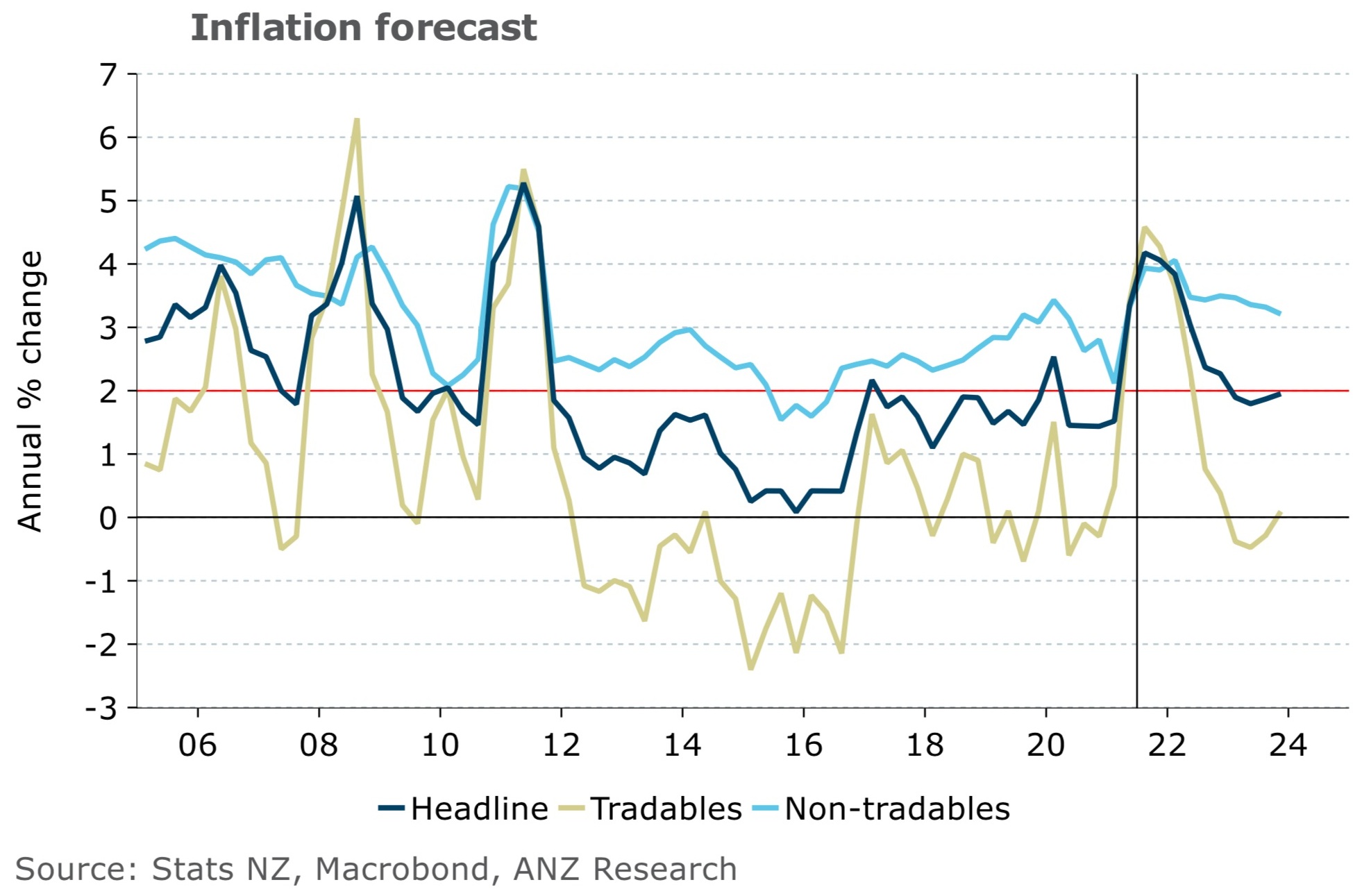

Economists at the country's largest bank now see annual inflation in New Zealand peaking at 4.2% during the current, September, quarter.

And the ANZ economists believe that annual inflation, which soared to 3.3% in the June quarter, will stay outside of the Reserve Bank's targeted 1% to 3% range for some time - only dropping back to 3% by June of next year.

