Reserve Bank (RBNZ) Governor Adrian Orr has provided a reminder the central bank might not have to loosen the monetary policy tap by as much as it has said it could.

Specifically, the RBNZ might not have to buy as many New Zealand Government Bonds as a part of its quantitative easing or Large-Scale Asset Purchase (LSAP) programme as it’s able to under an indemnity provided by Finance Minister Grant Robertson.

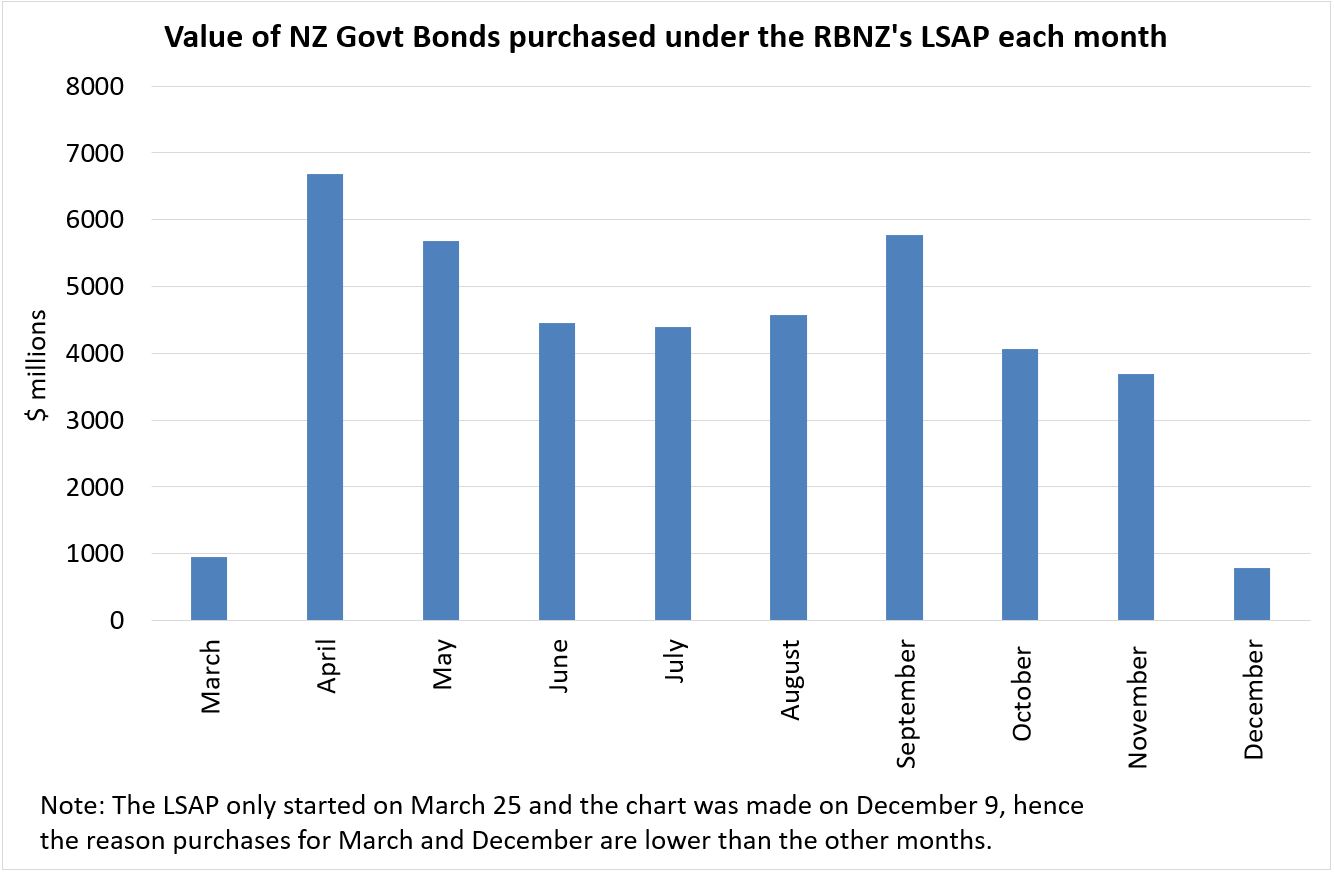

The RBNZ in August extended the LSAP programme, committing to buying “up to” $100 billion of mostly New Zealand Government Bonds on the secondary market by June 2022.

