A sharp correction in house prices remains a "plausible outcome" that would have broad economic implications, the Reserve Bank says.

The comment comes in the RBNZ's latest six-monthly Financial Stability Report released on Wednesday.

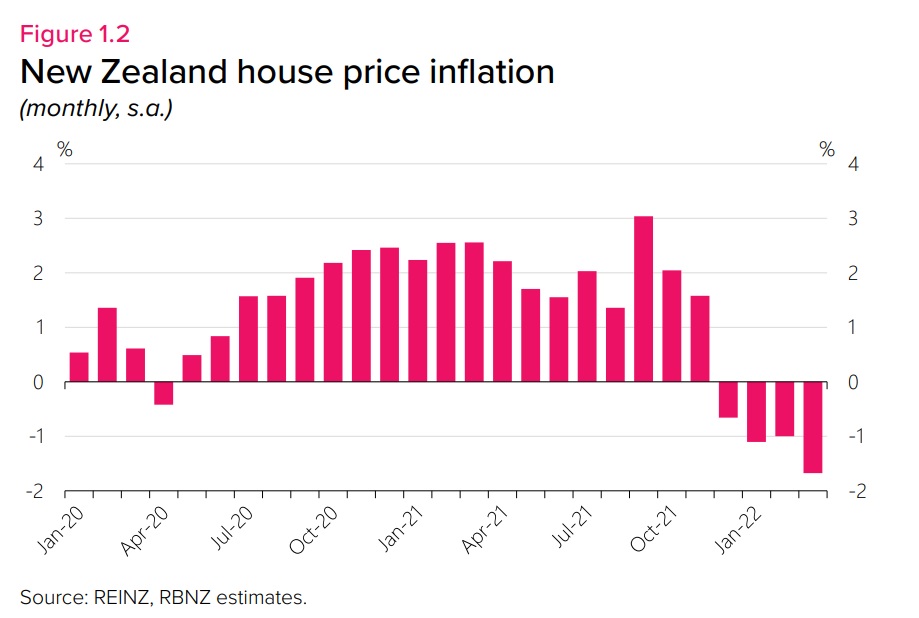

The bank says in NZ house prices have been declining since November, "but still remain elevated above their sustainable level". It says a "steady adjustment of prices towards more sustainable levels based on fundamental demand and supply factors remains desirable for the stability of the financial system".

"...While a gradual decline in house prices to more sustainable levels is desirable from a financial stability perspective, a sharp correction remains a plausible outcome that would have broad economic implications," the RBNZ says.

"Recent buyers with limited equity are particularly vulnerable to house price declines."

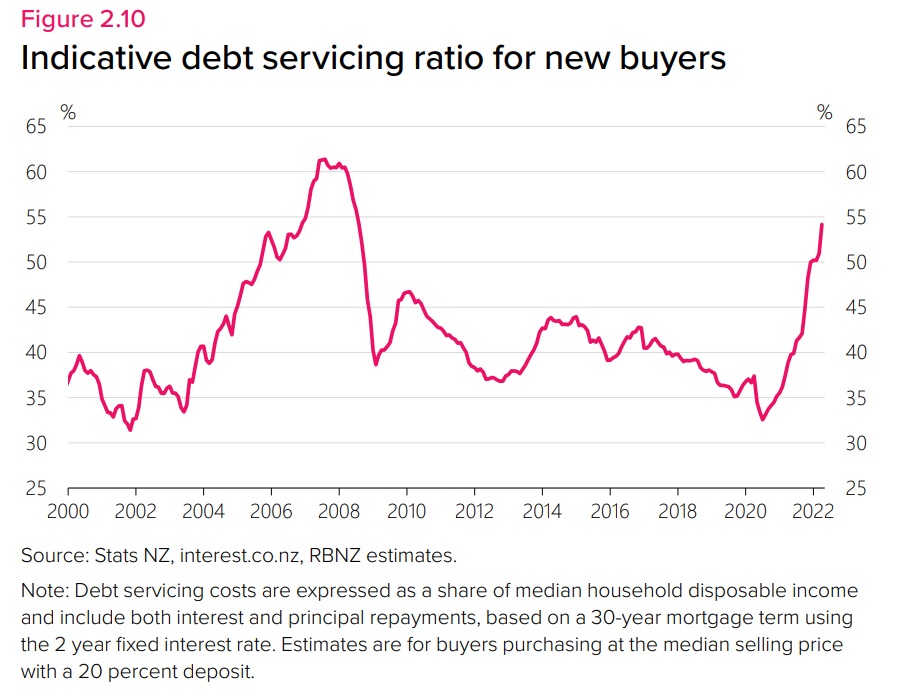

(Data released with the latest FSR estimates that between the end of September last year and the end of April 2022 the percentage of disposable income taken up by debt servicing for new buyers has risen from 42% to just over 54%.)

During the press conference after release of the FSR, the RBNZ indicated that about 25% of new buyers in the past year would have to pull back on spending with mortgage rates at 5%, while for rates at 6% this would rise to about a third of buyers needing to reign in spending, while with mortgage rates at 7% this would become about half of the buyers needing to tighten their belts.

"Furthermore, a large fall in house prices would significantly reduce housing wealth and could lead to a contraction in consumer spending, especially when combined with borrowers cutting back discretionary spending due to rising interest rates and higher living costs.

"Debt-servicing costs will increase significantly as current fixed-rate mortgages reprice over the coming year.

"Some recent mortgage borrowers are vulnerable and could face difficulty servicing their debts, but overall the threat to the financial system is limited.

