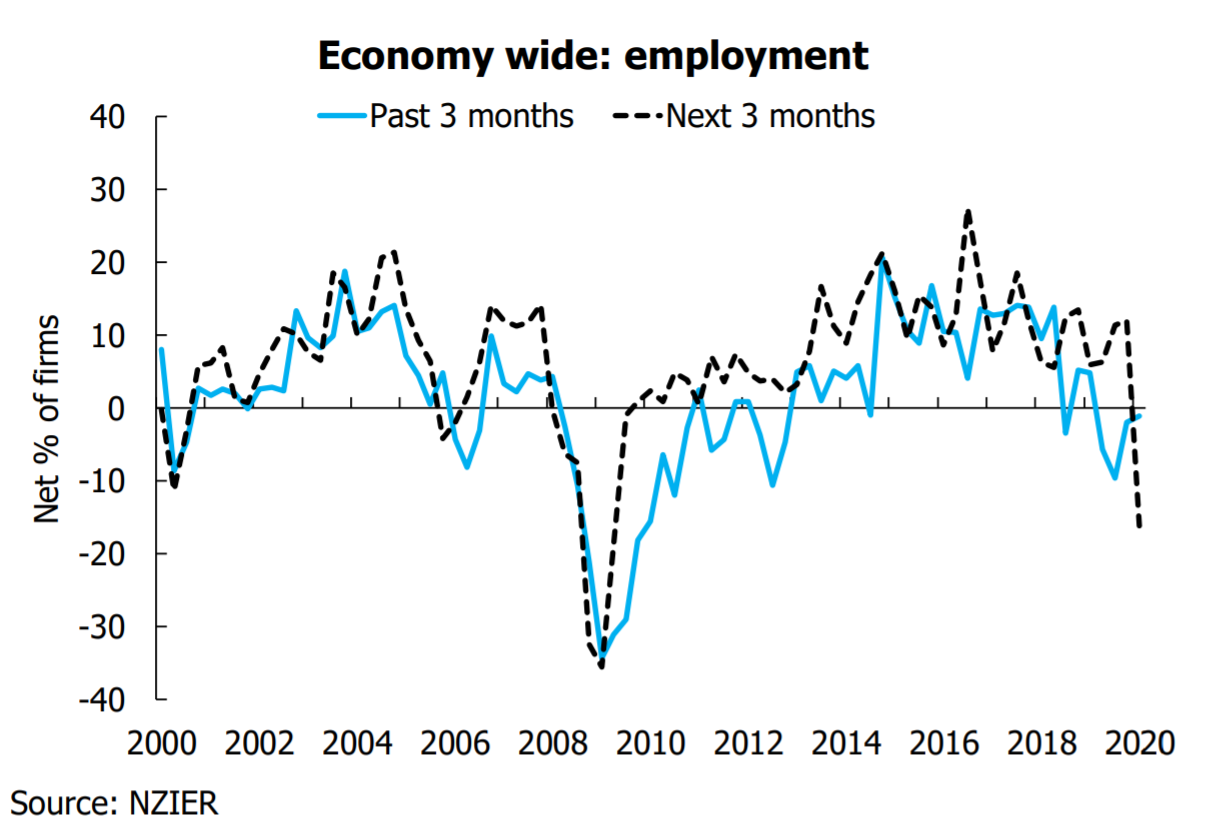

The NZ Institute of Economic Research's influential Quarterly Survey of Business Opinion (QSBO) has found that a net 16% of New Zealand businesses are looking to shed staff over the next quarter.

The survey was conducted up to March 20, so doesn't include the impact of the lockdown.

But even so, it is predictably gloomy.