Robertson agreed the RBNZ could buy up to 60% of outstanding New Zealand Government Bonds on issue.

The LSAP is one of the tools the RBNZ is using (in addition to the Official Cash Rate and its new Funding for Lending Programme) to lower interest rates in a bid to boost inflation and employment in line with its mandate.

Some RBNZ critics have suggested the central bank has gone too far lowering interest rates, adding fuel to the already hot housing market.

Asked by National’s shadow Treasurer Andrew Bayly, at a Finance and Expenditure Select Committee meeting on Wednesday, why the LSAP programme was relatively large by international standards, Orr pointed out there was a difference between how many bonds the RBNZ had bought under the LSAP programme, versus how many it could buy.

“What we have done to date is well short of what we’re capable of doing with our current LSAP programme and Funding for Lending Programme. We want to make sure the potential is there to be able to manage all possible outcomes,” Orr said.

Later in the meeting Orr clarified the LSAP programme remained a “key part” of the Monetary Policy Committee’s toolkit.

But when asked whether the current bond-buying “momentum” would continue, Orr said: “No. We can tailor the amount of monetary stimulus based on the situation.”

Since the LSAP was launched in late March, the RBNZ has bought $41.0 billion worth of New Zealand Government Bonds and $1.6 billion of Local Government Funding Agency bonds.

Should it keep buying bonds until June 2022, it will need to slow the rate at which it does so to avoid breaching that $100 billion cap.

This is unsurprising, as the RBNZ been clear from the start it’s front-loading its bond purchasing.

The RBNZ’s purchase rate has already inched lower:

It is also worth noting the LSAP programme could be constrained if Treasury doesn’t issue as many bonds (debt) as indicated earlier in the year. This could happen if the economy continues to perform better than expected and/or if the government sees less need to borrow to help cover new spending and investment.

Already, Treasury in September lowered its 2020/21 forecast bond issuance programme to $50 billion. In May, this forecast sat at $60 billion.

If Treasury pulls back further and issues fewer bonds than expected by the RBNZ in August, when the LSAP programme was extended, the LSAP programme might hit its 60% limit before hitting its $100 billion limit.

The RBNZ could, with the agreement of the Finance Minister, change these limits, keeping in mind the fact it’s buying bonds to meet its inflation and employment targets, not to finance the government.

However it still has room to further try to suppress interest rates by lowering the Official Cash Rate into negative territory.

103 Comments

Resign, take simple job an go to auction room, you will understand you are wrong the very next day

22/01/21 will decide Orr's fate. CPI between 1 and 3% = job well done.

https://www.stats.govt.nz/indicators/consumers-price-index-cpi?gclid=Cj…

Fully agreed, once the CPI into that band, 2021-25 NZ will be sweet as, so still more room to go down for OCR if not mistaken it's close/lower than minimum, reported couple weeks back (correct me if wrong here).

The unemployment is being mandated to RBNZ from 2018? - so expect more permanent guarantee of flexiwages subsidy, govt will administer it. The housing cost, is irrelevant to the CPI - means? this is the golden opportunity by RBNZ to increase their stimulus, NZ housing cost is rated poorly compare to Hong Kong, Singapore & Shanghai, look how stable wealth grow in their economy with the higher housing cost.

You only notice how high housing prices those cities got and how stable the wealth grow in those economy. But do you know their economy structures, their political systems and cultures? You can't just compare those cities with New Zealand's cities blindly and think their housing prices are much higher, we got more room to grow. It just doesn't work that way. All of them are Global Financial Centres. But New Zealand hasn't got one.

Come on.

It is not Orr's fault that house price is soaring.

It is Orr's credit that the economy is still floating and no mass lay off yet.

You appear to be confusing monetary policy and fiscal policy. The RB does not control fiscal policy.

KeithW

There was a question to Orr about whether Housing enjoys a privileged position amongst assets (through fiscal, monetary and taxation), he conveniently batted the question away as too broad and outside his remit.

The question needs to be:

Will the RBNZ always rush to housing's aid (through QE, removal of LVRs etc etc etc) if prices are at risk of falling lest the almighty 'wealth effect' is under threat??

That would be a simple "no" for Orr.

As I commented elsewhere a while ago, the perverse incentive these 'guardians of our economy' are creating for asset speculation is killing more productive enterprises than creating.

