By Roger J Kerr

Over the last two years at PwC Treasury Advisory we have been warning corporate borrowers that the lower borrowing margins/credit spreads enjoyed through 2014 period would not last and that there was a real risk of bank and corporate credit margins increasing off the lower base.

As well documented through numerous articles in our quarterly newsletter “Treasury Broadsheet” through 2014 and 2015, the time was right for borrowers to proactively manage their funding risk and lock into five year facilities at fixed pricing (margins + commitment fees).

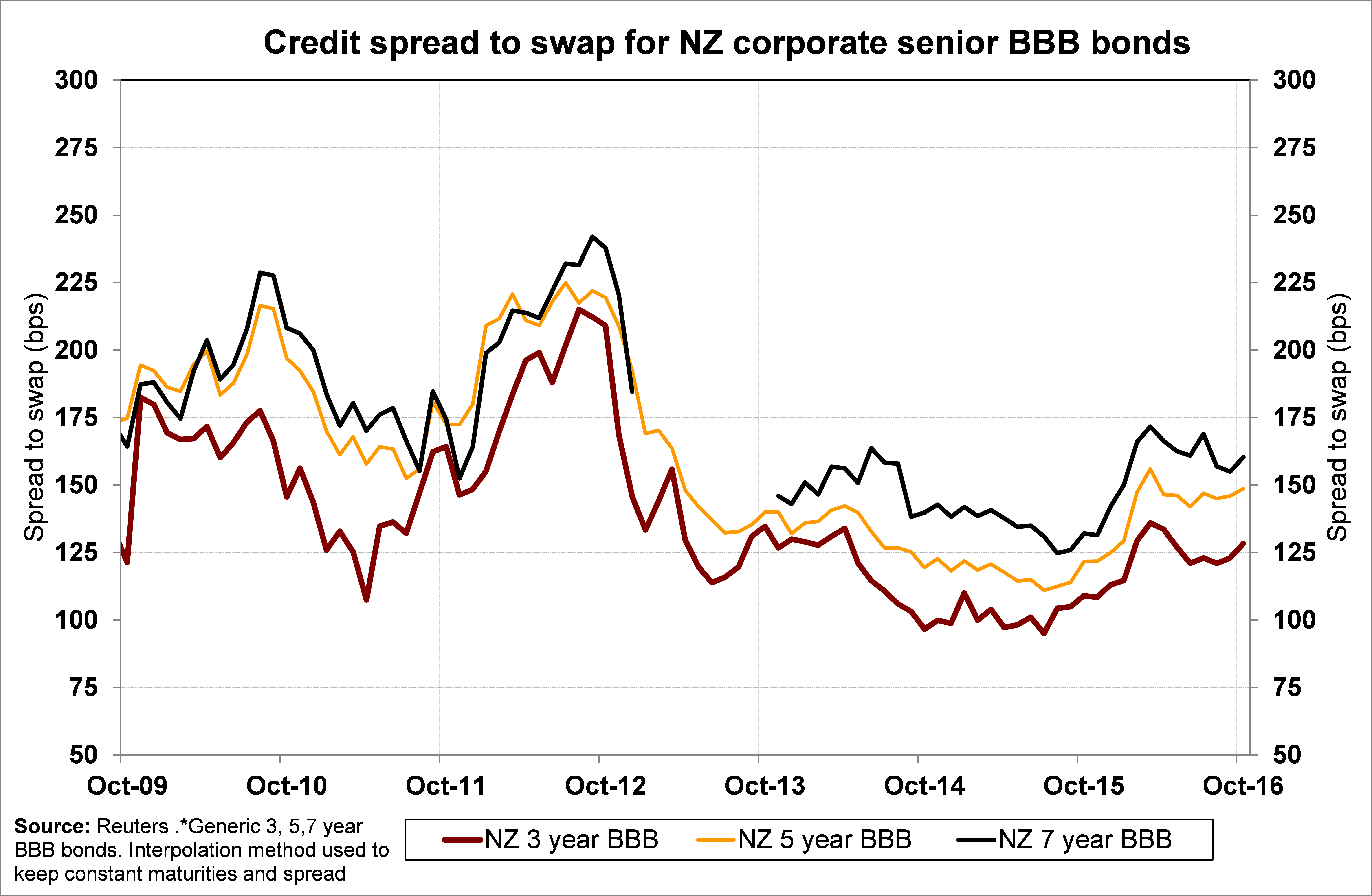

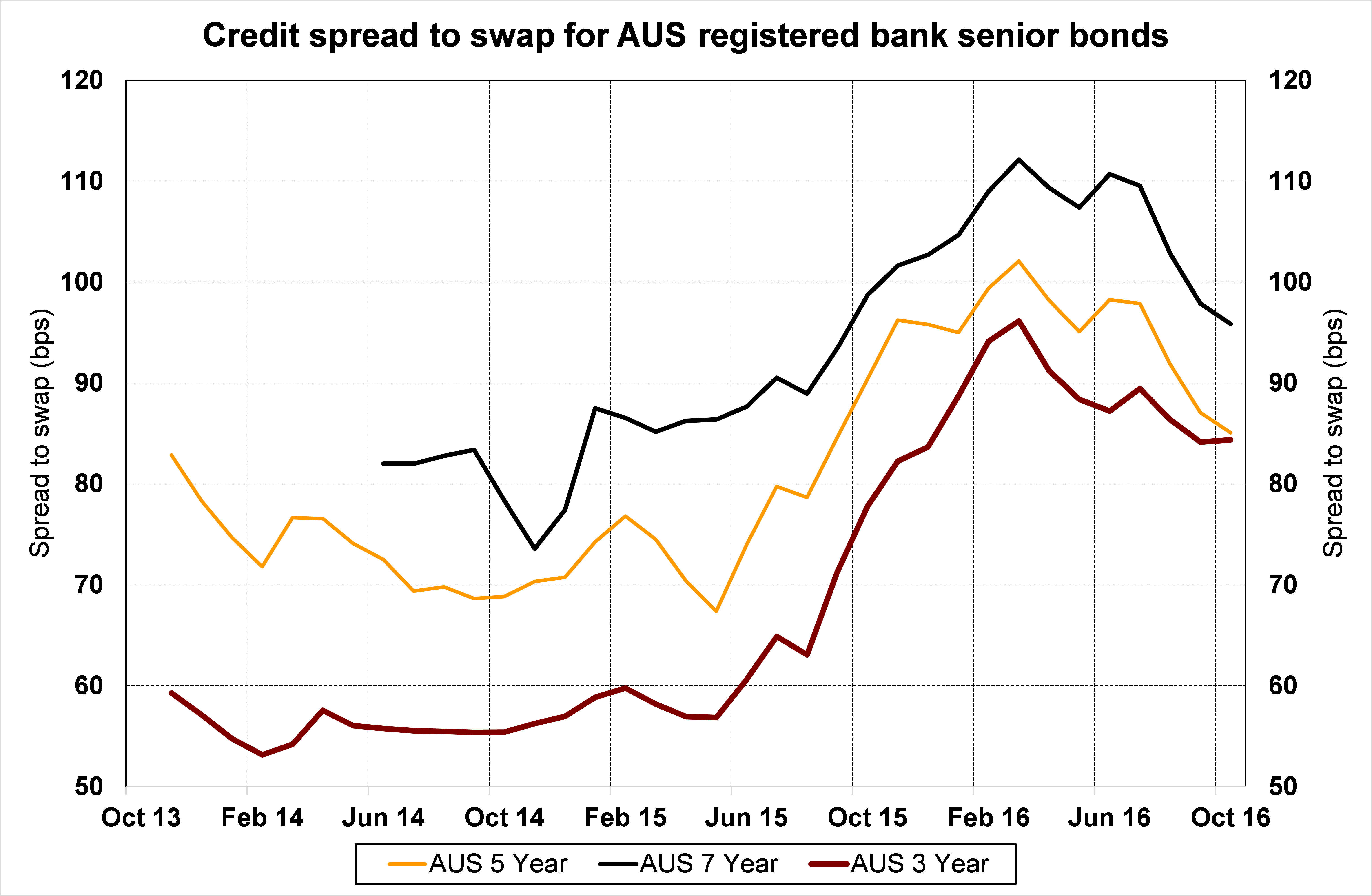

Those that heeded the advice should be well satisfied as both corporate and bank credit spreads have increased significantly over the last two years. The 0.15% pullback lower in Aussie bank credit spreads over recent months appears to have run its course (refer charts).

Looking ahead, the market forces and developments that have caused credit spreads to increase to date look set to continue into the future. For the first time in many years the banks in New Zealand are experiencing their own funding pressures from several sources and that can only lead to higher funding costs for the banks and their borrowing customers.