While all the major bank economists have been pushing up their near-term inflation forecasts following the actual June quarter figures being so much stronger than expected, a pick of 4.2% as by ANZ appears to be the highest so far.

In an NZ Forecast Update publication, ANZ economist Finn Robinson and senior economist Miles Workman say they've "revisited" their assessment of capacity pressure in the New Zealand and believe the country currently has a 'positive output gap' - meaning essentially the economy is trying to grow faster than supply constraints will allow. They see that situation enduring over the course of this year and next.

"We expect that CPI inflation will reach a high of 4.2% [year-on-year] in Q3 2021, as shipping disruptions, the border closure, materials costs and other one-off factors (eg rates increases) see prices surge. Underneath all this is a strong underlying inflation impulse, driven by the very tight labour market, rising inflation expectations, and firms finding that they have the power to pass on higher costs to consumers," they say.

On the capacity pressures, Robinson and Workman say the economy is currently trying to grow faster than Covid disruptions and labour shortages will sustainably allow.

"With goods in short supply, the labour market at or around full employment, and labour demand continuing to rise, demand in the economy is surging ahead of supply (ie a positive output gap). That puts a lot of pressure on costs, and importantly, we’ve seen firms passing on these rising costs to consumers."

The sizeable underlying momentum in inflation and capacity pressure "necessitates higher interest rates".

"We are forecasting the OCR [Official Cash Rate] will be lifted 25 basis points at the August MPS [Monetary Policy Statement], with subsequent hikes at each MPS until the OCR reaches 1.75% in November 2022. However, the strength in inflation means that an October hike is a possibility."

As for when inflation will start to drop? They forecast annual inflation will be down just slightly by the end of December 2021 to 4.1%, then 3.8% in March 2022, 3.0% in June 2022 and 2.4% by September of next year. They forecast it will get back just under the RBNZ's explicitly targeted 2% level by March 2023.

But in the near term they expect "very strong" inflation over the current quarter.

"This reflects a continuation of the drivers we’ve seen recently: housing costs, transport costs (in particular petrol and car prices), and food prices. In Q3 we can also add larger-than-usual council rate rises to the mix too. And the shipping disruptions from Covid are showing no signs of slowing, with costs continuing to surge at an almost exponential pace. Obviously that can’t continue forever, and we do expect a sizeable retracement of some of these price increases in the future. But for now, these costs continue to put pressure on consumer prices."

In terms of why they think inflation will be brought back down again, Robinson and Workman say the anticipated OCR hikes "will be very effective at taking some of the wind out of the economy’s sails".

"That should put a dampener on domestic inflation pressures, and help to contain rampant household inflation expectations. But the tight labour market should still keep non-tradables [domestic inflation] running slightly over 3% y/y. This will be essential for meeting the 2% inflation target in the longer run, given that the removal of large tobacco excise tax rises is expected to knock 0.2-0.3 percentage points off headline inflation.

"Secondly, significant disruptions to the global economy caused by Covid are expected to dissipate. While slow vaccination progress and the ongoing development of new Covid variants has slowed this process down, eventually things should start to normalise, although what the post-Covid 'normal' looks like and when we get there are both very uncertain. We do expect to see some of the crazier price increases reversed (at least partly), especially around global shipping. So while we’re forecasting very large rises in tradables prices over the next year, we’re also very likely to see prices fall further out."

For the future, the two economists see "balanced risks" to the inflation outlook.

"On the downside, there’s risk that a global normalisation in prices and shipping costs could see tradables inflation fall significantly enough to drag overall inflation well-below 2%. This wouldn’t be a permanent drop though – just a return to normal, that the RBNZ would likely look through (provided expectations remain well-anchored).

"...On the upside, there’s the risk that the extremely strong price rises we’re expecting in coming quarters cause inflation expectations to become significantly detached from the 2% midpoint of the RBNZ’s target range. Were that to happen, and if it were to be sustained, inflation could quickly get out of control and require a more aggressive monetary policy response than otherwise. This is one reason for the RBNZ to start removing stimulus soon, so as to head off runaway inflation expectations (which have already surged in recent months, particularly on the household side."

The ANZ's own Business Outlook Survey, next due out on July 29, will give the business sector's updated view on expected inflation levels, while the RBNZ's Survey of Expectations next due on August 12 will also provide a much-watched view of where inflation's seen as heading, particularly over the next two years.

