The Reserve Bank’s (RBNZ) says the stability of the financial system as a whole is robust, despite there being pockets of vulnerabilities and a number of uncertainties ahead.

There were no surprises in the RBNZ’s biannual Financial Stability Report, released on Wednesday.

The RBNZ reiterated its focus remains on housing-related financial stability risks.

Having reimposed loan-to-value ratio (LVR) restrictions, which are now at tighter levels for both investors and owner-occupiers than pre-Covid, the RBNZ doesn’t appear to be in a rush to introduce debt serviceability restrictions.

It reiterated it will start consulting on these in late-November (the consultation was initially due to begin in October, but was pushed out due to Covid-19).

It noted implementing a debt-to-income limit could take “at least six months” following the design and calibration of the tool. Setting interest rate floors on the test interest rates that banks use in their debt serviceability assessments could be implemented sooner.

However, the RBNZ said, “We expect banks to be more cautious about high debt-to-income loans given the risks of rising interest rates and to the economic outlook.”

Indeed, BNZ last week announced it won’t lend (initially only via its broker channel) to both investors and owner-occupiers seeking debt worth more than six times their annual income.

The RBNZ recognised how the flood of support provided to the economy by both central banks and governments around the world had boosted asset prices. The question now is how the removal of this support will affect these prices.

“Should inflationary pressure prove more persistent, and inflation expectations increase, this could prompt a faster increase in interest rates,” the RBNZ said.

“Coupled with weaker growth, such a scenario could lead to declines in asset valuations and lead to a sudden tightening in financial conditions.”

The RBNZ repeated what Governor Adrian Orr said in a speech on Tuesday - that New Zealand house prices are “above what is sustainable”.

“Market momentum has been maintained at a strong level, although at a slightly slower pace in recent months,” the RBNZ said.