Several industrial SME owners in my town are mulling an abrupt exit/early retirement. Even an 8-10% pre-tax annual return on equity in long-run from these enterprises can't compete with the multiples they could make on their initial investment tax-free by shutting shop and selling their land to housing developers.

We'll soon have more houses in my town at the cost of the jobs that are supposed to pay for them.

As I commented elsewhere a while ago, the perverse incentive these 'guardians of our economy' are creating for asset speculation is killing more productive enterprises than creating

Not their concern. The ruling elite promotes housing bubbles because of the positive impacts on consumer spending. That is their primary concern. Furthermore, SMEs' ability to borrow is influenced to a large extend by house prices.

Isn't Industrial land typically zoned separately from Residential land?

Seen quite a bit of commercial/residential mix, but never industrial/residential.

Is this really a thing?

Lets face it, there is no return to normal. The world is riddled with debt and even the slightest removal of QE and rates increasing will cause the Global financial system to go into cardiac arrest like it did in August / September 2019.

That is precisely what is needed

Maybe he should look at doing a cash drop somewhere in the cbd ?

Would be good if they could gift something to the poor. Pinocchio Ardern says the poor will just to have to tough it out. She's done all she can do.

OPINION: I tried to extract some value from this morning's select committee meeting to do this financial type of story. But I want to highlight my observation that some committee members displayed a complete lack of understanding of how the RBNZ works.

The committee has only just been formed, but some members confused fiscal and monetary policy, didn't seem to realise that QE has also seen some share prices soar (in addition to house prices), and didn't grasp the fact that while the Funding for Lending Programme is a liquidity tool, it's being deployed to lower interest rates. I accept these are tricky topics, but think the public deserves better.

To their credit, National MP Nicola Willis and the Green Party's Chloe Swarbrick get it and had done their homework.

But Orr and his colleagues spent much of the time explaining the basics, all the while somewhat impatiently and defensively batting away questions that inferred the RBNZ was responsible for the housing crisis - which it has of course played a key part in fuelling.

A truly frustrating 50 minutes! Stuff captured the mood well in this piece.

The questions around deciding where the funding goes to (agriculture and SME's) - a bit painful. But does make me wonder, at what point do we just do away with retail banks and let the central bank lend directly where it wants and the quantity that it wants. Given the control that central banks have over markets now, we may as well just admit we're not free market society any longer and perhaps should just go full communism on everything and set prices for everything...(it appears to be the way we're going).

Jesus christ... I already knew that the public was mostly financially illiterate, but I expected more from the people in these positions.

We're doomed.

Yes you are doomed theres one answer the first two words.

Jenée

Your second to last paragraph of your comment implies that you think the RB is not responisble for the housing crisis. It is correct that the shortage of houses is not caused by monetary policy. But the recent inflation of house prices is directly related to monetary policy.

KeithW

Hi Keith, I didn't mean to imply this. I agree with your statement and have added a line to my comment for clarity. Cheers.

....Funding for Lending Programme is a liquidity tool, it's being deployed to lower interest rates.

The result of successful stimulus is higher rates. Central banks know higher interest rates would confirm their success with monetary policies but in their absence keep calling low interest rates “stimulus” so as to stave off questions about their performance.

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar. Link

Low interest rates aren’t a central bank providing accommodation, they are instead its worst nightmare being shoved right back in their face. Well, our worst nightmare because for one thing despite repeated failures, rates that never rise testifying to that failure, central bankers are never held to account. Link

{kind=link}

"But I want to highlight my observation that some committee members displayed a complete lack of understanding of how the RBNZ works"

This is pretty true in all area's of politics, civil service and even in the commercial world - it's jobs for the boys. Have a look at the Boards of our SOE's, industry groups etc, never meritocratic appointments. They don't want anyone who may ask difficult questions or challenge management. The RBNZ Board is a patsy Board, completely at the mercy of Orr.

Hi Jenée,

Great work as usual. It's good to see we still have people working in the media who understand these topics and are willing to hold those in power to account.

I am constantly surprised that no one is challenging RBNZ on their systemic risks to our financial system of what is now a housing market bubble. Numerous papers from RBNZ over time have highlighted the risk of these sorts of bubbles and how they will create deeper and more severe recessions.

