Talk of a stronger-than-expected economic recovery prompting the Reserve Bank (RBNZ) to hike interest rates as early as next year has been making headlines.

But the thing financial markets will be looking for when the RBNZ releases its quarterly Monetary Policy Statement (MPS) on February 24, is signalling around the pace at which the central bank will keep buying government debt from banks and other investors via its quantitative easing or Large-Scale Asset Purchase (LSAP) programme.

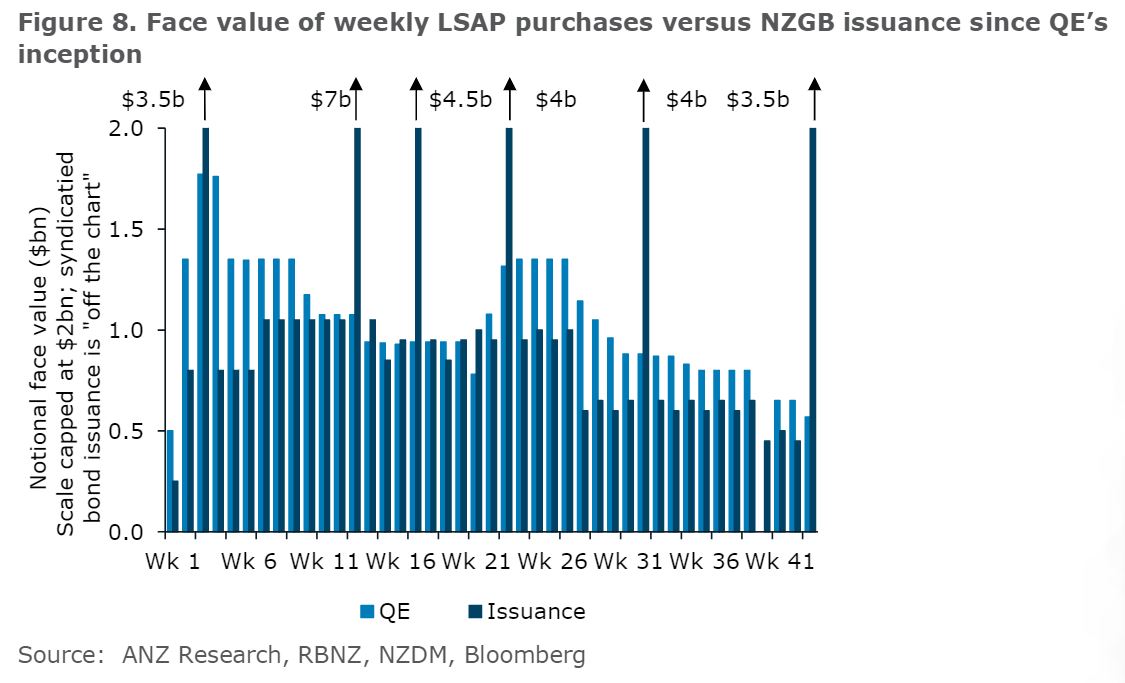

The RBNZ in August 2020 said it would effectively create money to buy up to $100 billion of mostly New Zealand Government Bonds on the secondary market by June 2022.

This $100 billion is a cap, not a target. It agreed to buy no more than 60% of the New Zealand Government Bonds on issue to avoid becoming a disproportionality large player in the market. To date, the RBNZ has bought $44.6 billion of New Zealand Government Bonds.

The point of purchasing these bonds is to lower interest rates in order to help the RBNZ boost inflation and employment in line with its mandate.

A positive side-effect of making these purchases is that it supports smooth market functioning at a time the Government is issuing a whole lot more debt than usual.

However, because the economy is performing better than expected, Treasury hasn’t been issuing as much debt as both it and the RBNZ initially expected.

Having said it would largely front-load its response, the RBNZ has also been slowing the rate at which it’s buying bonds:

ANZ senior strategist David Croy would like it to clearly communicate at the next MPS the pace at which it’s going to continue buying bonds at.

He notes the RBNZ hasn’t been clear whether it has slowed the pace because Treasury has been issuing fewer bonds, or because it believes it doesn’t need to provide as much stimulus.

Croy would like the focus to shift from the size of the LSAP to the pace of purchases. Why? Certainty.