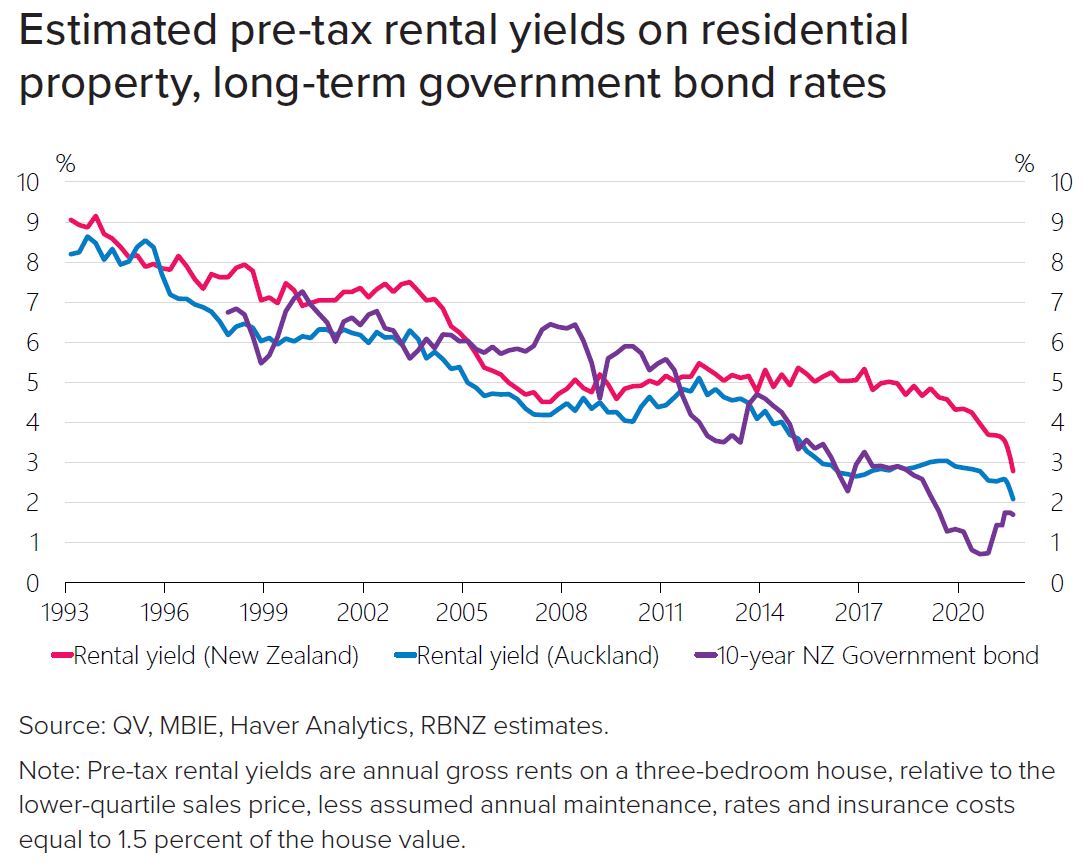

“Valuation metrics such as price-to-rent ratios highlight that prices are vulnerable to a decline as interest rates increase from their recent lows.”

However the RBNZ walked back a little from the house price projections published in its August Monetary Policy Statement, saying the “precise timing” of the house price moderation it projected for over the coming year is “uncertain”.

The RBNZ in August forecast annual house price inflation peaking at 30% in September 2021, before falling to 17% by March 2022, 5% by September 2022 and negative territory by March 2023.

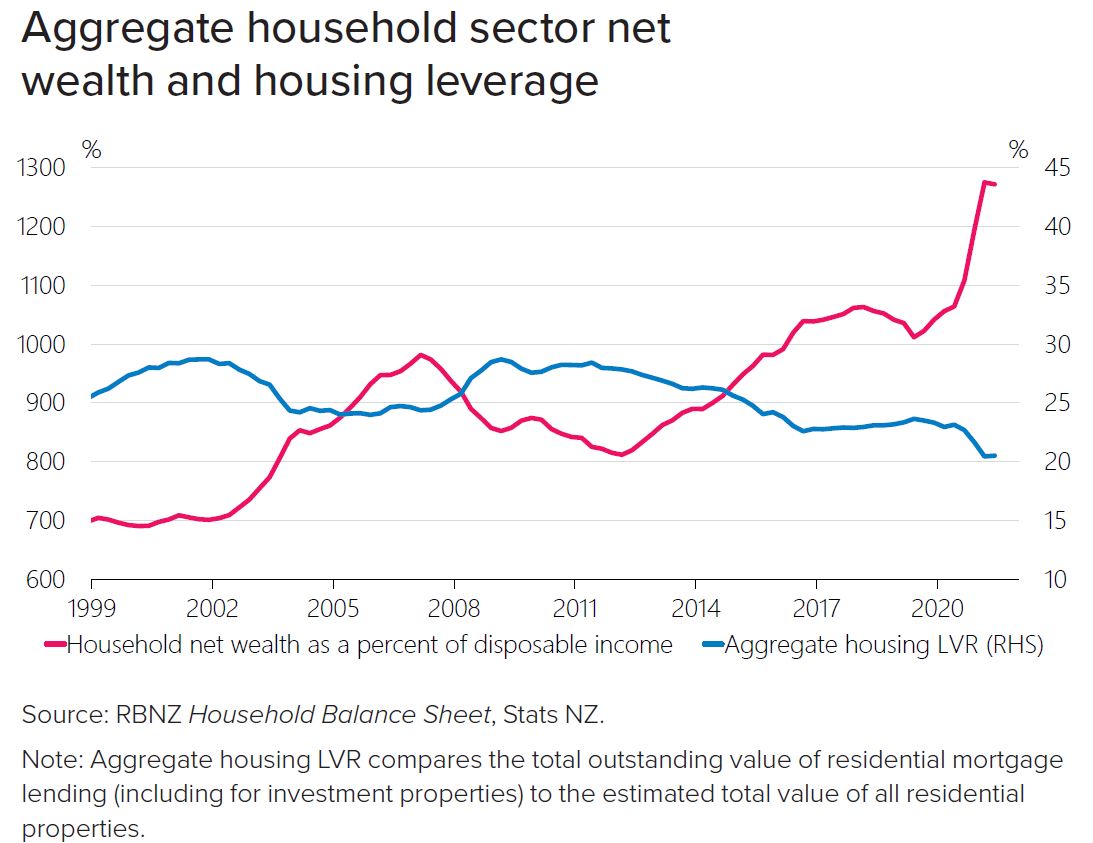

Again, the RBNZ made the point that in aggregate, households can absorb “sizeable” falls in house prices. In the 18 months to June 2021, total household net wealth rose by more than 27%. Property - mainly the land component - accounted for half of this gain.

