The Reserve Bank (RBNZ) is wary of the cooling effect higher interest rates will have on the economy, given the mountain of mortgage debt acquired in recent years.

The more debt people have, the more acutely interest rate rises will be felt.

Nearly 68% of the country’s fixed-rate mortgage debt will need to be renewed within the next year. This 68% equates to $194 billion.

Add this to the $38 billion of mortgage debt on floating rates, and you get $232 billion of mortgage debt that will be affected by rate hikes in the next year.

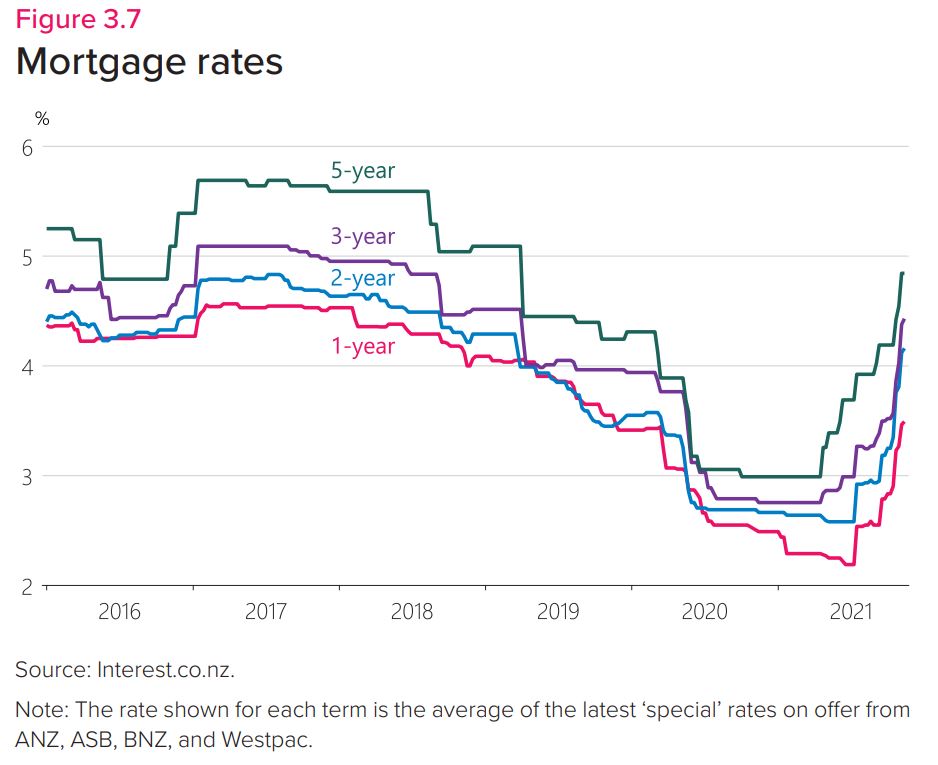

The average 2-year mortgage rate has already jumped in a short space of time to 4.1% from 2.5% in July, as rising inflation has seen markets price in higher rates.

Further retail rate increases are expected, as the RBNZ has signalled its intention to keep increasing the Official Cash Rate (OCR) from 0.75% to 2.6% by late-2023 - a level above what it deems to be the “neutral rate”, which is neither stimulatory nor contractionary.

This means mortgage holders will need to find several billion dollars within the next year to meet higher interest costs; a situation which will reduce their spending power.

In the words of the RBNZ: “High levels of household debt, and a large share of fixed-rate mortgages re-pricing in coming months, could increase the sensitivity of consumer spending to these interest rate increases.”

The RBNZ is mindful of this happening at the same time as the world faces uncertainty around what it means to live with Covid-19.

This goes some way to explaining why it said it plans to take “considered steps” lifting the OCR “for now”.

The RBNZ suggested it prefers making a number of 25-point OCR hikes to cool inflation, rather than making 50-point jumps (as some believe would’ve been justifiable on Wednesday, given how hot inflation is, how tight the labour market is, and the fact the OCR won’t be reviewed again until February 23).

