The Reserve Bank says it will push ahead with developing a framework to limit the ratio of debt home buyers can borrow in comparison to their incomes, but won't be setting the interest rate banks use to test borrowers' ability to cope with rising interest rates at this stage.

The Reserve Bank has published its response to feedback received on its proposed policy for debt serviceability restrictions (DSRs) on residential mortgage lending, which was issued in November. Consultation closed on February 28. (See our coverage of what the Reserve Bank said in November here and here).

It sought feedback on the merits and potential design of two types of DSRs:

- Restrictions on debt-to-income (DTI) ratios – which impose a cap on debt as a multiple of income; and

- A floor on the test interest rates used by banks in their serviceability assessments which test the ability of borrowers to continue repaying their loans if interest rates rise to a certain level.

“Our modelling indicates that first-home buyers would be the least impacted by a DTI restriction, with investors impacted the most as they tend to borrow at higher DTIs than other groups on average," Reserve Bank Deputy Governor and General Manager of Financial Stability Christian Hawkesby says.

"This aligns with our Memorandum of Understanding with the Minister of Finance on macroprudential policy which states that in designing DSRs, we will have regard to avoiding negative impacts, as much as possible, on first-home buyers. Additionally, the use of speed limits and exemptions can further mitigate any negative long term impacts on first-home buyers."

"We believe that DTI limits are an important additional tool for reducing financial stability risks and supporting house price sustainability, and would fill a gap that is not covered by existing regulations. We plan to have the framework finalised by late 2022, so that restrictions could be introduced by mid-2023 if required," says Hawkesby.

This pushes back the timeframe outlined in November when the Reserve Bank said banks needed to prepare their systems for the potential introduction of a regulated DTI limit no later than the end of 2022, saying a DTI restriction could be implemented by the fourth quarter of 2022, and a test rate floor could be implemented in the second quarter of 2022.

Hawkesby notes banks’ test interest rates have now started rising in line with market rates, and the Reserve Bank expects to see a slowdown in high-DTI lending over coming months.

"The new Credit Contracts and Consumer Finance Act regulations, changes to the tax treatment of investment property, and tighter loan-to-value ratio [LVR] restrictions on owner-occupiers are also having an impact on the availability of mortgage credit. We therefore do not see an urgent need to impose an interim test rate floor at this stage, but we are monitoring the situation closely and do not rule out this option if there is a resurgence of risky lending in the housing market," Hawkesby says. "We will undertake further work on the preferred methodology for this tool, in case it is required in future."

As reported by interest.co.nz over the weekend, ANZ says people applying for mortgages currently need to be able to satisfy it that they would be able to service debt at an interest rate of 6.7%. And ASB says it’s testing applicants using a rate of 6.85%. The two banks’ standard one-year to five-year fixed mortgage rates range from 4.49% to 6.45%.

In November's consultation paper the Reserve Bank assessed the impacts of introducing a DTI cap for borrowers of six or seven times gross income, and a test interest rate floor for bank lenders of 7% or 8%. However the Reserve Bank stressed these were illustrative models and might not necessarily be where it would set such restrictions.

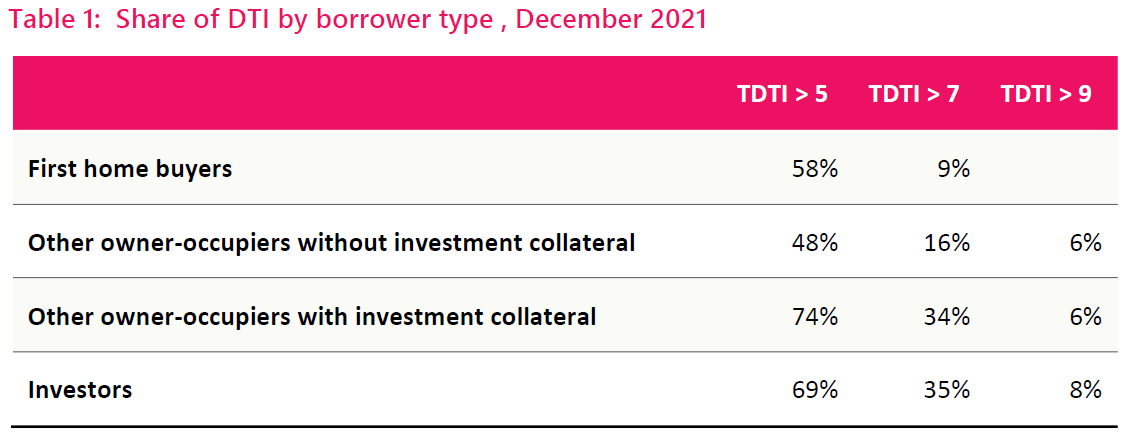

The latest quarterly Reserve Bank DTI data, for the December quarter, showed a levelling off of DTI ratios following very sharp increases over the past couple of years as the housing market went into overdrive.