In aggregate, household loan-to-value ratios have accordingly fallen.

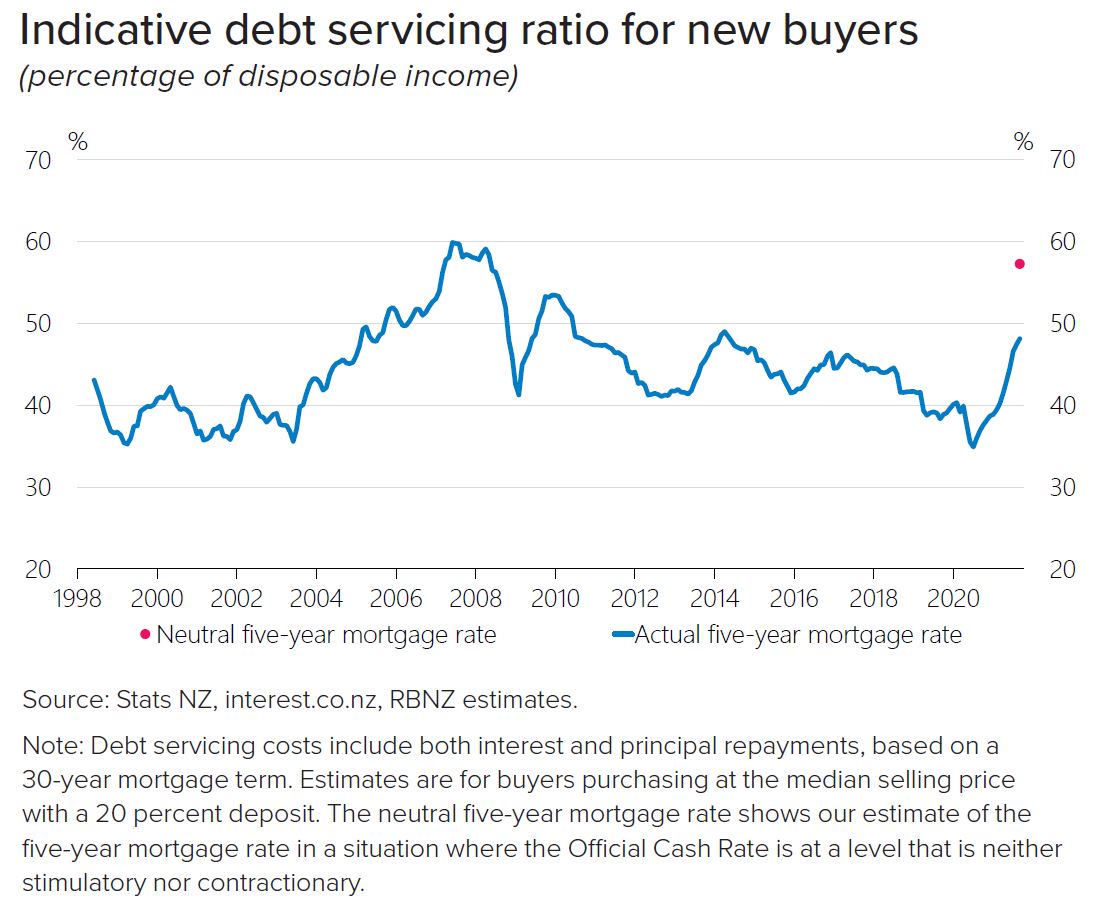

But, recent homeowners with massive mortgages are the vulnerable ones, who will feel a rise in interest rates.

79 Comments

So 'now' they are worried about first home buyers. Bit late.

Why do we pay them salaries? Interest.co common taters have been mentioning this for free for some time now.

Why is it too late now? The last 12-18 months have seen higher numbers of first home buyers than at any time since the GFC

I read KH's comment as 'too late to save those "higher numbers of first home buyers" from losing their (and their BOMAD's) equity stake and then some'.