Mountain of mortgage debt could limit OCR lift-off

ANZ chief economist Sharon Zollner is so aware of highly-indebted households’ sensitivity to interest rate rises, she believes the RBNZ won’t be able to lift the OCR as high as it is projecting.

She said this view was partly grounded in the fact it’s “difficult to engineer a soft landing after a boom”.

“A 31% rise in house prices in a year when New Zealand has suffered a negative net income shock means the housing market is vulnerable,” Zollner said.

“We underestimated the power of monetary policy stimulus in 2020, and we’re wary of underestimating its potency when put into reverse.

“The current momentum in inflation is impressive, but a rising OCR with household debt at fresh record highs is a potent weapon indeed.”

Orr puts spotlight on banks and homebuyers

While the RBNZ is wary of the potency of rising interest rates, Governor Adrian Orr was defensive when it came to discussing the potency of falling rates during the pandemic.

Asked, in a press conference, whether he regretted the RBNZ taking a “least regrets” approach towards monetary policy, while temporarily removing banks’ mortgage lending restrictions, Orr said, “Can I note that it’s banks that make the lending…

“I have no regrets of anything we did last year, because in the uncertainty that all people faced - remember this was a period when the virus was brand new; vaccines hadn’t even been invented - no one really knew what was going on.

“I did not want to be providing stimulus with one hand and then tripping over our own [loan-to-value ratio] policy with the other.

“So, we acted consistently to the extent that people have chosen to go off and do what they do. They need to interview themselves and have an interview with their bank.”

A journalist challenged Orr’s response, arguing it might be more constructive for the RBNZ to take some responsibility for soaring house prices, as borrowers have simply responded to the incentives put before them. Orr refused to engage.

He then said he strongly disagreed with the assertion very loose monetary policy had had a “catastrophic” impact on non-homeowners.

“Yes, it may be a challenge for those who want to buy a house right now. Full stop,” Orr said.

“No, it doesn’t mean that wealth inequality has magically increased. Those middle-income people who have a house have enjoyed in that wealth. Those people who don’t have a house have enjoyed in jobs.

“It is a much richer conversation than just continuously focussing on the marginal homebuyer.”

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

100 Comments

How about some sensitivity towards non asset owners who haven’t received a sausage (apart from keeping their job, as Orr puts it).

Job - $15,000 gain leftover from work per household.

Job plus house - $15,000+ $150,000 gain.

Minor disparity is all, nothing to see here

(All figures best guess)

And that $15,000 Job Leftover will get eaten up by transactional costs if you want to change homes. The $150,000 will = zero gain, at best, if you move like-for-like, and turn into a bigger loss if you aspire to something better. (And we wonder why Stock on Market is plummeting as people are trapped in situ)

What a fabulous System we've created for ourselves.

Yeah, the employment argument is a red herring. Most non home owners would rather have had a short sharp period of deep recession/unemployment (underwritten by govt anyway) if it reset house prices 50%. In the long term they would be much better off as eventually you get another job, but house price increases are a giant ratchet that weigh on your future.

Keeping you median salary job is just crumbs relative to what asset owners got.

Most non home owners would rather have had a short sharp period of deep recession/unemployment

Only the ones who were nearly ready to buy their first home would have wanted that. Most under-25s aren't even thinking about houses yet and need a job for income and lifestyle.

Most of the under 25 yr olds I work with (n=36) have given up entertaining the idea of home ownership.

Let's calculate how much an average kiwi on a average salary will save over their life time.

I take a positive view of average salary at 70000. Take home after tax will be 55k.

If they have some expense or good forbid they eat food, then spend 10k on food per year. Which is $200 per week. So now they have 45k in hand. If they drive a car, than 3k per year for gas and car maintenance. Now they have 42k in hand.

Utilities bills of 3k per year. And now they have 39k left for them to spend.

Now if they own a house for average house in NZ costing 850k. Let's imagine they made 20%deposit of 160 k and now they have a mortgage of 690k. At 3.5 % their yearly interest on this mortgage is around 24k. This is only interest, no principal payments. They are left with 15k now. I am sure they have to pay rates on the house. Even in cheap towns, it's around 4k a year. So they have 11k left with them now. Lets add house insurance. 10k now. If they pay 5k principal on the home mortgage, they have 5k left to save for their retirement per year. And i haven't calculated kiwi saver or any discretionary spending anyone has.

