Finance Minister Grant Robertson has given financial markets even more reason to bet on strengthening inflation requiring higher interest rates.

Yields on New Zealand Government Bonds rose on Thursday, following Robertson announcing the Reserve Bank (RBNZ) will be made to consider house prices when setting monetary policy and regulating financial institutions.

The RBNZ’s Monetary Policy Committee’s main objectives remain targeting inflation and employment, but a new clause has been added to its remit, requiring it to assess the effect of its decisions on the Government’s housing policy.

The news saw New Zealand Government Bond 10-year yields rise 16 basis points overnight to 1.79%, reaching 1.81% at one stage. Yields on five-year bonds were up 13 points to 1.04% and yields on two-year bonds rose 10 points to 0.36%.

NZ Government bond rates

Select chart tabs

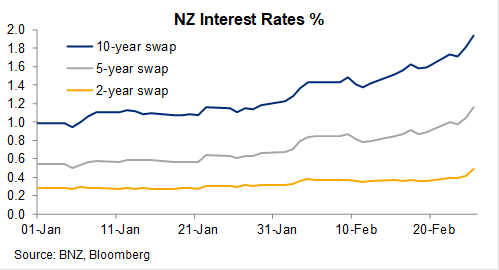

Swap rates were also higher, as per this BNZ chart:

The New Zealand dollar got as high as US74.5 cents - the highest it has been since August 2017.

All these measures point to a tightening of monetary conditions - the opposite of what the RBNZ wants.

The RBNZ was at pains to use its quarterly Monetary Policy Statement, released on Wednesday, to say it would keep interest rates low until it is confident its inflation and employment targets are not only attained, but sustained.

The RBNZ urged banks to use the support provided to them (like the Funding for Lending Programme) to keep interest rates low, even though globally markets are betting on economic growth and inflation lifting.

Markets saw through the RBNZ’s “glass half empty” tone, looked at how much its economic forecasts had improved since November, and drove bond yields and the dollar higher.

This isn't just a New Zealand phenomena. Yields on US Treasury 10-year bonds have been rising too:

US Treasury Bonds

Select chart tabs

But Robertson’s announcement added fuel to the situation. Him tweaking the Monetary Policy Committee's remit essentially signalled that with house price inflation through the roof, the RBNZ would need a very compelling reason to loosen monetary policy further.

The RBNZ late last year voiced its opposition to a house price consideration being added to it monetary policy remit, saying it “would be unlikely to result in significant policy changes.”

Governor Adrian Orr noted it already considers house prices, and if it had to make a trade-off between house prices and meeting its inflation and employment targets, it would opt for the latter.

If trade-offs were justified, the RBNZ was worried its monetary policy would be less effective. For example, higher interest rates could lead to higher borrowing and debt servicing costs and a stronger dollar.

It argued a house price clause “could also make the goal of monetary policy confusing and reduce financial market efficiency.”

Asked by interest.co.nz what he made of tightening monetary conditions, Robertson said: “That tends to move around a bit and I imagine that will settle somewhat as people think about what this actually is…

“The way money markets react to that will vary.”

61 Comments

Love the real life Shakespearean play in action. The government scapegoating RBNZ for its own fiscal delinquencies.

"If a house is divided against itself, that house cannot stand." - Mk 3:25

Watch how the entire thing collapse with folks on the street bearing the greatest misery of their lifetimes.

CWBW...picked you for more of a fire and brimstone, old testament type.

Better than even money the OCR is 1%+ by May next year?

Job 38:12

You mean only 3,821 people will have jobs?

I'm picking OCR kept very low for some time, but DTIs brought in to cool the housing market.

Orr has no choice, he’ll bring in dti tools, 1 March.

Easy now. You're getting me worked up.

Have some cold water.

And so it begins

I'm very disappointed that negative externalities might hold RBNZ back from going "full send" on the housing market. It would have been quite a thing to see if house prices could approximate the bitcoin chart. Maybe next recession, eh boys? :-)

Edit to add: "Negative externalities" seem to be the theme for this year so far from housing to global warming. Even politicians and economists are comming to the realisation that someone must do something. Perhaps it's time to change the catchphrase of the post-covid economy from "Build back better", which doesn't seem to ve living up to the hype, to "Better balanced."

"Build back better" means making houses without concrete, as the concrete is too carbon intensive

NZD now up 19% relative to USD over the past 12 months (which arguably makes the stupid housing bubble look even worse). Gold price in NZD down approx 6%. None of this really makes much sense (to me anyway). It will to people like Mike Hosking.

Over 10years still down however.

This is all turning into a real mess. Orr was overtly political from the start - making comments in 2018 that "incensed" Gerry Brownlee - and has been juicing merrily away on behalf of the people who put him there. And now I think those same people are going to push him under the bus.