Consumer prices index

Select chart tabs

91 Comments

Are we all millionaires in NZ? Recently I have looked at any new builds which might be available and they are all in the asking price of more than a million NZD. Is this the new reality? Every house in NZ will be soon in excess of 1 million dollars?

How much yearly income is needed between a couple to afford it?

Can this happen? Has this happened overseas and what's been the impact?

To all who claim housing is over priced I say, "Clearly you've never built a house"

If building is over priced, then those figures spill over onto the existing stock. And this is only part of the story.

"But that place has a bedroom less than us, so we're worth more"

"But that place is on 400sqm of land and we have 650sqm"

"But that place is 90 minutes from the CBD and we're only 75 minutes!"

It really is a race to the bottom isn't it. What happened to this country. Even in the early-mid 2000s we still kind of had a chance at righting the ship, but since then we've just been decided to abandon all hope that someone can work a solid day of work and make enough to get by, and just tell them they should have been working harder, no matter what they do.

I think around 2013/2015 was our time to get the policy right to prevent being where we are now...we didn't crash after the GFC but had the opportunity to allow prices to grow inline with inflation...but we haven't done that...since then house prices have been going up and massively outstripping inflation since that point...and house prices can't do that forever...eventually the debt needs to be paid via wages and wages haven't been rising faster than inflation...its basic math. At some point the chickens come home to roost.

50 year mortgages anybody?

I hear Japan does 100 year mortgages. Buy Bitcoin.

A little of Yeah, but Nah.

"Through the use of simulation, the conclusion is reached that the 100-year mortgage has failed to increase the affordability of homes. Instead, affluent homeowners are more likely to employ long-term mortgages as an estate-planning tool to reduce inheritance taxes."

https://www.sciencedirect.com/science/article/abs/pii/1061951895900047

I read it as the Japan 100 year mortgage was to get around taxes... which does lead me to ponder, if (and when) politico's decide to institute wealth / inheritance taxes - how quickly would our local NZ accountants and banks suggest 100 year mortgages as well as a workaround (just like Utes for Hairdresser's) ;-)

I'd say there were some flashpoints - the mid-2000s Income Tax Act rewrites that didn't revamp the tax system that was already creaking (Labour found a new sense of urgency around this opposition with the CGT thing), not laying down better framework for finance schemes that were underwriting residential development that tipped over during the GFC and not just saying "screw it" and coming up with a plan to actually deal with the leaky building crisis or even just declaring remediation to be repairs and maintenance for tax purposes and saving everyone a decade of pointless arguing and life-ruining uncertainty.

When you look at the decisions we did/didn't make around these moments, it's no surprises we've ended up where we are today. And we're still making the same mistakes - pretending jacking up a top personal rate counts as tax reform and a pathological inability to build quality medium to high density housing and connect it to infrastructure. At some point it's just going to come to a shuddering halt.

When you have been overseas a long time and come back you notice that the received wisdom that people use in this country sticks out like a sore thumb.

It's challenging to differentiate it from brain damage at times.

What happened to this country

What happened is .....Jacinda and Orr's dream of wiping out FHB is happening......and many were blaming John Key.

Queen with smile took average Kiwi for a ride......and now wondering if it was a Smirk........

By the time you add in extortionate Consent charges, original subdivision fees and charges, over priced civil works measures, increased geotek engineering requirements, double glazing and insulation, building to healthy homes standards, green measures such as water retention tanks and pumps as well as solar heating, lawyers costs, labour and materials increases.

Now you would argue many of those are necessary but they all add to the cost if a build.

Depends on the type of house you are building. It isn't that expensive to build a standard house. The high cost is the land which has doubled in places since covid. Plus now there has been massive house building cost inflation because they can now make bigger margins

We are seeing the impact. Homelessness, crowded slum like dwellings, violent crime, child poverty, social unrest, mental health issues, failing infrastructure, 8 hour wait at A&E, water quality crashing, polluted harbours, rivers and lakes....and on it goes.

One would think a rock star economy would have all these issues sorted out whilst the knight ruled. Nope. We are maxed out and have little ability to maintain the crumbling assets we have, let alone improve on them.

I would have thought that the mob who have actually been in power for the last four years might have done something about them too, but here we are.

They were too busy calling people doom, gloom, merchants who could see the consequences of the actions/lack of actions to prevent being where we find ourselves now.