Not to mention having their disposable income vapourised by ever increasing debt servicing costs for the foreseeable future.

I hope its only recent FHB but the cost of an average $600k is now $12,000 pa more so expect the reduction in discretionery income spending to rsult in other dominoes falling and consequences to unemployment, taxes etc, the future is looking very ugly at a time we have the most incompetent bunch of Bureacrats and Politicans in power Globally as well as NZ which may have the worst.

One reason is because younger people couldn't leave NZ for an OE etc, so it is logical that there world be more FHBs. Due to the emergency low interest rates and low number of houses being put into the market, prices have been artifically bid up by emergency factors. IMO the banks stress tests have been too low. 8 % plus should have been used and even 8%is quite low historically

This would have been great about eight years ago. It's a bit Clayton-esque now. Lives were put on hold, families deferred, people uprooted and moved to the districts because being a FHB in our main centres became impossible.

One thing to remember is that a $800k property needs to rise by 25% in order to hit a million dollars, but a 25% fall from there puts it back to $750k. Even a relatively small correction would hurt from these lofty heights.

I thought 800k - 25% would result in = $600k ? can you explain your math please? or you meant from 1M , ok then

A 25% rise from $800k is a $1M. My point is that a subsequent 25% "correction" from $1M doesn't take you back to where you started, it takes you back further than that.

So when people see a 25% YoY growth rate, and conclude that a 25% fall would therefore only take us back to the same time last year, they're not quite correct.

Sure but at the same time just 25%YoY growth now is not the same at 25% YoY growth was 12 months ago is it ? Because its now compounding. Those 4% monthly increases then are more like 5% increases now. It cuts both ways.

Indeed, which is why a "steady" 5% growth rate looks like a hockey stick in absolute terms over time. It's exponential growth, which is unsustainable, which by definition means it has to end at some point.

We might be reaching the grip on the hockey stick.

Agreed but its already gone WAY beyond what I thought was possible and its STILL going up month on month. You would think given all the data available it should be possible to calculate the limits. We must now be at the limit or very close or even actually in overshoot if interest rates go beyond 6%. There simply cannot be much gas left in the tank for the housing market now.

If investors are 'earning' hundreds of thousands of dollars (on paper anyway) - what is a 10-30K rent top up to them?

Do they even need tenants, NO~!! Selling houses back-and-forth to each other (for ever increasing prices) can go on indefinitely.. so long as the credit tap is turned on.

It's called "Painting the Tape".

Scope for a 25% rise is very limited but not for a drop so FHB even with a 20% deposit will be in negative equity but as long as they can pay the Bank its irrelevant so the hope is a drop in value is less than equity and income remains enough to pay the Bank if not the sh*t will hit the fan. I don't want to imagine what a 40% drop in values would produce.

"High house prices are a first class problem to have".

Our own Mr Orr, only a year ago. No credibility to talk on the subject.

What is it about this government and its agencies in that, everything happens faster than expected!

Not just this govt, all of them. When was the last time a govt agency bought a significant project in on time?

Someone might just go down the history being the one person to single handedly decimate the NZ economy and create a lost decade in the southern pacific.

I should still be in quick though, ya?

Before the decimation?!

Can I make a wild guess that its a PM who only lies when her mouth moves.

He wouldnt have had to worry about recent house buyers if he hadnt created the 250k price increases in the first place. Secondly, these 600k plus loans have been given to adults, not children, they should have all considered home loan rates normalising to at least 4.5% at some stage. These comments and lack of action from Orr are getting more and more ridiculous.

No NZ adult has context for this kind of housing unaffordability. Maybe the adults who created this mess over the last two decades should have considered the enormous consequences of doing it instead of filling their boots? Or are we only interested in finger-wagging when it's a chance to do it at young people?

Given to adults who, throughout their entire adult lives, had watched the government(s) and RBNZ not give a shit about what high house prices and rent were doing to them, and had no reason to believe that either body would suddenly start caring about the problem rather than mouthing platitudes?

Exactly, its hard to chastise a group of people who simply want the security and stability of their own home. Who have constantly voted for governments who have talked a big game around addressing affordability, only to find they actively make the problem worse once in power. If they have had to watch homeownership slip further out of reach each year, can you blame them for taking the plunge when they still feel they have chance?