And this is a single person. If they are a couple, we can have some synergies and save but god forbid if they have any kids.

So is this a sustainable economy or a country where any one can live a decent life?

You tell me..

No it isn't and the poverty level is rapidly rising up the through the professions. The only sane solution for people is to leave the country.

“Covid-19 Response Minister Chris Hipkins has today revealed New Zealand would revert to the alert level system if a new vaccine-resistant variant overwhelmed the country and the traffic light framework couldn't contain it.

Speaking to The AM Show, Hipkins said while the Government was absolutely committed to the traffic light system, a back-up plan would be reinstating the alert level system which is set to be dismantled next week.

The Government would have to revert to the alert level plan if it had a variant of the virus that was resistant to the vaccine, he said.”

can kinda see what’s ahead…

Covid dying in Japan. Humans have not survived just because for hundreds of years. Human body has evolved for generations with the virus. Humans are a strong species. There will be casualties but in the end we will survive and virus will die.

No, it doesn’t mean that wealth inequality has magically increased. Those middle-income people who have a house have enjoyed in that wealth. Those people who don’t have a house have enjoyed in jobs.

I don't even have words.

Wow, didn't realize all the homeowners are unemployed.

Too bad for people who face tripling their mortgage if they want to start a family. Of course, wages have also increased by 300% right? And all other living costs are static?

I didnt realise there was a correlation of employment security vs home ownership?

"so, do you own a house?"

"errr, no im 25 and they are very expensive"

"youre hired !" (until you get a mortgage)

"Those lords who have land have enjoyed in that wealth. Those serfs who don't have land enjoyed not starving to death."

A classic "Let them eat cake" statement from a fully out of touch public "servant". Followed up by actually marginalising those that don't own homes by calling them "marginal".

Taken as a whole, all his answers to questions are "I don't care if I pump the ponzi to unattainable levels, I can blame others and get away scott free. And I don't give a flying f$%k about people that don't own homes". It has an undercurrent of "I will leave anyway before I have to look responsible for any of my decisions".

Yikes. Careful mentioning the out of touch cake lady around here. Ed doesnt like it.

In medieval times, where this dude is taking this country, he'd be defenestrated. Here he can say whatever and the caravan goes on. Without people in the streets protesting there will be no change.

'defenestrated', Thanks for the new word!

Increased mortgage costs mean less spending money and upward pressure on rents. Now add in globally driven price increases and the imminent withdrawal of Govt fiscal stimulus (wage subsidy and resurgence payments). We had better hope that the price of oil, shipping etc comes back down quickly - or we have the perfect recipe for a demand crash.

we have the perfect recipe for a demand crash

My theory has been that this is all going to unravel through the consumer sectors of society. The ski trips to Queenie; the pricey coconut yoghurt on the supermarket shelves; and the Sunday brunch with the family at the trendy cafe. So far, all are standing up well according to the data. The wealth effect is working. No cause for alarm. Meanwhile, in other developed countries, everyone's migrating to the cheapest possible retailer to ensure the wallet stretches further.

There was actually a comment on here last week about a wellington restaurants stats.

Same number of people but they are skipping that extra drink and dessert.

That's what we need to slow down inflation.

The stupidity is caused by sheeple fellow kiwi. In the day and age of social media and communication, we are letting RE agents and media to take over our critical thinking. All buyers just need to get together on a forum and decide enough is enough. Just don't pay the big bucks and hold on. What you got to loose if everyone holds on for 6 months so and year and run with FOMO. You will see how prices will come back to reality.

We are a small country with 2 degrees Seperation and if one person tells the other, it will be revolutionary and we will have save our future. So just don't buy and see how prices will fall and be more realistic. Don't fight with each other at auctions. We are not animals. Think with human logic not your primitive brain where you have to compete to survive.

I guess even if a few listen, we can have a big impact. We are just making investors and RE leeches rich by doing what we are doing

Or it might just be predictable behaviour given the difference in the regulatory landscape between housing investment and trying to build up a small business.

