The Reserve Bank (RBNZ) believes reimposing loan-to-value ratio (LVR) restrictions will sufficiently help maintain financial stability in the face of soaring house prices.

The central bank, in its latest biannual Financial Stability Report, said “recent growth in house prices increases the risk of a sharp correction in the medium term, if the current demand and supply imbalances quickly unwind”.

It noted that because residential mortgages account for 97% of loans to households, the banking system would be “vulnerable to large losses if many households became unable to service their debts, and the value of their residential properties were to fall significantly in a severe economic downturn”.

It said borrowers on mortgage deferral programmes, or recent homebuyers with high LVRs/buyers who had relatively small deposits, were particularly vulnerable.

Nonetheless, the RBNZ was comfortable financial stress among households had been “mitigated by a functioning labour market, the continued decline in mortgage rates, policy actions by the Government, including the wage subsidy, and the strength of the housing market”, which produces a wealth effect.

It didn’t see the need to further restrict bank lending against residential property beyond reimposing LVR restrictions in March 2021.

The RBNZ reiterated its intention to reimpose the same restrictions that were in place earlier this year. These require most owner-occupiers to have a 20% deposit and most investors to have a 30% deposit, with some exceptions allowed.

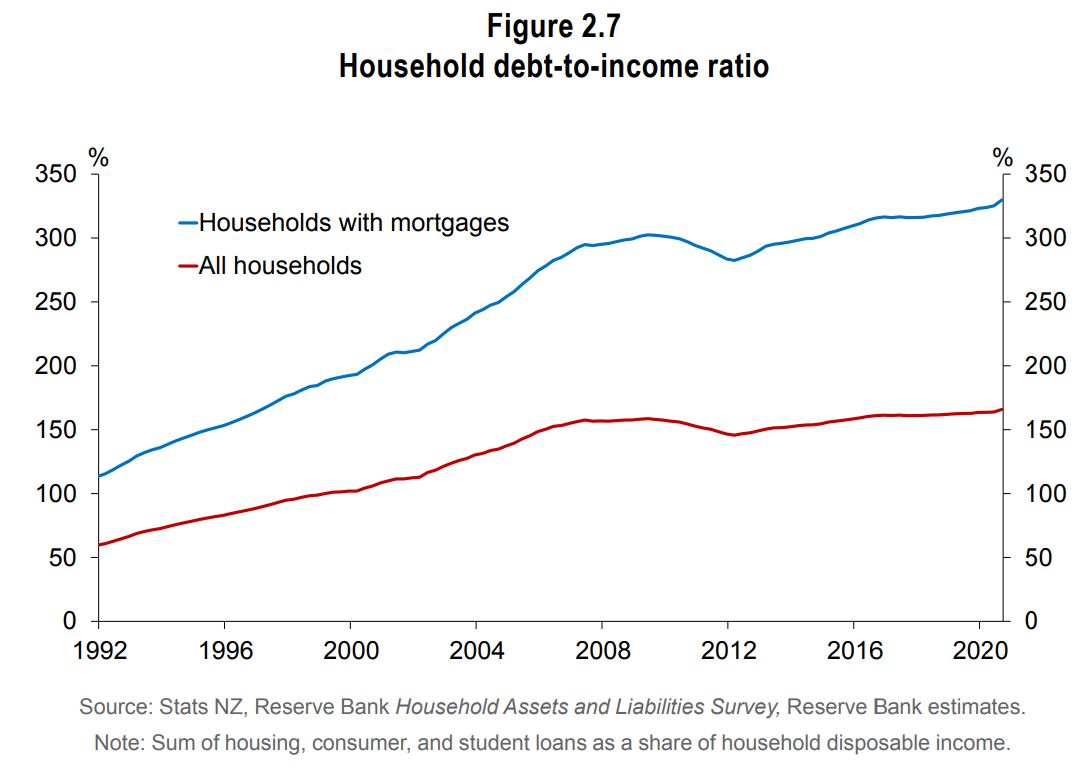

Yes, people are taking on more debt vs their incomes, but servicing debt has become cheaper

It recognised there had been an uptick in the portion of new mortgage lending to borrowers with high debt-to-income (DTI) ratios.

But it stopped short of asking Finance Minister Grant Robertson to add a DTI ratio tool to its macro-prudential toolkit.