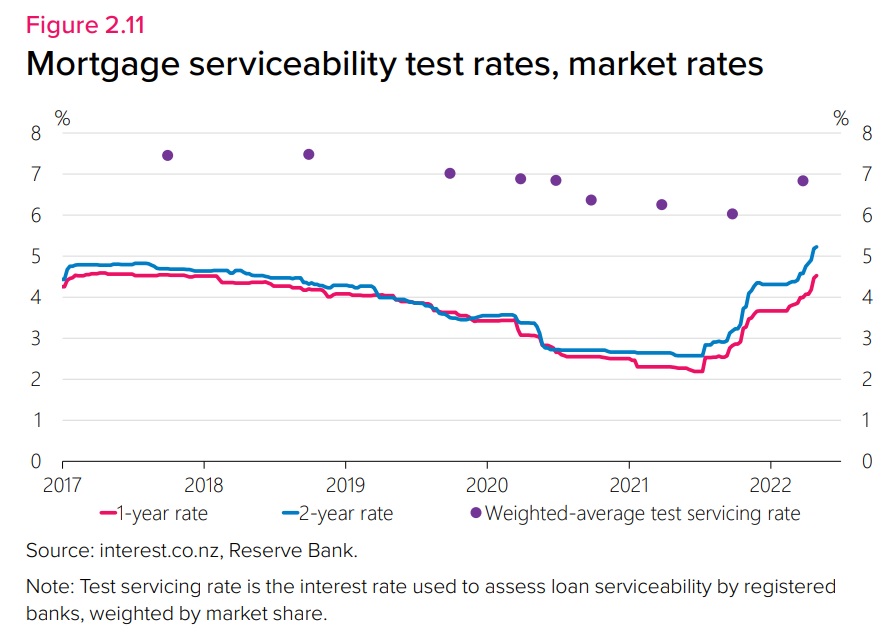

"Banks kept test interest rates in their serviceability assessments around 6% during the pandemic, which remains above current mortgage rates. This provides some reassurance that buffers are in place to ensure debt serviceability continues."

The RBNZ says the risk of debt servicing stress or negative equity is low for most mortgage borrowers as Banks have generally kept the test rates at which they assess loan serviceability well above the actual rates that borrowers have contracted at.

"This provides reassurance that sufficient buffers are in place as the stock of lending is repriced towards the mortgage rates now on offer in the market.

"However, recent borrowers with elevated debt levels relative to income would incur significant debt servicing costs if mortgage rates were to rise above these test rates.

"While we do not anticipate acute servicing stresses to emerge among a material proportion of mortgage borrowers, rising debt servicing costs as monetary policy tightens are expected to cause discretionary household consumption to soften."

(Separate statistics released with the FSR show that bank test rates bottomed at 6% on average as of September last year, but had risen to 6.8% by the end of March. However, they are likely higher now. The country's largest mortgage lender ANZ increased its rate to 7.15% this week, and ASB confirmed its one increased to 7.35% from 6.85% this week).

The RBNZ says that as house prices have begun to fall in recent months, it has continued to monitor the extent of mortgage lending in negative equity.

"Relative to December 2021 prices, we estimate that a 30% fall in house prices could lead to around 10% of all outstanding mortgage debt to fall into negative equity (that is, the value of the borrower’s property is less than the outstanding mortgage amount).

"LVR [loan to value] settings have acted to limit the risks of future negative equity for recent borrowers, while earlier borrowers have seen large gains in equity as prices have risen in recent years. Given the large increase in prices over the past two years, it would take a substantial decline in prices to see widespread negative equity."

The RBNZ has been working on the question of debt to income ratios and has recently released its response to a period of public submissions.

"We believe that DTI limits are an important additional tool for reducing financial stability risks and supporting house price sustainability, and would fill a gap that is not covered by existing regulations. We plan to have the framework finalised by late 2022, so that restrictions could be introduced by mid-2023 if required," RBNZ Deputy Governor Christian Hawkesby said recently.

In the FSR release on Wednesday the RBNZ said banks’ test interest rates have begun to rise in line with mortgage rates, "and we expect to see a slowdown in high-DTI lending over the coming months".

"The new CCCFA regulations, changes to the tax treatment of investment property, and tighter LVR restrictions on owner-occupiers are also having an impact on the availability of mortgage credit. We therefore do not see an urgent need to impose an interim test rate floor at this stage, but we are monitoring the situation closely and do not rule out this option if there is a resurgence of risky lending in the housing market."

This is the statement the RBNZ released with the report:

New Zealand’s financial system remains robust in the context of significant global economic challenges, Governor Adrian Orr says in releasing the May 2022 Financial Stability Report.

Globally the COVID-19 pandemic continues to pose complex economic and financial challenges. Ongoing disruptions to production and supply chains, such as those currently evident in China, are wearing on business confidence and adding to input costs. At the same time, international travel restrictions and related uncertainty are contributing to labour shortages and constraining production.

“Russia’s invasion of Ukraine has heightened these challenges, including the significant human impact. Trade flows are being severely disrupted by economic sanctions and logistical issues. With Russia and Ukraine being significant global producers of energy and food commodities, this conflict has lifted global commodity prices,” Mr Orr says.

Rising commodity prices and supply disruptions have driven global inflation above central banks’ target ranges, prompting a global tightening in monetary conditions and higher longer-term interest rates.

“The combination of a global pandemic and war is a significant challenge, but we are confident that the New Zealand financial system is resilient to a range of potential outcomes,” Mr Orr says.

In New Zealand, the reopening of borders and easing of COVID-19 restrictions will positively impact the tourism and hospitality sectors. However, many businesses will be tested as the broad COVID-19 fiscal support ends. Targeted fiscal support remains for the most affected households and businesses.

Globally, and here in New Zealand, asset prices are coming off their highs as investors have revised up their outlook for longer-term interest rates. In New Zealand, house prices have been declining since November, but still remain elevated above their sustainable level.

Banks and insurers are in a strong position to support the economy and provide the financial services we all rely on. Banks remain profitable and well capitalised – the latter in line with our requirements. The banking system is well funded and positioned to maintain lending in the event of a downturn, Deputy Governor Christian Hawkesby says.

“Our actions are safeguarding ongoing economic and financial stability. By raising the Official Cash Rate and signalling further tightening to come, the Monetary Policy Committee has acted to head off rising inflation expectations and minimise any unnecessary volatility in output, interest rates, and the exchange rate in the future. Our loan-to-value ratio requirements for mortgage lending have also limited the accumulation of highly leveraged loans, building economic and financial resilience,” Mr Hawkesby says.

