By David Hargreaves

The Reserve Bank says it is "not sufficient" to look at inflation outcomes alone when evaluating monetary policy, and central banks cannot "nor are they expected to" have "perfect foresight".

These comments from the RBNZ are in the bank's November 2015 Bulletin in an article headed: Evaluating Monetary Policy. The article, which comes in the wake of increasing comments and concerns being expressed in the marketplace about the RBNZ's inability to hit its officially mandated 1%-3% (with explicit 2% mid-range inflation target), says: "It is not expected that the Bank will always get its forecasts right", but it is important that the Bank learns from its forecast errors. The article was written by Dean Ford, Elizabeth Kendall and Adam Richardson from the RBNZ's policy analysis team.

The article also looks at the RBNZ's decision to hike interest rates in 2014, which has been viewed widely retrospectively in the marketplace to have been a mistake - though the RBNZ has refused to term it as such.

"When evaluating monetary policy, it is not sufficient to look at inflation outcomes alone. There are two reasons for this. Firstly, unanticipated events can affect how inflation outcomes evolve over the medium term and central banks cannot, nor are they expected to, have perfect foresight. Secondly, flexible inflation targeting gives central banks discretion in regards to the speed at which they aim to return inflation to target, to avoid unnecessary instability in the economy," the article says.

A large part of the article is also devoted to the decision-making process, with a special break-out 'box' article devoted to this. The decision on whether or not to move official interest rates is the sole responsibility of RBNZ Governor Graeme Wheeler. This too has been the topic of some discussion in the wider public, with some suggesting a committee-based decision process like those of many overseas jurisdictions might be a better way to go.

Wheeler himself raised this issue after the September Official Cash Rate decision was announced and gave a detailed explanation of how the decision-making processes actually worked within the RBNZ.

The latest RBNZ bulletin goes into yet more detail on this, saying that while the RBNZ has a legislated single decision-maker structure, where the Governor is solely responsible for monetary policy and other decisions regarding statutory functions of the Bank, "in practice, however, the Bank uses committees in its formulation of monetary policy to improve the decision-making process".

"Using committees as part of the decision-making process has advantages over a pure single decisionmaker model. In particular, it allows for a wider set of information to be considered and encourages deeper debate," the article says.

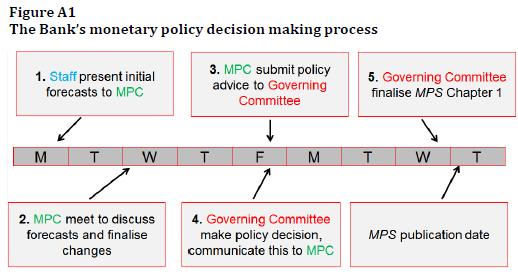

It says the Bank’s monetary policy decision-making process, which occurs in the lead-up to a Monetary Policy Statement, has five stages. The Bank’s OCR reviews use a scaled down version of this process. Three major groups of people are involved, including: "A wide array of Bank staff", the 13-strong Monetary Policy Committee (MPC), (made up of senior staff from the Bank’s policy departments, two external advisors, and the Governing Committee), and then finally the Governing Committee itself, which consists of the Governor, two Deputy Governors and the Assistant Governor. The diagram below demonstrates how these various inputs occur in the days leading up to a decision.

Going back to the main RBNZ bulletin article, it says that the Bank’s focus on medium-term inflation requires it to make many judgements about the future when conducting policy.

"Given the uncertainties, it is not expected that the Bank will always get its forecasts right, but that it will respond in a reasonable manner as new information becomes available, especially if this new information differs from earlier expectations."

Responding reasonably requires the Bank to continually assess the importance of new data and events, and determine whether they warrant a change in the stance of monetary policy. Doing so should result in better decisions and economic outcomes in the future, and enhance the credibility of the Bank’s framework, the article says.

The Bank’s accountability documents, speeches, and analytical papers should help the public to assess the responsiveness of the Bank to new information. In addition, the Bank periodically releases analysis of its forecast performance. If the Bank is responding to new information effectively, then there should be no systematic biases in its forecasts and the accuracy of its forecasts should compare well to those of other forecasters. How the forecasts have evolved should provide evidence of learning.

The article says it is important that the Bank communicates effectively.

"The Bank uses its Statements, speeches and analytical papers to communicate its judgements, interpretation of new information, changes in policy stance, and how it is likely to react to new developments. If communication is effective, the market will understand the Bank’s reaction function and how it is likely to respond to new information. Market pricing will adjust accordingly as developments unfold. This will help improve the efficacy of monetary policy."