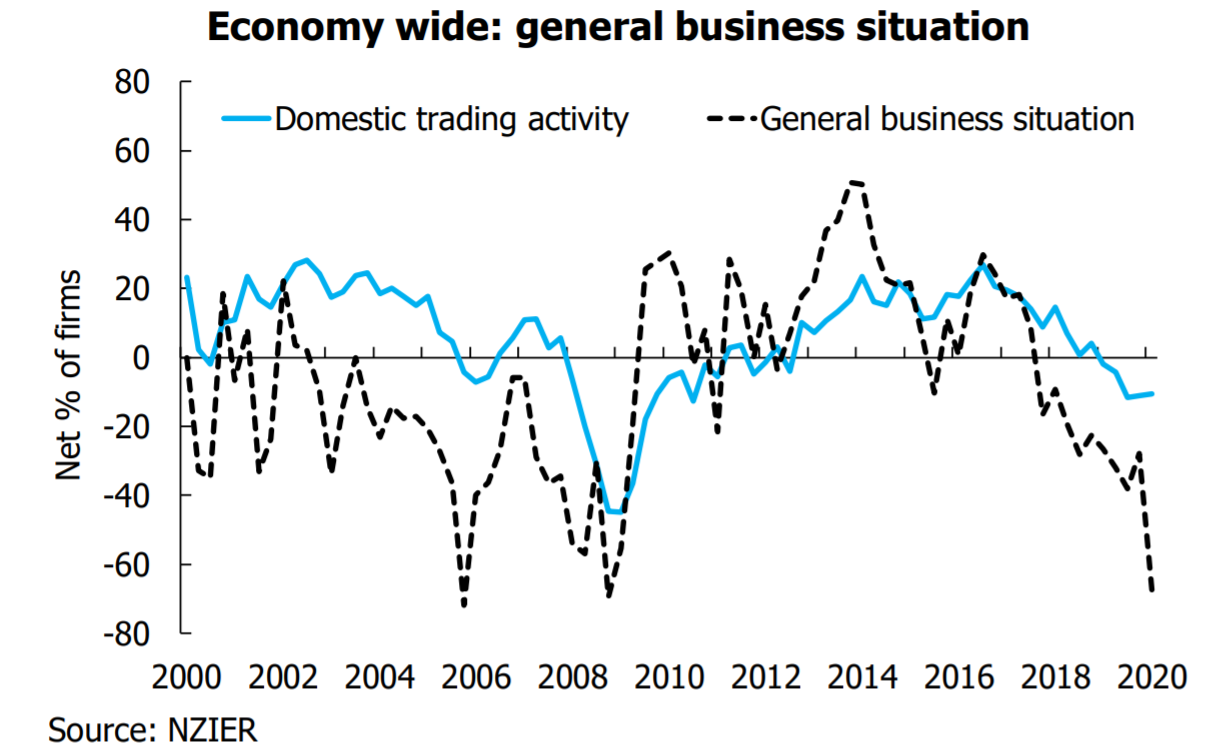

The reading for future hiring intentions is the weakest it has been in this survey since June 2009, while the overall reading for the business confidence is the weakest since December 2008.

NZIER says the survey is being issued in "extraordinary times".

"The QSBO shows a sharp decline in business confidence, with a net 67% of businesses expecting a deterioration in general economic conditions.

"When it comes to demand in their own business, the weakness was most apparent in firms’ expectations for the next quarter. A net 11% reported weaker demand in their own business in the March quarter, but a net 13% expected weaker demand in the next quarter – a marked turnaround from the 5% of businesses who had expected an improvement in demand in the previous quarter.

"A net 16% of firms plan to reduce headcount in the next quarter. Investment plans for buildings and plant and machinery have also been curtailed, with a net 15% and 7% planning to reduce investment in these areas, respectively."

NZIER said although the pessimism was broad-based across the sectors, the services sector was particularly pessimistic. A net 76% of services sector firms expect weaker economic conditions over the coming months. With firms in the services sector pessimistic about the outlook for demand ahead, a net 19% are looking to cut staff numbers.

Manufacturers were also downbeat, but there was a divergence between weaker domestic demand and stronger export demand in the weeks leading up to the lockdown in March. But a net 10% of manufacturers expect export demand to deteriorate in the June quarter. With the majority of the global economy shut down with a range of measures aimed at curbing the number of COVID-19 infections, economic activity has dropped sharply and there are widespread expectations of a global recession. This will have a negative impact on global demand for our manufactured exports.