The table below comes from the Reserve Bank.

The Reserve Bank says it uses macroprudential tools, such as LVR restrictions, to reduce the financial stability risks associated with boom-bust cycles in the economy. This, it says, helps meet its statutory purpose of promoting the maintenance of a sound and efficient financial system.

The Reserve Bank's attempts to add a DTI tool to its macro-prudential toolkit date back to at least 2016, but were previously stymied due to politicians' concerns about the tool's potential impact on first home buyers. The central bank previously consulted on the potential introduction of a DTI tool in 2017.

84 Comments

What's the odds the Debt to Income multiple is set at some ludicrous value in order to have absolutely no effect on the property market whatsoever?

Be Quick to secure a home ahead of the rule

There's word of the banks preparing for these changes with an internalized DTI of around 6. Ireland as an example has LTI (loan to income) of 3.5

Do you think existing mortgages will be grandfathered in and DTI limits will only apply to new lending, or will existing loans run into the DTIs as they come to re-fix?

Great Question!

I would suggest it would only be new lending.

If they were bright they would start it at 6.5 and reduce it by .2 per year until they reach their goal DTI

DTIs should only apply to new purchasers. Otherwise, homeowners who can afford the loan would be forced to sell because a ratio arbitrary to them is too high and no bank wants to refix with them.

I suspect there will be another set of ratios by borrower type. DTIs will hit FHBs the hardest, so Labour will want to shelter this cohort from such changes.

They could always apply separate DTIs to FHB and investors, as with LVRs.

Looking at the chart in the article showing DTI levels by borrower type, it appears FHB will actually be impacted the least!

I'd be happy with an exemption for mortgage renewal on a house that the borrow lives in - investors always have the option to sell to bring their portfolio in line.

As mentioned above and by me elsewhere in these comments, FHBs are not affected nearly as much as investors by a simple DTI test.

My understanding is that existing mortgages would not be affected by the new DTI limits - it would result in the need for widespread restructuring of loans and/or early repayments and political fallout.

That said, banks have a tendency to become over zealous when new rules come in and could force some borrowers to restructure even if not technically required.

Odds of a DTI that ends up having to be so high that it is functionally useless, or so low that it kneecaps FHBs at the expense of investors?

There is a middle ground that barely affects FHBs and knocks out the worst excesses of investors. Set a DTI at 7 (which I appreciate is very high internationally and should be brought down over time), and you impact ~10% of FHB lending and take out ~35% of investor lending.

https://www.rbnz.govt.nz/statistics/c40-residential-mortgage-lending-by…

Ah, but how likely are they to actually choose the sensible option?

Given the timeliness of this work, I am not hugely confident that they will choose a good outcome just because it possible for them to choose it.

I remain cautiously optimistic, even in the face of past disappointments.

The important thing to note from the data I linked to is that introducing a DTI is much more effective against investors than FHBs, and we should be extremely wary of vested interests crying crocodile tears on behalf of FHBs when they are introduced. FHBs have their wings trimmed a little while investors are kneecapped.

I wish I had your confidence, my good chum.

My guess is it may be set low enough to bite some investors but the Reserve Bank will be very alert to kneecapping FHBs because they will not want to irritate their political masters.

So late, so slow. I did not expect anything better from the muppets at the helm of the RBNZ anyway.

Yes mid 23 should have been mid 2020 !! In any case unavoidable interest rate hikes especially for NZ and US will stop the first tier A rated banks lending on overpriced housing speculation, especially in the highest price to income country in the world, you guessed it, NZ.

2023 a bit going on in the banking world. Deposit guarantee scheme is meant to be up and running sometime then too.

No, it should have been mid-2012. Now we have blown the bubble up so much it's almost impossible for it not to pop.

Exactly - DTIs were the tool to have in place when interest rates were falling, not now, when they are rising 🙈

They want to get them in place to limit the next rise.

Yeah, but what IO is saying is that it will amplify the fall, because essentially you are restricting lending now in multiple ways. It's like the RBNZ is in bizzaro world where it does all it's actions backwards, doesn't implement things when they should, then implements them when they shouldn't.

W-w-what is this? Bizarro World?

Worst. Reserve Bank. Ever.

But they have been trying - since 2016 and the government wasn’t keen at the time and hasn’t really been until they indicated differently last year! But it was far too late by then, there are countless people in way over their heads by now. It is just so unbelievably frustrating to watch this all unfold as everyone warned it would. I am left leaning politically so tend to give Labour the benefit of the doubt on most things, but I will never forgive them on this.

