Westpac economists believe that unconventional monetary policy could work in New Zealand if it is used with "sufficient vigour".

But in an Economic Insight publication, the economists say they use the term 'work' in the narrow sense of the Reserve Bank meeting its inflation target.

And they warn that monetary policy, whether conventional or unconventional, is no panacea.

The publication, written by Westpac chief economist Dominick Stephens, senior economist Michael Gordon and market strategist Imre Speizer examines the various options New Zealand has for unconventional monetary policy - although the authors say they don't actually expect that such a policy will be required.

There has been considerable discussion about unconventional monetary policy, as the RBNZ keeps pushing its main lever of conventional monetary policy, the Official Cash Rate closer to zero. The OCR currently stands at a record low of 1%. The RBNZ has its next review of the OCR next Wednesday (September 25).

The RBNZ has indicated it has work well under way on unconventional policy tools, should these be needed.

The Westpac economists have had a detailed look at the following options:

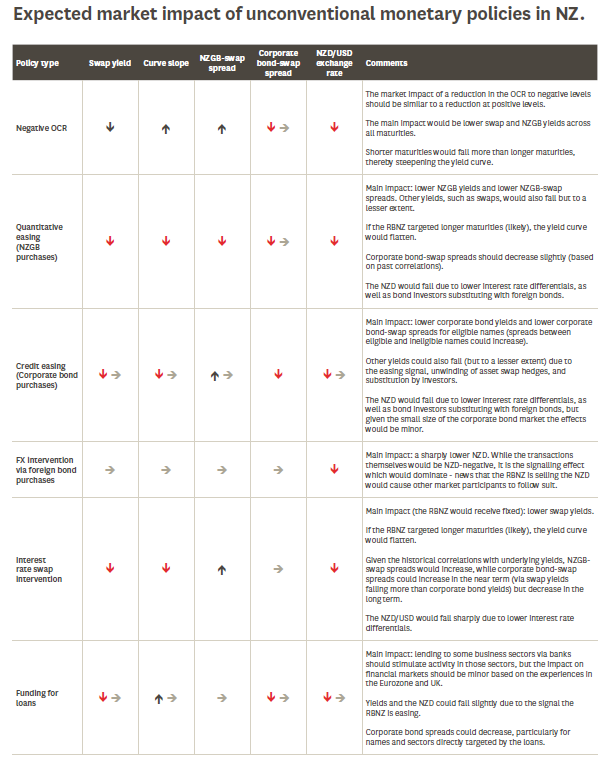

- A negative OCR

- Quantitative easing - or 'printing' money and buying government bonds with the proceeds

- Credit easing - involving 'printing' money and buying private sector bonds

- 'Unsterilised' exchange rate intervention - involving printing money and using the proceeds to buy foreign bonds

- Interest rate swap market intervention

- Funding for loans - with the RBNZ providing directly cheap funding to banks

The Westpac economists say there are "problems and unintended consequences" hidden within the detail of each brand of unconventional monetary policy.

"We argue that the key challenges with negative interest rates and quantitative easing are surmountable with careful policy design.

"However, the unintended distortions associated with credit easing or directly lending to banks probably make these policies unpalatable in the New Zealand context."

The economists point out that the more general criticisms of unconventional monetary easing – that it is distortionary, it favours borrowers, it pushes up asset prices – actually apply equally to conventional monetary easing.

"These are unpleasant side effects, but the economy is still better off taking its monetary medicine than not."

The economists say that in New Zealand, unconventional monetary policy would do much of its work via the exchange rate.

"This contrasts with some of the big safe haven countries that have used unconventional monetary policy. In those countries, the exchange rate tends to play a less helpful role in targeting inflation than in New Zealand.

"The first cab off the unconventional policy rank would probably be a negative OCR. We think the OCR could viably be reduced to around -1%, although its effectiveness would diminish as it approached that mark. Retail interest rates would not go negative – overseas experience suggests deposit rates would end up fractionally above zero, while retail mortgage rates would land in the range of two to three percent. We don’t expect there would be any difficulty with banks funding themselves despite a negative OCR."

They say the "next weapon" in the RBNZ’s arsenal would be quantitative easing (QE), which roughly translates as printing money to buy government bonds. A key impact would be to push the exchange rate down as investors are deterred from New Zealand and instead invest overseas.

