By David Hargreaves

Our Reserve Bank is wearing the look of a central bank that's been caught with its LVRs down.

The RBNZ seemingly went into the latest six-monthly Financial Stability Report needing urgently to do something about the rampant house market - but not being in a position to immediately do so.

Given the apparent success it had enjoyed when it first introduced a 'speed limit' on high loan to value lending in 2013, the RBNZ must have thought it could give itself some breathing space through the tightening of LVR rules for Auckland investors late last year.

This hasn't worked and the central bank's now got to come up with Plan B, which is looking suspiciously like debt-to-income ratios, something the RBNZ has been coy about previously, but has obviously had on its mind for a while.

Let me be the first to admit that I thought the Auckland-centric LVR measures would work, for about a year. Therefore I sympathise with the RBNZ, which has in a sense been left to look rather helpless just at the moment.

Nevertheless though, you do wonder why a Plan B wasn't ready and waiting in the wings for if the move against Auckland investors did not work.

And if we really examine what went wrong, perhaps the nub of it is that the LVR speed limit was a measure aimed at the banks, while the Auckland LVR measure was aimed at the individual investor. I have heard it said that buying houses is as fundamental to the New Zealand psyche as sex. So, what I'm trying to say without going up some smutty garden path is that New Zealanders WILL find a way of buying houses, it's a fundamental drive, and you don't stop fundamental urges.

The banks, however, are a bit different. They are the facilitators, the enablers. But they also need a bank registration, issued courtesy of one RBNZ. If the RBNZ levels a measure against the banks that is a condition of said banks' registration, then the banks will listen.

The real achievement of the LVR speed limit policy has been getting the percentage of high LVR lending on banks' books down from 21% in 2013 to about 13% now. And lest we forget, the RBNZ's real role is to stop the banks getting stressed, not to prevent individual people doing silly things in the housing market.

So, clearly the RBNZ is now focusing on debt-to-income ratios - a measure that would target banks and how much they could lend to people borrowing high multiples of money relative to their earnings.

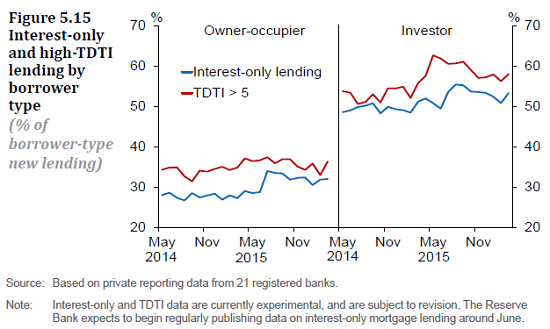

RBNZ Governor Graeme Wheeler says investors are currently accounting for about 42% of housing transactions in Auckland and 40% in the rest of the country. That is a lot. Also, the RBNZ's own figures show that about 60% of investors are borrowing more than five times their earnings, as the below chart shows.

In October 2014 Britain introduced a 'speed limit' meaning that banks couldn't do more than 15% of new mortgage lending on debt-to-income ratios of higher than 4.5. In fact many of the banks in England took it upon themselves to put a limit of 4 in place. Any such policy introduced in New Zealand could therefore be expected to have quite some impact, given the figures the RBNZ has collated.

It's worth noting that nearly two years ago the New Zealand Institute of Economic Research was saying that debt-to-income ratios were a better way to go than LVRs as a way of managing financial stability risks.

Hindsight is a glorious thing, but it is now surprising looking back that debt-to-income ratios were not included in the original macro-prudential toolkit as agreed to in a Memorandum of Understanding with Finance Minister Bill English in 2013.

Presumably, given that English's own department, Treasury, has already expressed considerable enthusiasm for debt-to-income measures, the minister is likely to agree fairly quickly to the RBNZ implementing such moves (although English is clearly not one to simply agree to what his department thinks.)

While the RBNZ's been collecting the information it needs from the big banks for some time now, it hasn't been getting the same information from the smaller banks. The indications are that this will start soon. So, if we assume that further information needs gathering yet, the assumption is that formal announcement of debt-to-income ratios could be some months off. And presumably there will need to be periods of consultation with the industry etc.