NZIER said prospects for the building sector are mixed, with the measure of activity in architects’ own office pointing to a soft pipeline of residential and commercial construction, but a still-solid pipeline of Government construction work. The Government is expected to play a greater role in construction work as private investment weakens and has indicated its intention to accelerate any ‘shovel-ready’ infrastructure projects that can start within the next 180 days.

"There has been more discounting in the retail sector as demand weakened. The impact of the lockdown will be severe for most retailers which are not deemed essential, given it largely removes any opportunity for sales revenue."

57 Comments

Could be a good time for some countercyclical behaviour. I bet these large companies laying off some great staff just by virtue of having to act so rapidly and in such an arbitrary way. For an astute business person this could be a good time to start thinking about skills you where unable to recruit while the market was tight.

And a lot of young people working in the tourism industry are naturally outdoor types who would likely love to participate in ecosystem restoration projects.

Government ought to think of gearing up DOC for all kinds of unfinished/delayed project work.

These results seem far to optimistic.

I mean a net 67% of businesses see the economy getting worse...does someone really think its not?

Its really a lot worse than one could imagine, and I feel for those in a worse off position than ours , it must be really stressful to face unemployment without a backstop , and even we, a middle class family, have seen the effects

We a family of 5 , with 3 adult children . Three weeks ago we were all employed with really good incomes

With effect from 1 April , my wife's employer has made 100% of the staff redundant and are paying them the subsidy and closing the doors on 1 June .

My eldest son who is a junior Quantity Surveyor has just been notified he no longer has a job, he is moving back home as soon as the lockdown is over .

My daughter is a Masters student who had a part time job , and that work has dried up , so she too is at home

My youngest son is in an essential service as a second -year apprentice keeping the electrical grid working , but because he is an apprentice , he is at home and not working, but being paid the minimum wage , no overtime , no standby or call outs , which are a significant part of his earnings .

So, as a family , we have gone from 100% employment (with a sizeable total family income ) to 60% unemployment in two weeks, and total income has dropped to around half .

I am expecting that to get worse .

We are unlikely to be included in the unemployment statistics as the MSD will never know our position , we do not qualify for welfare, we have assets and savings , and we have never been on welfare and dont wish to ever do so .

Our Kiwisaver has been gutted , all 5 of us have seen a staggering destruction of personal wealth, with my wife and I particularly hard-hit

Its a mess , our spending has been curbed to budgeted essentials only , and luckily we have no debt , we have unencumbered assets and investments and cash enough to survive for 2 years on essentials , I really feel for those that are living paycheck to paycheck.

Ditto, if it's any consolation; 2 of us, wife now at home; 3 children - the two in NZ on 'standby' ( son's marriage has cracked under the strain, and now he's a forced sell at the worst possible time) and the other in Qld just told her job at OPSM finishes at the end of this month if nothing happens.

But "cash enough to survive for 2 years " will be the saving grace. We really are, all in this together. Cheers.

Tough times no doubt.

Adaptability is key.

Still plenty of jobs at minimum wage end e.g. security guards, fruitpicking, nursing etc..

Obviously not good for ones chosen career, but we'll get through this

A lot more jobs may be minimum wage now. Just heard a friend has had his pay cut to the new minimum wage. He either agrees to it, or ...

Dp

I don't think many of the decision makers really understand this hardship. Nor many people in comfy public sector roles.

Painful stuff to read but the generous sharing of personal stories is appreciated. We are addressing the post lockdown govt policy vacuum by a 4 stage plan that will be triggered progressively in ratio to the hit to our T/O. It is a conflicting picture. Rumours of mass cancellation of AKL house construction contracts are circulating but our commercial vertical construction contract pricing team is flat out, with more staff added this week. Principals of most large scale long term developments are emphatic they have the finance and that their builds will go ahead as planned, which seems to defy logic. We'll soon see. But that we'll have to let a good number of our great people go is distressingly evident.

Or that the real 'minimum wage' is....zero.....