Only option is TOPs tax policy. Otherwise to many vested interests (MPs portfolios).

I tried that. Sold in 2013, thought things were high but infact they were very low. I occupy a service tenancy so don't need a house.

Result is eight years on I'm soooooo far behind with savings not within miles of keeping up that added to age means I will probably never own a house again and retirement isn't really an option.

Don't try this kids.

Unnecessary... the market will resolve itself in a disorderly fashion soon enough

“Can I note that it’s banks that make the lending…

So Orr is saying not to blame him for the credit creation to bid up the prices of a generally fixed housing stock, thereby destroying the value of people's savings and income.

“So, we acted consistently to the extent that people have chosen to go off and do what they do. They need to interview themselves and have an interview with their bank.”

Once again, not his responsibility. It's all about the sheeple and the commercial banks.

Orr has been abrogating his responsibility for his decisions since he came in. He is also abrogating his responsibility to maintain a sound financial system. Its a classic misdirection that we should all be aware of.

In order to maintain his policy of 'least regrets' he has to absolve himself from all responsibility- otherwise he might regret what he's done obviously.

Good grief his responses are just dripping with arrogance and hubris. The RBNZ clearly had a massive failure in predicting the impacts of its covid response, but he sticks his fingers in his ears and blames banks and borrowers for following the rules HE put in place. Reducing LVR's was a mistake from the get go, as many predicted. Initially lowering rates wasn't the issue, it was leaving them far too low for far too long.

People had jobs during the pandemic because of the government was paying half the countries wages, not because of of the RBNZ's ham fisted response. But the really concerning thing is he has "no regrets" about the financial stability risks created and the inflation risks, because "people have jobs". Labour adding maximum sustainable employment to the RBNZ mandate is one of the stupidest things they have done

What a mess

Well expressed. Looks and sounds like a man on the defensive, even though the edifice is crumbling all around him. This is a man fastened to and embedded in the dogma and status quo.

At this point it's all he's got. Inflation is kicking off well past the PTA range. House prices have blown out and they are entirely unprepared for the speed they should be moving on DTIs. If this isn't failure, then what is?

Perfectly expressed.

Further retail rate increases are expected, as the RBNZ has signalled its intention to keep increasing the Official Cash Rate (OCR) from 0.75% to 2.6% by late-2023 - a level above what it deems to be the “neutral rate”, which is neither stimulatory nor contractionary.

Hmmmm... R* equates to the neutral rate in NZ.

{kind=link}

From the point of view of orthodox policy, it has been the needs of monetary policy that drove everything lower and by extension upside down. The yield curve has only steepened in the 21st century, and yet the economy of this period has been slower and weaker (in sustained fashion) than at any point since the 1930’s. It sets up an inversion to where the yield curve gets steeper the more the economy slows, which by mainstream definitions can’t be the case.

To solve the “equation” we merely have to frame all references to the nominal. Thus, the steepness of the yield curve itself is a byproduct of monetary policy effects on the shorter rates. For policymakers that has meant R*, the assumed natural rate of interest.

We have to keep in mind that R*, or R-star as it is sometimes notated, is not something that can be observed directly, but despite that limitation is immensely important to monetary policy. It is supposed to define the balance between inflation and deflation; if monetary policy can get “real” rates below R* it is thought of as stimulative. Conversely, if the “real” policy rate is above R* monetary policy is believed functionally restrictive.

Given that framework, if R* is falling then each time the Federal Reserve or any other central bank wishes to “stimulate” it must do so with lower and lower short-term rates in order to get the policy rate underneath where it assumed the natural rate has fallen. Once at the Zero Lower Bound (ZLB), policy is constrained in nominal terms leaving authorities to undertake unconventional policies so as to push “real” rates down where they are calculated to be stimulative.

According to calculations performed by the San Francisco branch of the Fed, R* is indeed falling and has been doing so for decades. As a result, each time the US economy is confronted with cyclical economic weakness such as the Asian flu (which resulted only a near-recession) or the dot-com recession, the “required” monetary policy response has been that much more so. The result is what we see of the yield curve, where it steepens due to the weight of policy on the front end essentially pulling it downward.

