyers buy in small tranches like a gold chain for a start. And we haven't got to the power of alternative funding. Maybe the muscle between your ears lost weight recently?

Do the majority of people buying gold do so by borrowing in excess of 5 times their income? No. Are people able to borrow with 10% equity to buy gold? No. Are banks able to hold very low capital requirements to lend out to people buying gold? No

As usual, you make yourself look incredibly stupid every time you post.

Looks like your ignorance just reached a new level.

We have been able to invest in gold with a LVR 95 for as long as we had been doing it. People are able to buy gold with 10% down as long as the gold is the collateral marked to market at the point of investment.

I think you should be logging off the internet to enjoy your tacos instead of displaying further ignorance.

We have been able to invest in gold with a LVR 95 for as long as we had been doing it. People are able to buy gold with 10% down as long as the gold is the collateral marked to market at the point of investment

Who is selling you this? I own gold and have a relatively good understanding of the options available to buy gold. Just link to the provider please.

I'm not your free advisor, you should do your own research.

Just to tingle your curiosity, this is one example out of a thousand. (I'm not related to them or have any dealings with them.)

If all the marginal buyers that are able to outbid what you are willing/want to pay have been eliminated, you might just find your self with the leading bid.

If there is political will is there the banks can be prevented from lending to anyone who can outbid a FHB (at a DTI of choice). Considering the involvement of the Government in the housing market and general acceptance of a "housing emergency/crisis" I think the argument that window guidance for the banks is an acceptable tool to be implemented in some form.

DTI may be blessing in disguise for Many FHB who under FOMO are borrowing beyond and any change in their situation may prove to be a disaster.

This situation ( buy or not to buy as in both situation, FHB are now screwed with such lofty prices and borrowing) has been created by government and rbnz and even now are not satisfied with double digit rise of house price on a monthly basis adding to plight of FHB.

Neither Mr Orr nor Mr Robertson are genuinely concerned and are playing with time. If they are concerned of anything, it is the ponzi- what if it stops.

Mr Orr is taking months to give advise to Mr Robertson, who again will take its time to consult and decide......and if decide to go ahead will again be months .....though most probably will not go with it as can be seen that none of them have intent or could have acted by now but even if they do, will be months ......not be surprised if they kick it to next year.

All this exercise is to create smoke and fool the people.

Robertson was advised asset bubbles would be result of loose money

lTV and LTI were introduced into Ireland on 9 February 2015, after a two month consultation period and no phase in.

The Introduction of Macroprudential Measures for the Irish Mortgage .https://www.esr.ie/article/view/571 view

PDF.

With the exception of a couple of blips, house prices have risen steadily up some 40 percent from February 2015..At the same time FHB have found it increasingly difficult to enter the market Rents have similarly risen There is a chronic shortage of houses both for rent and sale both nationally and in Dublin

https://ww1.daft.ie/report/2021-Q1-houseprice-daftreport.pdf?d_rd=1

https://ww1.daft.ie/report/2020-Q3-rental-daftreport.pdf?d_rd=1

2014 was the end of the bottom after the crash. With all the cheap credit where else was there to go.

Their HPI data:

https://www.cso.ie/en/releasesandpublications/ep/p-rppi/residentialprop…

"Overall, the [current] national index is 15.5% lower than its highest level in 2007. Dublin residential property prices are 21.2% lower than their February 2007 peak, while residential property prices in the Rest of Ireland are 17.5% lower than their May 2007 peak."

How is this situation is comparable? It could support the idea that high house price growth leads to poor availability and high rents, as well.

I am unsure what your point is. 2014 actually saw rapid price appreciation in Ireland and particularly in Dublin, just prior to the introduction of their measures. Your link will also show that Dublin prices bottomed February 2012 and slightly later for Ireland as a whole. All that "cheap credit ' does not show up in Irish mortgage data where outstanding mortgage debt continues to fall, and has done so for a considerable period.

My point is where is the causality and relevance to our situation? Sure, DTI and LVR did not prevent the market from rising but I doubt they were intended to from where they were.

Considering people still need a 15 to 20% smaller mortgage (all things being equal) than they use to at the peak compared to people paying of larger mortgages this could be a factor. Do you have an article on this?

They were averaging 10% y/y capital gains for a few years in the EU were rates were lower than here, I would the speculators went nuts over there like they did here. You can read anything in this data.

