The Reserve Bank is warning that if cash becomes less accepted and available as a means of payment then Kiwis that are already "left out" of the banking or digital worlds may be "severely disadvantaged".

The RBNZ said in its recent Financial Stability Report that it was undertaking analysis of the future of cash.

It has now released a paper on the issue.

The paper says the number of people who are currently "excluded" from the banking system in New Zealand is "small but not zero".

"The World Bank estimates that only 1% of the population in New Zealand does not have a bank account," it says.

"Meanwhile, the Reserve Bank survey of cash use in 2017 found that 4% of people surveyed had used only cash in the previous seven days. Some of this will have been due to personal preference and some to financial exclusion. This group was weighted towards those aged over 60."

The paper points out that currently, no state agency has a mandate to ensure that the public can continue to use cash, and no agency has considered how reduced cash availability could affect our society.

The paper says a contraction in the cash network without regard to the wider benefits of cash in society might significantly disadvantage people who rely on the unique role that cash plays in their lives.

"This would be considered a market failure to the extent that commercial operators did not fully incorporate the wider network benefits of cash. As a result, government action could be warranted following the completion of this review," the paper says.

RBNZ Governor Adrian Orr says the bank views the forthcoming issues over money as centring around there being less cash - "not becoming cashless".

"There’s the real possibility of a contraction in the cash system which could end up affecting lives."

New Zealand should be making conscious decisions about the future of cash so that we can be prepared for future innovations, and ensure that sectors of society are not unfairly disadvantaged because cash falls out of favour, he says.

He also says that international tourists, people in the four Pacific countries which use New Zealand currency, and people in New Zealand who use cash for cultural customs might all be negatively affected without workable substitutes to cash.

"Cash gives privacy and freedom to spend that other payment methods do not, and its ability to back-up other payment methods in a crisis also needs examination. The potential consequences of cyber threats at national and personal levels might also be elevated with less cash around," the RBNZ says.

One upside of less cash, however, could be increased efficiency and reduced overall costs for electronic payments systems.

"As well as implications for cash users, there are consequences for the Reserve Bank and the banking industry. This includes choices for the Reserve Bank’s next generation of vaulting, and how to ensure the system for distributing and circulating cash is as cost efficient as possible with fewer transactions. We need to be ready to face the cash equivalent of falling posted letter volumes,” Orr says.

He says the RBNZ is working with its trading bank customers and others in the cash system to look at those issues.

"We are hoping that the kōrero building from the release of the paper today will give challenge, amplification, and most particularly put human faces and voices to the issues raised by less cash,” Orr says.

The Bank is urging discussion and feedback so that it can refine its views and develop options to help manage the future of cash.

It says it will publish an analysis of the feedback received, as well as further research. A formal policy consultation may follow depending upon what emerges from feedback on the just-released paper and further research and analysis.

Less using it but the amounts are going up

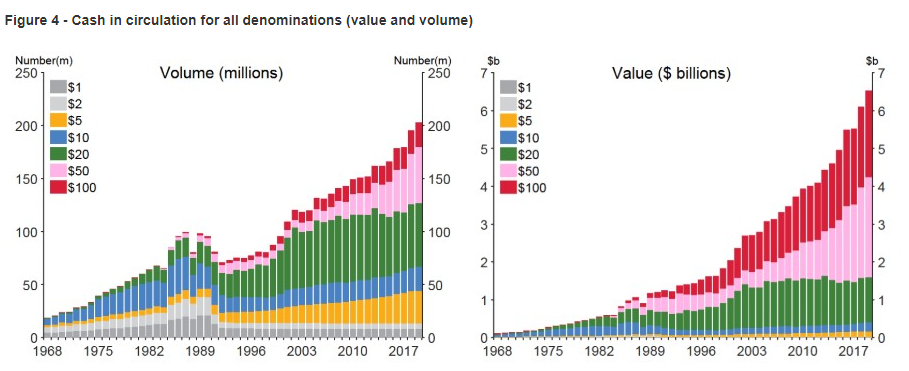

The paper points out that while significant portions of the population hardly ever use cash, the amount of cash in circulation (CIC) has continued to rise (see graphs above). The central bank also makes the interesting point that it only knows where about 25% of the issued cash actually is.

The RBNZ says International studies suggest that New Zealand’s CIC trend could be due to an increasing demand for cash as a store of value over time and a falling demand for cash as a medium of exchange.

"The drivers of an apparent increase in demand for cash as a store of value are largely unknown — the Reserve Bank can only identify the whereabouts of 25 percent of CIC. Inflation could also be a contributor to the growth in note holdings over the history of the note series — as prices increase, people must hold more cash if they want to maintain a similar store of value."

The RBNZ says another possible driver of the trending increase in CIC could be increased currency issuance to offshore currency holders such as money changers abroad. This might reflect tourist demand for notes before they arrive in New Zealand.

In fact the only two countries in the world where the amount of cash in circulation is falling are currently Norway and Sweden.

20 Comments

The answer is bitcoin. Or heck, maybe even this Facebook Libra coin or some competitor

So... you want to solve the problem of financial exclusion with an even more complex and exclusionary payment method.

One of my work colleagues recently applied for a mortgage. The bank downloaded his bank statements for the last 12 months and did a whole lots of analysis in his spending patterns! They questioned him on how he spent on coffees, some spending on betting websites, what bought from JB Hifi and frequency of eating outs.