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Bulleti…

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Bulleti…

Quotes from the papers:

" I’ve noted that, to some extent, monetary policy aimed at

keeping consumer price inflation under control automatically

takes asset prices into account in terms of their effect on

general price inflation. However, even so, sometimes asset

price bubbles occur, causing economic damage. I’ve

suggested there are some very limited circumstances where

monetary policy should look beyond the immediate inflation

outlook and respond more vigorously to asset price

developments. I have also noted that this carries risks and is

difficult to do. And I’ve recorded that the New Zealand to

constrain an asset bubble would certainly not be flavour

of the month because everyone loves a bubble on the way

up. Still, central bankers are required to think-long term

and sometimes that means taking decisions that won’t be

welcomed at the time but, in the longer-term, are in the

public interest"

"• Financial excess reflected in overvalued asset prices, or

indeed the subsequent financial fragility, often seems to

be associated with some of the deeper recessions here

and abroad. Doubts about continuing access to credit

markets can exacerbate any downturn.

• Substantial slowdowns tend to lead to net migration

outflows, which in turn deepen the downturn. The

effects of fluctuations in migration are most immediately

apparent in the housing market."

Jenée - not sure if you read all the comments but if you do, the next time you might have question time with the PM could you ask:

A recent poll indicated that 75% of kiwis want house prices to fall in order to improve affordability (per the poll in the news last night). How and why do you have the view that the majority of kiwis want house prices to rise if it appears that simply isn't true?

(based on the poll, the PM is basing her political stance off a false narrative - which is a very dangerous thing to do....we'll end up like the United States if we head down that path. Not sure who is advising her on this but she needs to get some better advice...pronto).

What poll are you referring to IO, do you have a link please?

Was on the 6pm news last night but can't find a link - anyone have one? (see Jenee's link to question time below also).

I'm just thinking with most kiwis owning their home, would there really be 75% of people wanting to see house prices drop?

I would be happy to come out perfectly square on what I paid for mine, which was ridiculous to start with. I'm paying down a mortgage and building up equity as I go. If people feel like sulking because you're not constantly getting an unsustainable gain, then owning assets might not be for them.

I have a solution for you, take out your mortgage in gold/bitcoin. That way when you come to convert your monthly salary into gold to pay the mortgage, it will cost you more and more of your salary. This salary loss will go a long way to get rid of your capital gain.

Or, you could accept that a fiat currency is a sh++ store of value and your house price increase is just preserving your purchasing power.

I have a solution for you, take out your mortgage in gold/bitcoin.....

Not sure if you're being ironic or not, but fiat currency is created through lending in the mortgage market. BTC is deflationary whereas fiat is inflationary. But your point is taken. The RBNZ is trashing the dollar without anyone one protesting about it.

However, the bad news. Thinking that buying NZ houses is the secret to protecting oneself against monetary destruction is somewhat foolhardy. While now it all seems like beer and skittles, there is no historical precedent of asset bubbles preserving wealth.

For those who only own one home why would they care what their latest valuation is if they have to buy/sell into the same market? It doesn't matter to them. But they probably have children and would like them to be able to afford a home one day - hence why even homeowners would say they don't mind prices dropping. I know of many family members who only own one home - they couldn't give a fuck if house prices fell 50%, because that means they one they would like to move to is also 50% cheaper. They're mortgage free so couldn't care what house prices do because they know they have to buy and sell in the same market. But they can see the damage that is being done to younger people who are being forced to take $500,000 mortgages to buy a shit box.

99.5% correct and right on the nail IO. The 0.5%? That's how much has to be borrowed for the mortgage. the higher the house prices are if a home owner sells, it is usually to move up, so a cheaper overall market means less has to be borrowed. A factor in this is also that wages and salaries have definitely not kept up with housing, so the impact of servicing bigger mortgages means less cash for other stuff. So significantly cheaper house prices means everyone benefits, except perhaps the RE agents.

I intended to sell in Nov. However, the massive price rises mean I won't be. The margin to get into a property a little more desirable is now more than my original purchase price. Why would i go from mortgage free to loose my freedom to a bwanker again?

This is why higher and higher prices are not a good thing. Inevitably they will stall the economy.

With the majority of those Kiwis owning only one home, and having on average paid a much lower price for it than it is worth today, why wouldn't they? It's not hard to fathom that they might want lower house prices for their children or grandchildren's sake.

I would suggest only those who own two or more houses are really any better off with house price inflation.

