By Gareth Vaughan

Whilst comments by Governor Graeme Wheeler and his deputy Grant Spencer on debt-to-income ratios rightly stole the headlines when the Reserve Bank issued its Financial Stability Report, there were plenty of other nuggets buried within the bi-annual report.

They took the form of both comments and charts. I've detailed some of the key ones below focusing on current and emerging trends.

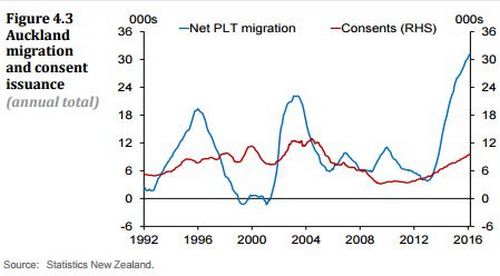

Firstly, figure 4.3 below gives a good indication of the extent to which demand for houses is outstripping supply in Auckland. As the Reserve Bank said; "The shortfall of available housing stock is expected to increase this year as population growth outstrips the supply of new housing. Net migration into Auckland remains strong, with more than 30,000 migrants moving to the city in the year to March (figure 4.3). Although building consents have also risen, to 9,600 annually, the supply of new housing is insufficient to match the increase in demand arising from migration and natural population growth."

Figure 4.3 could have been entitled 'population growth exploding, consent issuance crawling.'

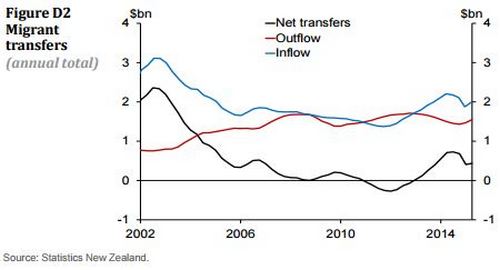

The Reserve Bank also charted the impact of record high net inward migration, with more than 67,000 more people moving to NZ than leaving in the March year, on the amount of money brought into the country. It noted Statistics NZ estimates over the last year, migrants brought about $500 million into NZ (figure D2 below).

"This estimate, however, may understate the amount of funds that migrants bring to New Zealand. Survey data indicate that around one third of migrants have assets of more than $100,000, some of which will remain offshore for some period as migrants typically shift their assets to New Zealand gradually. Therefore, we expect the measured value of migrant transfers to increase over time, particularly since the strength in net migration is likely to persist, adding to the New Zealand deposit base," the Reserve Bank said.

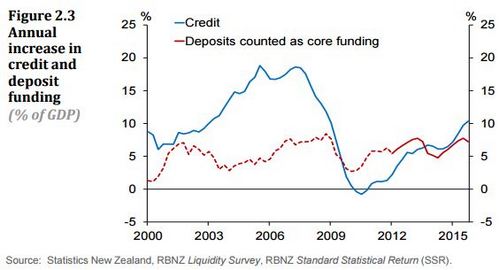

Next up, we have the Reserve Bank predicting that banks may have to rely more on alternatives funding sources to deposits than they have over recent years. This, the central bank notes, comes as lending (credit) growth outstrips deposit growth.

"Over the past 18 months, credit growth has accelerated across the household, agriculture, and business sectors, with aggregate credit growth now outpacing deposit growth. This may induce banks to compete more aggressively for retail deposits, or to increase their reliance on long-term wholesale funding, either of which could place upward pressure on bank funding costs. Higher funding costs would keep lending rates up relative to the OCR and short-term wholesale rates," the Reserve Bank says.