“We are working collaboratively with the industry and Council of Financial Regulators on governance, risk management, capital and liquidity. By strengthening our supervisory and legislative frameworks, we are investing in our own capability and capacity. We are adding to our macro-prudential toolkit through the design of a debt-to-income restrictions framework for future use if necessary. In addition, we are continuing to work with the government and industry on longer-term challenges like financial inclusion, climate change and understanding housing supply constraints,” Mr Hawkesby says.

166 Comments

"Furthermore, a large fall in house prices would significantly reduce housing wealth and could lead to a contraction in consumer spending, especially when combined with borrowers cutting back discretionary spending due to rising interest rates and higher living costs."

If only we had some sort of body that was in charge of maintaining financial stability in this country...

That does not describe the role of RBNZ, which is in-charge of maintaining the financial net worth of NZ's wealthiest homeowners.

No, that is not true, they only did their 'bit' ! Then this was further clarified by Statistics NZ that RBNZ only did '0.9% of a bit' :)

Slo-mo train crash meets implausible deniability..

GV27,

You beat me to it. I was going to copy the same sentence. When Orr was appointed, I thought it was a good move, but boy, was I wrong.

I guess it's whether we want to believe "maintain" is the same as a guarantee.

It seemed kinda fishy central banks could build speed ramps to jump over the economic headwinds of covid. Turns out they couldn't and we're inevitably paying for it. With interest.

I don't know about how those other countries fared with cheaper borrowings but RBNZ printed excessive amounts of money knowing well that much of it would be pumped straight into housing by commercial banks.

Now as these banks sit back and cream higher interest $s out of those gigantic mortgage assets, NZ can expect its unsustainably wide current account gap (sitting at -5.8% as of 2021) to widen further.

What's going on here is mirrored many places, just the timings will vary.

Because we dodged covid for the most part we've been partying the longest, so ours is ending sooner.

Never mind that the creamed interest payments largely go offshore, further weakening New Zealand

Yes our banking system has completely lost its moral compass. From a sustainable development perspective, the people and profit components are tarred with immoral actions that shouldn’t have been allowed.

Australian Gangstas

Could we also Feather them Tarred People with Immoral Action History?

I_O,

"Yes our banking system has completely lost its moral compass". Can you tell me when the banking system last had a moral compass?

The two go together like; Trump and honesty or labour and policy delivery. I am sure you can think of other examples.

You don't say

While a gradual decline in house prices to more sustainable levels is desirable from a financial stability perspective

Have they defined "sustainable" yet or are they still dodging the question?

3x-4x income ya reckon. Like up to the bank deregulation period in the early 90s.

hahaha,

RBNZ experts have no idea. they said house price fall by 7% during pandemic.

Mr Orr also said house price rises were caused by supply issues and not monetary policy. Maybe its a case of correlation not causation? But it seams to me that there is a pretty strong relationship between interest rates and house prices...

There is now irrefutable evidence that Orr is a political stooge and catastrophically out of his depth. The only chance we have is Luxon get's in and cleanses the lot of them.

Orr is gone next year anyway, isn't his contract up ? He will scuttle away, job well done with a golden handshake no doubt. Doesn't really matter who we have at the top, they are self serving their own best interests at the end of the day. You need to realise that once you join that "Club" they have your arse covered.

He doesn’t need the money. He didn’t come to the reserve bank for the cash, he made more at the super fund.

Yes, he may not need the money, but Orr will leave with his reputation in tatters.

Whatever good he may have done at the Super Fund is long forgotten.

. .. he will leave hand-in-hand with Trevor Mallard ... each tightly clutching their new Knighthoods ... Sirs of the Realm ... just rewards for a job well done ...

Queen Jacinda will be glowing in the background , a radiant smile ... so proud of her boys ...

... with his political stooges.

I am sure that 7 houses Luxon will have the interests of the average kiwi family front of mind.

If Luxon is our saviour, god help us all...

"Mr Orr also said house price rises were caused by supply issues and not monetary policy."

HAHA!!!

Mr Orr said Inflation in NZ is caused by global factors, aka printing dollars. Mr Orr somehow knows no newly printed dollar entering housing market?

Exactly. They over-stimulated the market, made soothing noises about asset price growth when questioned and are now going to destroy the economy to try and restore credibility.

The fact that the Kiwi $ is getting battered against our trading partners tell's you all you need to know about their performance.

Was always going to happen. Even back in 2019 there was only so far rates were going to keep dropping.

Covid was just the last suger fueled push to keep our economy pumping, but the rate rises (globally) and pressures from that were inevitable. Was always just a timing question.

Our issue is that out overshoot is more than most, especially in housing. But to me that's not a bad thing, just a normal credit cycle in need of correction.

I remember you saying the lesson from this was to not bet against/fight the central bank like what had happened was a good/ok thing (prices going up 20-30% in a year).

Do we say the same then if they crash the market and prices fall by the same amount?

ie no point complaining, just adjust your investment position based upon what the central bank is doing.

House prices can never rise at 30% per annum, that's totally unsustainable and I never said that was a good thing. My issue with Orr is his inconsistency.

But below you say that you 100% support the first year response which caused house prices to go up 30%.

You can't have it both ways!

Were they actually up 30% in the year to March 2021? I think you have to give them some slack, it was a huge unknown, shares were tanking. It's the period from June 22 they are culpable.

June 21?

Yes sorry, June 21

Agree

Not so long ago, he was saying increasing asset prices, including house prices, were a feature and not a bug in the bank's policy response to the pandemic because they make consumers feel wealthier and spend more

Call me cynical, but here's an interesting fact - the average age of millennials is now 34. Average age of first home buyers? Also 34. So the average millennial who has been lucky enough to buy has bought a house pretty recently, and now all of a sudden high house prices are not a feature any more, and the powers that be are not, as they have done in the past, pulling out all the stops to support them.

The average millennial graduated into the 2008 recession, faced a decade and a half of basically stagnant wage growth and soaring house prices, and now just when that average millennial has maybe just scraped into the housing market, prices are tanking and interest rates are rising, and wages are falling far behind inflation. If you set out to design a set of economic circumstances specifically designed to screw a generation over I don't think you could have done a better job.