RBNZ General Manager Financial Stability Geoff Bascand said the RBNZ remained “sympathetic” to having DTIs in its toolkit (it unsuccessfully asked for these in 2016). He said it would consider this in its discussions “next year”.

Bascand said DTI ratios had to be considered alongside debt servicing costs.

“If you think they’re [low interest rates] going to be there for a long time, then you can sustain a higher debt-to-income level. It’s a bit context-specific," he said.

Some economic observers maintain the RBNZ will respond to Robertson’s proposal for it to be made to consider house prices when setting monetary policy by targeting bank lending rather than changing tack on its mission to lower interest rates.

Robertson on Tuesday told interest.co.nz he was open to giving the RBNZ DTI tools should it want them.

The RBNZ will still be digesting Robertson’s request, having been given a heads up about it on Monday before receiving a letter on Tuesday.

It said in its Financial Stability Report: “The proportions of new mortgages originated to borrowers with high LVRs, and to those with debt-to-income (DTI) ratios of greater than five, have increased from a year ago. The proportion of lending to investors has also increased in recent months."

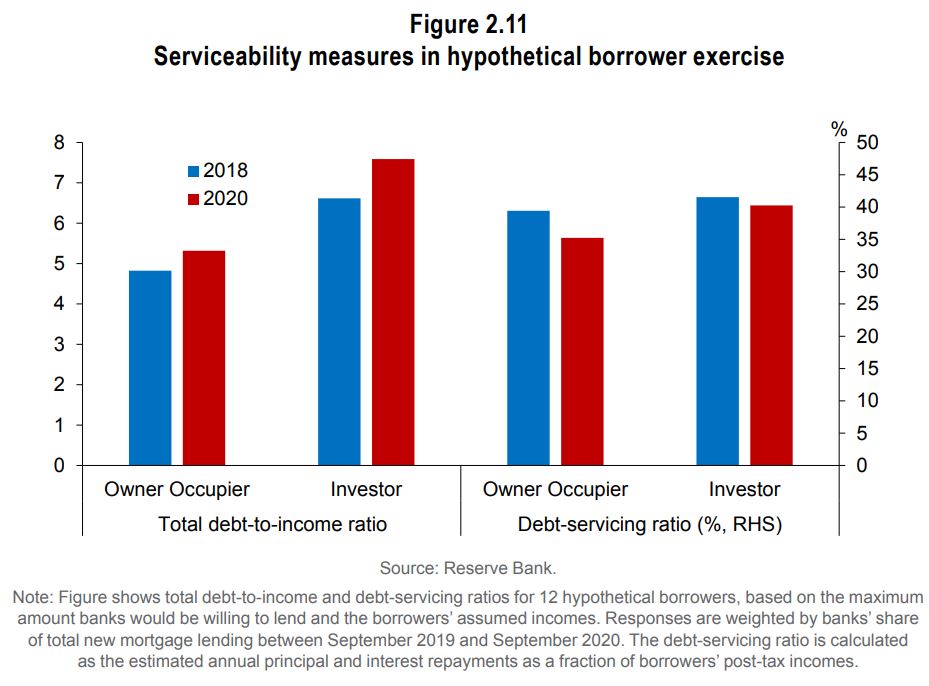

“The Reserve Bank recently completed a hypothetical mortgage borrower survey of mortgage lending banks. Results suggested that banks are willing to grant higher DTI loans to comparable borrowers than in 2018, with the average DTI for the stylised owner-occupier borrowers increasing from 4.8 to 5.3.

“Despite this, average debt servicing as a share of the borrowers’ incomes has fallen on average, from 39% to 35%, reflecting the decline in mortgage lending rates over the past two years.

“A lower debt-servicing ratio implies borrowers would have a higher capacity to absorb declines in income or increases in expenses, after making their loan repayments."

Focus on LVRs

“Until recently, some banks had increased maximum LVRs for investor lending from 70% to 80%, and there has been significant growth in lending to this category of borrowers," the RBNZ said.

“However, banks have been cautious in granting very high-LVR loans in the absence of Reserve Bank restrictions. And banks have reported that they have tightened serviceability thresholds for high-LVR loans to owner occupiers to maintain the flow of lending above 80% LVR at a relatively stable level.

“In part, this has been achieved by keeping the interest rates at which they assess borrower serviceability relatively high, with the average test servicing rate falling to 6.4% in September from 7% a year prior.