The people who will get hit the hardest in a correction are very much the people who least deserve it.

The responsibility lies solely with policy makes and vested interests who have profiteered from the unsustainable asset prices (so both labour and National, the RBNZ, banks, media and various investor groups).

It's only a matter of time before the "blame the irresponsible FHB" game starts from those who have had their noses in the trough for decades.

Kafkaesque!!

Breaking news most 3 year rates at at or very close to 4.5% on average.

What a bunch of complete idiots. How do they do their economic forecasting.

Reading tea leaves?

Reading 6 month old newspapers?

Drunken chats over a few lunchtime chardonnays

It seems to me that we have a huge problem with our public service and a really disconnected, weird mindset and culture in Wellington. They have absolutely no accountability and appear to do pretty much what they please to the point of ignoring and manipulating our political representatives. The culture of these people is totally disconnected and dismissive of the average Kiwi who's hard slog pays their over inflated salaries.

The property market may take a bit of a hit for a short while but I cant see that the government has taken any responsible action to fix the basic problems. As soon as National are re-elected (probably next election) expect the whole property circus to kick off again.

The best plan for young Kiwis is still to get the hell out of the country.

Aye it is starting to emerge just how intransigent and arrogant our bureaucrats are as evidenced in the recent court decisions decided against the MoH. This government has taken a lot of stick as a result of MoH being incompetent and completely uncaring about it. For instance early on the directive to test all border staff was not obeyed and instead the minister was lied to, by MoH saying it was. A bureaucracy that is opinionated, self-serving and unaccountable is a threat to society and democracy itself.

Foxy, disagree that it is starting to emerge. I think it's been evident for quite a long time. But consider they are having a review into the political structure in NZ and this includes extending electoral terms to four years. I will suggest that there will remain no way to kick a government out of office once elected. So would anyone want to say to the current crowd, we think you are so good at this, you can stay longer?

I hope not. They are working on undermining democracy!

Yes agree three year terms essential to halt an awry government. Would shudder to think that 4 year terms , would likely have see this government in power until 2025. There has to be a referendum on any change proposed.

Two term governments isverycommon. So think four years will mean eight.

I used to be a proponent of the 4 year term for pragmatic reasons. Now we've seen what happens under an MMP majority government I've changed my mind. As a German colleague pointed out recently, a Westminster government with no upper House is so incredibly powerful. NZ has no upper House to review laws, and our courts can't overturn laws, just point out they breach blah blah blah. Germany on the other hand was made to have MMP so that law changes would be made through consensus with a constitutional court that could overturn non-constitutional laws.

3 year term, written constitution and a constitutional court thank you.

I'm still a proponent of a 4 year term. 3 is just too short for politicians not to be completely short sighted on decision making i.e. prioritising the wrong projects just because then there will be a ribbon to cut in an election year. I think given the current government performance it is likely that we won't see another MMP majority government for a long time and its likely we'll see the start of more influence from minority parties as they attract more votes away from labour/national

Binding citizens referenda with power of recall have the same power as a consitution and can be a faster way to control Politicians in power and are abusing it as the wording could include the lifetime disbarment to receive taxpayer $ except superannuation and would galvanise those in the circumstances or suffer the consequences - real accountability!!

Lunch is served.. Hope you like it salty!

Just print a few more billions and it will be alright for next one year. Then print few more. Then few every year and it week be alright.

Let's make everyone billionaires in this country. Isn't this what Jacinda and Orr wanted?

Just tell me when is the tax rise coming. I see they are building up that story nicely.

Tax? You still pay tax? Repeat after me, "I didn't mean to make a profit from the sale of that investment property, sir" and apply that thinking to all your supposedly non-income.

Inflation is tax.

It really is when the brackets aren't ever adjusted.

Unexpected raise of interest rates ??? Under what rock has Orr been living ???

It was so evident, to anybody who just wanted to see, that current interest rates are unsustainably low, and that a normalization of rates was bound to happen sooner rather than later.

And after enabling one of the biggest Ponzi in the history of NZ - the current housing bubble - Orr only NOW worries about FHB's ?