"One intriguing possibility is for the RBNZ to just ‘print money’ and buy foreign bonds directly, which would amount to Unsterilised exchange rate intervention."

The final option they see as viable is the RBNZ intervening directly in interest rate swap markets to push fixed rates down. This would particularly suit the New Zealand context where swap markets are well developed, although it does expose the RBNZ to some risk of losses.

The economist say policies that have been used overseas but are less likely to find favour in New Zealand are credit easing (‘printing money’ to buy private sector bonds) and funding for loans (lending directly to banks in return for banks undertaking to on-lend to the private sector).

"Both have the potential to ‘pick winners’ and create distortions in the economy, which we think the RBNZ will shy away from. These policies would more likely be used in a crisis situation than in pursuit of the inflation target."

The economists have produced the following table that highlights their expected impacts of the various unconventional policies that might be applied:

12 Comments

Prediction: none of it will 'work'.

Perhaps the failure is that economics doesn't teach what 'work' actually is. It's somewhat tragifunny, watching global events unfold and seeing the emanations from the finance sector and the media, so far adrift as to be increasingly irrelevant.

Kicking the can down the road...

A couple of months ago it was, 'no issues here' now it's 'sweet as, yes it's going to be tough but we have the tools'.

Quite a turn arround in a short amount of time.

It's not going to be the slow side as predicted, if they change their tune that fast.

That would be why the bank sent a letter asking if we wanted to fix mortgage at 3.65%. Haha trying to lock in some $$$ for the impending rates race to the bottom

Just me, or does this sound like a junkie saying "One last big hit and I'll never touch the stuff again..."?

First, let's see how the US Federal Reserve handles it's current dilemma, after a few rounds of obviously failed unconventional monetary actions spilled over to destabilise the regular garden variety policy tool.

But now in 2019 we have an even bigger problem. It is the repo rate which is in control rather than the other way around. As repo gets crazy, it is making fed funds crazy, too. The one which is supposed to be influenced is doing the influencing.

And the central bank can and will only react if that influence is sufficient to break its own rules which were designed looking at everything backward.

So, the mainstream media will focus on “technical factors” that everyone and their mother knows is on the calendar especially each and every September (Lehman ring any bells?) and practically no one will ask, why this time? What has changed in 2019 that is making repo go insane and spillover into fed funds?

The only answer we’ve been given is, ironically, UST’s. This one guy at Credit Suisse keeps saying that primary dealers are being stuck holding treasuries they are forced by law to buy at auction, funding them in repo, and that combined with “technical factors” is how yesterday and today resulted. Dealers, whose entire job is to find buyers for these assets, we are supposed to believe cannot find any among a public which overwhelmingly wants to buy UST’s at nearly any price (thus, the yield distortions along the UST curve).

Including bills.

Everything is backward, explaining much about the current trajectory (heading no place good). That includes an overnight repo operation that has less to do with repo than you are meant to think. The overriding problem, where it all goes wrong, is incredibly simple but intuitively a very difficult hurdle to overcome. Some people will never accept it no matter how much evidence continues to pile up.

Central banks are not central. Link

You would have lost many with this, but in short the banksters Ponzi scheme is almost over. They have run out of buyers for their toxic paper trading system.

Kind of, its more the glut of US Treasuries due to ever increasing deficits that is causing the USD liquidity issues which caused the repo market to blow out. Interestingly the one of the ways to deal with this is more unconventional monetarily policy in the form of QE. More QE is probably just kicking the can down the road however till the US deals with the underlying issues with its economy.

Youngdumbandbroke, we had the same earnest vigour from our bank keen to lock in a rollover at current fixed rates. I think they were a bit surprised and disappointed I said nah, wait and float for a bit. Had to congratulate them for really trying though.

No doubt they would have suckered in a few to fix their rate

So the mechanism is as follows. The NZD falls hard. Foreigners become highly incentivised to buy housing and this corresponds to a real cash injection into the NZ economy, but at the expense of non house owners who're on the other side of that wealth transfer. RBNZ buys bonds from penson funds and the like, but they can only use the money to buy other assets like shares, so current holders of stock assets benefit.

Monetary Policy is an Oxymoron, as witnessed during the last decade.

"These are unpleasant side effects, but the economy is still better off taking its monetary medicine than not."

Better off for asset owners, sure. There is plenty of 'inflation' going on already if you open your eyes.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.