Agreed, crosses party lines for sure.

However the knight did have 9 years of strong public support (for most of it) that would have enabled him to progress some of these issues. Instead his ego became fixated with being mr cool and he then knighted himself. Shallow man.

C'mon Bro! Lazer Eyed Kiwi Flag got my vote ;-)

https://nzhistory.govt.nz/media/photo/fire-lazar

Living beyond our means.

Rastus not to forget more violence on street.......

Thank Jacinda....

.

I'm not giving National a free pass but everyone seems to forget that during their 3 terms they had to contend with a global financial meltdown, earthquakes that levelled our second biggest city and then a massive earthquake that cut the east coast of the south island in half! These three things cost a truckload of money to fix! And they started with the piggy bank empty after Clarke and Cullen spent the lot. Cullen even publicly bragged about it! The current rabble have thrown money around like there is know tomorrow during Covid - but they didn't need too!!! Mostly spent in the wrong places with very little pay back. Muppets!!

Imagine having somebody in charge of the balancing the state finances that can't even balance their own calorie intake.

Yet here we are...

Gerry Brownlee isn't in government now.

Sovereign debt skyrocketed under Key, which you justify be saying his government had to deal with natural disasters. You claim this government is spending money like there’s tomorrow and that they didn’t need to. But if you look overseas at countries that didn’t take measures similar to this government, their economies haven’t done as well as ours. So the fact that the economy is doing well suggests you are wrong.

Is the economy doing well? The people who sell houses to each other are doing well. The real estate agents and banks are doing well. The people who are facing inflation of living costs likely in the double-digits are being told by employers they are unlikely to get a payrise of over 3% if they get one at all.

This is not 'an economy doing well'. This is the economy that we had in 2008 when Michael Cullen's response to "What does he have to say to Kiwis who can earn better money, pay less tax and get more affordable housing in Australia?" was 'they should move there'.

"The economy is doing well" is 2021's "I'm alright Jack".

More Blah Blah

Yes, Key borrowed. However NZ came through the GFC relatively unscathed. Net public debt was still low. Most tax cuts end up back in the govt coffers anyway. During this covid crisis some prudent govt spending was certainly needed. However they have printed and spent like drunken sailors! Apparently you think forking over 5 million to VanAsh and a billion to Maori (for what exactly?) was money well spent? This is but two of a very long list of wasteful unnecessary spending by Muppetsville!

> And they started with the piggy bank empty after Clarke and Cullen spent the lot

Oh, you mean they started with net 0 government debt (when including ACC and Superannuation fund balance) because Helen Clark ran 9 years of surplusses and paid down debt each year?

The same "empty piggy bank" that in 2009 after the election Bill English said "this is the rainy day the government has been saving for"?

Just imagine how much worse the austerity would have been after the GFC if Brash had won in 2005 and doled out the massive tax cuts he was promising.

Imagine how much better the country would have been if Labour had actually built infrastructure during those years. Yes, the debt headroom was handy when we had an extreme run of natural disasters, but let's not pretend that getting state debt down to record lows wasn't its own kind of austerity.

Bonus points for also charging 39% in the dollar over $60K and ignoring the increase in personal debt being taken on because house prices were rising faster than they did under the bulk of National's term.

.

It didn't cost the Government a truckload of money to fix CHCH. In 2015 the RBNZ estimated the total cost to be $40b (including $7b for infrastructure). Insurers had already paid out $26b by September 2015. Yet National borrowed $60 billion even after the GST increase??? What for, tax cuts?

Refer Page 3 and page 5 of the following.

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Bulleti…

"What for, tax cuts?" Probably other stuff not related to Christchurch? Just a guess. The government does have an obligation to build infrastructure in other bits of the country too, and a bunch of that went on the back-burner post Chch. Just picking one thing you're ideologically opposed is an attractive shortcut but implies the government made binary choices between these two things, which is absurd.

They borrowed for tax cuts. It's pretty obvious.

Whether that's a good thing to do, at that time, is a separate question. In my view it wasn't.

Exactly. You have people saying "oh but but they had insurance funded natural disasters and a North Atlantic Financial Crisis to deal with", surely this is a good reason to NOT cut taxes???? 3% of that $60 billion went to bailing out investors who took a risk no risk in a Timaru based finance company.

