By David Chaston

It's time to review KiwiSaver fund performance again.

You can find your fund analysed using our regular savings method, and disclosing its after-all-fee, after-all-taxes performance here. (Or use the search box above.)

Our analysis covers 171 funds, so your one is sure to be included. Quite a few new ones have been added recently.

This article covers the overall results, identifying the funds with the best long-term track record. (We have done separate, more detailed reviews of the Default, Conservative, and Aggressive risk categories in the past week at these links).

As we have noted many times previously, track record is only one thing. What you really need to assess, and something we don't do, is whether you are in the best fund for the future. Track record is backwards looking.

And the future will almost certainly be different to the past.

In our March 2018 review, we expressed the view that markets are turning and that the long bull run may be coming to an end. If that is correct, it may affect how you position - or at least, think about - your KiwiSaver investments.

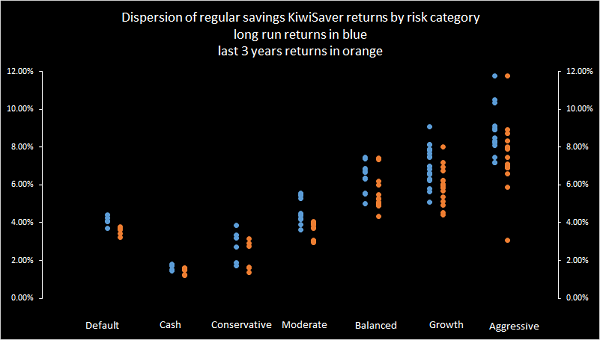

The chart below that plots risk related returns, shows a clear sag in results over the past three years compared to those since-inception. That is pointing out the tailing-off that we alluded to previously.

Yields are now very low by the standards of history. Falling yields pump up asset values, something that bolsters investor returns.

But if yields are turning up, the effect will reverse.

We may not see yields rise much locally, but that is not the point for investors. What is the point is that the major markets of the US, the EU, Japan and China all seem to be facing a higher yield environment. That means asset values for a number of key asset classes will come under pressure. Bonds and property will be affected the most, the asset classes that are strictly traded as a multiple to income streams.

The re-valuation of these assets classes will be automatic for investments in passive management structures. The manager will be unable to do anything about that.

Active managers, however, will have an opportunity to tune their asset allocations - even within bonds and property classes - to minimise the toughest adjustments.

But both investors and managers who have the opportunity to tweak their category asset risks should be doing the work now. We have said before that the imperative to do this is not immediate, but getting prepared is probably urgent. There will be no benefits for lagging the crowd.

This is not to suggest you succumb to the doom & gloom merchants (typically promoted by doomsday Americans, often with online 'offers'). But a shift in emphasis could be very valuable.

Remember, your objective in this part of the investment cycle is to tweak your portfolio of risk, constructing an investment set that is more resilient to asset price falls. More reliable income streams from equities might be on the menu, even looking at some 'alternative asset' classes perhaps.

In my case, it is de-emphasising some commercial property exposure, de-emphasising some bond exposures. But it is not getting out of good investments in these classes. Investments in companies that are fundamentally sound is always a good idea - even when you have bond, or property aspects.

As you can tell, this involves work. It reminds us that investment is work, sometimes hard work, involving sound research. You can either do it at the gritty 'company' level, or more likely you can do it in selecting fund management expertise. Your job is to choose your risk tolerance, and then a manager who can execute professionally.

Perhaps, now is a time to consider whether a shift from passive to active would be a savvy move. Or, if you have already chosen 'active' which portfolio structure you want.

Of course, I could be quite wrong - maybe the great bull run will go on and on forever, yields keep on falling, even below zero, debt continuing to juice the system higher without limit. But I doubt it.

You are now a KiwiSaver and increasingly it is becoming serious money, worth serious consideration.

Based on interest.co.nz's benchmark saver who has been in KiwiSaver since April 2008, one fund now has balances exceeding $60,000. In the way we assess these 171 separate funds, there are now eight more funds with balances over $50,000 and a further 49 with balances over $40,000. If you ignore how your fund is positioned, you will hardly be justified complaining about underperformance.

So, rather than looking at track record when making a KiwiSaver choice, now might be a good time to dive a little deeper and think about how your fund is invested and whether in the future that will weather any downturn better than some other strategy. You probably have a bit of time - maybe a year or two, but unlikely more, and possibly not that long.

You can see the way returns are starting to sag from these category charts. The first one is a view of all KiwiSaver returns, since inception in blue, over the past three years in gold, up to June, 2018.

