By Jovan Pavlicevic*

1. Credit where it’s due: the debate is back.

NZ First’s proposal to buy back BNZ and merge it with Kiwibank has reopened one of the most important economic debates in New Zealand. After years of inquiries, reports, hearings and recommendations - including three central government reviews - it sometimes felt like the banking competition conversation had gone quiet.

So even if people don’t agree on the exact conclusion, the proposal is directionally useful because it acknowledges the core problem: New Zealand’s banking market is not producing enough competitive pressure.

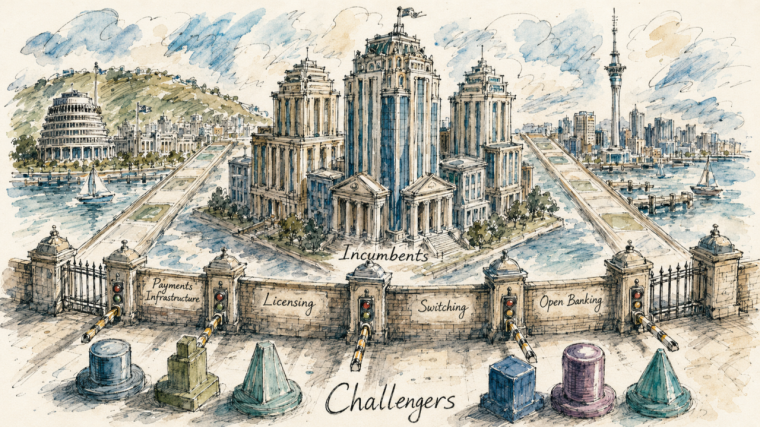

The question now is not just whether New Zealand needs a larger locally owned bank. It’s whether we’re prepared to create the market conditions that allow genuine challengers to emerge, compete and scale. Because ownership matters. But market structure matters the most.

The UK didn’t unlock banking competition by nationalising Barclays or Lloyds. It created better conditions for challengers to emerge - through a mix of regulatory reform, switching, open banking, infrastructure access, direct access pathways, competition funding and modern licensing approaches.

Monzo/Starling/Revolut/Tide - different models, same broader lesson:

Challengers emerge when the market structure allows them to.

2. Scale matters - but scale alone doesn’t create competition.

There’s also a practical question around the sheer scale of what’s being proposed.

BNZ generated around $1.5 billion in profit last year, implying a valuation north of $10 billion, and potentially in the tens of billions once control premium, strategic value and market conditions are considered.

That doesn’t make the idea wrong. It does mean we should be clear-eyed about what problem we’re trying to solve.

BNZ is not a distressed asset. From parent National Australia Bank’s perspective, it’s a highly profitable business operating inside one of the world’s most stable banking oligopolies, with deep structural moats.

So the obvious question is: why would they want to sell it? And if they did, what would the Crown actually be buying?

A larger locally owned bank may be part of the answer. But a larger bank is not automatically a more competitive banking system.

That distinction matters.

Because if NZ's only credible path to banking competition is a multi-billion-dollar Crown acquisition, then we’re effectively admitting the market can’t produce challengers organically - and that should concern all of us, because it means the issue isn’t just ownership... It’s market design.

3. We see this first-hand at Emerge.

That’s why this debate matters so much to companies like Emerge. We’re building modern banking infrastructure in New Zealand today - accounts, payments, cards, onboarding, financial access, and all the systems that sit underneath them. And the lesson is clear:

The problem isn’t that challengers can’t build. It’s that the pathway from credible new entrant to meaningful competitor is far harder, slower and more structurally constrained than it should be.

That’s the part New Zealand needs to fix. We’re one example of what is possible. There should be more.

More challengers, more customer choice, more pressure on incumbents, more innovation, more access... More ways for Kiwi customers and businesses to get better outcomes from the financial system. But great challengers don’t emerge in a vacuum. They emerge when the system plus conditions are deliberately designed to be conducive.

4. OK, so what can we actually do?

To be clear - I believe the BNZ/Kiwibank proposal raises important conversations around sovereignty, long-term capital, and national resilience. Those are valid discussions.

But if the conversation stops at ownership alone, we risk missing the deeper structural issue entirely - and falling out of the waka with the competition settings our global peers have been refining for decades. The goal shouldn’t just be a New Zealand-owned bank. The goal needs to be a New Zealand banking system where:

- new entrants can compete fairly,

- customers can move easily,

- and infrastructure access is open.

In my view, three changes matter most:

1. Designate the Interbank Payment Network.

The Commerce Commission has already recommended designating the Interbank Payment Network under the Retail Payment System Act. (See more on this here). Core financial rails are essential infrastructure. Access to them can’t remain dependent on processes owned by the incumbents if we genuinely want more competition. A modern economy needs modern access rules.

2. Create a challenger competition fund.

The UK used regulatory reform, innovation sandboxes and targeted competition funding to support a more fertile challenger environment.

New Zealand must explore a similar model - potentially recycling a portion of regulatory penalties or industry levies into a contestable innovation and competition fund for challenger institutions. Not handouts, and not favouritism. A deliberate mechanism to correct structural imbalance and increase competitive pressure where the market has failed to do it on its own.

3. Build a proportional pathway for challengers.

If every new entrant faces the same compliance burden as a mature incumbent from day one, incumbents win by default. That doesn’t mean weakening regulation, it means sequencing it properly. A staged, proportional pathway - with appropriate safeguards - allows credible challengers to scale responsibly while maintaining trust, resilience and financial stability.

Because competition isn’t just about ownership. It’s about whether the system is structurally capable of producing new winners.

That’s what drives better outcomes for customers.

And ultimately, that’s what competition is supposed to achieve.

*Jovan Pavlicevic is co-founder of fintech Emerge. This article first ran here and is used with permission.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.