But is this really true? There isn’t a whole lot of sense in this formulation. You can see at times that it amounts to reverse engineering rather than defining an internally consistent and logical explanation of the last thirty years, starting with the fact that economists have no idea what might have caused R* to decline in the first place. Further, the bond market just doesn’t work that way, as again interest rates define opportunity rather than being anchored almost exclusively to monetary policy.

A more common sense explanation would be the opposite direction for the chain of causation: the economy slows in structural terms causing the bond market to reduce in its overall nominal framing, where cyclical weakness is therefore more pronounced over time leaving the Fed not to “stimulate” with lower and lower policy rates but to announce in review what has already happened. In short, they are calculating a lower R* as a result of being unable to square reality with the orthodox parameters of how orthodox theory posits reality is supposed to be.

R* is just the plugline or balancing factor that attempts to make sense of why neither ultra-low interest rates after the dot-com recession nor QE in the aftermath of the Great “Recession” failed to work as they “should” have. For policymakers, policy rates went low and lower but since no great recovery resulted, especially from the QE’s, it is merely asserted that R* must have been that much lower still. From this view, QE was surely powerful “stimulus” but it didn’t appear to have worked, therefore R* was just that much lower than QE got the policy rate to. If “real” policy rates had been pushed down to -10%, the still lack of recovery would have left Fed officials claiming R* surely was -10.01%.

This reverse engineering is actually quite common and necessary for a philosophy that is so often backward. What comes first is the lack of growth, leaving economists to calculate an R* based on wherever interest rates happen to be due to their reactionary efforts trying (and inevitably failing) to do something about it. We can observe this relationship in any number of important ways:... Read more

Zollner acknowledges the sensitivity to interest rate increases (even moderate ones) given high debt levels (so, logically, mortgage holders are much more sensitive to say a 1% increase than they were with typically much lower debt 10 years ago) So she still thinks the OCR will go 2% plus?

I certainly don't. Demand in the economy will severely dissipate by the time it gets to 1.5

I don't know what Zollner's role is. ANZ sends here out like a puppet to make half-baked statements like she's concerned about implications in the real world while her employer is 100% committed to the bubble. It's quite bizarre.

Completely bizarre.

Yeah, but there's still the chance that the NZD weakens and forces their hand. USD is on a tear right now. NZD went down yesterday even with the announcement of an OCR hike.

Petrol price is already getting painful. It's a wedge - mortgages vs petrol/food prices... I believe the banks and RB would happily have us all living off potatoes and not going anywhere to save the housing market, but it's not politically popular.

True.

Question, though - how much do the RBNZ look at the NZ dollar in their considerations? Obviously a weakening NZ dollar has inflation implications, so they must look at it at least to some extent.

But, like other things, is not the OCR of marginal relevance these days to the currency anyway?

RBNZ has effectively painted itself into a corner , no matter how high inflation goes it is unable to respond rapidly only by 0.25 increments and those aren't likely to continue until February at least .

I think the 3 month break is very convenient for them.

The housing market is about to slow big time and demand will be sucked out of the economy with rising interest rates.

There's a possibility come February that the economy could look quite different and they may even be able to pause hikes although I think on balance that's more an April / May occurence.

3 months of no control from the RBNZ is a good thing ? Just let the Banks do their own thing over the height of the summer during peak selling season ? Sure what could possibly go wrong. Big risk if you ask me, things could be chaos by February.

I understand they can do an emergency meeting and decision if they really needed to.

What makes you think things could get of control in summer? Lending is cracking down, and the cost of borrowing has risen significantly.

All mortgage approvals are based on affordability at a test rate (circa 7% I believe), so I wouldn't imagine that RBNZ are even remotely concerned about repayment affordability right now. If people are defaulting because the rate moved from 2.5 to 3.5% or whatever that indicates an issue in the banks approval process and shareholders/bondholders will just have to take a loss for wreckless lending.

So they have moved the test rate from 6 to 7%?

I believe main banks have been testing at high 5% to mid 6% for a while now. If rates jump further we're not too far off it. Lets not forget, people accumulate debt outside their mortgage too which is outside the banks control...