Croy, as well as ANZ chief economist Sharon Zollner and ANZ senior economist Liz Kendall, maintain the RBNZ will extend the LSAP by six months until the end of 2022, essentially enabling the RBNZ to continue buying bonds at a slower pace, but over a longer period of time.

“Eventually, the RBNZ will look to reduce the amount of overall asset holdings by letting bonds mature and not fully (or partially) reinvesting the proceeds. This is likely to be a very gradual process,” they say.

Croy, Zollner and Kendall say the RBNZ could theoretically start hiking the Official Cash Rate (OCR) during any phase of the LSAP tapering, but will most likely wait until it stops buying bonds.

They characterise LSAP tapering as the “first cab off the rank” in terms of a return to “normality”.

They believe the OCR might start being gradually lifted in mid-2023.

The Funding for Lending Programme (FLP), which has seen the RBNZ make up to $28 billion of funding available to banks to borrow at the OCR (which is currently 0.25%), will keep ticking along.

Once again, the aim of this is to enable banks to lower interest rates. $1.14 billion has been drawn down via this programme to date.

“We expect the RBNZ will let the FLP reach its planned end from the middle of 2022. This will provide a liquidity backstop but is expected to largely operate in the background and then naturally come to an end, rather than being a key moving part in the tapering process,” Croy, Zollner and Kendall say.

But before embarking on “normalisation”, they expect the RBNZ will want to see employment, inflation and inflation expectations at, or close to, target.

“The lesson from recent history seems to be this: don’t hike too soon or your half-baked cake will collapse in on itself and you’ll have to start again,” they say.

“While formulated for slightly different reasons (ie primarily the balance of risks around impacts of the pandemic), that thinking is at the nub of the RBNZ’s “least regrets” policy. Better to run the oven hot and burn the edges of the cake slightly, the thinking goes; it’ll still be edible.”

The trio concludes: “A faster-than-expected return to inflation and employment targets would of course be welcome, but would bring its own headaches, particularly for the bond market.

“It’s a lot easier to get into unconventional monetary policy than out of it.”

35 Comments

We are already at the new normal. There is no going back.

Actually, we are on a pre-determined curve, so there is no 'normal'; normal is a linear comment.

https://www.businessinsider.com.au/the-limits-to-growth-and-beyond-2011…

But you are 100% right; there is no going back.

That little growth period, say WW2 until 1970 (my count) or until 2005/8 (the more commonly-understood inflection) is well over. Debt was wedged into the divergence to paper over the problem, but that is becoming eye-wateringly unlikely to be repayable.

Many times you have been asked on this site when is your predicted apocalypse coming, and never got a clear answer. But reading your link this time, we have a date. 2050.

So I am alright Jack.

We cannot make it to 2050. I've got it at 50% in the next three years, 100% by 2030. Early depends on mass-disillusionment, later due to resource depletions and compounding repercussions (fisheries collapse leading to land-ravaging, fuel poverty leading to forest-depletion etc) climate impacts, and the effects of Entropy on the complexity, scale and age of infrastructure (all needing maintained using said reducing resources; a compound-exponential problem)

And there are a lot of people - all someone's loved offspring - who may not thank you for such an attitude :)

I wouldn't be so pessimistic. I think people will still be around in 2050 but our quality of life will be lower and we'll have a lot more resource and environmental constraints.

Yeah there will still be people around in 2050, however the big question is how many people and what will the quality of that life be ?

ZERO chance of debt holding till 2050, or resources for that matter

Unless of course $50 million dollar houses are the norm despite $50,000 salaries...

Without debt holding supply chains are somewhat compromised to say the least

Theres only way out of this mess

We're currently living through the gradual transition now. You may have noticed how real 'growth' is almost impossible to find despite all the central banking tricks and how most people's standard of living is dropping rather than rising (cost of living / housing etc.)

Unlike in the movies, generally there is no single day where things flip from 'normal' to suddenly 'apocalypse'. History shows the usual trend is a slow decline that on retrospect looks a lot faster than it likely felt for people living through it.

You are correct, I'll re-phrase more accurately:

Our economies, as we recognise them, will not be around by 2050.

Yes, there will be humans around, living in lower numbers and at much lower consumption-levels. :)

If they start raising rates over 2 years away, it will result in a mass collapse of property, which of course is against the "financial stability" criteria of the RBNZ. Because by that time, the low rates will be completely entrenched into peoples purchases. And we are highly unlikely to get wage rises to allow increased rates. Ergo once you start a distortion, it will be nearly impossible to roll back. For reference see the US for the past decade - every time they even hint at rate increases, there is chaos and it's rolled back or some other mechanism is bought forward to replace it. QE forever.