Believe it or not, Marx had some ideas about this. He was writing at a time when Europe was economically dominated by land-owners; a time similar to our own, when whether or not you possessed property determined your station in life. However, as we see now, there comes a point where the cost of the property cannot be recouped by what people can afford to pay in rent, and is unprofitable. When this applies not just to land but to the application of capital in general (investing in plant, etc) it's a crisis of capital. Nothing profitable left to invest in.

How does it end? When there's a war or a revolution that destroys a lot of existing wealth and allows social mobility.

See Piketty's "Capital in the 21st Century" for examples. You don't have to be a communist to think Marx's analysis was onto something.

I bought my new build in Te Kauwhata last April. $240k for the section, $416k for the house build (4 bed, 2 bath).

Right now the section 2 down from me has come back on the market for $489k (and it is a back section while mine is a corner section), and the builders reckon at least $600k to build a house the same as mine this year.

So around $450k more for the same thing, year on year, how about that for moving goal posts?

Depends, is it being marketed as 'Auckland City Fringe'?

None of it is an accident. It's all been engineered by the crooks at the RBNZ.

They've added years if not decades of debt slavery to the housing have-not's just to increase the paper-wealth of the have's.

They should be in prison.

Yes, earlier in the year.. I stated I believed the 'average-NZ-house-price' could reach $1,000,000 by years end.

Austrian Economists Define 'inflation' as; "an increase in the quantity of money and credit". Holding this to be true, prices will increase as the money/credit supply increases.

I was a proponent of the government's proposed 'interest deductibility changes' and 'infrastructure development funding'. Unfortunately these changes would only be effective in "tilting the market in favor of FHB" in a declining market, otherwise such changes hurt both FHB and renters.

The announcement of the Auckland Cycle Bridge is just another illustration of misallocation of infrastructure spending, in an environment were companies [especially construction] are claiming worker shortages.

The NZ Banking System is still happily providing finance for record size mortgages, therefore prices can/will increase. It's 100% cliche to bring it up, yet here it is.. if inflation can cause bread to cost a wheelbarrow full of currency, All houses in NZ could some day be worth over 1 Million - if the NZD is still around.

NZ could be at the beginning of Stagflation, but we would need to see a steady-upward-trend in unemployment and hyper/high-inflation continue expanding from the housing sector into basic consumer goods.

I was a proponent of the government's proposed 'interest deductibility changes' and 'infrastructure development funding'. Unfortunately these changes would only be effective in "tilting the market in favor of FHB" in a declining market, otherwise such changes hurt both FHB and renters.

Sorry, but you're going to have to explain how removal of interest deductability for landlords hurts FHB in any market, cos I just can't see how you came to that conclusion.

My thinking was if 'interest deductibility' is introduced and house prices keep climbing, there is no added financial gain for FHBs, or increased ability to purchase.

FHBs get potentially 'hurt' because nobody is forced to sell. If prices keep going up, anybody forced to sell.. well, they'll likely sell to an investor - for a profit [higher price]. This would therefore increase rents due to the new investor's (likely) higher costs involved in servicing their mortgage.

Unless a FHB has free accommodation, they are likely 'hurt' through increasing rents, decreasing living standards and less ability to save.

A large decline in house prices would benefit FHBs. A small decline could increase rents if investors give up on short-term-capital-gains and increase rents to reflect their 'true costs' [???] and/or investors start paying down principle.

That's my thinking anyway.

Yeah, cos investors wouldn't jack rents as fast as they could anyway...

It's an effective policy to 'tilt' the market towards FHBs in a declining market. Otherwise it's an aberrant use of taxation laws at best.

If the goal were to reduce house prices, knocking interest only loans on the head would be a better starting point.

Governments and Kings make laws, they pick winners and losers.. it's a story as old as mankind. Home owners/investors are a favored class atm, it might not always be so. Though the ownership of land has often been a distinction between free citizens and slaves.. which is grim to think about I suppose.

Best to make work your best friend.

Nothing to do with a declining market, it makes the economics of owning an investment property much worse in any market.

. [duplicate deleted]

Lol. In Auckland it now seems to be quickly getting close to being a million dollars for just the build (not including the section).

Don't know of any places overseas this retarded. New Zealand is in a league of its own.

Immigration.

Politicians are getting smarter in fooling the electorate.

So would what that make inflation at the consumer level instead of the jiggery pokery Stats measured inflation? 20%?