Which do you stop paying first, is it the BNPL loan to afford that expensive Dyson vacuum cleaner or your mortgage?

The vacuum,

They’ll hammer you with late fees until you’re on the never nevers.

The bank won’t kick you out straight away.

Hmm its hard one, also got to consider that car, boat and jetski that's been financed...

It doesn't matter what the Test rate is; that's just a tick on a form the banks trot out, come mortgage issuance time.

What matters is actually spending pattern, and most people spend according to cash-flow + available debt.

What did we read last month? Something like 40% of all new mortgage loans in Aussie are based on Liar-Loan applications - and the banks know it! I doubt we are any different.

It's pretty common for a recession to follow a rate hike cycle. It's pretty rare that they get the rate 'neutral'

"Reserve Bank wary of households' sensitivity to interest rate changes in a tightening environment"

Is it really or ai just crocodile tears / concern otherwise, should they not have gone up when had opportunity to move by 0.5% and than in 0.25%.

Who is responsible for promoting debt.... is it not like Drug supiers raising concern of drug issue.

I keep saying, they don't want to hike, or at least not much. It doesn't matter what we think should or should not happen, all that matters is what they think and what they will do is quite predictable based on their recent behaviour.

Come April/ May they will pause at 1.25 or 1.5.

They don't want big hikes now, but inflation and US Fed's future rate hikes will force them to do so. Otherwise, people will lose their confidence in NZD.

by company of heroes | 24th Nov 21, 9:30am

The Reserve Bank has been heralded as a global bellwether before, including in the post Global Financial Crisis world of 2014 when it lifted the OCR by 100 basis points to 3.50%. In early 2015 it received The Central Bank of the Year award from London-based Central Banking Publications, in recognition of innovative work to enhance its contribution to the New Zealand economy.

But this time is different, our housing market is in a completely different situation from 7 years ago. I think they should increase 50 basis points to 1% this time. But whether they actually fullfill their mandate or not is another story. They claim that housing price movement is not in their mandate. But I highly doubt it especially see how they handle and implement DTI at the moment.

"If things are getting too expensive you need to look at yourself and try harder."

Yep. Next time I hear a property owner complaining about the price of gas, I'll explain the wealth effect and how it's good for all of us.

"Look, this encourages BP to spend more money into the economy, and we all benefit... it's essential for employment."

NZD taking a tumble might have to raise sooner that February before currency sharks have a feed

He then said he strongly disagreed with the assertion very loose monetary policy had had a “catastrophic” impact on non-homeowners.

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and

offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax. Link-pdf

Orr said, “Can I note that it’s banks that make the lending…"

Haha, I feel in 2 years time when we have a serious housing price correction, he'll probably use this phrase again "Can I note that it's banks that decide on their mortgage rates?" Hence why he is letting the banks take the lead for this round of rates hike. Pathetic!

Hopefully he's been fenestrated by then and we can just try to forget him.

Tough tits, if you take on debt you take on a risk that interest rates will fluctuate. Since when is investing only allowed to be upside only? What a coddled group of mummas boys this place is.

For those that are interested, Kathryn Ryan will be interviewing Orr on RNZ at 10:00am.

He's not eloquent, is he?

"remember this was a period when the virus was brand new; vaccines hadn’t even been invented"

You can tell that it's not rehearsed, it's all so 'clunky'

“I did not want to be providing stimulus with one hand and then tripping over our own [loan-to-value ratio] policy with the other"

"They need to interview themselves and have an interview with their bank"

Does this mean that he's not confident in what he's saying because he knows it's rubbish?

He knows it's rubbish. We know it's rubbish. The public can be fooled though and he can never admit responsibility as that would mean he has to admit his mistakes (impossible for an prideful, arrogant know it all, which it appears he is). Why doesn't he just admit the removal of LVRs was a mistake? It was clear then, looking at the data, it's even clearer with hindsight.

Question: Just how much control does the RB have over interest rates? Can the OCR become meaningless as other drivers set the 'market' rates?

Yesterday’s RBNZ decision described as “bird-brained” and “spineless” by Infometrics chief economist Brad Olsen.