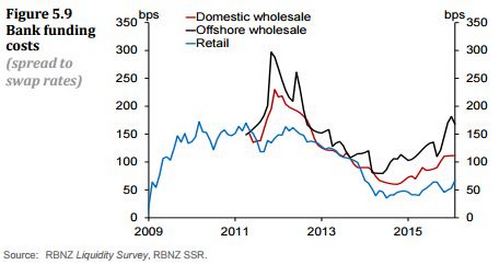

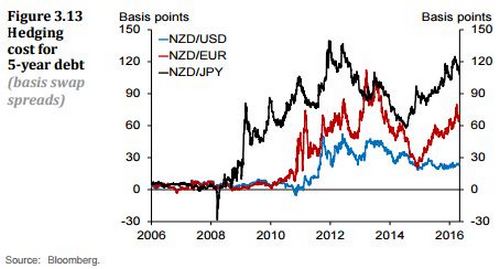

Elsewhere the Reserve Bank notes banks borrowing wholesale money overseas have seen funding costs rise by about 50 basis points relative to domestic swap rates this year. This increase is attributed to an increase in foreign currency bond spreads and rising costs of hedging exposures into the NZ dollar.

With lending growing faster than deposit growth, the Reserve Bank points out the currently very strong sector core funding ratio, running at about 86% versus the required minimum of 75%, may drop.

"Alternatively, banks may choose to protect their core funding ratios by issuing long-term wholesale funding to fund new lending and to replace long-term funding as it approaches maturity. It is estimated that locally incorporated banks will need to issue around $40 billion of long-term wholesale funding in the next three years to maintain core funding ratios if lending and deposit growth persist at current rates."

In what would be good news for long suffering savers, the Reserve Bank suggests banks could also maintain their current core funding ratios by competing more aggressively for deposit funding, or perhaps by reducing their rate of lending growth.

Dairy sector under the spotlight

Naturally the highly stressed dairy sector is well covered in the Financial Stability Report, with the Reserve Bank saying bank lending to the sector rose more than 9% in the March year as farmers borrowed to meet working capital requirements.

"In March, Fonterra cut its forecast payout for the 2015-16 season to $4.30 per kilogram of milksolids, including dividends. This is well below the estimated break-even payout of $5.25 for the average farm in the current season. Given the outlook for global supply and demand, the effective payout may remain below break even into next season, resulting in a third consecutive season of negative cash flow for many farms," the Reserve Bank said.

Farm values also get a good look in with the Reserve Bank outlining scenarios where farm prices could fall anywhere from 19% to 63%.

"If banks begin to take a more pessimistic view of the sector, they may force a larger number of troubled farms to be sold, which could create a negative feedback loop by reinforcing their pessimistic view. For example, in the most severe scenario in the recent Reserve Bank stress test of bank dairy portfolios banks reported that they expected to resolve around 25% of dairy loans through some form of forced sale procedure. Significant numbers of forced sales would place further downward pressure on farm values, which have fallen 13% in the last year. This is particularly the case as farm sale volumes are typically low, and demand for farms is likely to be weak due to poor farm incomes. In turn, lower farm collateral values would increase bank losses on problem dairy loans," the Reserve Bank says.

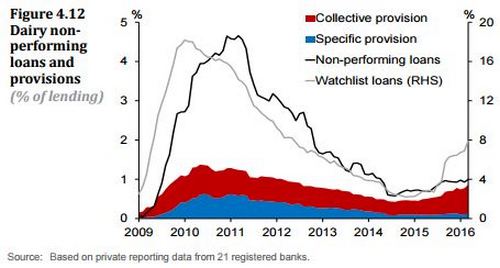

The prudential regulator also suggests rural lenders ought to be upping their provisioning against dairy loans.

"Internal bank metrics suggest that banks are now monitoring a larger number of dairy loans than those classified as non-performing or watchlist loans. Banks should be prepared to increase their provisioning against loans to the dairy sector to ensure that they are able to absorb potential losses. On the basis of recent Reserve Bank stress tests, it is likely that losses for the banking system would be manageable, even under a severe stress scenario for the dairy sector."

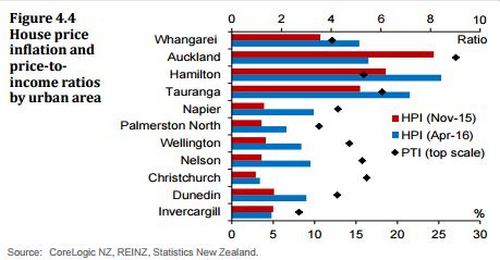

Whilst we've covered off housing and the potential for the introduction of a debt-to-income ratio macro-prudential tool elsewhere, I couldn't resist including a couple of charts on the housing situation. Figure 4.4 below shows how far Auckland's price-to-income ratio is ahead of the rest of the country.