Presumably the RBNZ would want to at least announce that the ratios are coming at about the time the housing market wakes up for spring (and there's already suggestions this year that it won't even bother with the usual winter hibernation). But that suggests an announcement possibly by September-October with implementation probably not till into the New Year.

That's a long time for the RBNZ to have to wait - and goodness knows potentially how wild the house prices - and the indebtedness of Kiwis - may have got by then.

The central bank will be hoping the Government comes to the party with some sort of arresting measure in the May 26 Budget.

We will see what happens.

While I think debt-to-income ratios are a sound and logical step, I don't think they are a complete answer.

I still can't help but feel that the real way for the RBNZ to go is to keep increasing the amount of capital banks have to hold against their mortgage portfolios. The banks will scream, because this lowers their profitability, but long term the banks are going to have to live with that. The rivers of cash flowing to shareholders are going to need to be reduced to a stream.

54 Comments

Shamubeel Eaqub says LV will work as excess liquidity is the problem ; there is " no other problem driving the Auckland housing market".

http://www.radionz.co.nz/national/programmes/morningreport/audio/201800…

Taking complex issues and explaining them in clear and succinct ways helped Eaqub on his way to winning public relations company BlacklandPR's inaugural communicator of the year award.

http://www.stuff.co.nz/business/industries/78786188/Economist-Shamubeel…

But Shamubeels views are well known to journalists.

http://www.pundit.co.nz/content/shamubeel-is-right-get-x-real-about-imm…

If you ask me then Shamubeel Eaqub is an idiot. Its the same person who thinks owning a house is a basic human right. A basic human right is to live in the house and have house but owning is not basic human right. Owning is hard work right. The problem is too many people and not enough supply. Tell the council to hurry up their processes and let people build houses and see where the problem goes. We need 13000 houses every year and we get 9000.. Worked for while and now problem has caught up.. Having Loan to Income Ratio is simply going to get us kiwi out of home reach. We will be renters in our own country..

Why on earth is he continually rolled out as the "spokesman" for economic & housing matters.

He represents an unusual elite-type of high earning city dweller who can afford & chooses to rent forever.

Was he chosen by who to sway public opinion against home ownership?

I think he is being used as a counter argument against any push-back on rising immigration & foreign ownership of NZ homes.

I don't like him either. I think he is a smart ass and very self righteous. He abhors criticism of immigration and foreign investment as he clearly has a chip on his shoulder and believes it is 'xenophobic'. And his analysis, in my opinion, is often pretty shallow. He's a real self promoter, too.

Of course we will be renters in our own country... But according to your own argument, that doesn't matter, because owning a house is not a basic human right, just living in a house is... Therefore it's a non-event if NZ is owned by foreigners and we pay rent to them... Your line says it's not our right to own... So what does it matter what the RB does to stop kiwi home ownership?

Of course we will be renters in our own country Reece.. But according to your own argument, that doesn't matter, because owning a house is not a basic human right, just living in a house is... Therefore it's a non-event if NZ is owned by foreigners and we pay rent to them... Your line says it's not our right to own... So what does it matter what the RB does to stop kiwi home ownership?

"The rivers of cash flowing to shareholders are going to need to be reduced to a stream."

While bolstering the banks long-term share prices, capital ratios, viability/stability and attractiveness as a long-term investment at no cost to shareholders long-term ROI, with the impact being only on cash flow/dividends.

Reducing leverage voluntarily or by regulation seems like a no brainer.

what's been grinding my gears for a while is the issuance of capital supporting debt instruments to the retail market. its financial wizardry to support the balance sheets while paying away dividends to the Australian parent co. The best way to support a balance sheet is to keep cash on it surely, not by passing the risk onto unsuspecting Mum and Dad investors at low yields

When the next (probably Asian) financial crisis hits, there will be mayhem here over the debt- binge. No amount of loan term extension and interest capitalization will work now.

