By Roger J Kerr

The tone, emphasis, messaging and signalling in the Reserve Bank of New Zealand’s next Monetary Policy Statement on May 11th has become something of a challenge for them as the actual inflation starting point is significantly higher than their forecasts and the TWI exchange rate level of 74.60 today is well below their assumptions for 2017.

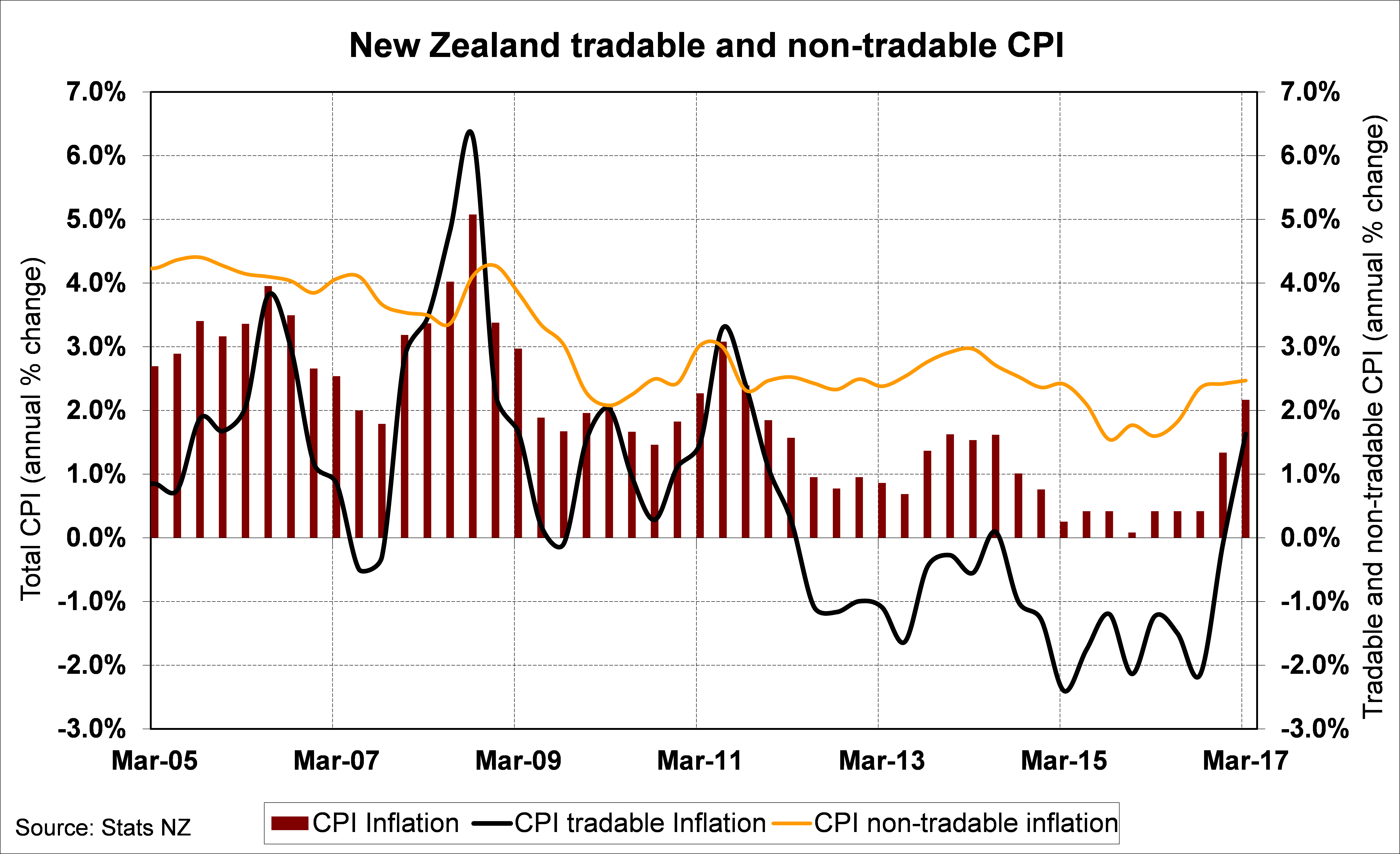

Annual tradable inflation (imported goods) roared upwards to +1.8% in the March quarter, the first time tradable inflation has made a positive contribution to the overall CPI inflation rate since 2012.

The dropping out of large petrol price decreases in late 2015 from annual tradable inflation figures has had a dramatic impact (refer chart below).

Therefore, annual inflation in New Zealand is suddenly above the 2.00% mid-point and target a lot sooner than the RBNZ and most economic forecasters anticipated.

That is what has already happened, the more interesting part is what is likely to happen going forward.

My outlook for inflation for the remainder of this year is that both tradable and non-tradable inflation will move higher still.

The lower exchange rate will cement-in tradable inflation above +2.00% and oil prices are unlikely to collapse again.

Adverse climatic conditions will keep vegetable prices up and higher export prices for dairy, lamb and beef will continue to push up these domestic food prices on local consumers.

Add in the ongoing squeeze on resources in the construction game and the conclusion has to be the RBNZ forecasting annual inflation being nearer to 2.5% to 3.0%%, rather than stabilising at 2.00%.

However this does not mean that Governor Wheeler will be altering his “no OCR increase for two years” message in his 11th May statement.

He will contend that global geo-political uncertainties and potentially very damaging (for New Zealand) moves by the US to impose import tariffs for timber, dairy and aluminium are justification for not signalling any change to his current monetary policy stance.

Later in the year (perhaps under the new interim Governor Grant Spencer) the RBNZ may well be forced by the economic data to change their tune and bring forward the timing of the first OCR increase.

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

10 Comments

They may have learnt the lesson to let inflation run for a bit and not increase too rapidly like they did two years ago. Then again they adjusted the rate on out of touch projections. They'll be lucky to last the two years as they'll get an itchy trigger finger.

How is it that the dropping out of late 2015 petrol price drops has 'surprised' forecasters who did not 'anticipate' it? Surely they knew this was coming since 2015?

Keeping the OCR unchanged for the next 2 years should do the trick nicely, and add another final 25% to Auckland house prices, giving us a classic blow off top.

We need to aim for 200-225% household debt to income and we're set. The timing will be perfect for increasing interest rates and the debt servicing percentage will be leveraged up. I'm hoping it's enough to snap kiwis back to reality and start using houses as homes instead of Icelandic style investment vehicles.

Why stop there? You may as well ramp it up to 400% and get the ("potential") crash over and done with.

If we wait that long there will be no middle class and we will switch to 20% high earners and 80% low income like in the US. Have the disaster before it significantly changes the structure of our economy, although that may be unavoidable as robots are set to take 50% of jobs in the next decade.

Good point. Maybe increase debt as much as possible as quickly as possible to bring about the crash sooner? Hopefully the NZ public will come back to reality after it has happened.

Why stop there? You may as well ramp it up to 400% and get the ("potential") crash over and done with.

According to official statistics, Japan's h/hold debt to income never exceeded 60%, even during their humongous bubble. Why does NZ have to punch above its weight at the h'hold unit? Because our private sector is incapable or too circumspect?

I guess it's because our house price inflation and wage inflation aren't increasing at the same pace, NZ wages are low across the board while the cost of living is high, and the NZ public drinks the "housing is the only thing to invest in" Koolaid.

Wow look at that photo, Inflation is on 100 (out of 100)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.