“While the share of high-LVR loans on banks’ balance sheets remains relatively modest for now, a material easing in standards for new lending could see risks increase over time."

Risks beyond housing

The RBNZ stressed New Zealand wasn't out of the Covid-19 woods yet.

"As government support schemes wind down and payment deferrals come to an end, banks are likely to see a deterioration in their loan books," it said.

The RBNZ also noted low interest rates globally are boosting equity prices.

"Strong asset prices have been beneficial for the global economic recovery so far, likely having a wealth effect on spending as well as feeding back to consumer and business confidence," the RBNZ said.

"However, in the presence of continued economic uncertainty – exemplified by a ‘wait and see’ approach to business investment – and a worsening health crisis with further lockdowns in some countries, elevated asset prices may mean that the risk of a correction is building.

"Price corrections in the markets for corporate debt, equities, and property could be precipitated by a phasing out of governments’ economic support programmes, or a prolonged development period for a COVID-19 vaccine.

"Under some adverse scenarios, a rise in corporate bankruptcies could add to the global economic headwinds, with spillovers from corporate balance sheets to broader economic and financial conditions amplified by high corporate debt levels."

120 Comments

"the strength of the housing market....produces a wealth effect".

This is simply trickle-down theory obfuscated. Noting a 'Wealth effect' is nothing more than hoping that, as home-owners bolt a larger ATM to their asset and commence withdrawals, it will bleed quickly enough and far enough out into the economy, to disguise the fact that it's actually increasing residential debt into Buzz Lightyear territory.

It might be face-saving (and Lord, what a face to save....) but the second- and third-order consequences are severe. But of course, far, far away from the RBNZ's immediate responsibility......

The strength of the housing market is the biggest driver of societal inequity (have vs have not), and cause of hidden inflation and govt financial misappropriation (WFF going to debt speculation/investor). In summary the root of all financial evil in NZ, right up there with the negative impacts of meth.

It looks like our whole society has been tricked into being slaves for the global debt owners. Investors are just proxying that risk onto a increasingly smaller and smaller group of kiwis. Sad.

Haha really? House price increases ≈ the negative impacts of meth?? Jesus, has interest.co.nz become an echo chamber for looney left wing activists only capable of single dimensional thinking? baa baa RBNZ bad :D

If you actually understood the negative social implications of runaway housing costs then you would realise that that statement isn’t too far off the mark.

He cannot put himself in other peoples shoes. Some conditions actually make it impossible to empathise with others. It might not be his fault?

Definitely, high housing prices are negative and cannot be allowed if we want to keep a healthy society. They are source of many health and social issues. Most left and even right wing activists are getting things totally right and seem to understand the issues that this causes, unlike what it seems from your comment.

Bring back Martin North and Mike Kirk to tell us it will be all OK and we are getting our price crash!!!!!

Agree Waymad, but I would add that it is disingenuous of Orr to try to distance himself from those second and third order consequences. These can be directly linked to actions of the RBNZ, even though they are not the only influence. Thus i think GRs mandate to be cognisant of the consequences of their actions is valid. However i do not think it will be enough to have much if any effect.

Yip its the arsonist firefighter who is telling everyone how well they are doing at putting out fires. They seem like a hero while you don't know the full story, but when you find out they've been lighting the fires, you understand they are not heroes at all - they are liars and hypocrites - the complete opposite of a hero - risking the safety and well being of others.

When deposit rates are low due to RBNZ , and other investments are less certain in the current environment, property seems a better and safer bet.

In March 2017, former Treasury and Federal Reserve (Fed) official, Peter R. Fisher, delivered a speech at the Grant’s Interest Rate Observer Spring Conference entitled Undoing Extraordinary Monetary Policy.

Wealth effect or wealth illusion?

The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax.

https://www.grantspub.com/files/presentations/FISHERGRANTSREMARKS15MAR1…

The family with savings likely ends up where they started

Unless the value of their savings is completely eroded due to hyperinflation. QE in every other instance in history has produced hyperinflation as people exit from the currency slowly then all at once. We're mad thinking that history doesn't apply to us and somehow this time around it's different.