- Overall credit growth in the economy (bank lending) has outpaced bank deposit growth. Mum and Dad retail investors have pulled funds out of bank deposits yielding below 3% in favour of higher yielding dividend stocks and property syndicates. Net result is banks being forced to pay higher retail deposit rates to attract and retain money to fund their books. Corporate loans are priced at a margin above wholesale BKBM and OCR benchmark rates which are static or falling. However, the banks’ actual cost of funds are rising and they will pass through that additional cost into higher borrowing margins they charge their loan customers.

- Changes to definitions under the Core Funding ratio regulations imposed on the banks by the RBNZ now means that “lazy” customer monies sitting in credit in bank cheque and current accounts no longer counts as retail deposit funding for the banks. In fact, retail deposit funds less than 90 days in term will also not count as qualifying retail funding. Add in Basel III bank capital requirements decreasing bank leverage and the picture becomes even uglier. The banks require a return on capital on every new loan they make and their cost of capital has increased. The return they require is higher for all corporate, commercial and property loans they make than straight residential home mortgages.

- The wholesale debt markets the banks tap for 25% of the funding have also seen increased credit spreads for AA- rated banks. The Australasian banks are also dealing with the risk that the Australian Government’s AAA credit rating is downgraded at some stage next year, which automatically would drop the banks into the A+ category. If this happened local institutional investors like the ACC would need to reduce their holdings of bank bond securities, unless investment limits are correspondingly adjusted. Investors being forced sellers of bank bonds would send credit spreads even higher.

There is always a debate whether banks price new corporate loans from their weighted-average carrying cost of funds or at the higher marginal cost of funds of where they can raise new money at. It is always a combination of both and also dependent on what ancillary (FX, swaps, trade finance, transactional banking) business and income the borrower can offer the bank.

Whichever way it is diced, any corporate borrower who has not refinanced early in recent years and faces major debt refinancing amounts over the next 12 months will be looking at significantly higher pricing (margins and fees).

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

6 Comments

Wow, Roger has been thumping the table about this for weeks now ............. DONT SAY YOU WERE NOT WARNED !

A half of One percent increase in borrowing costs will be a serious problem for may

... at some future moment the credit markets will do the work for us that the government refuses to ( getting houses affordable for citizens ) , and that which the NZ Reverse Bank has gotten utterly wrong ... they will force up interest rates ...

We have gorged ourselves on debt , and we are going to blow up just as bad as Mr Creosote did in the restaurant scene in Monty Python's movie " the Meaning of Life " ....

... someone please explain to Graeme Wheeler , before it's too late , that we do have inflation .... rampantly horrendous inflation .... in the property market and in listed stocks on the NZX ...

And to continue forcing down the OCR is sheer bloody insanity .... the fact that the price of milk and bread , and cabbages for consumers hasn't gone up 0 - 2 % is no reason to cause devastation in the economy with a property market bubble and subsequent collapse ....

... tick tick tick .... under the tables gang .... Mr Creosote is about to explode ...

This Creosote economy has a growth rate above 3.5%, strong jobs growth unfilled by massive immigration, and capacity pressures, all fueled by credit growing at 9%, and the RBNZ want's to lower the OCR.

Whiskey Tango Foxtrot!

Time to bring in a vancouver tax and limit the damage being done with excess debt

http://m.huffpost.com/ca/entry/12440200

The average price of a house sold in Vancouver saw its largest-ever drop in August, in the wake of B.C.’s new foreign-buyer tax — but before tougher new federal mortgage rules take effect.

It’s yet another sign that the tide has turned in a market that Swiss bank UBS recently argued is experiencing the world’s biggest housing bubble.

Greater Vancouver’s average sales price plunged 19 per cent from July to August, and was down 7.5 per cent from a year earlier,

In the year 2020 the government will acknowledge that as a result of the property taxes imposed by Hong Kong and Singapore in 2014, together with the ongoing taxes and restrictions in Australia, it appears there has been an exodus from Vancouver heading into New Zealand

The NZ government will announce an enquiry to commence 2021 with a reporting date of 2022

Let's see what happens with the Crown Resort arrests. Looks like a clamp down on Money Laundering by the Chinese Govt.

I think the NZ Govt will end up having to adopt a foreign owners tax. I fear we might have a major inflow of funds from China that previously were going to Vancouver property market.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.