I guess one way to avoid this is cash.. so cash will be back as king shortly!

With that kind of financial analysis by Bank's Definitely Cash is King

They will still be asked to account for how the cash was spent though

The RB, bless their innocent souls, ignores the black economy, which generalising wildly runs exclusively on cash. As it's total value is possibly north of 10% of GDP and may be up to 20% - think, Northland - the cash is gonna be around for quite some time yet. And it's also unclear how the Black Economy and the Wellbeing Accounting manage to intersect. My sense (feelz...) is that never the twain shall meet, except perhaps in A&E and the Health budget as us toilers pick up the pieces....

Well, the RBNZ reports $6.79 billion CIC and banks retain $0.888 billion in storage - hence ~$5.90 billion could be available to the black economy, which represents ~1.29% of outstanding NZ bank credit ($455 bn). Fringe operators in anybody's language, given a reasonable portion will be held for emergency transactions.

Indeed Audaxes. Which is why the money gets washed elsewhere to enter the digital/legitimate system of money. Recently an ice-cream parlour opened and closed within 3 months in my neck of the woods. Drugs was the business, ice-cream the launderette. Interesting discussion from Professor Werner attached on money creation by the private banks, ignore the interviewer but hopefully people will absorb what the good professor has to say. There is a war on cash, they are even making it hard to pay tax with cash now. Less that $1,200 dollars in cash per kiwi is a tricky spot to be in in a crisis... But we were the guinea pigs for EFTPOS etc etc, compliant and unquestioning folk are great fodder for a woolly balaclava pulled down to the chin.

A major concern in this is that cash gives the individual freedom, independence and privacy. All three of these are under assault by our govt and most govts around the world. That makes me pessimistic about its future, sadly.

The Reserve Bank could replace cash with blockchain-based digital wallets. This would help the IRD to capture the black economy and "cashies", and open the way for a government to introduce a financial transactions tax, painlessly clipping the ticket every time money changed hands, or rather, wallets.

The Reserve Bank could replace cash with blockchain-based digital wallets. This would help the IRD to capture the black economy and "cashies", and ensure total and permanent Gubmint control over every aspect of every soul's fiscal life from cradle to grave. What could Possibly go Wrong?

In a permanently-retrenching world, there will be Hong-Kong-like protests and usury will be outlawed (if societal cohesion persists). There is no room for interest in a powerdown world - and I'm sure they know it. They are extending and trying not to blink. Facebook is an interesting diversion, yet another challenger for a dwindling pie.

And loc; folk will just invent local currencies - as they always have.

https://en.wikipedia.org/wiki/Totnes_pound

Interest/usury has existed for thousands of years, so I don't see that changing anytime soon. Even if it was outlawed (highly unlikely as govts are the largest borrowers and would destroy the bond/debt markets overnight, along with the global economy...hey, presto, no tax income for govts, ooops!)

pdk,

'permanently retrenching', 'usury will be outlawed'. You big statements,but I never see you explain just why you believe them to be true. You quite often provide links to other sources,but I never see you back up your always deeply pessimistic assertions with any actual evidence.

if I am selling you short,I apologise. i am no Pollyanna and quite apart from other issues,climate change will cause massive disruption to much of the world. We have just learned-thanks to old spy satellites, that Himalayan ice is disappearing much faster than previously thought. It requires only a very limited knowledge of geography to understand why that is serious and not just regionally.

And what happens when the lights go out? Even PDK doesn't ask this question. To remove cash results in several things; it places a total dependence on uninterruptible power to run technology to allow for transactions and we all know that even today this cannot be guaranteed, it places unlimited power into the hands of private companies (the banks) making the ordinary Kiwi very vulnerable, it further disenfranchises those at the bottom of the socio-economic pile (note that all of these in the last two points are VOTERS), and makes the Government vulnerable to the banks over economic and fiscal policy.

Consequences will likely include the black market economy growing exponentially as banks exercising their muscle and the Government forgetting who they represent and are supposed to protect, screwing the pooch royally.

George Orwell would be so proud of who ever thought of this idea. They must have gone to the same school as President Xi Jin Ping

Surely that's Emperor Xi. And one of the results if the lights do go out is that hordes with pitchforks and torches will descend on anyone with supposed 'resources'. And one of the first targets would, as history shows, the Kulaks, because they appear to have more of them Resources and that is Sooo Unfair. Rural smallholdings would, of course, be at particular risk...

Notice how the amount of cash held in $50s and $100s explodes in 2014-16?

Not foreign buyers injecting cash in Auckland then?

Anecdotes of suitcase gentleman visiting for weekend to buy 10 houses.....

This is the money RB cannot locate and it has now been truncated by OBB.

Effect on liquidity?

Notice how the amount of cash held in $50s and $100s explodes in 2014-16?

What are you talking about?

The trend in high-denomination notes is consistent from the early 00's right through to today.

.

I have noticed the number of ATMs in Rotorua has reduced over the last year. This forces people to use their cards wherever they go. It means everything can be tracked. I'm not a fan of my bank or the government having knowledge of every dollar I spend. It's bad enough that ads on my phone and computer are already targeted based on my shopping and stores I visit, whether I buy or not. Apart from my direct debits, I withdraw my monthly budget in cash, this way also controls what I spend.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.