Exactly - for those with one it doesn't matter (as long as any fall doesn't put people into negative equity and they need to move/lose income etc - but what have we just done - loaned a bunch of money to FHB's at low LVR's...)

Jo owns a house Pete doesn't, if house prices go up Jo is better off than Pete. The opposite holds true if house prices drop

Pete is Jo’s son - get it?

What a strange comment.

It would depend how much prices drop, how much equity Jo had, what their incomes are, what if any other investments either of them have etc etc.

Just thought I'd simplify it so most can understand, looks like you still don't get it

Sorry, you're a knob, and a not very smart one at that

I love you too Fritz

Tbh alot of people rely on their homes increasing in value to support their lifestyle - taking out additional loans to make purchases (cars,boats,holidays etc). Many small businesses also rely on this to increase their cashflow etc. It's a bad cycle but that's the 'wealth effect' our mate Orr talks about.

Sorry Yvil, I'm confused too (no sarcasm). If Jo decides to sell s/he presumably will buy in the same market and pay an equally increased price

Unless Jo is exiting the property market I don't see the win?

Jo owns her house, it goes up $1 million in 10 years, she then has $1 million more to her name.

Pete rents, in 10 years he has no more than today.

So in 10 years time Jo is $1 million better off than Pete

Haha but then Jo isn't any better off because in terms of buying power in that market (the housing market) Jo has gone nowhere.

It's like saying I'm going to make $10 now worth $100 (i.e. inflation) because I like big numbers, but I like buying Big Macs as well, but they've gone from $3 to $30 in the same time. I can still only buy 3 big macs.

And at the same time we've said hey those people who don't have any money, because you didn't have $10, you now don't have $100, but the big macs, if you wanted one, are still worth $30 so you can never have mcdonalds now even if you dreamed of having it.

Why does Jo have to buy in the same market? Jo owns a home in Auckland worth $500k, 5 years later Jo sells house for $1m and buys a $500k house in Dunedin. Banks the other $500k.

Also as equity increases in the house Jo has access to more borrowing opportunities and/or lower interest rates. If prices drop Jo's equity could disappear and that could risk intervention by the lender e.g. more security, increased repayment obligations, forced sale.

I thought it was pretty obvious anyone who owns a thing would prefer that thing to increase in value.

They try so hard to complicate things to make themselves feel better.

It's not difficult, Jo who owns a house that goes up in value will be better off than Pete who rents. A 10 year old kid understands that

'It's not difficult, Jo who owns a house that goes up in value will be better off than Pete who rents. A 10 year old kid understands that'

Is that why you understand that line of thinking but not the other?

I know someone who sold up and moved to Dunedin recently - they didn't get a lot of change from the sale of their Wellington property so to all intents it was the same market, prices have risen sharply in many cities outside of Auckland too.

Its a bit like birds deciding to shit in their nest - some actually like their children and their welfare so they don't do it. Other's just prefer the $500k in equity they've gained. We can each chose our moral perspective on these issues.

Ah, I see, thanks. So Pete has acquired no asset and has spent 10 years helping someone else build theirs.

Yup - essentially, Jo is now able to borrow Pete's future earnings. Maybe better for Jo, but collectively, they are worse off than they would have been if that money has stayed earnings rather than been priced into an asset where it now has to be borrowed from a bank to be accessed.

Jo is better off for two reasons: if she's freehold, she can borrow up to 800k at a low interest rate. Also, she can (probably within a few months) access a million dollars if she needs/wants to.

But the problem with massive house rises is we are essentially trading one person being able to borrow hundreds of thousands for another person having to borrow that to get an equivalent amenity. No new wealth is really added.

Jo owns a house so she is already better off than Pete. If prices go up, Jo is in the same position unless she decides to become homeless. Jo also worries about how her kids will ever own their own house, and how she cannot afford a larger house which she might need, and the inevitable drop in living standards for everyone over time as income has reduced in value.

There's another option to owning a house or being homeless, it's called renting and that's what Pete is doing, missing out on all the tax free capital gain Jo is getting.

Also Jo does not have to worry about her kids as they will inherit her house when she passes away.

This debate about Jo and Pete is ridiculous haha. There's so many variables to who would be better off. What happens if Pete owns a multimillion dollar company, has a heap of shares and rents on a lavish house paying $2k per week. What if Jo is 60 and works part time, is unable to use any equity because the bank won't give her a loan. She can't sell because she wants to remain living in the same location for family and prices have escalated.