How right you are.

The RBNZ and Government have actually ramped up the Financial Market Instability Risk of our economy by their recent actions (since 2009 at the very latest).

Increasing the Risk factor of the singular component that underpins our economy; property prices, from whatever one considers 'affordable' - say, 4 times Average Individual Income, to something approaching 10 is adding the very Instability that they say they are trying to reduce! Madness, yet they think that by doing that they are actually doing the reverse - getting us to Borrow and Spend. I repeat, madness.

Cash is slowly being replaced by bitcoin.

Every government around the world could just print cash without any limit jeopardizes he credibility, making Bitcoin solid.

Now it is trading just under 50,000 USD.

Bitcoin has a long long long way to go. Is it not only worth $1trillion in total ? The US government is looking to "Give away" $1.9 trillion in a new relief package. Personally I don't think Bitcoin will make it long term, it will be trumped by another digital currency introduced by government.

Why would you buy a digital currency introduced and controlled by a government - that's the system we have now but just swapping paper for digital. BTC will survive as no one can mess with it - but its power usage is a worry at the moment.

so you are saying the masses dont want the Govt handout?

they would rather the no handout option?

People are currently swapping fiat currency paper for Bitcoin so whats the difference ? All your current paper wealth will just get transferred to a new digital currency. Better get that cash out from under your mattress, you will have a limited amount of time to get it into the bank then after that it will all become worthless. Its every governments dream, no more tax evasion and cash jobs, the government tax take will go up significantly. Every cent issued will be traceable.

And then... Jesus will return

Those things don't logically connect.

The weakness of currencies/fear of inflation does not make Bitcoin solid.

exactly

This "logic" if you can call it that, is that fiat doesnt have limits, therefore Bitcoin is the (fixed quantity) solution.

The bitcoiners think consolidating all this purchasing power into a few hands will come once we have mass acceptance... LOL

The fiat debt is income for the masses ...

The underlying problem (leverage because of resource limits) exists. Fullstop.

Its a PHYSICS problem

Not a monetary one

Lol pumpers gotta pump :) Doesn't matter to anyone a so-called "stable coin" that's 100% centralised just printed 2 billion "USDT" in the last week to pump up the cryptos as long as the prices are going up. Their collateral? Cryptos. The basic formula is they print, buy cryptos, raise the prices of cryptos, then sell to punters who come in with real fiat. Doesn't matter to me as it's only adding to my paper gains and gonna be hodling but just a warning to people who are thinking of mortgaging themselves to the hilt to buy an entry in a fkin ledger :D

Love that "real fiat" part there mate. HFSP

The key sentence is the last one:

“It’s a lot easier to get into unconventional monetary policy than out of it.”

And hence the risk of stagflation.

KeithW

KW - read this (top post) and maybe do one of your columns on it?

powerdownkiwi,

I have been thinking about energy economics for a long time, ever since, more than 40 years ago, I was teaching a masters level course in natural resource economics. It is not as simple as using energy as the overarching numeraire. I remain inclined to the perspective that molten salt reactor (MSR) technology, probably using thorium, combined with small modular reactor (SMR) design, may well change many things. I accept that world economics will look very different in 2050 than now but I am cautious about the specifics. When I look back forty years, most of us who were applying our minds to energy economics at that time, totally misjudged the impact of new technology. I think back with some irony to the specifics of 1979, the carless days we had at that time, and some discussions I had with Bill Birch down at Scott Base in Antarctica, with Bill being a key minister, including at that time the science and energy portfolios, in the Muldoon era of 'think big' aimed at developing energy independence from imported fuel. I don't think any of us saw the world as it is today. One thing I learned from that is to be cautious about predicting the world of the future.

KeithW

Thank you for the considered reply.

In 1980, there were 4 billion planetary inhabitants. Resource consumption per head was X. Now there are 8 billion, and it would be fair to say per-head consumption is 2X. Depletion has - inevitably - trended inexorably in the direction of Entropy (it now takes the removal of 400 tons of overburden to get at a ton f copper; it once took 10 tons. The energy we apply to that removal was once of an EROEI of 100:1, now I'd rate it at 17:1 and dropping like a stone. And the infrastructure we built with has never been more, and never more in need of maintenance - which we're triaging (think lead, think pipework failures). In energy terms. efficiencies (which is all technology can do, it can't create energy) have begun to plateau - which was inevitable and predictable since Carnot tumbled to it. Thus saying 'we're OK so far is - with respect - invalid. You're OK spending 100 a week from a 1,000 bank account, until week 11, reassuring comments from week 9 are just that.