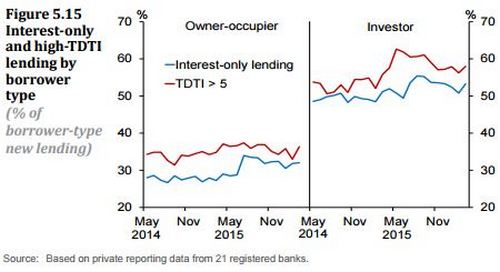

Meanwhile, the Reserve Bank says it expects to begin regularly publishing data on interest only mortgage lending around June. It provided figure 5.15 below comparing interest only lending and high total debt-to-income lending to owner-occupiers and investors.

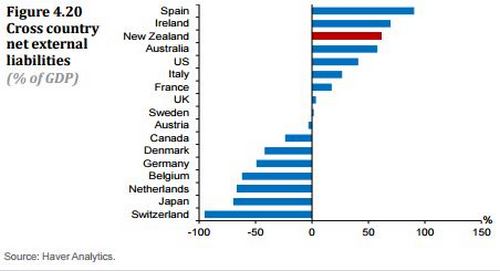

Finally, although it says the risks associated with NZ's net external liabilities are falling, the Reserve Bank included figure 4.20 below which shows us not looking very flash against a range of other countries. The largest chunk of our net external debt is, of course, sourced through the banking system.

*This article first appeared in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

12 Comments

Net external liabilities as a percentage of gdp doesn't look flash. It appears we are in with a good crowd Ireland and Spain. We know what happened with those two.

That combined with

-having the highest house prices relative to incomes in the world

- consumer debt rising at 8% p.a.

- consumer debt at 216bn

- investors making up over 40% of buyers and up to 80% in some areas

- house price inflation in Auckland at 15% yet wages moving by only 2%

- house price to income in Auckland (household) 10 to 1 approx.

- LINZ survey indicated nz citizens made up only 37% of buyers. (Students and temporary workers and not permanent residents). In SIngapore only Permanent Residents and Citizens do not need to pay the stamp duty on property. Not sure why we don't classify temporary workers and students as foreigners also ?

Not sure why they have not implemented the loan to income ratios already aside from the fact the National government are a "do nothing government".

We have an ex-banker running the show trading votes against the future of young kiwis.

Surely all those factors indicate we have passed the point of just "waiting to see what will happen". How many years can they use that line ?.

They have zero interest in helping first time buyers otherwise they would have done what uk and Australia did.

Stamp duty on investors

Loan to income ratios on investors

The young generation will be the ones that suffer. When those out of university and schools are forced to leave the country to countries with higher salaries in order to save their deposits. Lots wont bother coming back. WHy would you when most of your pay will be going towards mortgage payments or rent.

50% of rentals have government subsidies so the tax payers will be fitting the bill in the future all so some investors (local & foreign & foreign students & foreign temp workers) can make some quick money.

Absolute Disgrace.

#MakeourHousesourhomesagain

dp

With lending growing faster than deposit growth, the Reserve Bank points out the currently very strong sector core funding ratio, running at about 86% versus the required minimum of 75%, may drop.

"Alternatively, banks may choose to protect their core funding ratios by issuing long-term wholesale funding to fund new lending and to replace long-term funding as it approaches maturity. It is estimated that locally incorporated banks will need to issue around $40 billion of long-term wholesale funding in the next three years to maintain core funding ratios if lending and deposit growth persist at current rates."

Possibly, maybe?

In reality funding rose $30.079 billion from March 2015 to March 2016. $20.327 billion of which was raised in the O/N market and $9.348 billion out to, but less than one year. View RBNZ L3 table

In what would be good news for long suffering savers, the Reserve Bank suggests banks could also maintain their current core funding ratios by competing more aggressively for deposit funding, or perhaps by reducing their rate of lending growth.