Those millennials who brought before about mid 2020 will will have experienced great capital gains. It is just people (mostly but not all, millennials) who brought from about mid-2020 who are could face negative equity. Many millennials will be fine because their parents helped them buy and don’t expect to be repaid.

You are talking about a small portion of millennials. You also need to consider those who were unable to buy at all that are wishing for prices to crash.

Thanks al123, there are a lot of disenfranchised people out there. Someone told me that inequality is now worse than it was in France before their revolution. If people keep screwing over the youth, we will see history repeat.

Agreed - I think something that has not really had much attention is that seeing people who have made really similar life choices to you live lifestyles beyond your wildest dreams simply because they are 5 or 10 years older than you is a recipe for resentment. It is really hard watching people who are just a little bit older than you who do similar jobs and earn similar amounts take nice holidays and do nice renovations etc when you are still scrimping and saving and have no hope whatsoever of ever being as well off as they are, even if you work just as hard if not harder.

This may be a case of the grass is always greener. Not sure but people tend make out that their lives are better than they are to impress others.

Orr is symptomatic with what's wrong with the country : No one can man up & apologize... no one can admit to getting it wrong ... everyone in power is playing the blame game ...

.... you'll never hear a " sorry , I stuffed up , I promise to learn the lesson & to work harder at getting it right " ...

We are in the era of " pass the buck ! " ...

Odd, seems to me we live in the era of "The Apology". Anyone that behaved what is now considered a non PC way as a 4 year old, 50 years ago, now has to excoriate themselves publicly until the news cycle finds the next target.

That's only for important matters like offending the current "in" crowd. Minor thing like screwing up the economy, causing people to go hungry and homeless don't count.

It is a strong belief all across the management jobs, that you should never apologize or say sorry because that makes you look smaller and weaker and you will lose respect.

Currently, that's how it is running at least in the Oceanic region.

Yes.

However, admittance of fallibility (within reason) is a strong and admirable leadership trait.

They would normally fall during a pandemic but the drop in interest rates saved them. Now that interest rates are starting to rise prices are dropping. Economics 101.

You may remember essentially the whole world predicting economic doom at that time, RBNZ were hardly an outlier.

Hindsight is a wonderful thing.

This just isn’t a valid excuse. Dropping interest rates was justifiable during the height of the uncertainty. I don’t think the RBNZ is being criticised for that.

this issue is when the lockdown ended and the economy started overheating, the RBNZ failed to respond for months and months and left emergency stimulatory policies in place when they weren’t needed

But removing the LVR limits was a stupid idea at the time and looks even worse in retrospect

I agree re LVRs, that was a dumb call. The only benefit (obvious at the time and in retrospect) was to inflate the ponzi.

have to disagree -- as many commentators pointed out on here -- if you are not prepared to borrow when the OCR is 1.5% -- moving it to 0.5% is not going to change your mind - there was no need or practical justification for dropping the OCR and as you say droppign the LVR in order to bring investors back intot he market was not just stupid -- verges on criminal

I didn't say I support everything they did - I certainly didn't think they should remove the LVR restrictions. My point is that sitting here in the future and criticising previous predictions, at a time when the whole world thought calamity was on the doorstep, is a bit rich.

Criticise their actions for sure, but to criticise the prediction of falling house prices is to expect super-human foresight on their behalf. What happened took everyone by surprise, although again I agree the RBNZ was slow to adapt to reality once it became obvious prices weren't falling.

I supported their first year response 100%.

The issue we have now is that a generally small subset of the population did very well from Covid but now the average person is going to get clobbered and be far worse off than pre-covid.

If memory serves, it was you who said about a year ago that this is "a dangerous time to be middle class". It certainly is.

Foresight is even better. RBNZ knew the fiscal response (paying everyone during lockdown and guaranteeing mortgages), but had to look like it was doing something. So it went crazy and did way too much. The fiscal response was enough, Robertson was throwing the visa card at everything and anything.

The huge OCR drop was beyond stupid, like many of us said at the time. A .25% drop would have been more sensible given that they knew low interest rates were blowing up the housing bubble. These guys aren't supposed to panic, remember? They are supposed to stop bubbles remember?

Then they dropped LVR's in a move that is possibly the dumbest thing they have ever done. Right when you need financial system stability, you throw out the thing that is helping financial system stability. It's stupidx10 and we all knew it. I still think Bascand is gone because of it, just nobody is saying that's the case. Whether that's because he didn't want to look any more embarassed than he already did or because he was pushed on... not sure. But the timing is way too coincidental.

Then out came all manner of funding for lending programs and money printing. Completely not necessary. Remember how they aren't supposed to blow up bubbles, but then readily admitted pumping up property prices so that people would go out and spend!

All in all however, they should have predicted those actions to be pretty dumb. The pandemic didn't change and wasn't likely to change the monetary environment enough for them to warrant such egregious, irrational responses. And now we all have to live with their horrific decisions.

Agreed - at last RBNZ recognise what has been blindingly obvious for a year or more to us with more than two brain cells. Next the RBNZ will predict you get wet by standing outside in the rain - but don't hold your breath for there announcement.

We plan to have the framework finalised by late 2022, so that restrictions could be introduced by mid-2023 if required," RBNZ Deputy Governor Christian Hawkesby said recently.

Going hard and early.

RBNZ certainly has the luxury of time to foot-drag when it comes to restrictions on house price growth. Contrast with the speed they acted to remove brakes on mortgage-lending in 2020 at the mere whiff of house prices predicted to slip.

“We plan to have the framework finalised by late 2022, so that restrictions could be introduced by mid-2023 if required…”

We could be well into a crash by then. So reactive and not at all pro-active.

This isn't very "on brand" of the RBNZ. They aren't supposed to say that "a sharp correction in house prices remains a "plausible outcome". Why would they say something is plausible unless they are sure of it happening? Are they sure that house prices will correct sharply? Say it ain't so...

I wonder how many spreadsheets it took t decide if they should use plausible as apposed to possible or likely?