If Bitcoin didn't exist then PM's would be the safe hedge against this as they have since time immemorial, in spite of their inherent problems with Portability, Auditability, Scarcity, Fees and Divisibility (all of which BTC solves). The financial sector is waking up to this slowly, but there's a time coming soon where they'll wake up all at once. The financial storm and fallout from this will likely be apocalyptic.

And remember - BTC > 20k by Dec 2020 - like clockwork.

Don't take my word for it. Listen to the very articulate and smart Lyn Alden. Winter isn't coming, it's here.

https://www.coindesk.com/lyn-alden-money-printing-bitcoin-80-year-debt-…

Don't take my word for it. Listen to the very articulate and smart Lyn Alden. Winter isn't coming, it's here.

Could have told you that quite some time ago, even without Lyn Alden. This shouldn't be a revelation.

You're already a BTC maximalist J.C. That podcast is for the Boomers.

5-Year, 5-Year Forward Inflation Expectation Rate from

* checks notes *

the Federal Reserve Bank of St. Louis.

"The Federal Reserve Bank of St. Louis is one of 12 regional Reserve Banks that, along with the Board of Governors in Washington, D.C., make up the United States' central bank."

I'll probably take their predictions on QE and related inflation with a grain of salt Audaxes. No doubt that's your point though?

No-its derived from market prices.

You need to email that to Grant and Adrian Audaxes.

Exactly the RBNZ is concerned for the banks.

The Banks.

Not the home owner

Not the borrower

Not the renter.

The Banks.

GR & Our Lady of the Lockdown need recognise some root cause analysis and possibly a mirror to their collective already 3 years of policy failure.

# activists make terrible governors

Fun fact. Some Wellington folk in the ranks are sick & tired of the Ardern Govt., this one & last, ignoring ministry advice and making policy statements to match shallow slogans.

Example 1: Energy policy.

Yep I'd have thought a wealth effect comes from having X dollars/week going into my savings account rather than to the bank to pay the mtg.

OK I came out earlier saying I think DTIs will come in by March, now it sounds like they may not. Wouldn't be surprised if more continual tinkering around the edges occurs but perhaps where things might change the most could be in relation to taxation of property. I would imagine inheritance tax will be a big one on the cards and removing interest deductibility. That'll be a game changer in terms of tax take but still don't think that'll stop investors. Fundamentally people always flock to bricks and mortar as a safe haven. I think this is the main motivation at the present time.

Inheritance tax won't make a difference to property prices though. What problem are you trying to solve?

Removal of interest deductability will just push up rents as well.

Not a word on effect on NZ market of QE of up to $128 billion

To put that in context, QE in UK in 2008-10 was about $500b and the pop of UK is 13 times higher than here.

QE is well known among economists to produce most gain and advantage to those closest to the spigot, ie those already holding substantial assets able to leverage.

UK has DTI ratio of 4.5 but of course canny old NZ does not need them, being on 9 already.

QE is government deficit spending in disguise. But as you say the "deficit spending" of old would have benefited certain group of working people with monopoly on their line of work and political power (unionised and with Mercantilist protection from political power) to some extent. while QE only rewards asset owning class, prevents or postpones the fall of small owners and impoverishes everyone else.

I'm not convinced DTIs help at this point (from a FHB perspective - perhaps to banking stability). Without addressing the demand from speculators, they seem to just have the same effect as LVRs have had - a massive barrier to entry for those not already in the market. The UK's DTIs seem to do just that - FHBs can't get banks to lend enough to them to buy at their massively inflated prices, which does not apply to buy to lets leveraging equity. There was some research quite recently (link is escaping me right now) that found that the growth in buy to lets from around 2005 or so in the UK had outpaced the growth in new housing stock in the same time, meaning they'd captured *all* of the gains in supply over that period.

mikekirk.. exactly. Massive QE in most developed nations and almost all of them have experience high house price inflation (as well as solid stock appreciation). Coincidence?

As Bernard Hickey has remarked, "This is what happens when you build an economy that is really just a housing market with bits tacked on and your banking system is all about lending to landlords and other home buyers."

LVRs requiring a 30% deposit by property investors won't accomplish much.

What is needed is a Government mandate that banks lend only to intending owner-occupiers for existing houses, and to other property investors only for new builds that increase the national housing stock.

Let the would-be landlords go cap in hand to the non-bank lenders.

