By Roger J Kerr

Two variables stand out over others as the major determinants of market interest rate movements in 2018:-

NZ Inflation Outcomes:

Local interest rate market participants (borrowers, investors, the RBNZ and the intermediaries i.e. banks) all remain very wary about predicting the annual inflation rate climbing above 2.00%.

Inflation has been so low for so long and there have been too many wrong forecasts in the past of increasing inflation, that most just do not believe that inflation will ever increase again.

To be convinced that inflation can significantly increase in 2018 they will have to be convinced that “this time is different”.

Well, what is different today from it any time over the last three of four years is the following:-

- Fuel prices are up through the increase in crude oil prices and the lower NZD/USD exchange rate.

- Food prices have increased semi-permanently due to adverse weather conditions.

- Provided demand in the economy remains robust, business firms will be passing through wage increases into their selling prices. The majority of businesses across industries such as construction, tourism and manufacturing have realised they will have to increase wages to attract and retain skilled labour.

- Construction costs will continue to increase as resources are stretched to breaking point across the building industry.

- Technology advancement over recent years have driven telecommunications price lower and lower. At some time soon, these plunging prices must get to a point where they flatten off. Are we near to that point?

US Treasury Bond yield movements:

As discussed last week, the time is fast approaching where the downtrend line in long-term interest rates since 2007 is no longer sustainable.

My view is that the Federal Reserve will stick to their planned three interest rate increases in 2018 and the interest rate markets will be forced by the weight of US economic data to adjust market pricing to higher yields than what they are currently pricing.

Rising short-term rates will drive increases in US long-term interest rates and New Zealand bond and swap yield will follow.

All the best for the festive season!

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

15 Comments

Four dangerous words, “this time is different”, epitomised by "there have been too many wrong forecasts in the past of increasing inflation".

"the downtrend line in long-term interest rates since 2007 is no longer sustainable." that was true in 2010, and 2012, and 2014, and 2016 and, yes, today. But guess what......?!

My view is that the Federal Reserve will stick to their planned three interest rate increases in 2018 and the interest rate markets will be forced by the weight of US economic data to adjust market pricing to higher yields than what they are currently pricing.

Hmmmmm....

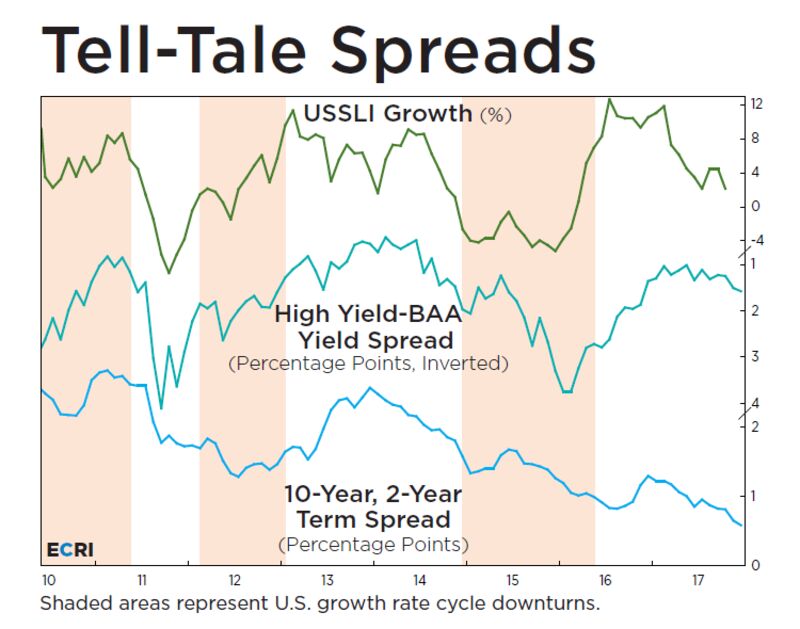

Nevertheless, the chart shows that the cyclical ups and downs of both the quality spread and the term spread have followed those of the Short Leading Index's growth rate. In other words, our leading indexes, as well as two very different bond market spreads, are telegraphing an economic slowdown that nobody sees coming. It certainly threatens to blindside the Fed, which -- fixated on the Phillips curve -- keeps projecting multiple rate hikes over the next year.