@ergophobia you are onto it . A financial meltdown in China will make Chernobyl look like and summer camp campfire

Listening to Eaqub he makes a great deal of sense. Bring in a ratio of 5 to 1 and thus reduce the availability of credit which is fueling the housing boom.

so then very few locals will be able to afford to buy in auckland, great whilst we allow overseas owners.

unless you close that door you will only make it harder for NZr's

Be careful what you wish for, by regulating locals out of the market with open borders creates and easily manipulated market, we will be all renting in our own county!

at the same time as other long overdue moves, the RBNZ should require banks to charge a higher mortgage interest rate to non owner occupiers to start putting the risk where it belongs (investors) and to provide more financial stability to NZ banks. The Australian owners of NZ banks have no difficulty in doing this in Australia - for the past year. Nor do they have difficulty in restricting mortgages given to foreign purchasers.

The problem is that the RBNZ - and more to the point the Government - wants measures that will work (stop house price growth), but not work TOO well (crash the housing market).

That is why they will end up fluffing around ineffectively. The DTI Limits will not be introduced.

the earliest estimate is 1 year, should be 1 mil average in auckland by them

This is precisely the issue. It is all too big to fail now (it will fail though).

A DTI of 5x applied across all borrowers would arguably crash the Auckland market - not because a family with a household income of $100k borrowing $500k is insane, but because most investors borrowing $500k are generating income of about $30k. It will knock most investors out.

The Government can say that it was an RBNZ decision but a crashed housing market will get them booted out of parliament just the same.

It would be really interesting if a couple of active property investors here could run a ruler across their own debt profile and income and let us know what sort of multiple they have currently.

I'm not exactly sure how you work it out. Is it total mortgages divided by gross combined household income (salary and rent)? If so mine would be 7.64.

Goodnight then Dr Smith!

Why is it "good night Dr Smith!"? No new rules have been brought in yet and it would likely only be applied to new mortgages. I doubt it would be implemented here. But even so it would be possible to have a high number but still have very high equity.

Owner occupier 1.9 (for comparison I don't have investment properties).

If someone is generating 4% return on 20% equity then that would be 1% return on debt (unusual terminology). Or a debt to income ratio of 100.

Wonder how many multiple property owners have no debt??

I know a number who bought houses and paid off the mortgages. I know commercial property owners that tend to borrow a lot less than the bank would allow them to. They are out there.

Some statistics would be interesting.

Me - I also have near $1M that I need to invest asap - and you know where I am looking....

Having said that we did it hard for a long time. No going out, crappy cars, boarders all the time, budget cell phone, lived in dunger houses, started in a crappy area. Seems many younger people don't want to 'not have a life'. They need to get over themselves.

I have 11 rental streams (commercial and residential) with the properties having a valuation of over $4 million and debt less than $500k, so my LVR is low (however LVR is only measured over the properties used as security and that is higher, as I only use some of them). My rental income (gross, so some expenses like rates and insurance are deducted, but they are recaptured from commercial tenants) is around $170k and other (investment; some non-taxable) brings this up to $200k. I also have other property assets (my own home and forest blocks and related land, that brings in income only every 30 years say), so over $6 M in property. So my debt is trivial in comparison. The DTI is less than 3.

However, the banks already heavily discount rental income (c.f. wage and salary) - IMHO the former is more reliable. They already monitor my earnings wrt what they will lend me very conservatively.

I am not sure why we need (I can understand 'want') more regulations. Most have the opposite effect of what was intended.

I would say that you are not the typical investor, nor the type of investor they are targeting.

Yes, I agree totally...except I don't think they really want to do anything at all. Just looking busy in the background but not actually doing a thing.

David Hargreaves - the RBNZ do not want house prices to decrease or even remain flat as that will cause financial stability issues...why do you think they are enforced to drop interest rates?...every action the RBNZ has undertaken has made sure there is maximum momentum to the upside while there is a severe supply side issue..........NZ'ers have over $153/4 billion in savings, total debts are what somewhere between the $400 to $500 billion mark (government, business, agriculture, housing and private) there is a lot of equity tied up in housing, many people who have paid off there mortgage have not removed the mortgage instrument from their paid up property so as to cheaply access money if they need to in the future without having to incur the mortgage instrument set-up costs, NZ'ers have many asset classes and the ability to generate income in the future.....business is mainly competitive internally in NZ but bureaucratic influences have affected our international competitiveness in many areas and their policies do nothing for value adding.

I think the RBNZ is telling porkies to the public when it waffles on about its concerns re escalating house prices and the need to intervene for financial stability purposes all the while never mentioning its real goal of fighting deflation which would see underwater mortgages if house prices declined.......I told you that they have snookered themselves and I think Iconoclast was onto this issue as well........