You assume they know how to create a workable spreadsheet!

Just putting the idea out there so that if it does happen they can claim ‘see we told you this was possible’ as opposed to being perceived as completely caught off guard.

They used plausible because it's happening now and they are pretending they aren't sure. They know that prices are already correcting sharply in some regions.

I can’t think of any investment that has huge returns with zero risk. Anyone who thought housing was a one way bet was either gullible or incredibly naive. I feel sorry for the FHBs, but any investors caught out by this only have themselves to blame as they were sucked in by FOMO. Yes government policy has changed, but history show us that this can happen and the risks should be managed accordingly. It was never going to be sustainable at LVRs of x10 household income.

So you feel sorry for FHB but investors only have themselves to blame? How does that make sense?

And how do feel about FHB's who made a killing over the last 2, 3, 4 & 5 years?

Nobody with 1 house who wants to keep it has made a killing - they still own the same house, with the same debt. The benefits of rising house prices accrue to those with > 1 house, and possibly those who want to downsize who are very unlikely to be FHBs.

They have only made a killing in comparison to the poor unfortunates who were unable to get into the market.

MFD, the FHB who bought 2, 3 , 4 or 5 years ago is $hundreds of thousands better off than the renter who didn't buy. From the renters point of view, the FHB made a killing

Yes, they have only made a killing when compared to those who couldn't participate in the market.

I bought a house 3 years ago and it's gone up in value quite a lot, but this doesn't have any impact at all on my life, financial or otherwise. I have the same house I bought and the same mortgage I would have had if prices hadn't increased. If prices fell 30% from here, still no impact on my life, financial or otherwise.

If I buy a second property and the price goes up significantly, or my share portfolio doubles - that's making a killing. That actually impacts my life. I disagree with the idea that house prices rising actually helps your average owner-occupier.

But if you have borrowed money, you have made a much larger capital gain (percentage wise) than if you had 100% equity financed the purchase. Only those who own a home without debt (and do not need to downsize to fund retirement), are truly indifferent to whether prices fall or rise.

Yes, but that capital gain is irrelevant as I can't realise it. If I want to keep living in a house, that cap gain is tied up in the market and doesn't contribute to my lifestyle. It's just numbers on a spreadsheet, not to be converted into money I can spend unless I want to downsize in a few decades time.

My mortgage is not particularly significant compared to my other assets, so I'm indifferent to what happens to house prices in NZ from a personal perspective. From a societal perspective, I hope they fall.

You just have an issue that you also "made a killing" of untaxed unearned money. You prefer to save thus term for the "bad" investors but you can't stand being in the same group as them

No, you are misreading me. I would class myself as an investor and I have a healthy untaxed capital gain on my share portfolio. That's something I could sell and spend on retirement, a holiday, a new car, whatever. I still own a house in the UK as well - that's something I can sell and realise as I don't need it to live in, and I am doing exactly that.

The increase in value in my NZ property is not consequential to me as I can't realise it if I want to continue living in a similar or better house. This capital gain is categorically different. This is the case for virtually all owner-occupiers and appreciating this might reduce the dull and damaging obsession with the price of our houses which contributes to our current crazy situation.

Those who truly benefit from rising house prices are the small minority of people with > 1 house.

OK, thanks for clarifying mfd

Only if they sold Yvil. If they haven't sold it, they made nothing. If they borrowed against the change in value, they may well be deeper in the poo than the could have been.

How does a FHB make a killing? The capital gain cannot be realised without selling the property and if they want to move to a larger property or retirement home, those properties have also become more expensive, they can only make a killing if they sold up and moved to a cheaper area or overseas. Paper gains are not gains.

Many investors congratulated themselves on how clever they were playing the tax system and leveraging equity. If they have been caught out by the market turning it would suggest that most gains were due to luck rather than skill, and that they were speculating not investing. There wasn't much sympathy for those locked out of the market by the property mania of recent years.

I broadly agree with your argument that FHBs ( or in fact owner-occupiers in general ) have not "really" made a gain on the place they live at .

In this light what do you say to those ( TOP , Greens .. ) that would still tax them on that imaginary gain ?

It's offset due to changes in other areas of how you're taxed.

When you say offsets I presume you mean lower income taxes etc. right ?

Still there would be a large difference in tax due for a home owner vs a renter on the same income - how is that an "offset" ?

It is a daft policy that punishes those approaching retirement who have spent 25 - 30 years paying off a debt which cost them over twice what they borrowed due to interest. Does it take into account costs in maintaining the property? If I paid $600k for it, spent $200k renovating and it was then worth $800k. Would this be a $200k capital gain? What happens in a falling market? Do we get a tax rebate? The only policy that makes sense is to tax realised profits from sales of homes that are not the primary residence.

If you are a investor and lost money investment is not your game. The good investors would have left the market end of last year and most of them did. The end of this housing market crash will be discussed for years probably be one of the biggest falls from top to bottom in modern history

Some speculators may have sold but not investors. Also the good investors don't buy the average house, and they are, as you say, still very much up on what they paid

We're looking to sell a property in Wellington, so this isn't exactly the best of news for us. However, I've felt for a long time the "market value" was disconnected from the "real value", and I've prepared my wife for the likelihood that offers will be below CV despite the property being in excellent condition and a prime location.

But while this will put a damper on our plans, I'm kind of okay with this.

We've owned the property for nearly 20 years (it was our first home together, not bought as an investment) and we'll still walk away with a good amount of money. We always thought we'd hang on to it forever, and maybe retire back there, but now we have new priorities.

We're actually quite excited about being able to focus just on ourselves now. Sure we're probably down $200K or so from the peak, but we never had that money in the first place, it was just made-up digits on a screen, and if it means someone else gets in for a (slightly) more reasonable price then I'll call that a shared win.

If it goes to a FHB, I hope the market stabilises and they can be happy with their very own home. If it goes to an investor, well, ya pays yer money and ya takes yer chances.

What a healthy attitude.

Its pretty easy to have that kind of attitude when you bought the house for $250K and sell it 20 years later for $1.2 million. My attitude has kind of shifted that way in only 15 years.

