The country's wholesale interest rates have become "too high and too expensive", according to Kiwibank economists.

In Kiwibank's latest First View publication, chief economist Jarrod Kerr, senior economist Mary Jo Vergara and economist Sabrina Delgado say they "would expect to see a fall" in wholesale rates, following the Reserve Bank's review of the the Official Cash Rate (OCR) this week.

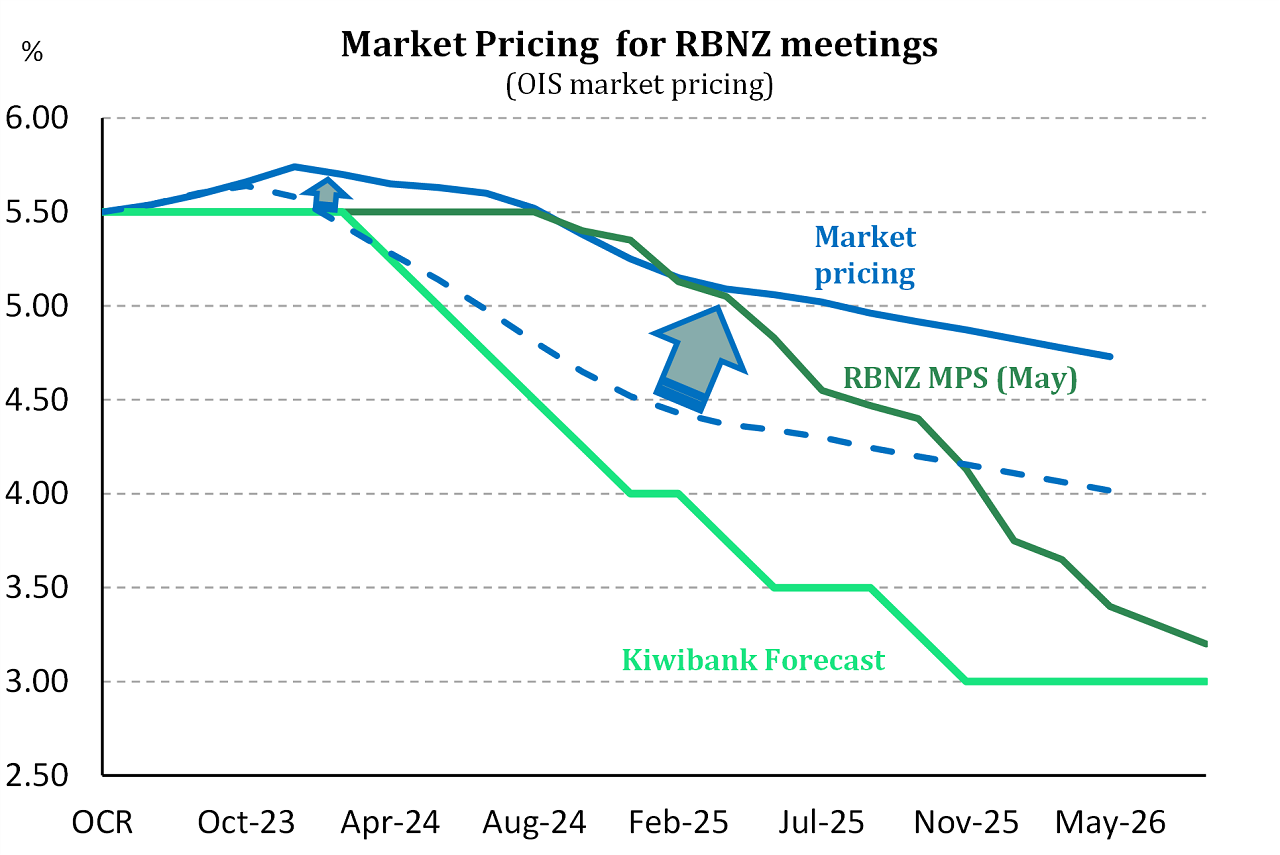

The central bank is universally expected to leave the OCR unchanged at 5.5% after it published forecasts in late May showing it wasn't forecasting any more increases and it was forecasting the OCR to remain at the 5.5% level till the second half of next year.