Pig headed govt ideological obstinacy to proceed with increased min wages in the face of economic disaster knowing that this will accelerate the misery.

That was an ideological comment also.

Whose misery?

Whose misery?

The majority

In a depression, the majority are unemployed.

Any thoughts on counter/opposite monetary policy to fix all this?

It would appear that we're ruined if we allow reserve banks to continue status quo....we are heading into a big nasty recession given all indications - so lets accept that and try to do something different.

Why don't we put the OCR up to 10%, give people with savings some return. Give them the option to spend in the future, instead of taking their cash from the bank and hiding it around the house and giving them no ability to invest in the future (which appears to be the effect of low rates...spend now, create bubbles, crash the system). Yes there will be defaults, but there are going to be defaults anyway? Looks what is happening.

Clearly the actions post GFC haven't worked, so why not try the opposite? Playing devils advocate here....fire away... yes it will destroy the housing market, but I think current plans will anyway. And at least higher rates will give savers/FHB's an opportunity to grow deposits and a chance to enter the market when prices fall. Isn't society better with a higher rate of home ownership?

Too many important people with too much to lose with a strategy like that - albeit on the right track.

Think SCF for a template of who's going to get saved, and who's going to pay for it....

...at the expense of FHBs who entered the market after waiting years for non-existent government interventions as promised the election?

Yea, I'd be rioting in the street. You can only make one group of people the crash dummies so many times before people start figuring out how rope and lampposts can be used to make a daring yet effective political statements with the 'assistance' of their hitherto-overlords.

But....the entry cost ( purchase price) for FHBers will be so much lower for the next lot than today?

Those who've already bought - doesn't matter which demographic they are from, will simply stay put, and the term of their loan ( time) will get extended at 'compassionate' mortgage rates - 50 years not 30?.

Just think. The next home ,after the First Home, ( upgrading?) will also be less - for all buyers.

Yes everyone will be affected to differing degrees!

Many will be out of work unfortunately and others will take a pay cut until things pick upon,

Personally at the moment wen haven’t had any tenants not pay the full rent but there has been a few enquiries.

We are fortunate it won’t affect our standard of living at all once we are out of hibernation due to our choices however we will need to help out some of our friends who are less financially fortunate which we have done several times previously.

I do believe that people will have changed views on things going forward including investing in more solid investments like housing rather than gambling on shares!!

I do believe that people will have changed views on things going forward including investing in more solid investments like housing rather than gambling on shares!!

The whole point of the above comments is that NZ needs to stop taking wealth from savers to blow asset bubbles...not to encourage more of the same.

Haha yes I almost liked TM2's comment, then he added the last sentence. The problem can't be the fix...but that doesn't seem to resonate with those who have skin in the game. (i.e. high debt, high house prices can't be the fix to high debt, high house prices...unless of course you're a property investor!).

TM2. We lease multiple commercial buildings and all bar one (a notoriously combative property management outfit) have proactively offered multiple month rent reductions, without us having to go down the C19 prevention of access argument route. The reductions in all cases are substantial. We are impressed at their collaborative partnership approach.

I don’t think you will “be rioting on the streets” , the lockdown is something that would prevent you from going there. Ohhh, sorry, I forgot, the lockdown is to prevent the virus to spread... Stay at home

Good point. I guess the yellow vest problem has gone away in France. For now.

Am I reading this correctly? If interest rates go up, you'll be on the streets stringing politicians up from lampposts? You are completely insane mate, check yourself into the nearest facility.

If interest rates are tripled as suggested simply to appease cashed-up deposit holders and potential FHBs because the government couldn't deliver on their election promise of actually provided cheaper housing, then yes, many mortgage holders will be financially ruined. I can't see them taking it that well, especially after being forced to pay over and above the odds for housing in the first place.

Frankly, some of us are sick of always being handed the bill to make life easier for others. I am one of them. If I loose my house so boomers can get better returns on their nest eggs, am I expected to be partying in the streets with gratitude?

