The Reserve Bank wants to get more hands-on with our cash.

It has issued a consultation paper in which it has outlined proposals take on "a stewardship role" in the cash system, providing system-wide oversight and coordination. It also proposes:

- The Reserve Bank be given the power to set standards for machines that process and dispense cash.

- The Reserve Bank Act set out regulation-making powers that enable the government and the Reserve Bank to require banks to provide access to cash deposits and withdrawals.

RBNZ Assistant Governor Christian Hawkesby said in releasing the new consultation document on Wednesday that the changes proposed "would have significant consequences for all participants in the cash system".

“These proposals are not the complete answer, but they would help create a foundation for the Reserve Bank to be more than the issuer of notes and coins when it comes to how we use cash which is an important component of our social and economic activity,” Hawkesby said.

"Banks, cash-in-transit providers, independent ATM operators, and the broader retail sector would likely be particularly affected. We want to continue to hear views and feedback from everyone about the purpose and desired attributes for the mechanics of the cash system, and how we could collectively improve it."

The RBNZ says the purpose of any new powers given to it would be to ensure that the cash system supports an appropriate level of access to cash deposits and withdrawals, for as long as those services are needed, in order to protect those who rely on cash most heavily.

"If such powers were included in the Reserve Bank Act, we would not intend to use them in the near future, or indeed at all, unless we observed a significant failing in the ability of the system to meet the needs of the public."

These proposals are the latest step in work the central bank has been undertaking on the future of cash as society moves more and more towards a cashless system. Public submissions are being sought on the proposals and these close on November 6.

In a previous paper on the subject released earlier this year the RBNZ warned that if cash becomes less accepted and available as a means of payment then Kiwis that are already "left out" of the banking or digital worlds may be "severely disadvantaged".

That earlier paper said that the number of people currently "excluded" from the banking system in New Zealand was "small but not zero".

"The World Bank estimates that only 1% of the population in New Zealand does not have a bank account," it said.

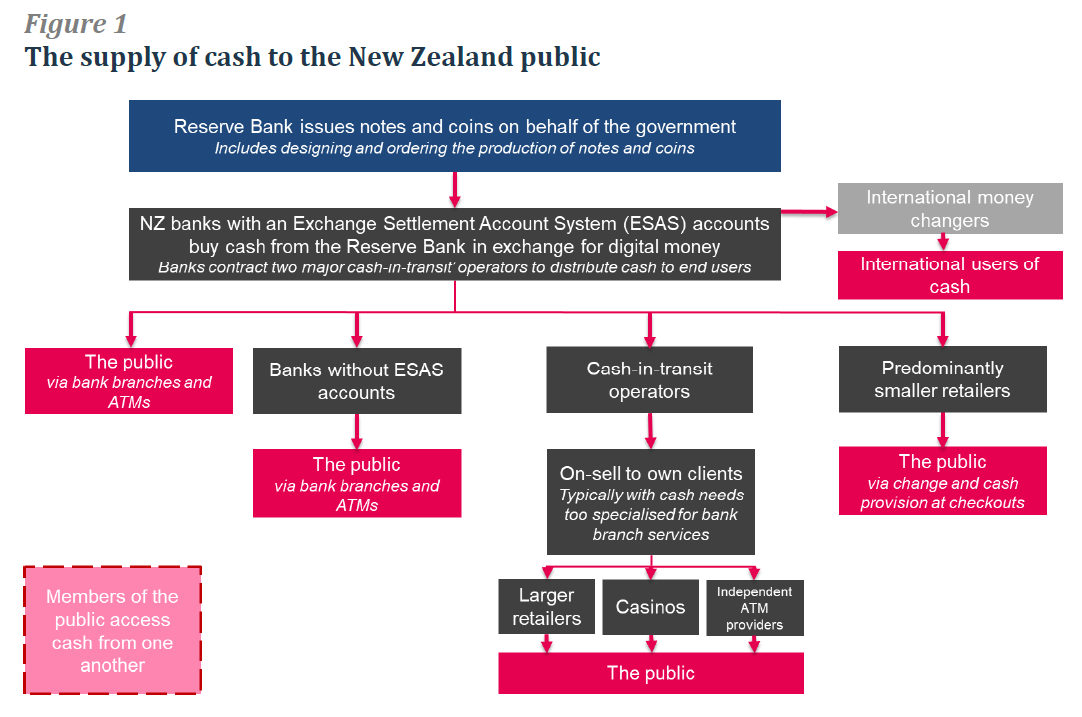

The key participants in the cash system in New Zealand are banks, the Reserve Bank, cash-in-transit operators (specialist cash transport and management services), and non-bank ATM operators.

The consultation paper says that currently the Reserve Bank has "very limited" oversight of the system that supplies cash to the public, and no influence over the quantity of cash in circulation.

"We simply sell and buy back cash to and from our wholesale customers on request. The number of banknotes and coins that enter circulation, the distribution of cash throughout the country, and the number of places where people can access cash are determined by public demand and the response of private businesses to commercial incentives.