Exactly - and interest rates should be set accordingly.

Yes. We need to stop referring to the CPI measure as "inflation." Why? Because the price level as measured by the CPI doesn't measure the "real inflation": the expansion of the money supply. It wouldn't surprise me if many of the politicians and bureaucrats didn't understand this. The bank economists 'should' understand but they can't talk about as it creates negative perceptions of their employer's involvement in the charade and their privileged position in society.

Stop calling it inflation and start calling it "wage shrinkage". At least it's honest.

Being more correct/honest is to call it tax. That's what it is.

Theft is more accurate

The big increases to money supply are mainly the result of massive household borrowing for mortgages. The injection of credit money from the banks has driven hugely inflated asset prices but the impact on the prices of other goods and services has been minor. Inflation of goods and services is due to supply chain disruption - it will be transitory as wages aren't going anywhere.

The big increases to money supply are mainly the result of massive household borrowing for mortgages.

Yes. Even the BoE Guv admitted this (after he had moved on). It's one of the primary channels for money to enter the "system." Now, I know that this is how the banking system works, but essentially if you're just bidding up prices of existing stock, there is marginal benefit to the economy, except for the wealth effect. At the same time, you're devaluing the price of labor. It's moronic.

If you look at money supply (say M2) and look at the year to year % growth, a rough average is 8-10% over the last 3 decades. Way higher than what is reported in the CPI.

I think the definition of 'inflation' should be considered/clarified before giving this article much weighting.

https://www.forbes.com/sites/johntharvey/2011/05/14/money-growth-does-no...

A thoroughly debunked theoretical position written in 2011.

Believe

Goes with religion

An up and down in inflation with a 1 year time frame is too short to make drastic changes to interest rates- probably no action is needed unless inflation is sustainable for 18 months or longer.

the reason they see inflation dropping back is because of the OCR increases up to 1.75% by next Nov.

The ANZ is not making any assumptions for inflation based on the RBNZ doing nothing

"In terms of why they think inflation will be brought back down again, Robinson and Workman say the anticipated OCR hikes "will be very effective at taking some of the wind out of the economy’s sails""

Damn, you should have let the RBNZ know when the China virus appeared a year ago. No need to have done the drastic and reckless things they did. Their cure is hundred times worse than the disease.

Is 12 months transitory / temperory by definition.

By saying 12 months ..easily push the situation.......

What if it shoots above 4.2%

Any reason the RBNZ won't just leave policy settings as they are, call the inflation "temporary" and "pent up" because inflation has been below target for so long? I can't see why they wouldn't, we have an enormous debt pile asking to be inflated away... as long as wages also move up with inflation, it might not hurt us having a bit.

If house prices stay the same then we can start wage inflation shrinking the cost of housing. Ha! Who am I kidding!

Housing unaffordability. It's all Govt. policy:

Clark Govt: Bad

Key Govt.: Worse

Ardern Govt: Worst

It’s just neoliberalism at work.

Nothing neoliberal about the artificial scarcity of land we have had since 1991

I think this rise in house prices and rising inflation will result in home buyers priced out of the market. Then who will buy all the houses that these builders are building and pricing in excess of million dollars each?

I might be very very wrong but for how long this crazy game will be played? Do we all get paid hundreds of thousands of dollars each year in salaries. We are not all Members of Parliament or Council members or consulting doctors.

My guess is that something is not right in this equation of housing in NZ right now. But i could be very wrong too and my panic is not real.

There's a whole lot of stuff not right. When you can buy a 300m2 brand new house nearby Melbourne for 900k including land and the same thing will cost you around double the same distance from Auckland/Wellington...

The market for already built houses was broken quite a few years back. There was hope that new housing would fill the gap, so the powers that be have ensured that is broken as well.

Surely housing in NZ is now a bubble? Property bubbles aren't new, they occurred in other countries prior to the GFC. Why do people in NZ think that it won't pop? Or do they think the government will bail all these people who overpaid out? Pretty sure the RB Gov warned house buyers to not get sucked in by these low interest rates.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

The banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

Sorry Pathos, could you repeat that? Missed it the first thirty times I'm afraid.

I think they said that the banking industry's measurements of inflation, along with those of government, are gaslighting.

To give credence to them is denying the reality of what you see with your own eyes.

Well why didn't he bloody say that then?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.