A "key conclusion" is that it is not sufficient to look at inflation outcomes alone when making such an assessment.

"The Reserve Bank operates policy to achieve price stability over the medium term and unexpected events can cause actual inflation to temporarily deviate from the medium-term target. New Zealand’s flexible inflation targeting framework also gives the Bank discretion as to how quickly it should seek to return inflation to target, to avoid unnecessary instability in the economy."

The article says that "based on its interpretation" of the Policy Targets Agreement between the Governor and the Minister of Finance, the RBNZ conducts policy such that future inflation is typically forecast to be comfortably within the target range in the latter half of the three-year projection period.

"But how quickly this occurs depends on prevailing circumstances. When conducting monetary policy, the Bank focuses on returning inflation to the midpoint of the target range. This midpoint focus helps anchor inflation expectations near 2%, making the outlook more resilient to temporary deviations of inflation from the target band."

When evaluating monetary policy, inflation outcomes are assessed, but how the Bank has responded to new information and forecast errors is also very important, the article says.

"An ex-post [after the event] assessment should consider whether the Bank responded reasonably to new information; whether these developments were communicated effectively; and, whether the credibility of the monetary policy framework has been maintained. While it is not expected that the Bank will always get its forecasts right, it is important that the Bank learns from its forecast errors. Continuous learning about the state of the economy is important to ensure that monetary policy is set appropriately."

Another break-out 'box' illustrates "how the ex-post criteria for assessment outlined here might be applied", using material from the RBNZ's September 2015 Monetary Policy Statement.

"In March 2014, the Bank began to increase interest rates, increasing the OCR by 100 basis points from March to July that year. The outlook for the New Zealand economy was very positive; consumer price inflation was expected to begin rising and it was judged prudent to lessen the degree of monetary stimulus to keep future inflation contained. The Bank and markets expected that the OCR would need to increase by more than 200 basis points in total," the article says.

"However, several unforeseen circumstances led to inflation being weaker than expected – including significant falls in the prices of oil and our commodity exports, a stronger-than-expected exchange rate, weaker-than-expected capacity pressures, and weaker-than-expected non-tradables inflation. The Bank used its Statements, speeches and analytical papers to discuss these developments.

"The first criterion for ex-post assessment is whether the Bank responded reasonably to this new information. While the Bank could not have foreseen these developments, it progressively eased its tightening bias as evidence of weaker inflationary pressures developed . This easing started with the Bank scaling back the extent of its projected monetary tightening from the June 2014 Monetary Policy Statement.

"Subsequently, the Bank cut the OCR by 25 basis points for its June, July and September 2015 OCR decisions.

"The second criterion for ex-post assessment is whether the Bank’s communication of these developments was effective. The change in monetary policy outlook (along with other factors) contributed to a fall in retail interest rates from July 2014, leading to easier monetary conditions. Wholesale interest rates also declined in anticipation of the Bank’s response to new information.

"The third criterion for assessment is whether the credibility of the monetary policy framework has been maintained. Medium-term inflation expectations have fallen over the past six months, but are currently near the 2% target midpoint. External forecasters also expect inflation to return to target over the medium term."

37 Comments

This is tantamount to burying, as opposed to drawing back the veil of central bank infallibility. Time to put the shovel aside.

Makes you think, have they finished digging the hole?

I have been banging on for over a year about the total lack of evidence of inflation .

From a CONSUMER ( CPI) point of view everything was coming down , food , fuel , Auckland rates , fresh meat , motor cars , white goods , clothes on the internet , mortgage servicing costs (mine is paid up so I don't have one ) but even our short term insurance costs declined until I had the house revalued .

From a PRODUCER point of view ( PPI ) wages in the construction sector were going up but everywhere else it seemed stable , although the costs of imports due to the high kiwi$ seemed to fall.

The benefits of cheaper imports still have mostly not been passed onto consumers , we pay too much for fuel and clothing by int'l standards

The reasons are obvious and plentiful - the wrong type of inflation is being bench marked with the connivance of both central banks and governments to affect a transfer of wealth from labour to capital.

Wall Street is counting its winnings from seven years of easy money.

In a report sent to clients on Sunday, Bank of America Corp. strategists totted up the results of 606 global interest-rate cuts since the collapse of Lehman Brothers Holdings Inc. and the $12.4 trillion of central bank asset purchases following the rescue of Bear Stearns Cos.