We have peak valuations here and they are still probably 40-50% under their peak after inflation.

Risky time for FHBs. Wait until end of year in the hope that these make a dent, or buy now and secure yourself for the future? The calls to wait have been coming since 2013, heavily in 2017 and now again in 2021. I’d personally not take the risk of prices rising higher and get in now if I could.

Bad idea. Even a 10% correction and the powers they be will step in, slashing this and that

Wow !

So many comments but why is anyone surprised. Was it not expected that both Mr Orr and Mr Robertson will play to a drafted script and this is what is been played out.

Everyone should take a chill pill as come what may neither of them are going to do anything except give hope with mention of future announcement.

FHB has been and will always be screwed. Vote For Jacinda Arden.

The government have been the experts when it comes to giving the public the illusion that they are actually doing something. Still awaiting that review on fuel prices from years ago. Yep they just push out any "Decisions" just far enough for something else bigger to come along and by then its all been forgotten and we have moved onto the next big thing. All done with a nod and a frown of concern its a brilliant Oscar winning performance.

Excellent footdragging by RBNZ on any measures to curb house price spikes. Contrast this with their urgency and immediate action to loosen bank lending last March 2020 when house prices were looking like going into a decline

They all stand exposed but does it matter to them.

They forget that in 2021 with internet and social media where news travel fast and where ever action or for that matter any inaction by them will be under microscope making it hard for them to get away unlike earlier where they were able to manipulate and spin.

Earlier they understand, better for them.

In the foot dragging department,Orr and Robertson make a hungry, tired, autistic toddler look positively willing and cooperative

Yes, lets allow two Arts graduates, with no banking experience, who have never had a private sector job in their life, to take over the running of our banking system. I'm sure that is going to work out well.

Well the good news is that now that Jacinda has stopped tax deductions for interest, investors "incomes" have now increased significantly, allowing them to borrow more than before.

Yup, us FHBs have been sucked into huge debt.

My partner and I owe just over $1mil on our place. We’re well off with household income 200k and both frugal, good savers. We made the decision to spend a bit more to get something freehold because apartments/townhouses felt like bad value for money.

I’m comfortable at the moment financially because interest rates are so low. We put our extra savings to principal. But with interest rates set to rise I truly don’t know what the future will hold and I’m anxious. $1 million is a hell of a lot of money to owe. I’m early 30s and would love to start a family but we can’t afford to even think about that right now - and not sure when we will ever be able to.

We’re actually the very lucky ones who have managed to buy a home - majority of my friends in their 30s are in shared flats or living with parents. Not sure if/when they will be able to save enough deposit required.

Honestly we’re probably gonna get screwed and it’s pretty scary. Remember, millennials and younger haven’t really experienced high or increasing interest rates before so we’re pretty naive when taking on huge mortgages.

Change is desperately needed, I really hope DTI and end to interest only are brought in

Still RBNZ and Government are in Wait N Watch mode instead of least regret.

Shameless creatures.

200k household income and nervous to have a kid...To be honest i think you'd be fine but it really is a damning statement.

Just saw a news in newshub that FHB are not only competing against investors but also from government. This confirms what have heard in real estate that government is extensively buying house and that too lower end house, which many FHB are interested.

Their should be an enquiry on housing mess created by Labour government ( even national was supporting but Jacinda Arden took it to a different level).

How does one compete with government, who till now was hiding behind investors :

https://www.newshub.co.nz/home/politics/2021/04/government-buys-hundred…

How much premium was government paying, just to be the last bidder and Jacinda Arden was unaware, really.

Global synchronized housing market slowdown. Orr et al are taking their time introducing these measures as they need to coincide with the global downturn (especially amplified in the USA).

Same reason Auckland goes in and out of lockdown every 3 months or so. Need a reason to print money for subsidies to match the money printing being done overseas. If NZ doesn’t match, then the NZD becomes too strong which will kill our export industry. It’s all about keeping the balance.

House prices soar globally, need to instantly remove LVRs so NZ house prices soar at the same rate. US (and global) housing market about to burst midyear? Better start signalling moves to initiate the downturn in NZ. This is the window for overleveraged investors to get out while they can and avoid a stampede once the global sentiment turns.

dp

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.