These blokes at the helm of the RBNZ are just a bunch of clowns. Incredible.

Agree. He is a yes man for Jacinda and Robertson. Yes mam. Yes sir.

Nothing good was achieved by yes men in this world.

I could afford a 100% drop in house prices.

Renters could also afford 100%.

50% would be just fine. Need to recognise some value.

Bring it on.

I concur

A correction in house prices has little effect on people LIVING in the house long term. It effects speculators and the 40,000 empty homes in Auckland.

It does if it pushes you into negative equity or wipes out any that you've got - there goes any hope of ever moving into a bigger house to expand a family or move for schooling reasons, etc. Once you hit negative equity you're basically trapped.

Trapped in a house you like enough to own, purchased at a price that you agreed was reasonable to pay.

Thems the breaks, at least you aren't at risk of being out on the street.

I think very few people would have agreed that the price they had to pay was 'reasonable' for a very long time. And 'liking a house enough to own' is not a very high bar when the alternative is worse.

The problem is that for a long time now, people were trapped between two terrible options - a stressful, expensive, competitive rental market where a lot of the houses are terrible quality, get no maintenance done on them, are stupidly expensive, and you could get kicked out on a landlord's whim; and stupidly expensive houses - again, where you might have to buy somewhere with a ridiculous commute, that needed work that you couldn't afford to do. Given two terrible choices, it's reasonable for people to choose the slightly less terrible. To make out that whatever the consequences of that are are all their fault because they 'chose' it ignores this crucial point.

.

As long as the payments are equal to or less than rents for an equivalent property you're fine. Provided you don't need to move towns. That's when things get gnarly.

It also affects banks, whose loans will be undercollateralised if the house ends up worth less than the mortgage on it. This won't be an acceptable situation for the bank if it becomes too common, at which point they will make sure it is very much a problem for the mortgage holder, not them.

It becomes a problem for so called depositors as well if banks are forced revalue downwards the price paid for the mortgage contract asset in the first instance. If that step is realised, what banks claimed they owed when the mortgage security was first purchased has to take a similar haircut. OBR

The reality of this situation is a complete mockery of the FSR Nov 2021 mention of the future Deposit Takers Act.(page 9 (11 of 52)):

Because banks don't take deposits and they never lend money. They are in the business of purchasing securities. When one gets a bank loan, the loan contract is a promissory note. The bank purchases that contract from the borrower. Now the bank owes the borrower money and it creates a record of the money it owes, which we call deposits - source. Same principle as central bank QE.

Demand deposits referred to by the public as “cash in bank” is recorded and reported by monetary financial institutions (MFI) in units of account by double-entry bookkeeping in a process which the MFIs call “lending ” — but which is effectively a nullity — by debiting loans receivable and crediting demand deposits.

These so created units of account are then denominated at will in dollars, pound sterling, euros, etc., depending on the terms of the documentation or underlying promissory note, or whatever is the legal document giving rise to this type of “lending,” using whatever is the name of the currency in the jurisdiction in which it takes place, but legal tender the “demand deposits” are not.

Banks do not have pre-existing funds in the form of legal tender to lend, except in miniscule amounts relative to the size of their loan portfolios.1 In other words, banks create demand deposits out of nothing, and it therefore remains a nothing. The malpractice continues because public accountants as auditors sanctify the aforementioned practice by “certifying” the banks’ financial statements, provoking credit expansion, moral hazard, asset bubbles, liquidity-stressed financial markets, bank runs, and eventually global financial crises. Link-pdf

The effects of Basle 3 requirement to mark to market is under estimated.

He uses FHB to shed crocodile tears / concern, only to screw them.

Sometimes I feel like we are living in a simulation, and the people controlling it are just having a laugh at our expense.

https://www.newshub.co.nz/home/money/2021/11/level-and-trajectory-of-ho…

What the F#@$ is he talking about and showing concern. Is he that helpless.....should resign.

Has he heard where their is a will their is a way.