We are entering a very different epoch, not sure you and I will like it, but it'll be an interesting experience. What is needed is a complete re-think (not to be confused with a Davos reset).

Bottom line is the future is becoming more and more predictable. Many of the trends are irreversible so the final outcome becomes more and more predictable with time. To many people think that tech will come to the rescue, well it won't once we go beyond a certain point in time.

"When I look back forty years, most of us who were applying our minds to energy economics at that time, totally misjudged the impact of new technology."

Trouble is Keith, tech hasn't had ENOUGH impact. In fact its "failed" miserably to outpace diminishing returns. Instead we are basically relied on economies to scale, debt, leverage and population ponzis

Why am i so sure?

Because of the massive Debt burden started 40 years ago, necessary to keep the party going

Debt has this marvellous time shifting ability (thorugh leverage), where we can consume more today by promising EVEN more down the track...

It works until no one believes the promises

It works until citizens are told they are wealthier (eg on paper) but they know they are finding times ever harder ...

I see that ANZ are offering 3000 cashback for FHB according to an add that's popped up a different screen. Whether its a recent change to its mortgage offerings or a long standing act of kindness for FHB I am unsure.

Was it Ben Bernanke who used to call quantitative easing "extraordinary measures"? We're now well past the point where LSAP and FLP should be viewed as 'ordinary measures'.

Reserve Banks seem pretty determined to take credit creation this to its bitter conclusion regardless of the costs to society. So many economists careers and legacies have been staked on the idea that if we could just make credit a bit cheaper inflation would miraculously appear that it's become the sacred cow of economics.

Government debt issuance is a throwback to the days of the gold standard when we had a fixed supply of money but we now have a fiat currency and so it is no longer necessary. It doesn't finance the government in any case as we are lead to believe. It is all part of the neo-liberal narrative of the government as merely a currency user and of it being dependent upon the private sector for its financing.

This certainly suits the banks as they prefer not not to have any competition in the field of money creation and our high levels of private debt also means high levels of profits for them.

Economist Warren Mosler has this to say about government debt issuance.

Proposals for the Treasury

I would cease all issuance of Treasury securities. Instead any deficit spending would accumulate as excess reserve balances at the Fed. No public purpose is served by the issuance of Treasury securities with a non convertible currency and floating exchange rate policy. Issuing Treasury securities only serves to support the term structure of interest rates at higher levels than would be the case. And, as longer term rates are the realm of investment, higher term rates only serve to adversely distort the price structure of all goods and services.

I would not allow the Treasury to purchase financial assets. This should be done only by the Fed as has traditionally been the case. When the Treasury buys financial assets instead of the Fed all that changes is the reaction of the President, the Congress, the economists, and the media, as they misread the Treasury purchases of financial assets as federal ‘deficit spending’ that limits other fiscal options.

https://www.huffpost.com/entry/proposals-for-the-banking_b_432105

Mar 2023 Adrian Orr's term is over. I almost feel sorry for his replacement. Orr appears to be determined to follow his path rather than admit he was wrong.

You are so right. Orr's replacement will have to pick up the pieces, and it ain't going to be pretty. The long term effects of Orr's policy mistakes will be felt by the NZ economy and NZ financial markets for a long period of time.

The point of purchasing these bonds is to lower interest rates in order to help the RBNZ boost inflation and employment in line with its mandate.

ANZ senior strategist David Croy would like it to clearly communicate at the next MPS the pace at which it’s going to continue buying bonds at.

{kind=link}

So much for the negative OCR. ANZ is a nice contra, peak bearish back then, peak bullish now.

Cyclicality of rates shows a nice half cycle between the two periods.

So timid. They shouldn't be buying a bucks' worth of government bonds from here on out.

This constant fear of market reaction is reflexive. If markets were to build in the expectation and knowledge that central bank responses could be decisive, they wouldn't be so brittle. In the same way that coddled children become mentally weak and unable to cope with adversity, the same applies to markets.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.