I’d go as far to say that having some disappointment in a paper loss, but ultimately gleefully taking advantage of the next homebuyer is quite unhealthy.

My wife and I had this conversation when selling in 2020 - do we offer it at a lower price to a FHB? The answer was no, because unless the vendor of our new house did the same thing we'd be transferring our wealth the the FHB. In the end it was academic because only FHB tendered on the house.

What wealth? There is no wealth until you sell, the wealth you're talking about losing is the buyers future wealth to begin with. They are trading years and years of generating income and paying interest for a roof over their head. Any gain that was made on that sale over and above wage inflation is the buyer paying you with their time for no real world value add.

Versus us increasing our mortgage to make someone else's mortgage smaller? That's just foolish and our children would suffer the consequences.

"the wealth you're talking about losing is the buyers future wealth to begin with"

What a self-entitled comment.

Read it again, and don't stop until you understand it properly.

Baffled.

Maybe read the words again.

Dropping interest rates to zero has impacted asset pricing (upwards valuation) by borrowing cash flows from the future and bringing them into present prices. Raising interest rates will do the reverse.

P = CF / r to infinity.

r = discount rate (mortgage interest)

CF = wages/rent

I should point out we've bought and sold in the years in between - we moved out of Wellington for health reasons but had to keep an "anchor" there in case work called me back. We lost on the house we subsequently bought during the GFC, and gained on the current run. If prices had been more stable in the intervening years then my income now would have allowed me to live in a much nicer house than we are now, and my children, who will be looking to buy in 10-15 years, would be able to buy their own home easier too.

There is no glee involved here, and the only disappointment is with the price rises that have painted me as a villain in the eyes of some. While I'd love to be able to hand the property off to someone else for much closer to what we paid for it, that wouldn't make much of a dent in our current mortgage. And so the cycle continues.

Oddly this is classic bubble psychology…while prices are going up the narrative is ‘I’m holding onto this asset forever so price rises and falls don’t bother me’. But then a strange thing happens in human psychology when prices do actually start falling…people start processing their paper losses and then choose to sell because they are driven by the pain of losses (read Kahneman). …and more then more do the same until what was an under supply of homes becomes a glut.

Someone posted something similar regarding crypto a week ago. Was a HODL believer before, but no more after fearing more paper losses.

Yes it is interesting isn't it? One can pretty much just argue that the value of the whole market will move consistently, the only issue will be whether they would have to borrow to go where they want, but likely not in this circumstance.

I was of the opinion we should sell about a year ago as it seemed unlikely work would ever recall me to Wellington, and we had an established fmaily life in Hawkes Bay. However it just took my wife a year to come round - due to her health she is no longer able to make quick decisions. As I said before, this was never an investment for us.

I’m sure if you asked yourself this simple question then you might understand that you’ve not lost anything, and your gain comes at an incredible loss to some other poor mortgagee:

If you inflate the income you had when you originally bought, to when you sold, would it be possible for you to purchase the house from yourself? Make a direct inflated financial comparison. The difference in gains between those two values is somebody else’s additional debt. That is debt beyond what is reasonable to pay back.

Exactly - unless you believe the benefits of a financial Ponzi scheme are endless/limitless.

So we're in agreement - I've lost nothing because I never had it, and the property market is insane.

For what it's worth, I've just used the RBNZ wage inflation calculator, and yes someone in the equivalent position would still be able to borrow enough to buy the house today. Gathering the deposit, of course, would not be so easy.

But doing that calculation has also shown me that despite nearly 20 years' worth of experience, knowledge and promotion, I'm only just ahead of the inflation curve.

Depress yourself. Check out how your wage tracks against growth in the minimum wage, which has been kept low by accommodation supplements that fed into inflationary housing pressures - over the same time period. Not to say the minimum wage should be low, but have your wages grown as much as it has?

By 235%? I bloody wish!

Call me confused.

Your wage has inflated by less than 235% in the last 20 years, though the median house price has inflated by more than 500% in the last 20 years. Though you also stated on the same inflated wage your could buy your property off yourself though "Gathering the deposit, of course, would not be so easy". Based on the income, it's more than twice as expensive.

If you originally bought with 20% deposit, the equivalent DTI would mean covering the 50% difference in house affordability with deposit. So you would need a 60% (50% plus 20% of the rest) deposit. Not so easy, but you may have solved FHB problems for sure. Simply save a 60% deposit :)

It's much simpler when you take out broad figures and focus on this specific situation, which was the original question.

Back when we bought we could pay for it easily because it was a run-down dump with maggot-infested carpet, in which the previous owner, a confirmed bachelor, died at 92 years old, and I was making bulk money in IT. The 20% deposit was about 70% of my annual income. Unlike FHBs of today we didn't have to mortgage ourselves to the hilt just to get a foot in any door at all. We then spent four years slowly turning that dump into a lovely, warm, dry house.

Today an equivalent person, as a FHB, making an inflation-adjusted equivalent income to what I made back when we bought (which the RBNZ calculator suggests is my old income x 180%) would still be able to afford the house, but it would be much closer to the pain limit, and saving the deposit would be an order of magnitude harder at about 160% of their annual income.

However, that equivalent person would also be acquiring a well maintained, fully renovated, vastly improved house to what we bought.

I'll reiterate once again, I think the market is nuts, and has been for many years now. I've never told a Millennial/Gen Z to eat less avocado, nor to work harder, nor claim to have paid 24% interest on my mortgages, nor any other statement used to make younger people feel bad about themselves. I know we had it easier then, and I know how hard it is now. For crying out loud, I like younger people so much I made a couple of them (with help).

"(with help)."

Ah, so that's what I've been doing wrong!

I like the senitment in this post, but it did highlight a point around this:

However, that equivalent person would also be acquiring a well maintained, fully renovated, vastly improved house to what we bought.

Houses aren't supplied in run-down bargain basement form into the market, so if they get snaffled up and done up, eventually the 'foothold' we only had by virtue of having so much crappy stock relative to population at the time disappears. If people start doing it en masse to flip for the tax free gains, AND you end up with more imported population, AND you basically supply no new affordable housing into the market, you've got a recipe for a rising floor. And it's an invisible problem if it's outside of Wellington, for the most part, which is where the decision to cram in more and more people and build less and less get made.