I really do empathise with those struggling in the face of rapidly rising house prices (not withstanding this community has been largely bearish on property prices since I've been here). However, by blaming the RBNZ you are failing to get to grips with the issue. NZ is a small open export driven economy and we have undershot our inflation target for 10 straight years. Our monetary conditions are currently tighter than Australia and the UK for example.

IMO, the culprit in NZ is the tax environment, council red tape and cost of building supplies - none of which are an RBNZ issue.

I recommend reading up on the Dornbusch and Mundell curves and the relationship between the exchange rate, cost of money and the export sector.

In reality the money supply is “created by banks as a byproduct of often irresponsible lending”, as journalist Martin Wolf called it (Wolf, 2013). Thus the ability of capital adequacy ratios to rein in expansive bank credit behaviour is limited: imposing higher capital requirements on banks will not necessarily stop a boom-bust cycle and prevent the subsequent banking crisis, since even with higher capital requirements, banks could still continue to expand the money supply, thereby fuelling asset prices: Some of this newly created money can be used to increase bank capital (Werner, 2010). This was demonstrated during the 2008 financial crisis. [RBNZ suspended bank dividend payments, thus building bank capital buffers]

Money will flow where it get best returns.

Is this responsible RBNZ regulatory oversight?

Banks extending 60 % of their lending to one third of already wealthy households to speculate in the residential property market because the RBNZ offers them an RWA capital reduction incentive to do so.

{kind=link}

Or this?:

RBNZ cutting OCR in half five times since July 2008, causing the rich to capitalise rising discounted present values of future unproductive asset cash flows.

{kind=link}

The cause of our rapid rapidly rising house prices is not one thing or another, it's a perfect storm of a host of factors - accommodative monetary policy is certainly one of them, as is the willingness of banks to lend against property, as are the factors you mentioned. Culturally New Zealanders also favour property over investment classes, so that must be contended with.

I think it's fair for commentors here to knock the RBNZ for it's effect on house prices - the relationship between interest rates and house prices is well known, and the RBNZ is explicitly targeting house price inflation to achieve their mandate. I think it's unfair to solely target the RBNZ however, they are simply one cause in a sea of causes.

If the RBNZ had not cut rates as they have, the NZ$ would be a lot stronger and we would be hearing cry's from exporters. The RBNZ have blunt tools and are doing no more than any other central bank. It's not credible to say the RBNZ should not have cut in my view. Also, there is a pattern to house price rises - short periods of mania followed by long periods of no to little growth - it's not a straight line.

I don't think we should fully rely on a weak NZ$ to keep up our exports. As we are killing our productivity at the moment, the risk of high inflation for kiwis is near in future. By that time, we will have to force our interest rate up, then we are not only having a hard correction for housing price also a insufficient exports to keep everyone in jobs. This will risk our financial stability. Like I said before, the issue right now is not low interest or lvr restriction, it's the cheap debt caused by low interest rate not injecting into our productive sectors. This will get worse as RBNZ and our government keep promoting housing price will just go up.

Shouldn't tighter margins from higher production costs and lower commodity prices in NZD terms force exporters to invest more in either productivity enhancement, product innovation or both?

Contrary to your argument, a weakening NZD with stable commodity prices would simply allow our exporters to keep reaching for the low-hanging fruit (pun intended).

Sorry, I should've made it more clear. When I mentioned that "we are killing our productivity", I was referring to, cheap debt that created by RBNZ flowing into housing rather than be used in our productive sectors. This is killing our productivity. RBNZ and government's actions give people wrong indication that housing price will never fall, don't invest into other areas rather than houses.

Nonsense. NZD is on a tear. Mon policy has not benefitted exports because of their actions.

You left out immigration

Yes, also not part of the RBNZ's remit.

nigelh.. don't most people seem to leave out immigration even though it affects demand far more than anything.

No it doesn’t, credit availability does.

so where do all these extra people live?

When I started reading your comment I right away started looking for your "but", didn't take too long to find it though.

House price index shown on this article is very scary.....I'd be shitting myself if I were Orr or Robertson...but then again I guess this will just become someone else's problem down track when they've finished pumping the system with QE.

And in the red corner - Orr, Jacinda, Robertson, Judith, Key, Bindi, rich investors, elites, the greedy and in the Blue corner - homeless, poor, young, renters, divorced, disabled, newcomers. The Haves are determined to further ruin the Have-nots. I can now see that I have no other option but to leave the country I love because the ruling class hate my type and are determined to make my life as hard as they possibly can. And Jacinda wonders why kiwi mental health is at an all time low? She looks concerned but does not give a damn.