Brad certainly not holding back – suggests the bank needs to act more strongly.

I tend to agree.

Is it just me of is the RBNZ guilty of causing most of the soon to be carnage, or extreme bank profit with their movements from the last 24 months?

The key takeaway is the nearly 70% of mortgages that are rolling over in the next 12 months. If rates keep increasing or even if they don't drop now from the current position this will really begin to bite in 2023. With energy prices still increasing and inflation high, 2023 could be a total shit storm. Seriously is anybody thinking about all these factors colliding just before our next general election ? I can see some never before seen in NZ street protests happening in 2023 by the disenfranchised youth of this country.

100% agree. Look out for carnage from late 2022 or early 2023. Followed by OCR cuts...which will be significant, and not coincidentally occur in the lead up to the 2023 election...

Btw, I don't think 2022 is going to be smooth sailing at all in terms of covid. It's a key factor underpinning Shamubeel Eaqub's bearishness on the economy and OCR.

The RBNZ could insulate current mortgage holders from cash-flow harm (keep them solvent, in other words) by dropping the OCR to Minus 5% if it chooses, as long as it restricts the issuance of New Debt. That could mean the 'value' of their current holdings deteriorates as 'demand' goes unsatisfied by new debt, of course. But it's a trade-off.

This whole situation isn't about 'the price of debt' it's about 'the quantity of debt'. As Stephen has written on so many occasions, it's about the Risk Weighting that the banks are allowed to place on residential mortgage issuance. Fix that, and the interest rate becomes of secondary importance.

The last bit especially (where he is challenged by the Journo) but all of it has left me gob smacked because it really shows just how disconnected he is from reality.

Under is watch our economy has experience minimal inflation in most areas but in housing 10, 20% + making it significantly imbalanced, and having serious negative influences on other parts. In 2019 he told us they had stress tested the banks and found there was no issue if a 50% reset of house prices occurred (which proves he knew it was an issue), but now he is telling us he is concerned about the impacts of a reset, and that last year he wasn't concerned about the localised inflation!??????

housing 30% 40% or more...

“No, it doesn’t mean that wealth inequality has magically increased. Those middle-income people who have a house have enjoyed in that wealth."

I really don't understand this wealth effect. How is that wealth realised? Maybe if you sell and bank the capital gain but otherwise the "wealth" has an interest component to it that is now increasing if drawn against. Surely the net effect to society for any realised wealth effect is increased costs against it. One persons wealth is anothers debt.

"wealth effect"? I think it's more like "wealth illusion"...

Wealth effect=zero discretionary spending. Why? A storm is coming alongside opportunities. Only a fool borrows against their house to buy non-income producing assets.

Be in a position to ride it out and capitalise on the recovery. In a recession, no-one can see the light at the end of the tunnel.

I think your wrong there, every man and his dog is using the house as an ATM to buy that new car or even spend it on a holiday. Live for today is the new motto, after all who really cares about 20 or 30 years time

Utter rubbish Carlos. I'm mortgage free, have not borrowed against the house for ANYTHING, EVER! Just got rid of the mill stone, and then tried to save for retirement. Currently retirement, if I take it at 65, is looking pretty thin, so I will have to keep working until I can't anymore or I can afford to retire. Certainly the GRI is not enough to live on with a reasonable, but not flash lifestyle.

Jaw dropping. Just how detached from you and I is he?

“I have no regrets of anything we did last year". I welcomed Orr's appointment, but now can't wait to see the back of him. He knew perfectly well what the result of slashing the OCR would be and quite deliberately chose to do so. He expected consumers to use the "wealth effect" to keep the economy going by ........consuming.

Of course there was great uncertainty, but he could have chosen to be much more measured in his approach to reducing the OCR. I also find it hard to swallow his (mis) appropriation of Maori values and language.

Perhaps he and Collins should hold hands and disappear from public view.

The guy is clearly not accepting asset inflation is causing issues and saying what he has done is correct.

No point this is what it is, take it or leave NZ.

Yep it all depends on what side of the fence your on. Plenty of people will be happy about the house price increases if they already own one. Its no better overseas, house prices have rocketed everywhere. House prices in the main centers of Australia were eye watering years ago now they are just crazy stupid.