{kind=link}

There’s a choice. Perhaps it is different this time, with the Fed, the stock market and Wall Street analysts all outsmarting the bond market and ECRI’s leading indexes. Or you can heed these slowdown signals, and begin thinking through the implications. Read more

I am not trying to be doom and gloom at this festive happy time. However!

Whilst the future of interest rates can not be predicted with certainty, the likelihood for winds of change and uncertainty should be worrying for many.

The implications for Joe Bloggs is that shifts in inflation and interest rates will flow onto mortgage interest rates for New Zealand home owners.

On a $600,000 mortgage, a 1% rise in interest rates will cost $115 more a week, and - even by historic standards - a modest 2% interest rate will be $230 per week or $460 a fortnight.

Especially for FHB, can the family budget withstand an extra $460 after tax a fortnight?

If banks tighten on interest only (no principal repayment) mortgages as has been signalled, the situation becomes more critical for those in this situation.

I worry.

Roger's comment, "All the best for the festive season!" may be more significant than intended.

....and no need to increase the rates to see the danger. Try moving from $600,000 interest only at say 5% = $576 per week to 20 yr mortgage at same rate = $913 per week.

...and when did the Interest-Only fad really kick into gear again? 2012, along with the next uptick in prices and volumes. Right on 5 years ago; the *maximum extent of the grace principal period. So from now on.....

https://www.interest.co.nz/charts/real-estate/house-price-index-reinz-r…

(* Banks are quite happy to talk about 'extending the interest-only period', apparently! That, smacks of desperation....on both sides of the contract.)

I agree with these replies.

It would take either a brave or foolish person not to think that a risk of a "perfect storm" doesn't exist for those - especially FHB - who have purchased a home in the past couple of years with large interest only mortgages. Potential of increase in interest rates, end of interest only period, and even a mildly falling property market will create an untenable position.

Most of the drivers over the past seven years (foreign investment, cheap money, high likelihood of capital gain, high immigration, lack of LVR until recently etc.,) which have created rapid house price inflation no longer exist.

For those who disagree, I hope for the sake of young FHB that you are right.

I understand what you're saying, but do you think the banks really have signed on first home buyers to Interest Only mortgages that they couldn't afford to service on a P & I? An ending to interest only period for most borrowers would put them in a situation where they don't want to be, rather than a situation they cannot afford.

I do agree with your comment about the drivers over the past seven years, one thing i have noticed is that those on this site who claim that house prices will continue to rise across the board haven't really given their argument any substance, they don't talk to the "drivers" of house price inflation because the rooms empty.

I think you could be right if all those things eventuate, that would be stressful for FHB. Those of us who have had properties for 10-20 years will not worry.

Interest only loans would only have been given for a short time only with some sort of take out (changed circumstance) at the end of that period.With the loan then being changed over to P & I repayments. If not this is careless lending practices. Wonder how much of this type of lending is around?

Movements in inflation and interest rates are not exclusive , a spike in inflation will lead to an increase in interest rates , like it or not they work in unison ( or in tandem ) under our current monetary policy regime

I'm not sure I can agree with you there Boatman. We have just gone through a period of high house inflation being fueled by low interest rates.

Yes , but house price increases in our case are NOT normal inflation as in CPI increases

There are two critical aspects to interest rate increases which Central Banker & Politicians should be aware of, widespread defaults due to rate increases and unemployment increases may cause a Banking collapse and the problem of devalued assets and little liquidity to mark to market in making actual sales.The second is the real threat of civil disorder against Politicians Councilors and large tax evading corporates including Banks all of whom should review the French revolution to work out how their class fared last time.

Rumpole , a little over the top I think. Widespread defaults??Yes some will find it hard to pay higher interest rates, but most will stick in there.

PKchew, its possible that you may be struggling to visualize NZ in a situation like what happened in Ireland, Spain or maybe even Greece. One could argue well, I would have to see it to believe it first but by then it's too late.

This will all reach a conclusion shortly one way or another. Each financial event has a hindsight explanation. What happens next will be blamed on the QE post 2008 you can safely bet on that.

I hope a Australasian style banking crisis doesn't happen although with each passing day, it seems a little more likely it will. We are too far into the can kicking to safely assume this will all end well.

Long term interest rates are NOT rising.......

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.