The Reserve Bank's attempts to add a DTI tool to its macro-prudential toolkit date back to at least 2016, but were previously stymied due to politicians' concerns about the tool's potential impact on first home buyers.

Does this give them enough time to crash the market and lock in a sensible DTI limit like UKs 4.5?

The horse hasn't just bolted, it's already been turned into glue and dog tucker. Unbelievable.

Yes it is an academic exercise in keeping those earnest folk at the RBNZ employed. That they cannot see the complete lack of value in it says as much as anything.

Agree 100% with the comments above.

Emergency OCR levels should have been accompanied by the likes of a DTI to avoid the current property bubble. I'm surprised that the RBNZ are happy to make announcements like this that draws attention to their incompetence and tardiness.

Exactly, the emergency stimulus would have been available for real needs and business, and a DTI would have limited the amount that was used for property speculation. Hopefully RBNZ has learned if we ever need QE again in the future.

Surely they must have realised dropping the LVR would have such an effect...

Well most commenters here certainly did. I was fuming at the time but didn't bother commenting because everybody was saying the same thing.

What is the meaning of this now?! Are they trying to put some FOMO back into the market?

Current NZD to UDS: $0.656

Official NZ Inflation: 6.9% [just say 7%]

NZD's Purchasing Power Adjusted for Comparative Inflation:

0.07 * 0.656 = 0.04592

0.656 - 0.04592 = 0.61008

Though crude [TWI Free], at BEST today's NZD-to-USD currently buys what USD $0.61 brought a year ago.

Forget housing, find a store of value! The RBNZ is still NOT taking inflation seriously! The OCR at 1.5% proves they don't understand the gravity of the situation.

Thoughts on viable stores of value these days?

My thoughts would be to dollar-cost-average into:

- Bitcoin

- Silver

- Rare Earth Metals ETF

- Uranium

- Perhaps Copper (though it's already had a great run)

'Shorting Plays' are also a strategy, though one that's seen many go broke. Diversifying forex holdings would probably provide some form of hedge.

Lol at Bitcoin suggestion, which is down almost 50% from its high.

Consider zooming out further.

$US.

Think how many trillions of dollars of $US-denominated debt are out there. No matter what happens, dollars are needed to repay those debts. The demand isn't going anywhere. And the Fed is tightening.

You a Brent Johnson/Dollar Milkshake theory fan Sam B?

I've got USD, Yen, EUR, AUD to cover FX risk coming up...they make all tank initially against USD if the demand for dollars increases with high debt burden/interest payments denominated in USD.

This does seem to create a FOMO in the short-term provided the DTI is not too high (which would make it useless). In the medium to long-term, 3 years + this could bring about greater stability in the market that may manage risk and mitigate extreme house price increases as buyers (first home or investors) are constrained with the amount of lending/funding they can access. Unsure of the details related to how investors' cashflow/income (if not on a normal 9-5 wage/salary) is accounted for as part of DTI and how this affects homeowners/investors that have significant equity.

I think it would have been great if they implemented this in the past year, or the past 14 years rather.

The glimmer of FOMO would surely be turned around when they get out the calculator and plug in the interest rate though right? ‘Ooh better borrow 9x my income today, oh nah wait can’t. Can’t even do 6x right now, dam veggies, petrol, interest rates, council rates etc’

Absolutely. DTI of 9, interest rate of 6%, there goes 54% of your gross income on interest alone.

Moving with urgency, you can tell RBNZ are serious about reigning in the property market...

So now that interest on rental properties is taxed as income will it also be viewed as income for DTI calculations?

Interest is not taxed as income though, no idea what you are on about.

Yeah, so interest is a non-deductible expense for tax purposes. Not income.

Same result different words

No, it's not even close. Are you having me on right now or is the actual level of intelligence of your typical property investor?

You can certainly work out those who have been investing for 30 odd years in many diversified investments and those who think they know with no personal experience at all and probably nothing to show for it as a result. Typical intelligence of those who dont vs those who do

Diversified investments? From the sounds of it you wouldn't be able to read an income statement so I imagine the only diversity in your portfolio is in which suburbs you bought a rental in.

FTFY :

Are you having me on right now or is the actual level of intelligence of your typical interest.co.nz common tater?

And the answer is slewing rapidly towards yes IMO.