There has been quite a shift lower in just three months. Our expectation is that this market will shift to lower growth as 2018 rolls on. There will still be some great outlier performers, but generally the sagging will extend.

Time to prepare.

Our June 2018 reviews of the Default, Conservative and Aggressive funds can be found here, here and here.

Top of the list

We award our special 'star'

This is the list of the top funds at June 30, 2018, based on our regular savings return model. For comparative purposes, we have only used those managers who have been in existence for the entire analysis period of April 2008 to June 2018. In the future, additional funds will be included after ten years history.

1. The Conservative Fund data in the table includes cash funds.

2. There are now nine default funds, however, only five have been in existence for the full period of our analysis.

3. Insufficient number of funds to provide data.

In the Aggressive category at least, the winners have been single risk funds targeting yield gains. Such narrow, specialist targeting may not be the best in the future and you can see how quickly these sorts of fund returns have been turning lately, even if they still top our reviews. The past is no guarantee for the future.

For explanations about how we calculate our 'regular savings returns' and how we classify funds, see here and here.

The right fund type for you will depend on your tolerance for risk and importantly on your life stage. You should move only after receiving appropriate advice and for a substantive reason.

8 Comments

I remember that for a couple of years immediately after kiwisaver was set up, the growth funds were actually performing worse than the conservative ones. So since inception, there has been more volatility than the graph above shows.

If there is a real downturn, conservative funds will not do well, but I would say that without exception, growth funds will do much worse.

Of course. That is what you would expect in the short run. But over the long run (what KiwiSaver is all about) that has not proven to be the case. For your view to be right, you need to judge that "this time is different" and after the next downturn there will be no recovery. Seems very unlikely to me.

KiwiSaver has now been going more than a decade, long enough for the economic/business cycle to be through nearly one wave. And all that shows is that economic cycles come and go. It also shows that over a full cycle, righer risk returns outperform.

But if you break it down to short segments within a cycle, you can find anything you look for. (Conservative funds won't "do well" - they will only outperfom growth funds during that down period.)

Very interesting read, thanks.

I’m in an aggressive diverse managed fund and I couldn’t care less about the upcoming slowdown and what sort of a hit my fund will take.

There will be plenty of ups and downs over the next 34 years for me, but it’s only the end result that I care about. Short term volatility, including big drops, is just fine. I’m not going to flip flop about for the next three decades trying to time the market - I’ll leave that to the fund manger. And no, the contradiction with respect to my username is not lost on me.

While an advocate of reviewing one's fund, I have no problem with your stance.

You have at least thought it through and are prepared to take risk knowing the consequences. You have identified your risk tolerance; you will be neither surprised nor concerned if there is down turn and accepting of possible drop in the value of your fund in light of longer term correction.

The scale and scope of data and concise, independent, analysis here far surpasses the often selective, superficial or click-bait financial journalism often seen elsewhere. Thank you.

Thank you David! This has been a concern of mine, and a comment for which I have been criticised.

It would be really great in future if there was as much discussion about what one should be doing with KiwiSaver as there is about when potential FHB should enter the property market. As individual KiiwSaver funds become significant in size, the implications for individuals is equally important.

I agree, on the basis of long historical performance, for a passive long term holder of a KiiwSaver a "growth" (care how that term is interpreted) tend to perform better than conservative or default funds.

However, as one's KiiwSaver becomes more significant in size, then people need to be more active in managing their fund.

This is not to say that one should try to be beating the market or reacting to short term events; events such as the markets reaction to the results of the Brexit vote and Trump's election as these were very much short term. However, there are significant events which can have long term implications which one needs to consider; examples of this includes what appears to be a consensus of a slow down in the global economy

- even John Key's comments today align with Winston's earlier comments :) :) - trade wars, tightening of QE, likely potential of rising interest rates etc.

A really great feature of KiwSaver compared to other managed funds, is that many providers allow transfer between different funds without a fee.

It is interesting looking at my KiwSaver fund (as I am 65+ and have a range of other investments) which I use as a vehicle as for exposure to the local and international share markets that the fund managers have actually greater proportion of funds invested with conservative options (e.g. cash vs equities) against targets, and more compared to targets in conservative Australasian markets compared to international equiites. So I guess that fund manager is currently also taking a more conservative view.

As a crypto-investor I am used to 30% overnight swings in my portfolio value. That being said I have moved by Kiwisaver to all global bonds & overseas cash.

If you start mandating anything other than the safest option for the default funds, do you take on some moral responsibility for the result?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.