Plenty of people will be happy about the house price increases if they already own one.

Basically just entitlement mentality.

Actually the opposite is true. Those who bought house(s) paid it with their own deposit and their own money. Those who have a mortgage commits themselves to servicing it.

It is those who has no money nor willing to commit and whines every moment about house prices that are entitled.

No point this is what it is, take it or leave NZ.

You are correct. No point in fighting it. But question is, while the currency and the value of labor is being destroyed, what do the sheeple do to protect themselves?

A journalist challenged Orr’s response, arguing it might be more constructive for the RBNZ to take some responsibility for soaring house prices, as borrowers have simply responded to the incentives put before them. Orr refused to engage.

House prices leaped up - they lost touch with the ground - but it’s not my fault, says Adrian the Clown…

https://thekaka.substack.com/p/dawn-chorus-orr-lacks-regrets?token=eyJ1…

Blatantly Arrogant with no remorse = Power Corrupts = Dictator

Surely a study of economies that had house price crashes after the GFC should show Orr that NZ was getting into dangerous territory.

The dogs in the street knew what was happening in the last 12 months with the housing bubble being in the euphoria stage.

The banks and the sheeple cant be left to make the decisions when there is tasty cheap and easy money available they will choose greed of course.

There is no industry in NZ, milk powder can only go so far, the economy is based on debt, the recession will be tough but inevitable.

I agree when the recession comes its not going to be pretty. When the shit really hits the fan your going to want to be debt free. I can still remember 1987, everyone got shit canned. Lucky I was young, still living at home and debt free so I really didn't care at the time.

It's very easy to see how this plays out next 2 years:

- Late 2021: start of big property slowdown

- By Autumn 2022: the property slowdown starts to turn to a correction. Covid spreads in the community, with or without lockdown, and spending slows after a moderate pick up over summer

- By June 2022 the OCR has been raised to 1.5 / 1.75. With a rapidly slowing economy, the RBNZ pauses

- by Spring 2022, the economic and property slowdown is well underway. Median prices have dropped 5-7% from their December 2021 peak

- by April 2023, recession has hit. The residential construction sector has been hit significantly, with significant job losses, and unemployment has risen above 5.5%. In the first half of 2023, the RBNZ cuts the OCR back to circa 0.5

- with a deteriorating economy, and a resurgent National Party, the Nats win the 2023 election in a close run election battle

More or less agree except the OCR will not be coming down. Energy prices are going to start to go through the roof, its already happening and this flows through to everything in our lives so inflation is coming like never before. The RBNZ is going to get stuck between a rock and hard place, the OCR will need to keep rising.

This article shows clearly that the RBNZ does not play favourtism nor succumb to the agenda of a minority group. Neither does RBNZ play into the dramatic manipulation plays of the mammoth market players or bank economists. It also displays the independence and macro-economic level in which the central bank operates.

If minority interest groups have issues with their special interests, they should go to their ministers in the government instead as they are really the ones whom are responsible for fiscal policies, national planning and budget allocation.

Keep barking at the wrong tree won't change an iota.

The RBNZ did it right!

The RBNZ did it right!

Did what right? Raising the OCR by 0.25%? Nobody is disagreeing with that.

Is it really possible to be employed as the RB governor when you don’t comprehend economic cause and effect ????

Remind me who appointed him????????

I'm afraid to say that Orr and his advisors ..if he even consulted them has proven to be incompetent .....he could easily cancelled some of the "printed money" and stopped the outflow of the cheap money from all the commercial banks and thus the rush to invest in housing.

Its Time we get rid of the Babyboomer policies of the past, greed before people and focus on policies of their parents.

Im a house owner, but this is not fair.

The young need to step up, and people should vote them in.

Pension Asset Test all assets, Tax the hell out of the asset wealthy whom have done well from these unfair babyboomer policies of the last 30 years and introduce a UBI for everyone.

Return stolen money back to the youth, their children and their childrens , children they need it more now than the Babyboomers.

and stop working for families most people on the street don't have children or families.

Single people without children matter too.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.