NZ is a poor proposition for our young people. I would feel worse for them but as a millennial home owner, it will likely only improve at my expense. Damned if you do, damned if you don't.

It's been my experience that there will always be crappy housing available in NZ to do up, because we're still building plenty of them. Before we bought our current house (a barely livable, uninsulated 1910s bungalow) we rented a "premium" 2016 build in Havelock North. Both houses have the same temperature and dampness issues.

The big difference, of course, is that they used to be cheap.

No one is forcing anyone to take on that debt. Don't want the debt, don't pay for the house.

Be quick! Blow off top followed by an Ark funds style collapse.

Where I live two types of houses are not selling. The old big and expensive character homes and the entry level houses in average locations. The latter are usually poorly maintained. Near new homes well located and tidy/new lifestyle properties are moving on under two weeks.

This is economic dissonance.

Monetary tightening in the US and Australia will put such downward pressure on the NZD that Orr will have no choice but to shadow their moves with OCR hikes in the face of a falling housing market. It's a race to the bottom. Property prices or the NZD.

So why would he start pushing DTI which is only going to drive the property prices lower after a brief period of FOMO prior to it landing. It just boxes him in even tighter and removes options. Another beautifully executed self inflicted wound.

DTI a good idea to prevent a bubble forming…introducing it during the possible capitulation phase of a bubble seems some what crazy.

Well it's been a good run. Bought our very basic first home in 2017 in Wairarapa for $200k with 25% down. Sold late last year for just shy of $600k and put that into a dream character home on 1/4 acre in a leafy street.

Good luck everyone!

Yes some other poor fool is holding the $400k capital gain you made in mortgage debt somewhere else in the market.

I was thinking the exact same. $400k clipped as the bank collects the interest on it for x years.

Printing value out of thin air.

It’s a fools paradise.

Exactly that's the sad thing. The capital gain we made was then handed over to the vendors who buggered off to Australia. So while we have the house, we have a bigger mortgage and a good amount of "equity".

It would be comical if it wasn't so sad. The gains move offshore to Australia. The interest on the loan gets paid to offshore banks. A $1m mortgage paying a swap back to RBNZ... So for that compounded ~$1.5 - 2m of NZ income, we're pumping how much back into the NZ economy?? We're trading the cake for a slice.

Agreed. I too could angrily shake my fist at the sky, but like most owner occupiers I'm just trying my best to provide my family with a stable and comfortable place to live. Nobody had guns held to their head when making offers and taking out mortgages.

Maybe not guns but there were some fairly strong arm tactics used by RE agents to encourage FHB to borrow as much as they possible could. In my dealing with agents they said the market would never go down and rates would be low for ever. "If you don't go high someone else will and you will miss out" They scoffed when I suggested the market was over valued, "don't worry about thinking you over-paid, it will be worth more tomorrow". Fortunately, I never trusted any of them.

While that might be generally true in the market, we sold (and bought) via Deadline with a B.E.O. There was no negotiations at each end, it was just "here's our offer, thanks, bye". Our REA asked if we wanted to negotiate further, but the offer was inline with our BEO amount so we just accepted it.

My blame lays solely at successive Governments who have been too incompetent to bring in something as simple as a Debt to Income ratio limit. We might all be financial gurus on here, but I know of aspiring FHB that wouldn't have a clue what would be deemed a prudent amount to borrow in relation to their income. Many have little understanding of interest rates. They'll buy a house when the bank approves their finance and the vendor accepts their offer.

My observation was that the agents were taking advantage of the lax lending environment that you mention and encouraging the naive FHB to borrow to the limit of what the banks would lend them, rather than what was sensible to borrow. The bank would have leant me almost 3 times what I borrowed, but I knew I couldn't afford it if rates went up.

Caveat emptor, quia ignorare non debuit quod jus alienum emit

"Nobody had guns held to their head when making offers and taking out mortgages.".

Exactly this.

Lets say it didn’t rise. Was still worth $200k when you sold, you could have got that nice character home for how much? $400k? So $200k extra lending. That sounds pretty awesome as well right?

Yes you are correct, if prices remain static then the amount you need to borrow to trade up is a lot less. Depends on individual circumstances.

In our case, vendor paid $540k in late 2016. We would need another $50k on our initial deposit if we wanted to maintain >80% LVR, and then borrow $430k. Instead we borrowed roughly $500k at a considerably lower LVR and the cream went to the vendors who moved to Australia.

Yea trading up can be done a few clever ways.

While the market is trending up, if you put in a conditional offer of your house selling first, then it's possible the value of your house might have gone up by the time it sells and you made a small profit towards the offer.

While the market is trending down, you want to sell before you buy. The sudden turn in the market recently has caught people out by this very simple mistake. ie they can't sell in the same market they've already bought in.

While the market is tanking, sell and go on a vacation for a year... or move to Aus as it would be.

Except the vendors typically put in an escape clause giving you 3 - 5 working days to go unconditional if they receive an offer that's not less favorable from the market, why is why it's also important to have a back up plan if you have your sights set on a particular property.

Do a key word search "must sell" on Trademe property. Now look at the prices that those would be sellers are still asking. Now look at photos of the property. This has a long way to go. Pity the FHB's and the overstretched upgraders of 2021.

Or will Mr Robertson have a surprise parachute for the housing market to deploy on budget day. Labor are down in the 30's now.

... it's one of life's ironies that whatever Robbo does , he keeps helping the rich get richer ... every cackhanded plan Ardern's government has hatched to right the wrongs , to level the playing field , has ultimately backfired , and caused the lot of lower & middle socioeconomic Kiwis to get harder & harder ...

its always been he same --- long as i remember -- Labour promises much to the poor and working class --- but in the end their mismanagement usually causes inflation, borrowing, unemployment and impacts more on their core vote that the wealthy -- just this time they have managed to couple it with spectacular asset price gains -- the like has never been seen in NZ ever -- making the gap even bigger !

the unemployment will come next year, right on cue to remind all those voters that they made a dreadful mistake 3 years earlier. Hopefully we never get a majority party in power again, we need that small coalition party in there.