"No single organisation has system-wide oversight of the cash system or a formal role to support it," the RBNZ says.

It also says that while the banks and other cash system participants have been willingly and actively engaging with the RBNZ work on the future of cash "there is no formal mechanism to promote cooperation and coordination across the cash industry".

The RBNZ consultation paper says that the cash system is costly to run.

"It requires costly infrastructure in the form of vaults and depots, armoured trucks, ATMs, and cash-processing machinery. It also incurs high running costs, such as those of fuel, drivers, bank branch staff, and insurance and security. It also contributes to greenhouse gas emissions."

The costs of running the cash system are shared by the main players: banks, the Reserve Bank, cash-in-transit operators, and independent ATM operators. Cash-in-transit operators and independent ATM operators are commercial entities that deal in cash for profit, so their costs are passed on directly to users. Cash-in-transit operators recover their costs by charging commercial banks and retailers for their services, while independent ATM operators recover their costs by charging people directly to use their machines. The Reserve Bank’s costs are recovered when the banks purchase the notes at face value. The income the Reserve Bank makes from selling banknotes and coins is called seigniorage, and provides "a significant proportion of the Reserve Bank’s funding".

"The consequence of the current cash system structure is that most of the costs of the supply of cash to the public are borne by the banking sector. The extent to which these costs are passed on to the end users is uncertain. Many cash services are currently provided by banks for free, particularly for individual customers. However, banks may recover some of their costs indirectly from customers by charging for other services."

The RBNZ says if the current level of cash access is to be sustained then considerable innovation and efficiency improvements will likely be required within the industry.

It says further changes to the cash system may stem from the Reserve Bank itself, as it looks to modernise its own vaulting and distribution systems.

"Our bank vaults in Wellington are ageing and we think the current arrangement is sub-optimal, with the Reserve Bank holding a large proportion of the country’s banknotes and coins in Wellington. The Reserve Bank is currently exploring a range of cash vaulting and distribution options with the banking industry and key stakeholders, and these options imply varying levels of innovation and system change. We will continue to work closely with stakeholders in the coming 12 to 18 months to reach a decision and to develop a plan to update and upgrade the current Reserve Bank vaulting system and associated commercial arrangements."

26 Comments

The advantage of a cash system is that ordinary people can use it.

The problem with a digital system is that (a) banks take their slice, and (b) it is based on debt, and the planet is already incapable of underwriting the existing debt (mostly expressed as forward bets on future energy/resources/work). So we are going to see either massive defaults and a crash of the system (via lost trust) or we are going to see the 'worth' of digital wealth plummet.

My bet is that we crash globally, that cash works in the short term, then we invent something very local - because that what all we'll be trading; locally.

The article sounds as if the RBNZ is going to protect our access to cash but I think it's more likely that this is the first step to get rid of cash readying our system for negative rates. I was wondering when this was going to happen.

I have to say that I generally agree. I think it's part of a wider war on savers, although it's still relatively stealthy at the moment, and many people are not really aware yet. I think that those with savings and those with debt are in a tug of war, and that those in power are increasingly coming down on the side of those with debt, while doing so in a manner careful not to upset the powerful elite and their savings, of course, and to give them time to arrange their affairs.

Mainstream media are starting to talk about it plainly but still only in passing (e.g. "BA governor Philip Lowe said in a speech on Tuesday night at the RBA board dinner that Australia could not ignore global trends and had to cut rates to encourage a shift from saving to investment." https://www.afr.com/chanticleer/rba-and-the-savings-dilemma-20191001-p5…). Read this as forcing cash into other asset types.

I have to wonder longer-term how long it takes before savers really start being thrown into the fires of debt as a last-ditch effort to keep this cycle going, rather than facing an economic re-set. What a reward for their thrift! But I guess they are essentially being viewed as literally cash-cows to be milked.

Feeling a bit despondent about the future today...

The answer - obvious for a decade - has been to turn your savings into tangible things you thing you will need in the future.

Before your savings (forward bets, no more, no less) are rendered worth less, or worthless.

Yes, like houses, gold and shares. Cash is no different to air-mile points, the only way to manage the liability is to devalue aggressively.

Governments do not like cash as electronic payments can be monitored, charged for and taxed. This is why Cryptos are here to stay.

I agree with most of what you've said except "while doing so in a manner careful not to upset the powerful elite and their savings." To me, getting rid of cash is part of the effort to keep inflation going inflating the assets of the wealthy elite and reducing the purchasing power of those without assets. This is the major cause of increasing inequality in western societies since the 70's - 80's.

I agree with most of what you've said except "while doing so in a manner careful not to upset the powerful elite and their savings." To me, getting rid of cash is part of the effort to keep inflation going inflating the assets of the wealthy elite and reducing the purchasing power of those without assets. This is the major cause of increasing inequality in western societies since the 70's - 80's.

I think the 1%ers are becoming more aware of the the rot setting in throughout society with the neo-feudal transformation. Disenfranchise the masses and you get the U.S. and France.