"Let them eat cake."

Yip - I agree. I think our property bubble has a lot to do with the anxiety and mental health issues of people in their 20's and 30's.

Had witnessed an eastern european crying at auction and husban was so helpless and frusrrated but could nothing as 900000 house that in high market should have gone fir 1.1 million maximum went for 1.395million.

And Mr Orr the GREAT RBNZ Governor.....patting himself fir agenda accomplished and by not acting now i stwad giving few months of mire opportunity to speculators to play and test mire highs as MR ORR STILL NOT SATISFIED ALONG WITH JA

You exist to be farmed. A bit like slavery. But you have to pay for your own food and accomodation.

It is a sad but true indictment.

Ardern pledges to care 9% more by 2030

https://thespinoff.co.nz/politics/24-11-2020/ardern-pledges-to-care-9-m…

"In her post-cabinet press conference, the prime minister would not be drawn on whether she would care passionately about child poverty but deeply about climate change, or the reverse. The adverb she would use to care about housing affordability was still being decided. “Intensely” and “strongly” are rumoured to be options and Ardern refused to rule them out, declaring, “I’m leaving every option on the table. I will choose a word ending in ly. That is my commitment to you.”

"Some economists and political commentators question whether these levels of care are sustainable, predicting that Ardern will risk straining her neck and run out of adorable children to do Facebook livestreams with long before she reaches her new goals, while others have suggested Ardern’s majority government should do actual things to reduce house prices and carbon emissions and improve the lives of children, a suggestion Ardern has dismissed as anti-caring."

Don't forget ''we got this ''

Grant has got it or

Adrian has got it or

The team of 5 million have got this,but don't worry

Somebodys got it.

It just ain;t me

Orr responses make no sense from the point of view of rational thought and are literally a poke in the eye.

His actions are comments are the same as the other central bankers across the world. Get the people into as much debt as possible for as long as possible. When the sh1t hits the fan those with big debts and high levels of household expenses will become desperate with few options. This is all part of their (IMF and WEF) plan.

As of 13/11. There are 3.9 bln worth of mortgages on full deferral. This number is ticking down.

12 Bln restructured to interest only. This number is ticking up.

11,155 missed mortgage payments with a total exposure of 2.3 bln and average of 210k. Also ticking up

Seems like people are being taken off full deferral and converted to IO. On the basis that the bank thinks they are capable of paying at least the interest based on their incomes. But those people can not adjust their spending to fit their new incomes and are missing mortgage payments. Probably consumer loan and credit card payments as well.

Going back to deferral should not be an option. So next comes gentle pressure from banks to sell. Hence the stimulus applied over the last 8 months to ensure that every property owners equity has been pumped in the meantime. Because the dump days will be coming and the banks need to at least try and break even.

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Statistics/tables/c6…

This is a very interesting comment.... thanks for the link.

"Strong asset prices have been beneficial for the global economic recovery so far, likely having a wealth effect on spending as well as feeding back to consumer and business confidence," the RBNZ said.

How is something being more expensive a good thing? Sure it may be for existing home owners. But for the economy as a whole this is not true. Things being more expensive is frankly not a good thing. The wealth effect is essentially a delusion. The actual wealth of an economy is based on the goods & services it produces there is no such thing as the wealth effect. If Mr Orr thinks that the money is any thing other than a means of exchange he is a muppet & should resign.

What a guy this Orr is. When returning kiwis come back home in good faith and bring their cash to buy a home, Orr pulls his levers and makes house prices 20% higher. This means that the returning kiwis cannot afford to buy anymore and decide that the only option is to move back to where they came from. So what does Orr do? He decides to lower the kiwi dollar so the people who now have to leave because he has made house prices too high, risk losing many thousands on the pathetic exchange rate? He is trying to trap returnees and force them to pay over the top prices for million dollar cardboard houses? He is fast becoming a Marvel bad guy.

Won't someone think of the poor overseas Kiwis

Is that the same poor overseas kiwis who left in the first place because the wages are so low in NZ and the house prices too high? Why should anyone care about those scumbags trying to better themselves when everything in NZ is stacked against them?