Other than the “unchanged” announcement on Wednesday the economists we expect the RBNZ to reiterate a steady path ahead. They think the last line from the last statement in May will stay the same (or very similar. It was: "The Committee is confident that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1% to 3% per annum, while supporting maximum sustainable employment." (RBNZ MPS, May’23).

The economists say that wholesale rates "have lifted beyond the RBNZ’s own projected OCR track".

"Expectations for the terminal rate, or peak in the OCR, haven’t changed much. But the expectations for the RBNZ pause have pushed out a lot."

They note that the wholesale rate increases have pushed expectations of rate cuts back from February next year to October or November of next year.

"We think short end rates are too high, and too expensive. We think wholesale rates should fall back to where they were."

Where the wholesale rates were previously is denoted by the dotted line in the below graph:

Ross Weston, Kiwibank's Head of Balance Sheet – Treasury said the NZ wholesale yields had continued to lift "on offshore direction".

"In NZ there are +25 [basis points] of [OCR] hikes now priced into November which at this juncture feels unlikely to be delivered, with the first -25bp cut now pushed out to August."

Weston said "a punchy rinse and repeat" of the RBNZ's May OCR statement is largely expected, but the wholesale interest rate moves increase the chances "of a more forceful on hold message given the recent weaker data and increased mortgage holder pain".

Kerr, Vergara and Delgado noted that they had updated their NZ economic forecasts last week "but not by much".

This had included a 'double dip' recession forecast. While they had also noted that mounting migration means more demand, and higher house prices.

"We ultimately think inflation will fall far enough, and fast enough, to enable rate cuts from February next year."

They pointed to the Government Crown Accounts of last week as being supportive of this view.

"The Government’s coffers are a little lighter than expected. In the eleven months to May’23, tax revenue came in $2.2 billion below forecast at $103billion [largely due to lower corporate taxes] and points to a much weaker than Treasury-forecast economy."

19 Comments

"We think short end rates are too high, and too expensive"

But only relative to the far dated rates. It is those that will rise. i.e. the curve is going to flatten and eventually sense will prevail, and it will return to a positive inclination. And if short end rate ease at all, it will be a surprise.

I so wanted to see negative rates just for laughs, to top off the shit show, before the end.

Frustratingly, we just can't seem to accumulate enough bad news all at once to put sufficient fear of God into the central planners.

In the aftermath of the financial crisis, Threadneedle Street slashed borrowing costs to 300-year lows ... in the space of just a year. Many experts believed that borrowing costs would be permanently lower. This conviction is still widespread. But as the battle to cool the economy drags on, voices of dissent are growing louder...In the US, rate-setters at the Federal Reserve have started raising their expectations of where borrowing costs will settle in the long run... shrinking labour forces as populations age are among the key factors that will raise prices and thereby interest rates...“The last three decades from about 1990 to about 2020 were extraordinarily historically unusual,”

https://www.telegraph.co.uk/business/2023/07/09/interest-rates-never-fa…

"The bond market is always right"

https://www.afr.com/markets/debt-markets/three-more-rate-rises-on-the-c…

Australian households face up to three more Reserve Bank cash rate increases, after carnage in global bond markets stoked speculation the central bank will be dragged into the US Federal Reserve’s efforts to tame inflation.

“Central banks including the RBA don’t want to hike rates, but they might be forced into it,” said Vimal Gor, chief investment officer at Sydney asset manager Trovio.

If the Fed keeps going up it will be hard for us not to follow.

We simply must follow. That is, we must be higher.

Failure to keep higher than Fed will cause international investment to wander elsewhere, but too high for local economy could cause us to default on out debt obligations and degrade our credit rating then international investment will wander elsewhere. So expect spending followed by tax.

Our country was created on a fault line, this is like the modern day origin story…

re ... If the Fed keeps going up...