I'm sure many net depositors see themselves as currently footing the bill for your little property excursion. I'm sure the banks means tested you at a higher interest rate though, so you should be fine right? Might just have to lay off the avocado toast for a bit, cancel Sky TV even.

ohh, I'm afraid the Sky TV will fall another 60% then

Someone (most likely many) are going to lose in this game (I don't have a better term to use) that is being played out. Government can't prop up wages for long (debt will get too high) so there will be high unemployment and a significant drop in earnings for businesses and families.

Question is, who do we protect. If we try to protect everyone, everyone loses. Someone is going to see hard times ahead....if we try to protect those with high debt, we will likely make things much worse in the future.

Just my opinion, it isn't nice, and it isn't pretty (and I'm not a boomer..).

If interest rates are tripled as suggested simply to appease cashed-up deposit holders and potential FHBs because the government couldn't deliver on their election promise of actually provided cheaper housing, then yes, many mortgage holders will be financially ruined

What you are describing is the exact unwinding of what has been done to savers over the last years simply to appease debted-up asset holders, because the government could deliver on their election promise of improving NZ's productivity.

If it's not fair for the central bank to unwind it, was it ever fair for them to wind it in the first place?

I'd generally agree, but go you one further - we need to disestablish the reserve bank entirely. The interference of central banks in the market is the reason we are in trouble today, the virus was just the trigger. They have proven time and time again over the last decade that either the economic textbook they are reading from is wrong, or they are wilfully blowing asset bubbles.

One wonders how many investment properties the leaders in central banks and the governments they work with have, on average.

Recall that Bill English - who denied the Reserve Bank the DTI tool to help slow asset bubble creation - was leader of a party with an average of 3.4 houses per MP. So they've interfered to inflate the value of their own portfolios, now putting the New Zealand economy at risk because of that.

How many houses per MP did Labour have between 2000 - 2008 when house prices rose faster than at any other time, and why do people keep pretending like John Key signed an executive order on his first day that invented homelessness?

I remember John Key campaigning on solving the housing crisis because it was destroying a generation's home owning prospects. He said all the right things, you can still find the old interviews from the time online. As soon as he got in though, there wasn't a housing crisis anymore - it was a sign of our prosperity.

Yes but he quickly realised there was political gain to give people paper wealth...so 'at the end of the day' his policies were very self centered - as soon as he realised the market had peaked (2017) he jumped ship so he wouldn't be at the helm when things fell apart.

And remember Winston Peters warning, about the time he was choosing whether he would side with National or Labor...it was that we were on the very edge of a recession when National left office.

https://www.interest.co.nz/opinion/94907/acting-pm-winston-peters-warne…

What surprises me is how popular National have remained - even with Bridges in charge. But many of the National voters I talk to are property owners or property investors. So why would that party want to end the party?

I put it to you that JK realised that long before the election, and merely said whatever he thought would get him elected with no intention of following through.

Maybe the support for National has got something to do the the Labour Party lineup, as a very recent example, the health minister David Clark leads the charge, out mountainbiking and driving 20kms to a beach with his family while the country is in lockdown and supposed to be staying local, dah!

Indeed. Precisely why many folk voted for John Key. Great speech, John: https://www.scoop.co.nz/stories/PA0708/S00336.htm

I spoke to him around this time, and I voted for him on the basis of this commitment.

He and his government clearly failed.

I did a quick check for you. Adrian Orr has three property titles registered in his name, Graeme Wheeler has three and Alan Bollard has four. Haven't bothered to check if any companies they are shareholders or directors of also own property, but that should give you an idea.

hey , how and where can you quick check those things?

LINZ has all sorts of wonderful information freely available. The particular dataset I used is the NZ Property Titles Owners List, which is a list of every property title in NZ and it's owners.

https://data.linz.govt.nz/table/51564-nz-property-titles-owners-list/

To download this you have to create an account and agree not to use this for commercial purposes, then you're good. This is a very large csv file so opening it in Excel probably won't work - I have written it to a database and can query from there, but you can also use the command line utilities cat and grep if you have linux or WSL on windows.

thanks for the link, but it says Page not found

Try going to https://data.linz.govt.nz and searching for "NZ Property Titles Owners".

ok, could not find that one. I found just Titles, but not owners

You do need to create a Koordinates account and agree to the terms of use before you can access it I believe.