I get your attempted point JustAnOpinion but the brightline rules are a completely separate debate. What about properties not affected by brightline rules. Taxing interest as though it is income is fundamentally flawed and goes against all the common sense rules of accountancy. By all means address any perceived issues with good legislation but at least come up with something that stands up to scrutiny.

you have no idea what you are on about. Interest is treated as income not an expense - simple

If you're a bank, yeah.

Funny

Wasn't a joke.

"Interest is treated as income not an expense"

Are you getting confused because deductability is being phased out for investors?

Might want to refresh the concepts and laws found in the Income Tax Act 2007

Income Tax Act 2007 No 97 (as at 16 March 2022), Public Act Contents – New Zealand Legislation

Why would it? The investor is now worse off as they are paying more tax on the same rental income, why would that justify more borrowing potential?

Seriously though, I have heard from other commenters here that rental income will be discounted with some formula to account for the associated expenses of the rental property for DTI calculations, I don't remember the precise details.

That's odd. The RBNZ proposal considers DTI to take gross income into account, not net. That is income before tax and expenses.

It would be perverse if rental income were taken at face value for a DTI, without any discounting for the insurance, rates, maintenance and likely interest costs associated with the income. Treating this appropriately is a nice clean lever to affect investors without bothering FHBs, which the Government has made clear should be spared the worse of any regulation.

Ahh yes I'm with you now.

Either way, with 40% LVR and a DTI of ~6, the rental yield would need to be around 10% to be able to purchase. If that income is _after_ interest, insurance, rates and general maintenance then the impact on small scale investors would be incredible. Goodbye yellow brick road.

Absolutely - the old strategy of growing a rental empire using equity from your existing portfolio is dying the death of a thousand cuts.

Another waste of time. You cannot implement changes in a years time to correct problems that exist here and now. With the timing of this and an election next year, everyone will have forgotten about it by then anyway. I can see why some people on here get as mad as hell, its just jawboning and then you wait forever for it to happen then its crickets on that as they talk about the "Next big thing".

Yeah they started brining in LVRs in 2013 when they knew they had a problem.

nine years ago and boy has the problem got worse

And removed LVR's at the same time as they carried out emergency cuts to interest rates - in hindsight, this could possibly be viewed as one of the biggest blunders the RBNZ has ever made in its history.

DTIs are a clunky regulatory mechanism.

They would not be needed if monetary policy were used to dampen the business cycle rather than a tool that has been used excessively for what are more fundamental structural issues.

KeithW

More policy for the next election to be fought over. Elimination of tax rinsing underway, and promise of DTI, hopefully in a way to target debt based property speculation.

Add in elimination of interest only, and you got my vote.

DTI Was at 3 when I first purchased house in uk.when interest rates hit highs in early 1990 people were just handing keys into bank. Just imagine what would happen now if rates hit double digits.

They should have a variable DTI for new loans and additions to loans. The formula could be:

(10 - the interest rate) / 3 + 4

That way the DTI would range from between 7 and 4 assuming interest rates are between 1 and 10%. If you want to slow the movement of it you could restrict it to moving by 0.1, 0.2 or 0.5 per annum towards the target level.

Debt is so huge around the world even if rates stay at this level people businesses countries are going broke the whole system will implode in next few years and hoping for just a 50% drop will be best result.

Ref the table showing % of borrowers vs DTI, the bottom 2 rows total more than 100%. I can understand it being less than 100% as some DTIs will be less than 5, or am I missing something here?

DTI > 5 includes DTI > 7 and DTI > 9.

So of 100 people, 69 have DTI over 5. Including 35 people with DTI over 7 and 8 people with DTI over 9.

60% of mortgages are refinancing in the next 12 months - with double the cost of debt at minimum

8% are going broke

35% will probably be under considerable financial pressure and need substantially increased income

69% have ignored the old golden rule (that no more than 30% of gross income should be used for debt servicing) so discretionary spending will be hammered unless they somehow manage to increase their income or reduce their debt

Good summary DDDD, I remember refinancing my loan last March, DTI criteria used by the bank was debt = loan balance (plus any over draft available) + bank accounts including overdraft facility @max + credit cards @ max limit. Income was income + overseas income @70% + rental income@70%. DTI max was 5.5

So they stress tested DTI while refinancing your existing debt? Did they give any indication of the fallout if a DTI of 5.5 was not met?

Yes if DTI was not met refinance would be declined.

Plenty of errors there DDD. 60% were for the whole year, we are almost in May already. Many people would have looked at the option to break and refix, the writing was put on the Wall by the RBNZ months ago you had to be living under a rock if you didn't think rates were going to rise. There is no 30% golden rule to that effect, had I done that I would still be renting and broke like so many on here. I maxed out on debt and repaid it as fast as possible.

Why do these things take any time at all.. Oh for some leadership.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.