The results represent a clear victory for Wall Street over Main Street, according to the team of Michael Hartnett, BofA’s chief investment strategist.

For every job created in the U.S. this decade, companies spent $296,000 buying back their stocks, according to the New York-based bank.

An investment of $100 in a portfolio of stocks and bonds since the Federal Reserve began quantitative easing would now be worth $205. Over the same time, a wage of $100 has risen to just $114.

For every $100 U.S. venture capital and private equity funds raised at the start of 2010, they are now raising $275, but for every $100 of U.S. mortgage credit extended five years ago, just $61 was extended and accepted this June, BofA said. Read more

it seems you are intent on destroying NZers businesses and employment with no justification past neo-con dogma, financial blinkers and/or greed.

ie If you set the OCR by "inflation" in a few overly expensive suburbs in Auckland, the rest of NZ would not have an economy or SME's to speak of elsewhere.

Sure Wall street is winning from 7 easy years, that is because they have bought the politicans lock stock and barrel, whatever the OCR was in this situation makes no odds if teh bankers are not jailed or at least stopped.

If you set the OCR by "inflation" in a few overly expensive suburbs in Auckland, the rest of NZ would not have an economy or SME's to speak of elsewhere.

Justify that nonsense to those on $50,000 or less confronted with the uphill task of saving to buy into this reality - work has little justification if it's advertised rewards are beyond reach.

Just in case clicking the link is a reach too far here is the headline.

The average value of a home in Auckland hit a new all time high of $918,153 in October which was up 24.4% compared to the same month last year.

Is this a sprint to the finish?.

http://www.aol.com/article/2015/11/01/sprint-says-aims-to-slash-costs-u…

Sorry guys, the Taylor rule does a good job of indicating where interest rates should be.

We can simply replace the RBNZ function of setting the OCR with the Taylor rule & a robot. RBNZ Governor would only need to step in "extreme circumstances".

"In all three countries, the actual interest rate rarely diverges greatly from the Taylor rule rate."

http://www.rbnz.govt.nz/monetary_policy/about_monetary_policy/3075589.p…

I suspct not quite that simple...but better probably than many other non-methods.

--edit-- also the rule states the neutral rate today and not for say 2 years out or if you want to cool or heat the economy, that is a human judgement call.

I am disappointed in the Bank. Its clear that the inflation forecast errors are heavily biased. Basic statistics indicates this. The Bank is purposefully acting against its legal mandate and targeting lower than the required inflation target zone. To argue otherwise is to treat us all as idiots. it is time for the Bank to realise that it is a public servant and not the arbitrator of what is an appropriate level of annual inflation.

To argue that non- perfect foresight justifies undershooting for years on end is ludicrous. Can they not tell the difference between above and below 1%.

Good points. Even in this paper they do not explain at all why they jumped very quickly on perceived inflation possibly going up, but then took over a year to drop rates after the supposed unforeseen events had occurred. They also remain silent on the very clear exchange rate market reaction to both their actual interest rate increases or decreases, and to the change in direction in them that they indicate. They state that the exchange rate remained higher than expected, as though it being so was entirely independent of their being I think the only central bank in the developed world that increased rates in 2014.

As it happens I would personally advocate they use different tools than just interest rates, as super low rates do cause other problems (like asset bubbles, debt bingeing and saving disincentives), but in this I believe we are going to have to wait for the major world central banks to make some bold moves.

The OCR does seem to be a blunt tool that is not well targetted. To do more however I think would take Govn action ie new laws rather than looking at "pretty" flags. Just pathetic IMHO.

Agreed, the targets and tools would have to change, and that is a government/ Minister of Finance role. Bill English has proven over conservative in my view (in a lets not rock the boat conservative view, rather than a right wing bias). Labour have a range of other issues to sort but Robertson (as Parker was before him) is correct to want a broader range of objectives, and some integration with fiscal policy, even if still very much with an independent central bank.

I dont agree on the broader range of objectives ie some will be mutually exclusive. Frankly labour is a bunch of clueless twerps. They one day they will be the Govn so its on them to act just like its on BE to act now, and it was for HC and co to act in the past.

failure..

Why would you set a tightening bias anytime since 2009?

Obviously responding to general criticism in the media, including BHs column.

Still, no explanation as to why NZ is several steps higher in interest rate settings compared to most developed economies.