People on work visas losing their jobs, this is going to be a massive issue:

https://i.stuff.co.nz/national/health/coronavirus/120867883/broke-and-d…

Yes there would look to be a significant restructuring of our work force and society taking place - and happening in as little as a few weeks. I personally have no issue with what is going on - globalisation appears to be great in good times, but quickly falls apart in a squeeze such as this.

400,000 working visas! What percentage is that of our labor force anyone know? Edit...just looked. 2.6million. So that's 15% if my calcs are right. So if I was an employer I'd probably look to put citizens first as well - as long as they were willing to work at a rate the company can afford (which might be one of the many issues we are going to face going forward....what is going to give first, the debt people owe, or the amount they are willing to work for...it could be a nasty cycle downwards).

But we're paying Australians who are working in NZ, correct?

Solution : 'The Ministry of Social Development is advising those ( in the work visa category) in financial difficulties to approach their embassy'. The German government, among others, is progressively repatriating its citizens.

As the NZ govt has said ........just, go, home.

IndpendentO. According to a recent govt statement around 200K in the work visa category are not eligible for welfare. Few of these would have much property or debt in NZ, I imagine.

I was stunned when I saw it was 400k.

If half of those leave NZ that will have some profound effects, some of them positive (depending on your perspective)

Well perhaps after this our leaders will actually form a population policy that isn't based on hard working migrants coming in their hundreds of thousands with a dream of building a new life to end up in low wage jobs and unable to go back home because their families went into debt to get them to NZ. Sold a dream and ended in crummy jobs. Let's put pressure on our politicians to get a proper policy that doesn't exploit migrants and makes everyone in NZ better off, not just exploitative employers. Shane Jones is the only one who has made any noise about this, but fool me once shame on you, fool me twice, shame on me.

There’s an even worse problem, according to the MOH. Some 5000 people die each year of it in NZ or 13 people a day. Something called Benson&Hedges-20, apparently.

Are we all at risk of dying of this condition and how contagious is it?

The tea leaves tell their own tale, but the graphs are interesting. Reality is a little more moderate than our emotions allow at times, but that's the good news. The other reality is the recent downward trend & we're talking cliff face stuff here. Most of the damage has already been done. The combination of the speed of the virus & the speed of the global reactions, it's all knee jerk stuff with a weeks worth of study behind it. Nobody's got it right, but then nobody was expected to get it right, right?

Remember we're all in this together. The good, the bad & the ugly will be experienced by everyone at some point in some way, shape or form. What I'm hoping is that we're brave enough for some new millennium thinking that might help most of us back into a job, or being able to stay in the place where you are at a bit longer, or the encouragement to try new things, new ways or better ways of doing stuff perhaps. This is a great chance for a reset. Are we brave enough or mindful enough or clever enough to approach this moment with an open mindset, or will we end up arguing the toss in the lead up to the election by throwing personalities under the (empty) buses once again?

This will probably fall on deaf ears, yet, for what it's worth, a suggestion for a few newly unemployed. Blockchain. I see most have already stopped reading. Employment globally in the digital market has been growing enormously, and many, if not most, organisations will be, or already are, employing blockchain in aspects of their business. There are courses online, and research is implicit. The financial services sector in particular will/ are, migrating many of their systems to blockchain, as the efficiencies gained are implicit to a low margin environment. You could be one of the few walking in the door, as the many are walking out. Simply a thought, like I said, it's only for a few, yet blockchain has been a dirty, hidden, at times possibly abused word in financial sectors. Point is, not many even know about it, or it's applications. Nike use blockchain to track their products from factory to customer, customers use it to check the authenticity of their purchase. There are many more large, and small business using blockchain, and qualified people are thin on the ground. Even the likes of the big banks, jp Morgan, HSBC etc, they're all into blockchain. Hope it helps at least a few.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.