Australia could not ignore global trends and had to cut rates to encourage a shift from saving to investment." https://www.afr.com/chanticleer/rba-and-the-savings-dilemma-20191001-p5…). Read this as forcing cash into other asset types.

Utter nonsense: regulate banks to expand their asset base (loans) collateralised by new productive investment that qualifies to be included in national GDP calculations rather than predominantly lending to those buying and selling each other pre-existing assets, which is no more than speculative casino economics. Furthermore, savers have little choice about where their collective savings reside since they act as a balance sheet liability offsetting existing loans (assets). Central banks are really trying hard to transfer blame for the mess they created based upon the stupid notion of guessing the current level of the neutral interest rate.

Bang on Jetliner, those with savings and those with debt in a tug of war is what Ray Dalio goes on about all the time and says it's been back and forth for 5,000 years.

Only comment is cash can't be forced into other assets as such as the person you swap the cash for assets then has the cash.

Exactly right, I smell a massive rat... One section of the article the Reserve Bank is 'protecting us' against going cashless, then they go on an all out attack how terrible the system is...

I've been waiting for this as well.

In the interest of saving costs to the government, RBNZ and the Banks, the ordinary people will have to experience more inconvenience and trouble. This is nothing but a compulsory hijacking of the common man's comfort to feed the vultures.

I think some of the independant ATM operators need a very close examination, I have doubts about how clean their money is. I withdrew some cash from a machine in my local GAS franchise and it had white residue on it! I asked the cashier for a replacement and she wouldn't do it and when I complained to the manager he just said he couldn't do anything about it either. I'm hoping it was just construcion dust from when the store was fitted out that was trapped in the machine somehow...

Let cash die if that's what the market wants. Why force the banks to prop up the RBNZ's product.

If you're comfortable with bail-in legislation, that's your call, but not everyone is happy with it.

Right now 95%+ of our money is not physical cash. Not sure forcing Banks and taxpayers to maintain cash does much.

I'm working as a volunteer in Timor Leste. This is a cash based economy and seems to function effectively. When the ANZ shut up their retail banking function last year, thousands of people had to empty their accounts (mostly via cash withdrawal) seeing people walking the streets with suitcases full of cash. Interesting commentary on Timorese society (in Dili 40+% unemployment) is that at the time, people being accosted and robbed was virtually unheard of. Collectively probably millions of US$ was carried in suitcases.

Societal resilience is an important consideration. With digitised trading, any disruption to power supply has serious impacts. Or natural disaster like earthquake when critical comms infrastructure is knocked out for long periods. Cash provides the ability to purchase at those times.

So commercial efficiency needs to be weighed against societal resilience.

I reckon access to cash should be cemented into the human rights Act. And if there is a cost to that, then is it really any different from the investment we make (should make) in disaster preparedness.

Soon, only corrupt politicians and business persons would be allowed the use of hard cash. The rest will have to eat plastic.

There is hardly any cash held in bank vaults in NZ, compared to other digital bank assets - savers would be hard pressed to turn their bank liability claims into currency in any circumstance.

Austrailia is looking at a cash ban.

Yep, prep for negative interest rates.

The tell being the laundry list of reasons, including green house gas, for doing so. (Make the armoured trucks electric!!!).

Add in the fact of savings being taken for bank bail-ins. It feels like cash (already debt based) is rapidly becoming a liability!

Things are getting unconventional.

Astutely put. It's interesting to see what we physics/Limits to Growth types have long foretold, playing out in a hithertofore ignorant language; namly economics.

Yes, things are different. We have never been here before, and it can only happen once, globally.

Agree with all the commenters above - plus any move to remove cash is an early move to undermine democracy as it effectively removes choice, and embeds banks, private business's, within any transaction.

And to add to Jetliners comment above, those elites are more likely to be a bank owner than the ordinary people who carry debt, so if they face additional costs they will be offset by profits somewhere else.

What about USD cash machines? USD notes seem to be the choice of the citizens of failing states worldwide. That or gold coin selling machines. Apparently there are now more USD notes in circulation outside the US than in, as more countries choose to trash their own currencies. Couldn't happen here, of course. Er could it? Oh, wait a minute, it already has.

Surely, each time house prices double, it means the purchasing power of the NZD has halved?

Someone thinks there is going to be a bank run and wants the power to shut off the cash?

If 97% of the money in circulation is created by the Banks (loans) and 3% created by the Government (cash) and there is talk about getting rid of cash doesn’t that tell you something? As to who is actually wanting to control everything?

Agree Sailor Rob / Patricia. Societies across the globe are being gradually hearded away from cash to digital by the political & financial elite in their pursuit of control & self interest - there’s the rat. The US no longer prints $500 bills - Hasbro, the makers of Monopoly no longer uses notes it uses voice activation. As I’ve said before, when you put money in the bank it no longer becomes yours. Do we get a choice in the decision making process - hell no! because it’s all about protecting us, efficiency and cost. - yea right!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.