Labour have totally stuffed up the Reserve Banks mandate from something that was clear-cut to now being a 3 headed hydra. They were too clever by half, and we'll all pay for it.

Adrian Orr was appointed Governor of the RBNZ in March 2018

He's good for 5 years until March 2023

You can bet he won't get another term if Labour are still aound

Orr was overtly political from the start - making comments in 2018 that "incensed" Gerry Brownlee - and has been juicing merrily away on behalf of the people who put him there.

He burst on to the scene trying to wax lyrical and sound like he was an artist, not a dogmatic bureaucrat. He's the latter. No doubt about it. And the flashy, expressive language and confidence are gone. He's even now being all cautionary about risk (related to the stupid property bubble).

https://www.rnz.co.nz/national/programmes/morningreport/audio/201877444…

Maybe because he understands what the risks are

Maybe because he understands what the risks are

Anyone can state there are risks. It doesn't mean someone fully understands the probability of and size of risk. This is a common frailty among central bankers.

TV - no, they represent us, being too clever by half, and now having to pay for it.

We all though we could consume like there was no tomorrow. Some thought they were 'winners' in the system, some though they'd be winners one day, others just accepted that they were cannon-fodder. But it was just like the Titanic; rich, poor, optimistic, pessimistic, clever, stupid - all succumbed to physics. Don't blame banks, Orr, Robertson, or even the Chicago School. They all failed to see what was coming. And the few of us who have been tracking it for decades, failed to influence the societal narrative; the Chicago-ans won that one. Sort of like winning the rights to live on the upper deck....

I suspect Orr is smart enough to understand all that but his focus is more immediate

What a colossal own goal. Robertson just increased the cost of servicing his own government debt and achieved nothing.

As for “taking advice” on debt:income measures and restricting interest only loans, come on Grunter, you’ve had 4yrs in government to think about this, and time in opposition before that.

Fine if you want to pass the buck and get the RBNZ to help solve the problems you’ve happily enabled, but at least give them the full suite of tools to do it.

"Bet on high interest-rates"

Closer to the mark than most people realise.

:)

Immovable object meet unstoppable force.

But Robertson’s announcement added fuel to the situation. Him tweaking the Monetary Policy Committee's remit essentially signalled that with house price inflation through the roof, the RBNZ would need a very compelling reason to loosen monetary policy further.

Surely the quantity of leveraged bank credit extended to residential property purchases, not the cost of it determines the capital price of this asset class. Large dollar amounts of corporate stock buy backs in the US have been credited with propelling stock prices exponentially upward over a decade or more.

I recently noted: Bank lending to housing rose from $50,788 million (48.36% of total lending) as of Jun 1998 to $292,645 million (59.71% of total lending) as of November 2020 - source ( $295,957 million of Dec 20)

.. the most important macroeconomic variable cannot be the price of money. Instead, it is its quantity. Is the quantity of money rationed by the demand or supply side? Asked differently, what is larger – the demand for money or its supply? Since money – and this includes bank money – is so useful, there is always some demand for it by someone. As a result, the short side is always the supply of money and credit. Banks ration credit even at the best of times in order to ensure that borrowers with sensible investment projects stay among the loan applicants – if rates are raised to equilibrate demand and supply, the resulting interest rate would be so high that only speculative projects would remain and banks’ loan portfolios would be too risky Link

It correlates, but doesn’t propel it.

And the amount available is determined by reserves....those reserves are mobile.

What a dog's breakfast this is, the RBNZ only just released their MPS yesterday. At least give the new investor LVR's a chance (it specifically said investors in the new clause)

The whole point of the RBNZ Act is that they are independent. Labour added the full employment clause to the RBNZ's target which requires easier policy, then add a housing target. Good grief.... What can the RBNZ do about immigration or council red tape?

The whole point of the RBNZ Act is that they are independent

The RBNZ needs to be challenged by those who give them efficacy because of past and current failings.

That means the citizens and the politicians they empower.

QE is hardly harnessing the NZD and the 10 year NZ government bond yield rise.

We need to immediately call into question the veracity of unconventional central bank policy actions (QE) based on evidence.

Interest rates to go up, housing supply to go up, prices to go down.

This government wants you to remember them with Jacinda sound bites like “Kiwis expect house prices to go up” and Robertson publicly blaming RBNZ for this mess. Buckle up because it’s about to get messy. But remember Labour come next election because they said all the right things just before it all came crashing down.

As a FHB I hope you’re right and that what we can currently buy for 700k we can get something at least a little more liveable.

Oh you think something for 1 Mil is suddenly going to be in your 700k budget do you? Dream on.

If interest rates go up to 5% plus and wages stay the same. It’s highly likely. Will that happen is the ??

No, I just figured we may get windows that close and floor that isn’t rotten. Yano, something at least semi dry. Beggars can’t be choosers though right.