That's a very big If given they - like the RBA - have currently paused. (They know there are global deflationary forces at work and are prepared to let them work through the system.)

Unlike what far too many posters here say - it is NOT the nominal interest rate that matters when trying to reduce inflation. (i.e. those looking back 30 years and saying we must return to rates higher than '30-year average' rates.) Sorry. That's wrong. (But the RBNZ doesn't mind you saying it - even if it's wrong.)

What matters in the inflation 'fight' is that rates are higher than recent rates in 'normal times' - the recent goldilocks periods. In the case of the OCR - that's around 3.5%. So at 5.5% the OCR message is very clear. Destructively so.

Good grief. The whole point of high interest rates, as these economists well know, is to stop people borrowing to buy stuff, so that prices, and therefore inflation falls. They know full well that it worked in the 1980s, and it will work now. The only problem is that the bank bosses think their life will be easier this and next year with lower rates, so they instruct the economists, whose wages they pay to spout this nonsense. The banks do not pay economists good money to spout the wrong statements.

To be fair things have changed. Many people are now carrying such massive debt we no longer need 20% interest rates on mortgages to stop people spending. The problem with just raising rates now is that its not hitting 100% of people equally and its only hitting a relatively small group really really hard. These people are going to get wrecked long before rates come down. Those people with no debt and big term deposits can do the opposite and spend like drunken sailors. The side effect of this is just even more inequality.

If that's true and not much is dependent on housing but more on savings then why not let the house prices fall further and let the correction take its course.

Because the effects aren't uniform. The ones taking the biggest hit will be primarily younger, with families and struggling against other living cost increases that other people with smaller or no mortgages may not have to face. That's the reality that hiding behind averages masks, which is what our Reserve Bank does.

You can't endlessly flog the same group of people over and over again for 'the greater good' if it just means continually worse outcome and then act surprised when young people leave the country en masse.

I also benefits the young who haven't got houses, and are saving for a deposit, those deposits earn more interest while house prices fall. Unfortunately those in the middle that bought houses at insane prices because of FOMO will suffer. The only alternative is keep the housing Ponsi scheme alive so the next generation can suffer too. Its a hard lesson to learn but as long as the government protects house prices, people will always believe in "as safe as houses" and never start investing in actual business.

To destroy the housing market is very painful for a small group of recent buyers. Yes, some of them are younger FHBs with families, etc.

But not to destroy the housing market is worse. The insanity that we've seen in recent years is incompatible with any kind of social stability - with democracy itself. And while raising rates increases 'inequality' between high-equity and low-equity homeowners, the truth is that any younger person who has purchased a property in recent years *is* wealthy, or at least has generous gifts from parents. Buying a house on a median income, without any inheritance to kick-start you, has not been possible in NZ cities for some years. FHBs are relatively wealthy people, which is easy to forget if you live in a leafy suburb.

To be fair, taking on too much debt is a personal failure. As Mr Micawber postulated, thrift will always be rewarded, and should not be conflated with inequality. Trouble with the inequality argument is that those who are more ‘equal’ tend to have worked harder and saved more.

I think you are perhaps taking the inequality comment personally. Not everyone has worked harder and saved more to obtain a beneficial position. For those that have, point taken.

@Zwifter

Stop it—too much common sense.

Bugger!

now you know how savers felt when rates were lowered to an almost non existent rate of return

hurts ha

It's I threshing to read this article originating from Kiwibank and the one on average interest rates originating from Westpac. Government owned Kiwibank THINKS things should oo lower.

Westpark FORECAST weighted average rates are going up.

With 50 percent of mortgages coming up for renewal in next year, demand for money will keep rates up for longer. The amount of fixing longer periods is only up slightly meaning people are still fixing for a year expecting rates will be significantly lower next year.

This will push the figure for people fixing over next year to well over 50 percent and create a huge demand for short term keeping rates higher for longer.

On supply side people will want to lock in higher rates on terms deposits so will want more on short term one year rates keeping them high.

Oh sure they wil. Just like the Ukraine is 'winning?!'

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.