When will the RB target of 2% inflation be met? Ever?

Go back a couple of years, didnt they expect the OCR to be 4.75% in 2016 or 2017?

They are still maintaining that the new neutral rate is 4%!

Ok, let's run the OCR at 4% for the next 3 years and see things grind to a halt.

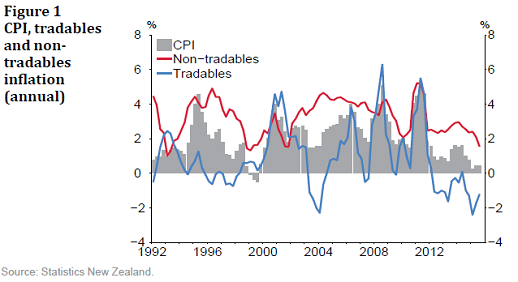

look at the tradables graph looking like -2%, 3 more years and what -6%? -8%? seems they dont give a damn about SMEs.

--edit-- Forwarding that trend looks like about -4% by 2018, so -1%? per year do we really want to keep doing this to our employers and their workers?

The economy will certainly grind to a halt @ ZIRP.

In his first public speech in England since his term at the BoE ended in June 2013, Mr King said he was concerned about a persistent weakness in global economic demand, six years on from the depths of the financial crisis.

“We should worry about that,” Mr King told an audience at the London School of Economics, where he was once a professor.

“We have had the biggest monetary stimulus that the world must have ever seen, and we still have not solved the problem of weak demand. The idea that monetary stimulus after six years … is the answer doesn’t seem (right) to me,” he added. Read more

The thing is,

a) what has been avoided by the stimulus, ie what we see is a NET effect.

b) the alternative seems to be the inflationistas wanting to rise rates. Yet we have -2% in that sector with a maybe 1% per annum decline even at an ocr of 2.75%. Just how the SME's keep going in this situation defies belief.

In fact its almost like some ppl want to crash the economy.

Mr King, well maybe read the entire piece for a better context,

http://www.telegraph.co.uk/finance/economics/11356492/More-QE-will-not-…

we don't have the wage inflation needed, and wont have anytime soon with a rising unemployment and high immigration.

that and with no interest being paid to the old folks living off deposits not being spent in the shops,

more and more income being spent on housing,I can not see where inflation is to come from.

the only hope is a very low exchange rate

Inflation via a lower exchange rate increasing the prices of goods can't work when people can't buy those goods and that is what happens now.....basic costs like food and housing are too expensive relative to incomes so when that dollar goes down and imports go up people don't spend which increases the financial instability issues for the RBNZ.........The GFC has been caused by Governments and bureaucracies overspending the tax payers dollars for years and years........the crisis happened because the ability to take money off the private individual, SME etc to fund the bloated system had reached a capacity point where they could not afford to pay anymore and that was going to sink the economies of every country concerned......NZ despite a golden run during a world financial crisis has not trimmed back and made the public system efficient and neither has any other country.............NZ over the last 20 years has become so over-regulated that one cannot move an inch without extensive costs involved in meeting the regulatory requirements and answering to some bureaucracy in some capacity.........the more regulation involved the more money taken off the consumption table.

There will only be inflation in NZ when there is major deregulation of the SME businesses!!! Everyone knows or should know about the downstream effect of a dollar earned and spent by the e.g. farmer has a multiplier effect on the economy but the bureaucracy and many of the commoners ignorantly believe that the same effect is derived from every dollar they spend.....it is complete and utter ignorance to forget about the earning side of the equation!!

Inflation is really nothing more than an increase in Government expansion/spending which forces prices higher.....financial stability is the general public's ability to keep paying and the two converged causing the GFC......we are in a new era.

they need their bumps felt.

Man look at that tradables graph, going down or what.

and such a huge gap to non tradables

Excellent visualisation tool by stats here;

Thanks for that, big increases in the last two years

alcohol and Tabaco which will be government taxes RB can not do much about that

education same as above government issue

housing, you can see why they are reluctant to drop rates.

everything else small or decrease.

interesting three issues the government could tackle if they wanted to so as to give room to RB can drop rates

but even that is heading down. So both have a trend/trajectory down and the RB and govn sits and does nothing.

It must be frustrating being an employee for the RBNZ, and essentially a thankless job. I wonder how many in the department disagree with the RBNZ's application of their policy over the last few years.