Where's the detail in these examples Yvil? Way too simplistic...

Yvil your true colors are showing again...might be time to remind us of all the charity work (your wife) does.

Yes the true colour of a person who uses simple logic over subjective wishful thinking.

Oh that Yvil guy is so bad because he describes things as they are rather than as people think they should be.

Note I never say that house prices going up are good or bad.

No your comments don’t reveal simple logic, to the contrary. They reveal that you are tone deaf and simply out of touch with the majority. Your query as to why 75% of homeowners want house prices to drop to improve affordability is just another example of a comment of yours that highlights your moral failings.

I guess not all of us are evil and we'd like our children to be able to afford a house one day. And therefore we do want to see prices drop.

And not only for our children, but also for the good of the average person who has been priced out.

I'm yet to see the advantage to the country of buying a house and getting yourself a million dollar mortgage that ties you to the bank for 30 years.

Higher value will probably let 75% of NZrs to feel wealthier(as per rbnz’s intention) however it will lead to higher council rates, insurance etc ( real effect) So in reality all just start to pay more, as if they sell the house they buy in the same market. So in reality only RE and private house flippers are benefiting

Andreas

Your assertion “Higher values . . . lead to higher council rates” is not correct.

Are you able to explain why this is not correct or is it you don’t you know why it is not correct?

Rates are calculated based on RV , so next RV revaluation will bring rates up, where am I wrong?

Andreas

Wrong/fail.

So you really don’t know why your assertion is not correct. :)

I’ll help you out with a leading but realistic simple scenario.

My 2020 RV is 30% higher than my 2017 RV. However, despite this increase in property value my rates next year fall compared to this year even though council rate take goes up 5%.

A very simple answer as to how this can be possible.

So what is the answer (and it’s a real case and not a riddle)?

Hint: If you know how councils determine rates you will know the answer and as to why your assertion that if a property increases in value it doesn’t necessarily mean that one’s rates go up.

Andreas

Ah . . . I see you give up. :)

So, you really don't understand why your assertion is not a valid premise and this is confirmed in your response.

Just because one's RV (as a measure of property value) goes up, it does not in itself mean that one's council rates goes up.

In the example I gave, even though my RV went up 30% if properties in my council area on average rose by 40% I would be paying proportionally less of the share of rates - and provided council didn't increase their total rate take I would be paying less rates.

How council determine rates is that they budget the total required and - simply - apportion these on a pro rata basis of RV or estimated property value (that is why it is called ratable value) for which they calculate a multiplier which - simply - is the total ratable value of all properties divided by the required rate take.

Just because properties RVs go up by 40% it certainly doesn't mean that rates go up by 40%.

Your response "so next RV revaluation will bring rates up" is another assertion that is not a valid premise.

Look at the positive - at least you have learnt something today.

Cheers

Christ you’re a sad individual. Let me guess, you were bullied at school?

I've noticed a strange correlation between property investors (P8 was property investors association member wasn't he?) and narcissistic personality disorder.

Here are the signs to look out for:

https://lh3.googleusercontent.com/proxy/Tbu_IfznxUX5Fny1N79rgJOctuCr_oZ…

P8, you've made a mistake above. A premise cant be valid or invalid. Arguments are valid or invalid. Premises are true or false.

So, lucky you - you've learnt something today too!

So according to your logic , your rates didn’t go up after 2017 revaluation as well ? Let’s say 2015 vs 2018 ?

andreas

You really aren't getting it.

RVs are not responsible for rates going up - council increase in their total rate take (what they budget or want to spend) is responsible for that. One's RV simply determines the share of the rates and if your RV goes up by the same as the average your share of the rates will not - just simply by any increase in council rate take.

To put it simply which you really need to get your head around:

- Increase in RV as a measure of house price increase do not increase rates as you wrongly assert

- Increase in rates are due to councils increasing their rate takes (the amount they spend)

- RV simply determine as to how these are shared.

A 10% or 40% increase in RV is not going to increase your rates by 10% or 40%.

Your rates going up since 1960, 1970, 1980, 1990 or whenever is simply due to councils increasing their total rate take and not increasing RV.

You need to look at your rate bill and you should see a multiplier for a variety of rateable factors - that multiplier changes from year to year.

you did not quite answer the question about your rates 2015 vs 2018 ?