I find the RBNZ's position somewhat confused. Are they concerned about financial stability or issues of equity when it comes to what type of property owner loses out more, if prices fall? Clearly they have a remit for the former - ensuring the taxpayer doesn't have to bail out the banks. However their comments seem like overreach to me, unless they can prove FHBs are a riskier borrower class than an investors per se (which is not what the rating agencies would tell you).

https://thekaka.substack.com/p/why-the-rbnz-was-more-than-a-bit?token=e…

Mr Orr stands exposed - Good of Bernard Hickey to highlight Mr Orr's lie in trying to manipulate to deflect responsibility.

Everyone, who can should and must raise / question Mr Orr's- not giving him satisfaction of feeling that he has managed to fool idiot Kiwis instead should be made to realise that he now stand exposed.

That is an exceptional piece by Hickey. Needs to be in mainstream media. At least Mike Hosking covers this in his show to highlight the ineptitude of Orr and Robertson.

I hate Ardern.

Since last two days lot of discussion and media highlight just like it was in November last year than in February / March when everything pointed towards ever growing housing ponzi but what happened....NOTHING.

Same will happen this time, in few days will be a thing of the past and Orr will be happy and ponzi will continue........

If RBNZ or NZ Gov wanted to fix this issue they could fix it easily. Just increase interest rates for starters, yea some people will lose money, tough, that's what investing is you take a risk, it'll come back and regress to the mean over time. Why are we a culture of coddling? We coddle everyone for every reason under the sun. If we try to coddle everyone and whisper didims in their ear then society in it's practical terms will crumble as we all sit around in blankets crying playing the victim game. NZ GOv and RBNZ, grow some balls and do what needs to be done, you can't please all the people all the time.

On a side note i feel the same about increasing the Wellington airport runway to allow international flights. Because Mavis down the road doesn't like it, tough, we need it as a country, do the right thing and don't let a few people hold everyone to ransom. Same with the Covid jab. People have to take personal responsibility and suck it up sometimes.

Cancel accommodation supplements and it will correct overnight. Landlords will forced to drop rents. Home owners be just fine.

This is a continuing subsidy to landlords...Not a subsidy to tenants.

Time to be bold.

Really feel like RBNZ has a PR team & spin doctors behind them guiding them through statements & phrases... so much BS designed to hit headlines that actually means nothing. Reminds me of the government.

Point to ponder. Why do RBNZ does what it does ....because Media - fourth pillar of democracy - atleast suppose to be allow RBNZ to get away by not asking counter questions and allow them to put it under carpet .....if Media wants can pursue.....

First this little scare, then next week "RBNZ seeks to lock-in windfall gains for property owners".

The f$%king RBNZ idiots are now up to blaming everyone else for the mess they created. Classic bureaucratic blame shifting from small people with ego's that far exceed their mental capacity. It's like the collective bunch of economist idiots now pretend they have nothing to do with the market and their actions couldn't possibly have any effect.

Again, watch for the retirement announcement from Orr, that will be when the s#%t is really about to hit the fan.

"It noted implementing a debt-to-income limit could take “at least six months” following the design and calibration of the tool. Setting interest rate floors on the test interest rates that banks use in their debt serviceability assessments could be implemented sooner."

Why six months.

Another point to note, government gave them tool in August so......delaying tactics at best.

Set rents at $3 per sq meter so 200 sq metre house $600 a week

Same $3 for Auckland central vs Porirua? Queenstown vs Mangere? Rent controls = socialist heaven.

This is so stupid... really mind numbingly daft. The fact of the matter is that none of the powers that be, and have been, are remotely interested in solving the problem. Orr, Arden, English, Key and beyond. We know this because it could have been solved in a day by any of half a dozen solutions, and nothing has been done. They are all interested in making statements that they can look back on and say I told you so..

We need to go the Iceland route. When politicians and reserve bank employees abdicate their responsibilities resulting in the complete mess that this going to become, the public led by the media need to hold them to account, they should end up in jail. It should also be remembered that the NZ media has also run alongside the powers that be slapping backs and buying property, while actively shutting down any contrarian views. Lock them up too.

The government seem to be doing what they like under some health policy can make people take experimental drugs or lose job can’t go out into society if they can do that putting regulations on housing will be easy. Once citizens give freedoms away how can you fight against next project they have in store.

