By Roger J Kerr

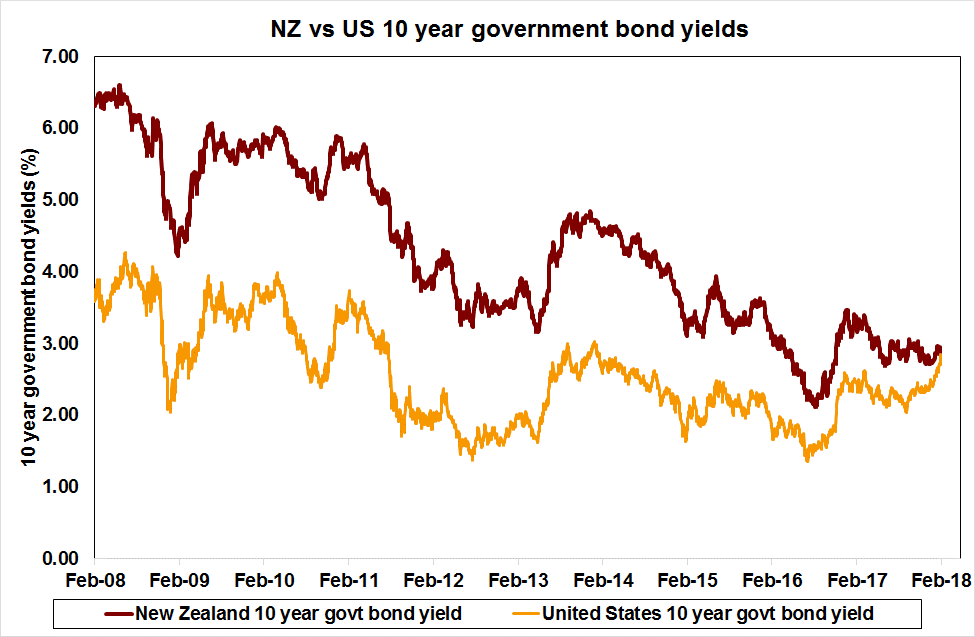

Our long-term interest rates (10-year NZ Government Bonds) have always moved in lockstep with US 10-year Treasury bond yields (refer first chart below).

The reason for this very high historical correlation is that foreign investors have held in excess of 60% of NZ Government bonds on issue and they tend to buy and sell NZ bonds in tandem with their US bond buying and selling.

Hence, our interest rates track the US rates very closely.

Offshore fund managers have traditionally invested in NZ bonds as a straight yield enhancement on US Treasury Bonds.

Overseas investors have dominated our bond holdings due to the historically low level of internal savings in New Zealand i.e. we have to offer a yield premium to attract investors into New Zealand to fund our external Balance of Payments deficit and internal budget deficit, as we do not have sufficient savings ourselves to fund these shortfalls.

In the past, the risk premium applicable to NZ bonds over US bonds (also called the bond spread or margin) has ranged between 1.00% and 2.00%. Although it did blow out to a 2.5% gap in 2009 when foreign investors all departed the shaky isles at the height of the GFC and the Kiwi dollar plunged to 0.5000.

Today the bond premium or spread is only 0.15% (NZ 2.98% against US 2.84%) as NZ bond yields have not increased over recent weeks with the sharp increase in US 10-year Treasury bond yields.

There are two factors behind the compression of the NZ/US bond spread to only 0.15%, well below historical levels:-

- Up until recently, the world was awash with cash seeking any kind of yield return enhancement. New Zealand bonds offered that return and that investor demand has kept our long-term rates very low and driven the spread inwards. However, the previous loose/loose monetary conditions have well and truly ended in the US and are now ending in Europe.

- It may be argued by some that the growth of our KiwiSaver funds and the NZ Super Fund has meant that we are less dependent upon foreign savings as we have more of our own to invest. Therefore, we do not need to offer such a big risk premium to come into NZ bonds. I question this rationale as a good whack of the local savings are going into equities and offshore, not all into NZ fixed interest/bond funds.

Our Balance of Payments “Net International Income Position” has certainly increased (as a percentage of GDP) and this reduces the risk premium we have to offer foreign investors.

I do not think the NZ economy has improved so much compared to the US to justify our bonds trading at an interest rate on par with US bonds.

We are still a remote, narrow-based economy with a small and illiquid bond market. At some point, the foreign investors will not see the merits for staying in the NZ bond market and will sell out.

When that risk point occurs we could well see a “double-whammy” increase in our long-term bond and swap rates with both the outright interest yield increasing (following the US) at the same time the bond spread blows back out.

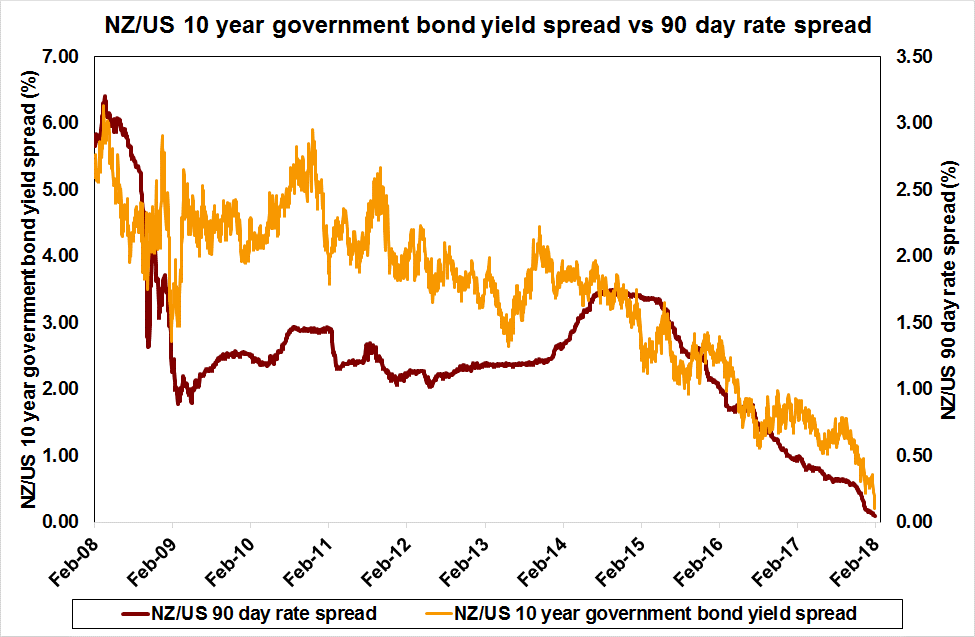

The timing of this two-part adjustment upwards in our long-term interest rates may not occur until our short-term interest start to move back up and we widen the differential to US short-term interest rates again (refer second chart below).

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.