Re:"A 10% or 40% increase in RV is not going to increase your rates by 10% or 40%." no , they are milking you a bit slower, otherwise Jetstar would be superstar as would be flooded with one way tickets purchases

and read this https://www.aucklandcouncil.govt.nz/property-rates-valuations/our-valua…

Yes this is Auckland Council's one of main pages , the say it in the very top paragraph

"A rating valuation is a three-yearly assessment of a property's value and is determined by house sale prices on a specific date. We use these valuations as a guide for setting your rates."

Andreas

Stop digging that hole.

Cheers

very constructive, you answered all questions

Cheers

Wish you well - a commonly misunderstood facet.

Just a note from the Auckland Council page your referred to

"Effect of a revaluation on property rates

An adjustment in a property's capital value does not mean that property rates will automatically change.'

yeah, sure, some properties are more equal than equal

by Audaxes | 8th Dec 20, 6:21pm

by Ocelot | 8th Dec 20, 12:19pm

I think using the household stat is very deceptive. I live in an owner occupied house as a boarder, so I'm included in the owner occupier stat. I think this article from 2014 shines a light on the true situation.

https://www.interest.co.nz/property/69025/census-figures-show-home-owne…

Home ownership by adults fell below 50% in 2013, and for under 40's fell to 22%.

I'm another who would happily not have a house worth twice what I paid for it many years ago, if it meant that my adult children had something approximating the chance I had at home ownership thirty years ago, when my first house was purchased for a figure ($40,500) within cooee of my annual (working class) income ($40,000).

Can I second that.

We bought our first home stupid late, about 6 years back after 17 years of renting. We just squeaked on to the property ladder, another couple of months and we would have missed the boat.

Our RV is 50% up on when we bought but that does nothing for our monthly finances or feeling of security, and even less because that same effect means my best mate since college is going to be a life long renter with nothing to pass on to his kids.

Cash in, then move to OZ? read this today:

https://www.stuff.co.nz/national/education/300179542/results-in-maths-a…

Your kids have more opportunity to study, learn, earn, pay for reasonable housing with wages - NZ is currently very discriminatory on their policy.

For sure it's not like what happens in the past in different countries, but do read/listen/watch any news in NZ for a week? then you'll get it.

Yes

How many of those home owners have kids should answer your question.

How many of those home owners owned multiple, empty dwellings? - C'mon leave the RBNZ bring the OCR into negative, you already seen how the money distributors feel, and even react to self impose the LVR into 30-50 etc. more good times ahead if RBNZ steadfast with their current moves. You can't correct things by keep on tinkering and not achieve any significant changes, RBNZ clearly can.. the more they amplified their current 2020 actions span towards 2025 in distributed way, the much better it is for NZ.

Honestly, I'm thinking that RBNZ & govt decision are like Chemotherapy, is a good enough treatment NOT to kill the patient, cancer is the target. Painful, but yea.. got to do it.

From 60%? home ownership to 75%? - clearly for increase the potential investment of current 20% soon after RBNZ stimulus & removal LVR is a good things for Kiwis, agree with you there.. what we need 2021-25 is clearly to have more home ownership towards 100% with assurances of no price correction to be allowed by govt & RBNZ, this is where their intertwined policy of essentials subsidy, bail out, hand out, stimulus, deferral etc. need to be carefully re-wording.. my amateur estimate, this can only be achieved for yearly increased of 20% every year towards 2025. So the next stimulus roll out must be equate to the amount for this 2020, But most importantly? change the acronyms. That's the key.

I would be happy for them to drop and I own several houses. I think any homeowners with adult kids would also be happy to see house prices drop. It's not much fun watching your kids struggle to pay rent in today's world. I know when my kids are ready to buy a house I will need to help them with substantial deposits or accept they are probably look overseas to build a better life. I have bought a house recently with the sole purpose of selling to fund their deposit when they are ready.

I understand that a lot of people won't be able to do this for their kids and will either have to watch them struggling to make ends meet or leave the country.

So yes, I think a lot of homeowners would be happy to see the value of their houses drop if it means that their kids are more easily able to get into their first house.

Lucky Ptolemy, one of the Central Banks chosen winners. Welcome to the club as one of the new landed gentry. Once you help your children out, they will then be second generation landed gentry and will curiously wonder why their friends did not get help from their parents and simply follow in your footsteps, leveraging the land you have paid for in multiples to push out more potential FHBs. By the third generation all vestiges of empathy will be forgotten and your grandchildren will be uncaring slumlords.