Yeah right. As it stands ANZ claimed the cost of foreign wholesale funding (presumably rolled) causes them to withhold OCR cuts to debtors, but the absolute increase in short term funding, which is totally dependent on domestically calculated bank bill/ swap rates, savages savers with no end in sight if we are to believe this type of hyperbole - BT Investment Management predicts the Reserve Bank of Australia will cut its cash rate to 1 percent and could even take the benchmark below zero as inflation and economic growth disappoint. Read more

Incredible negative rates. Are we at the stage that the Reserve Bank & Government are perhaps too scared to act as they don't want to kick off a housing crash ?

We at the too big to fail stage? Would explain their lack of action.

Govt/RB want house prices to keep moving up so people feel wealthier and thus spend more in the economy thus help create inflation...

It's worse than that - there is no developed economic understanding of what the consequences of low interest rates entail.

Chairman Alan Greenspan was blunt in his summation of the prospect, for once (likely because it was private) admitting that what lay ahead of them below 1% was not well understood. He had good reason to be apprehensive given the circumstances of that day:

One is that I don’t think we know enough about how the private financial system works under these conditions. It’s really quite important to make a judgment as to whether, in fact, yield spreads off riskless instruments—which is what we have essentially been talking about—are independent of the level of the riskless rates themselves. The answer, I’m certain, is that they are not independent. But how their dependency functions and how those spreads behaved in earlier periods is something I think we’ll need to know more about. The reason is that I don’t believe, as I said before, that we can construct an effective preemption strategy. Well, we can construct a strategy, but I’m fearful that it would not be very useful.

Greenspan raised this point in response to Dallas Fed President Robert McTeer’s report that banks and businesses in his district were resisting the Fed’s moves before ever getting to 1%. Some of that was associated with what the Committee and Greenspan called uncertainty, but in truth Greenspan (as in the quote above) was not entirely unsympathetic to what “ultra-low” might mean as potentially very different than more normal monetary operations – with good reason. Read more

It has taken about 80 years since Keynes figured out how to stoke the economic engine. Now the world has changed and we need to figure out how to operate "successfully" in a low interest environment with no growth. It might take another 80 years...

Too big to fail? Or too big to save? That would also explain lack of action.

Best fill the lifeboats you have and avoid panic as long as possible. Above all else, don't tell the plebeians that there aren't enough life boats. Until you're safely away, of course. Then they'll work that out for themselves.

"Too big to exist" I heard that term the other day and it makes sense. What needs to happen when we hear something described as "too big to fail" we should saw it into bits immediately to avoid a fiasco in the future.

You....have nailed it Joe.

If he put that much effort into getting a better job he would have enough for a deposit on a house. Instead he spends hours typing the same regurgitated garbage that no one of consequence thinks is remotely a good idea. I had to leave NZ to get a better paying job to buy a house in 2000! Nothing has changed ratio wise. Interest rates are now much lower. 13 -14% has dropped to 4% and won't be rising for a decade or more. Stamp duty is a vile disguising tax. Thank god its not going to be introduced. The Govt could help FTB by expanding the deposit scheme. He is barking up the wrong tree. Joe would do well to get his head around that sooner rather than later.

How many liar-loans do NZ banks have on the books, both local and foreign?

http://www.abc.net.au/news/2016-05-09/westpac-and-anz-approve-hundreds-…

How much of the Big Chinese Money is actually large local bank loans being paid down gradually as money is secreted out of China?

http://www.bloomberg.com/news/features/2015-11-02/china-s-money-exodus

http://www.cnbc.com/2016/01/29/

Should a property price collapse occur, how many students, work visa holders and Chinese-affiliated-investors will stick around to pay down hopelessly underwater loans? What impact will this have on the property market and the stability of NZ's banking system?

I'm sure that English, Wheeler and Co have asked these questions and have it all well in hand.

So, on average each new immigrant brings about $7,500 into the country (67,000 x 7,500 is about 500 mil). But a third have assets over $100k. That is not much.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.