To release a defence for what they have done or not done over the last few years is encouraging to me in one respect: does this maybe mean the RBNZ are actually starting to listen to the public of which they are paid to serve?

The biggest thing I gleaned out of their defence is this: once 'they' (Wheeler?) has made a decision, it takes a massive amount of effort to change 'their' (his) mind to change course if that decision was wrong (and it looks like his mind still hasn't been changed...).

In defence of the RBNZ 'though, we are in interesting times, and so, they are on a hiding to nothing. Auckland house prices continue to go through the roof, all the regions continue to stagnate or die, and (it appears the RBNZ are admitting) there is nothing the RBNZ can do about it.

"It's not our fault, we are only implementing policy"

The RB still can't acknowledge that interest rates are no longer the driver of Auckland house prices.

Immigration, international students (& effects), nonresident buyers, investors, and distrust of all alternative investment types, 'main city' effects, lack of economic development in regions, etc are driving prices, not interest rates.

agree, and they don't have any power or tools to slow that. there best bet to protect locals would bring in 30% LVR for all property and max LI 6 times drop the OCR to 1.5% and let Auckland pop. then once investors, overseas buyers and banks get hurt they wont come back in a hurry.

.

The RB still can't acknowledge that interest rates are no longer the driver of Auckland house prices.

Nobody believes you and in fact one could easily mistake you for a real estate bubble apologist just like Bill English.

New Zealand central bank Governor Graeme Wheeler needs to get inflation back to target and some observers think he has “plenty of room” to cut interest rates, Finance Minister Bill English said. Read more

Ben Bernanke was not kidding either when he declared the success of LSAPs.

Importantly, the effects of LSAPs do not appear to be confined to longer-term Treasury yields. Notably, LSAPs have been found to be associated with significant declines in the yields on both corporate bonds and MBS.14 The first purchase program, in particular, has been linked to substantial reductions in MBS yields and retail mortgage rates. LSAPs also appear to have boosted stock prices, presumably both by lowering discount rates and by improving the economic outlook; it is probably not a coincidence that the sustained recovery in U.S. equity prices began in March 2009, shortly after the FOMC's decision to greatly expand securities purchases. This effect is potentially important because stock values affect both consumption and investment decisions. Read more

For whom, one must ask? Not the working class.

The RBNZ are either liars or they genuinely got it hopelessly wrong .

I hope its the latter

Read my posts about inflation ( or the absence of it ) over the past 2 years on this site

If even a layperson such as myself who keeps records of all my expenditure, could see there was NO INFLATION and in our household case everyday costs such as food , fuel , council rates, telephony and power costs actually falling , then , how could they say there was an inflation problem ?

Furthermore there was every indication that the prices of all commodities were falling due to either oversupply ( oil) or the Chinese buying less .( milk powder , ore , aluminium, coal , steel , copper ,) and most countries we trade with were doing everything possible to weaken their currencies to make their exports cheaper and stimulate their moribund or slowing economies

There was nothing to suggest any of this would change , and if I recall correctly I seem to remember getting into correspondence with David Chaston who reasoned that there were inflationary expectations of the horizon ( some commentators were seeing wage inflation in NZ and building costs escalating )

The Preserve Bank of New Zealand doesn't know when to put salt on the fire and when to stir the embers and add a little more fuel........their role is not for the commoner on the ground but ensuring the "System" being the bureaucratic empire can keep up appearances!!! Socialism is an unusual beast!! You have to make it look like it has a benefit, smells like it has a benefit and even offer a little benefit (sacrifice a small amount of the takings) one must complain of long hours, hard work and stress as these appeals are the same as the commoner faces daily and this garners empathy.........

I love how the ranks have swelled within the Preserve Bank and how the report churners are now wanting to flick a new preservation switch....The Governors head would no longer be the sole head on the chopping block and the proposal for the OCR to be a team effort would see many hands getting a payout when the PTA is breached!!!!

I think you should replace socialism with Capitalism notaneconomist. After all Otto von Bismark created State socialism to forestall the complete overthrow of neofeudal capitalist class relations in the social upheavals which sprang from the Continent wide popular revolts of 1848. itself precipitated by the social dislocations caused by the introduction of capitalism. Socialism is just the obverse side of the same coin. Just like in the physical realm, every action in the social realm creates an equal and opposite reaction.

The RBNZ's mandate IS to keep inflation at 1 - 3%, that's a fact, the RBNZ gets distracted by too may other economic phenomena. Concentrate in achieving your prime mandate !

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.