Although I just re-read your comment. There is far too much compassion in your comment and not enough blaming of young people for eating avocado. There is also far too much understanding on what has caused this. Until you begin to deny all of these things and simply enjoy your privileged place, you cannot be part of the landed gentry and your club card is revoked.

The answer is a resounding, unequivocal yes.

I own a mortgage-free family house in a central Auckland area that I bought in 1999 and where I still live, and a small mortgage-free 2-bed unit, still in Auckland Central, that I bought a few years ago for my daughter.

Do I feel that I got "richer" just because of the ridiculous house price increases in the last 20 years, that saw my properties increase in value beyond and realistic level ? Not at all.

But I would be delighted to see a decrease in house prices. And quite a few colleague/friends I know find themselves a situation not dissimilar to mine and they agree with me on this. Some people do worry about the next generations, and the perilous and unbalanced state of the NZ financial system, more and more reliant on the NZ housing Ponzi. When the bubble burst, unfortunately it will pose a serious risk to the real economy too.

Correct, it was on the 6:00pm news.

It said that 75% of Kiwis want a reduction in house prices.

I think he asked himself , 4 times .

Good question thanks. Julie Anne Genter asked Grant Robertson a similar question in the house today. You can see this at 1min 40sec here:

Thanks Jenée - feel's like we're going around in circles with this. What a shambles.

The spin doctors must be working over time for Labour. They're all getting good at avoiding the questions.

They obviously watched Teflon John for 9 years and picked up a few ideas.

Jacindas stooge is a slippery little bugger isn't he.

He didn't actually answer half of JAG's question, should be pulled up for that and told to answer.

How about, question to PM to state the ideal number of relative to income affordability/DTI for NZ, where she thought it should be at? - Because, if no one would bring the equation closer from housing side, then may be? it's for govt to doubling the salary figures? .. it's just a number right? - oups, silly soon as that happening.. the other side of equation will be automatically tripling, we call it proportional balancing.

The devaluing of waged and salaried labour continues.

Just wait for us to crank back up to 50K+ arrivals to make up for lost time.

Pretty sure the floodgates will open again very soon. It will simply be a case of show us your vaccination card and your in. Its pretty obvious that the government equates immigration with "Growth in the economy" so lets get it moving.

Read your comment then saw this in stuff.

https://i.stuff.co.nz/business/123644402/kiwifruit-company-fined-230000…

Devaluing of labour on so many levels.

A comment from the authority interested me.

"Those most affected were migrant workers".

Not true indirectly this affects every single participant in the labour market. And definitely a common occurrence.

The LSAP is one of the tools the RBNZ is using (in addition to the Official Cash Rate and its new Funding for Lending Programme) to lower interest rates in a bid to boost inflation and employment in line with its mandate.

FLP has yet to record a transaction since its inception on Monday.

But banks’ offshore funding seems to be still intact and possibly profitable, given this recent issue of xccy basis swap counterparty hedging collateral.

World Bank capped an active year in the Kauri market with a record-breaking deal on 26 November. The issuer pursued a dual-tranche strategy designed to bring in bids from multiple investor bases, while a recent backup in New Zealand dollar yield produced a further demand bump.

WORLD BANK NZD NEW DUAL-TRANCHE 5.5YR AND 10YR KAURIS***

5.5 Year tranche:

- Firm order book in excess of NZ$1,010m (incl. JLM trading interest)

- Issuer will print a minimum NZ$1,000m trade, and is open to further upsize subject to demand and pricing

- Issued NZ$1,000m

- Pricing set at Mid swap +23bps / Yield [0.751]%

- ISIN NZIBDDT016C7

- ANZ B&D10 Year tranche:

- Firm order book in excess of NZ$350m (incl. JLM trading interest)

- Issuer will print a minimum NZ$250m trade, and is open to further upsize subject to demand and pricing

- Issued NZ$300m

- Pricing set at Mid swap +39bps / Yield [1.304]%

- ISIN NZIBDDT017C5

- ANZ B&D

Clay Pigeon shooter shouts, "Pull!" Then aims and fires the gun. Bullet hits the 'pigeon'.

Orr, "Fire! Pull ..."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.