The NZ economy has irreversibly changed thanks to RBNZ rules, tax rules, Council rules and MMP........the whinging left have brought all the issues on themselves as they constantly looked over the fence thinking the grass was greener and demanded controls adding layer after layer of bureaucratic crap, costs and regulation........when their concepts don't work they stupidly add more of the same it is nothing more than a circle of insanity........the whinging left need to realise that if they can't get up and run their own business then they sure as hell have no right to interfere in anyone else's but interfere they do!!

NZ has a legal price rigging system when it comes to houses.......one bureaucracy creates a shortfall through the local planners, the next bureaucracy influences the price of money, the next bureaucracy influences products and design which is backed up by the first bureaucracy ensuring those obligations are met, then there is another bureaucracy which creates the who can and who can't claim costs, then there another bureaucracy that ensures the numbers needing a house rises through immigration.........but never mind you journalists want to keep encouraging tinkering at the edges........so that makes you part of the problem!

Indeed, layer upon layer of cost, added by clueless bureaucrats. $5K here, $10K there, pretty soon it adds up to Real Munny.

When one considers that the raw cost of a 600 squares chunka dirt (at hort prices of $50K/ha and allowing 1/3 loss to reserves and roads ) is $4,625 - do the math yerselves, it's near enough - and allow say $60K for getting that roaded, levelled, topsoiled and ready for Bob the Builder, then section prices of more than say $100K are a rort, pure and simple.

And if the land price is wrong, so then is the price of anything built upon it.

Legal price rigging it surely is. Welcome to trailer parks (no bureaucracy involved), the grey nomads who have sold their McMansion and live on the road, the homeless, the perpetual renters, and of course the mortgage slaves, drifting off to sleep each night with a lotta zeroes still on the tab. Sweet dreams.....and we still call it GodZone.

Last time I looked there was no hort land available in inner Auckland.

A 600m2 chunka dirt in central Auckland is going to be worth a lot more than in Pokeno. Your logic doesn't factor in the value of location!

Supply - fair enough.

But the "value of location" is planner and zone-induced gain. The Productivity Commish http://www.productivity.govt.nz/inquiry-content/2060?stage=4 noted that raw unimproved land prices several clicks either side of a MUL had a gradient of about 8-9 (counting from the purely rural side at 1, ending in the burbs at 8-9).

Planner gain. Cui bono?

the whinging left have brought all the issues on themselves

Yes, and No. the whinging left come up with a rule about something and then business interests work very hard to capitalise on said rule. A classic example would be Import Licensing in the 1930s.

Import Licensing was brought in to try and solve a real Balance of payment crisis. But ended up creating fortunes like the Todd Family fortune. Import Licensing built business empires. So blame the left if you like but the right are not blameless.

DTI ratio will never be introduced as it would effectively correct the housing market and there will be far too many people overgeared and will owe banks hundreds of thousands of dollars

thats only if you believe its only 3% of overseas buyers, it might slow it but will also give an advantage to those that dont borrow in NZ

Westpac gross yield currently 6.4%. Hardly a 'river of cash going to shareholders'.

Difficult to use the current yield to decide whether a company is 'too profitable', as the price will respond to any increase in income. If they become less profitable, the price is likely to fall and the yield could be similar, but the 'river of cash' will have dried up a little.

I agree, you can't. But as a snapshot on the day the article was posted, current yield is the relevant measure to examine the nonsense claim that shareholders are currently receiving 'rivers of cash'.

Call me crazy but I believe Auckland property prices will NOT significantly increase in the next 12 months (less than 5%) we shall see

DTI ratios, if implemented, will have a real big impact on house values, I actually think, if it is implemented, DTI will be the trigger for a serious downturn in Real Estate values (ironically exactly what DTI are aimed at avoiding)

DTI ratio will mean the end of the one family income if it hasn't already ended.

It will also mean more family members pooling together to buy.

I want to use the "F" word in utter frustration . Has Wheeler lost his marbles ?

A debt to income ratio will exclude any young Kiwi family from home ownership while the Mum is having babies and the income is halved

For goodness sake man , stop immigration while we get on top of the housing backlog .