Feel for you. Bought 8 years ago a place that had holes in the floor and windows that wouldn't open for less than half your budget. Took 7 years and half the purchase price to make it into a warm, dry home (build back better?), but it was totally worth it, because it was ours. So even if you are a beggar, if you're prepared to do most of the work yourself and learn new skills, you can get what you want. Just not straight away.

If we didn’t have the kids we would absolutely be buying the worst house/okay street we can find and ripping into it.

If it wasn’t for them our want for a dry home or windows that close (seems to be a key feature in homes we’ve looked at - indoor outdoor flow maybe haha) wouldn’t be as high. It would also be maxing ourselves out so won’t have surplus funds to make it liveable within a year, it would be a 3 plus year project. If interest rates went up... ****.

At this stage Christchurch may be getting some new residents. Sacrifice friends and family but at least get on the ladder in what seems like a great part of the country.

I get you. For us it was wanting a warm house as our rentals were freezing and impossible to heat. The only difference between us is some years. So unfair

Brand new houses in nice areas selling for $1M? No, definitely not.

But old houses in South or West Auckland with asking prices of $1M today when they were only worth $700k maybe 5 years ago? Yes, I can definitely see that happening. All it takes is a change in sentiment that causes these overleveraged investors to sell all at the same time for an oversupply. Maybe increasing interest rates would do the trick.

Read it again - they said a little more livable

When it happens it will be peasant Dowding.

Peasant is very apt for you Landers well done.

A proper dyed in the wool DGM!

FHBs wishing for that to happened can forget about ever being lent something from the banks for a very long time

Again good luck to all the DGMs that infiltrate this site with their negativity

Listen to yourself dude.

LordD..."among all forms of mistake, prophesy is the most gratuitous." George Eliot.

House prices down would be a great thing. That day when the speculators realise capital gains are negative, is the day the behaviours change.

But I can't see RB moves alone doing it.

Higher interest rates are more than welcome.

At the very least, there is no more chance of that completely moronic idea of negative interest rates eventuating in the near future.

The physical underwrite for high interest-rates is no longer there. This was a global - physics-based - problem, insurmountable with $-based 'tools'.

The only fit to the down-side, post-peak, is negative rates. The alternative is a Wile-E-Coyote cliff-overshoot. And you've seen what always happened to him...

So much for RBNZ "independence". Orr should have told Robertson to piss off. A very bad precedence imo

Can't have the apparatchiks overtly running the show - that would unveil the shroud legitimising democracy.

How unedifying from Robertson

To me this is all theatre. I can’t imagine RBNZ never considered house prices thus far. I felt it was implicit all along. RBNZ has always noted the vulnerability of the housing market to financial stability. This announcement only makes it explicit. Therefore, to me this changes nothing.

Think you're on the money there!

No, Orr would get very aggro at reporters for questioning him about house prices and for writing media articles about house prices "clickbait" he called it. He was very clear it's wasn't his mandate.

Now it is. Lol.

Really pulled into line! The beatings will continue until morale improves

I agree with the earlier comment, it hasn't actually become part of the target so is mostly theatre. All that will change is there will now be a paragraph saying that house prices could go up by x% as a result of monetary policy. If anything I think this puts the pressure back on Robertson to do something else.

Why is Mr Robertson the FM, if he cannot tackle the housing problem, which he had answeres when was in opposition but now when in power has got dementia of the way to tackle it.

The rot set in when Cullen changed the inflation target from 0 - 2% to 1 - 3%. For some reason, leftists think higher inflation is good for working people. Then Jacinda/Grant added full employment to the remit, not understanding that the dual mandate has exacerbated inequality in the US by giving the Fed an excuse for keeping monetary policy loose, thereby helping asset owners. Now Grant has thrown house prices into the mix - too many things to control with the single knob of interest rates. If the NZD keeps rising, he might add its value to the remit!

What is going to be left for the government to sort? Oh yes! Covid

Dti what a great idea. How do landlords increase income? That’s right increase rents.

Rents are set at a level that the market can afford. If a landlord increases rent too much, the tenant can choose to move to a cheaper rental. Your scenario will work if ALL landlords increased rent all at the same time. With so many vacant properties (due to no international students / people on work visas) that scenario is highly unlikely to happen.

That comment fails to factor-in the increasing debt held by the total system.

Who holds the parcel when the music stops?

Those with the most debt ie the overleveraged investors who came late to the party who rely on tenants to pay their mortgage. FOMO and misconception of "prices ALWAYS go up" lured them into the landlord game they have no business or risk appetite to participate in.

There's that new statistic that nearly 80% of landlords own just one property. There's gonna be a lot of pass-the-parcel going on and it's a race to the bottom to see who can sell first.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.