While we will enter a nasty recession, fortunately unemployment may not go too high.

Because of so many kiwis emigrating over the next 6 months.

I reckon the recession will be nasty but unemployment might ‘only’ peak out at about 6-7%.

The interesting thing for me is how much the die was ways cast two years ago. If we wanted higher LVRs/DTI ratios, that was the time to do it. Nothing we do now from a financial stability perspective matters. I don’t know how much the market will drop, I think a lot of the fall will be soaked up by inflation so a 30% real fall might only be a 10-15% nominal fall. That will make everyone feel better about the situation.

It's only soaked up by inflation if wages rise to match inflation. If not, you get poorer. If so, inflation continues spiralling up.

Looks like by the time this over society will have won you just can’t have average house costing 12 x average couples income still a way too go.

No surprise. Reset to a Dti level the average man can afford, and move away and legislate to ensure there is no repeat of the finance ponzi of stupidity.

KABOOM!

A good, well balanced assessment of the housing situation and risks

RBNZ FSR May 22 claims: Domestic petrol prices are currently 29 percent above the average from the past five years. And yet:

The GDT dairy auction price index plunged 8.5% at the overnight auction, more than the 2-3% expected, driven by falls across all product groups. Skim and Whole milk power prices fell 6.5%, while butter was the biggest mover, down 12.5%. The price index has now fallen for four consecutive auctions, taking the cumulative price decline to 13.4% since 1 March. Link

More to the point, Diesel prices are knocking on 3x higher. I get truck stop diesel for the ute, and a couple of years ago paid a little over 90c/l. Now the latest invoice is $2.26/l. And diesel, not petrol, runs the economy.....Food, logistics, construction, industry - all the basics.

And still we have the roading lobby pushing hard to double down on this reliance rather than pivoting away to more sustainable transportation system.

We don't need a central bank; the experiment has failed. Central planning is a communist ideal. How about 1000's of community/public banks across the country in a decentralised way? The opposite to central planning. If anyone has read Prof Richard Werner's work you will know where I'm coming from.

He's been pretty active on twitter lately...essentially saying that QE has turned asset markets into a pozni scheme. And if QE ever stops, the system collapses upon itself. That brings us to about now...

It was never intended to become the solution to the problem....and now it has become another problem that in itself needs to be solved!

Central banks need to be forced back to using a much smaller tool set. Probably just use the OCR to control inflation, and have a minimum floor of say 2% OCR. No more of the crazy shit, if we get deflation at 2% OCR then let it be.

There shouldn't be any servicing stress caused by rate rises yet because we are still well under the test rate. As long as unemployment holds everything will be fine in the wider economy, we'll just start to see deleveraging.

Except when banks had to begin looking at potential mortgage customers actual expenses instead of imagined ones. Due to CCCFA.

They were suddenly deemed to be no longer credit worthy as the banks believed that if interest rates rose to the stress test level. Those customers could not realistically trim their expenses enough to make the mortgage payments. So you could assume that prior to December 2021 there were mortgages approved at a lower stress test rate than exists now. For customers that would have been denied a mortgage if their actual expenses had been examined.

We'll just have to keep an eye on arrears and defaults to see if stress is starting to show.

Figure 2.10 is amazing, I might get it printed, framed and hung on the wall. Look at how quickly we went from 2020 with "the most affordable" debt servicing in decades to the nudging the least affordable back in 07/08. Of course, the mortgages are 2x - 3x bigger this time and we've only just started lifting off interest rates from emergency lows so this is just the start.

"RBNZ says sharp house price correction remains a 'plausible outcome"

Tell us something new Mr Orr. With your action, are you surprised.

So I gather we are in agreement that we are past the 'if' stage, and even past the 'when' stage and are now just debating the 'by how much' stage?

Are we not duffrunt?

No. Most of the western world has binged on a frenzy of cheap FIAT, and inflated assets to a degree that borders on stupidity.

Time to spell fundamentals.

Ashley Church might be the only person left who is still in the ‘If’ phase. Actually he’s never even been in that phase, it seems that a house price correction is something he can’t even register within his very limited mind.

He popped up in a brief market summary from one of the news outlets the last few days (trying to find source) and he was looking rather rough around the edges. Almost like he was in a state of shock/severe cognitive dissonance.

Adrian Orr looks that way fairly often.

He reminds me of Beaker from the Muppets.

He admits that his genius strategy is to use the past to predict the future. He obviously hasn’t studied world history (sub prime USA, Ireland, Japan etc).

Frankly, the guy is an idiot, who has been misleading lots of people, especially impressionable and desperate FHBs. I'm starting to prep my letter to the Herald about their lack of balance in reporting on the whole house price fiasco, and am thinking to take it to the Press Council too

The real question coming up next after we get to the bottom of this fall whenever that is, is "what policy changes do we need to make so this does not happen again?'

Or are we just going to do a rinse and repeat - seemingly have learned nothing.

I guarantee it will be rinse and repeat.

If you get to the perfect point in a cycle to make changes (never let a good crisis go to waste) but do nothing, then it will show the politicians to be either corrupt and/or incompetent.

From what I can tell from the theory, and 35 years in the industry, there is no more goodwill, no slack left in the system.

If changes are not made for the long term better, then both the short term and long term are only going to get worse.

To be fair to RBNZ they'd painted themselves into such a corner with low interest rates and quantitative easing that getting out without crashing the market would have been an astonishing feat.

If the RBNZ was a private company, the board and CEO would have already been sacked. The incompetence is next level. Very low interest rates created massive distortions. Money in the bank became worthless, so it moved to real estate and the share market. RBNZ intervention is more trouble than it is worth. Of course the mortgage rates have shot up quickly, but not so quickly for the deposit rates. RBNZ guestimates are mostly wrong with hindsight.

What are they (RBNZ) crying about, are they not perpetrator .....crocodile tears.

No Shame.....No Moral....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.