One word for you:

Globalisation.

This does not work for nationalistic citizens.

This is already the case. We are already priced out of housing or priced out of kids or both. Childcare is so expensive that your wife working doesn't mean a whole lot in most cases anyway.

It's fine though. Who needs kiwi families when we can import them.from Asia.

I think debt to income will bring DOWN prices if set at 4.5x. NZ's banks are the fundamental enablers of this bubble. They are selling the ammunition.

But agree, you can't introduce DTI without addressing the foreign buyer issue.

I bet if National are ousted next year you'll see the housing market "soften" very rapidly.

Yeap, I'm with you on that one. The anger is hard to contain eh. We need to hit the streets next election and really put the fear in these clowns

The question around DTI is, IF and when DTI is introduced, will it be be applicable from a point in time onwards or will it be applicable for existing owners too?

I am almost certain that it will be from a point in time but nothing can be ruled out unless made official. It will have devastating effect on property market eitherways.

Wow finally some ideas that will actually make a difference. With 42% of current sales going to investors this has to be a public issue that the government can no longer ignore. I am a home owner not an investor I have no problem with this proposal. Immigration, greed and housing market tilted heavily towards investors is destroying the fabric of our society and it feels like we are losing all the things i love about this country. Lets face it houses should be to for living in not investing this has gone on far too long at the expense of the least fortunate sectors of our society and eventually my children.

This announcement should have many investors looking over their shoulder for the door.

Lets just hope this isn't more BullS#$% from this national government

Approximately 40% of the population rent their homes. So the fact that 40% of purchases are to investors should not be surprising. This is in balance. Of course, not all renters rent from private landlords and not all houses bought by 'investors' are rentals. e.g. IMHO the number sold in Auckland to overseas owners (and left vacant) is far higher than the figures released this week indicate.

its higher than 40% now as investors drive FHB out of the market (they both compete for the same housing stock) as for overseas owners that is also a lot higher then 3% and you would have to be a numpty to fall for the smokescreen this government has put up using a badly designed linz form to lump a lot of overseas buyers in as non overseas

look at Question 2

DTI should be brought in at the bottom of the market, not at the top, unless you want it to cause a bottom of the market.

Interestingly, they bring the DTI announcement out after the release of the LINZ stats, which Nick Smith and the Media have conveniently interpreted as having only 3% foreign buyer influence, which we all now is nonsense. Most foreign house buyers won't be affected by a DTI, so could have less competition, First home buyers and lower income will miss out, and foreigners getting houses cheaper.

But they believe the low foreign %, hence the DTI announcement.

However, it is only an announcement at this stage, they have never actually done anything that has made houses more affordable, so don't expect it to happen.

Surely this DTI thing wouldn't stop the most pressing demand side pressures on house prices - foreign investors, and NZ based investors?

Surely, an investor who has 5 properties and therefore has an income probably well in excess of say 150K, could then easily buy yet another 600K property if the DTI limit was 4.5:1????

Or have I got that wrong?

I'm not so sure although DTI doesn't seem to make much sense. My niece has just bought a house in Hamilton for 340K that is currently rented at $380 a week. She is buying it for her own use. Currently this will be way cheaper than renting for her. But in isolation if you wanted to buy it as an investment it would make sense. If you put down a 30% deposit of around 100k you would then need to borrow 240k. The income would be 19.7k which is 12:1. Yet it would be a cash positive investment.

The point of DTI is to avoid house prices fluctuating during the interest rate cycle.

At 8% interest (probably closer to a "normalised" rate), and including principal repayments, rates, insurance etc this may not be cash positive. And don't forget you can use your own salary as part of the DTI. It doesn't really punish any property investor until you get beyond 2 investment properties.

i have ayoung guy at work looking to buy his first house, he does not need to live in it yet (lives at home) so with the rules the way they are i have told him to rent it out until he is ready (maybe five years), he will be able to hit the mortgage a lot harder.

his DTI under that circumstance would be far greater than if he moved in with flatmates

Clearly we can't build houses fast enough and probably will never be able to with the amount of people pouring into the country. So, if we can't keep up with supply then do something about the demand!! I mean how busy and populated do you really want Ak to get!!!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.