Check this out - Pfizer falsified data on the spike protein (Experimental non vaccine) reported in British medical Journal but not in UK press?? I smell global Nuremberg 2 trials and an excess of demand over supply for prison accomodation.

https://www.zerohedge.com/covid-19/falsified-data-pfizer-vaccine-trial-…

I think they won't raise rates .. this is RBNZ telegraphing this to the public?

LOL

RBNZ is requiring the Aussie banks to have more equity in NZ.

How about a petition to underline the populations desire to not bail out the banks in a reset. Kiwi bank sould also offer a depositor guarantee. Deposits would flood into Kiwibank if the Aussie banks dont match that offer.

Yes, it's like depositing in a bank is becoming an equity holder with no dividend.

Another option - take deposits out of the bank and into crypto.

I am probably one of the few commenters here that doesn't agree on what the problem is. For the main most people here believe that Adrian Orr is a bad person who has over extended a credit bubble that has put the price of houses out of the reach of first home buyers.

But I ask myself what if Adrian Orr is not a bad person but a conscientious public servant doing the best he can with the tools he is given?

How much of the lending done by banks for housing actually ended up being used by business owners to support their businesses through the Covid period?

For Mr Orr to ask the banks to lend to businesses is laughable. They didn't lend to business when they should have and they won't do it now. They will lend for the purpose of financing property or to established businesses with collateral. Collateral which generally involves property.

We are at the point where property is the transmission mechanism for the finance of business. Very little finance will be extended without property being used in some form as collateral. The past finance transmission mechanism of loans from banks to businesses based on a business plan, a past record of success etc seems to be broken.

In a low growth world, just because finance rates are low doesn't mean finance is available. Finance at low rates is available with high quality collateral and with many strings attached, or finance is available at very high rates on a precarious basis.

If property is one of the few assets available that will retain it's value relative to other assets and is one of the few assets that will ensure a loan at a realistic interest rate then the value of property in relation to other assets will rise.

I find the Alhambra Investments guy Jeffrey Snider fascinating. His main idea seems to be that QE is irrelevant and doesn't actually work. What works is how large and liquid the worldwide pool of Eurodollars available is and how whether people worldwide are buying Eurodollars or having to sell assets that are convertable to Eurodollars.

When the interest rate of Eurodollars is low it means that they are in demand and that people are willing to accept a low rate of interest in order to obtain Eurodollars because they a recognised medium of exchange and a good store of value.

What interests me is the idea that QE from the Fed does not mean that there are suddenly a lot of Eurodollars around available for foreigners to buy. Why not? I far as I can figure out it is because US banks require good collateral to extend eurodollar loans to foreigners and if that collateral isn't available then the loan doesn't happen.

So then if foreigners need to pay interest on eurodollar loans (in eurodollars) they have to sell assets that people will pay eurodollars for.

So the situation now is that growth in China has slowed, growth in Germany has slowed, export orders to these countries have fallen and the eurodollar rate is low meaning credit is actually tight in the world.

Which is the opposite to what I would have expected with high baby boomer and Asian savings sloshing around the world. I guess it might be a large pool of risk averse savings not readily available to lenders without excellent collateral. And when the same groups of people that have the savings also have the collateral where does that leave the younger lenders with the bright ideas and the willingness to work hard?

So the way I look at it is - if credit to business is actually tight in New Zealand, the govt is reluctant to lend except through the banks (who won't actually lend to business - so it's like saying no the govt won't lend to business, directly or otherwise) then Adrian Orr has actually managed to keep the wheels of credit turning through the lowering of interest rates and the leverage of property as collateral for loans.

If inflation is due to supply constraints, overseas growth is going to fall everywhere but the US (and maybe even there because of an anemic fiscal package) then we are going to be back where we started with a neoliberal govt who won't lend to business and a RBNZ governor who must again chose between recession or house price rises.

If there is a villain it is the neoliberal government who guards it's own budget surplus in tight economic times at the expense of it's own taxpayers and their ever increasing private debt.

Personally I would rather the govt come up with state loan schemes to support younger people to get ahead rather than the govt come up with schemes to confiscate older people's assets (supposedly to give to younger people) which they then use for their own purposes, a la Venezuela or Zimbabwe.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.