Did they care enough to maintain tax residency or did they expect everyone else to prop up the state in their absence?

Is there something on your shoulder there GV 27?

Of course, how silly of me. Yes, let's further tilt the playing field in favour of cashed-up Kiwis overseas, they're definitely the ones who are most deserving of our attention at this current juncture. Everything here is just tickety boo, after all. Let's rationalise all of our monetary policy on the basis of how we can best serve those who don't currently want to live here or pay tax here, but might some day.

Yip, cashed up me. Worked my guts out in oz as a carpenter. Saved 300k (cashed up????). Came back to buy in my home town of Gisborne. Was so excited. Prices rocketed as soon as I got off plane. Can't believe this has happened. Feel like NZ hates me. People like u hate me. Why bother staying?

If they left because wages are too low and house prices too high, why come back and cry about low wages and high house prices?

Perhaps because they saved enough to buy a house 3 months ago but the extra 20% rise in the months since they arrived back have made buying impossible?

Kiwi dollar is at a 2 year high

Its going the wrong way against the Ozzie today thanks to Orr. I am ready to pull the trigger and send my money back to Ozzie because NZ elites won't play fair. I am done here. I should have transferred it yesterday.

Compared just to the one currency that keeps going down, same as all other currencies which are pretty much at the same level with the NZD as before.

I think Robertson raised the dollar by sending a letter to the RBNZ. Seems unlikely they will lower rates further now (unless they want to really stress their independence).

This is the sad irony of the present system is that they see you as just another golden goose to be plucked.

And this is one of the reasons why overseas companies don't like investing in NZ.

It goes something like this:

NZ city promotes itself to entice companies as a great place to live, cheaper commercial property to set up a business, and cheap housing for new companies employees etc. And then by you making the investment, the vested interests will turn that against you with house price increases, getting the support from the existing community who benefit by getting a super profit based on your hard work.

Think of it as an Ambush.

See No intent and as is forced to act giving window of opportunity to all his friends and well wishers to go for a kill as much as in four months, result will be rising high price.

No urgency as for him higher the price better for him.

Let's say Peter has a modest investment portfolio worth $1 Million at the end of 2019, he had 80% LVR, so he owed $800k, today his portfolio is worth $1.2 Million and he stil owes $800k, his LVR has now dropped to 66% below the 30% lending limit…

LVR's are not good tools in a rising market

Let's say Karen and Irene are first home buyers and just bought a modest Auckland home. They've scraped together 10% deposit with their parents help on a $1M 3 bedroom house far in the burbs. Out of nowhere (but entirely predictable given the developed world debt mountain) there's an external debt related shock. Suddenly the NZ banks and government are unable to roll over debt as liquidity has started to dry up and NZ is seen as risky given our ridiculous amount of private debt (and growing public debt). The reserve bank try to print their way out of it but this leads the NZ$ to fall quickly to 50c against the USD. Suddenly oil goes to to $2.50 and all imported good rise by 25%. The reserve raises interest rates to dampen the fast rising inflation shock that has flowed through to many imported goods and to stabilise the currency while banks tighten credit. Sally and Irene's house is suddenly worth $800k and their deposit / equity is suddenly negative $100k. Sally loses her job at the bank as banks profits start to take a hit and they begin cutting costs. Irene's income isn't enough to pay the mortgage and the bank calls in their loan and they are forced into a mortgagee sale. The bank sells the house for $750k and Sally and Irene still owe the bank $150k but have to declare bankruptcy. The bank has many bad debts and have to raise more capital as they fail stress tests as their loan book is marked to market.

Depositors start to withdraw funds from the banks and wholesale lenders refuse to roll over debt funding. The banks closes and the RBNZ invokes the OBR. Remaining depositors get 10% of their deposits back when the bank reopens after the RBNZ has audited their capital adequacy against their remaining loans. Consumers affected by this, stop spending money as they have lost 90% of their savings. Credit is impossible to get from banks as they concentrate on shoring up their existing loans. Economic depression pervades.

It'll never happen right. NZ house prices only go up.

Great - post and yes agree that this could be a very real outcome. Its very similar to what I witnessed living in the US during the GFC. If people want to know what hell looks like, we'll lets keep pumping this bubble.

Are borrowers falsifying loan applications or borrowing 110% of the home value, does NZ have a surplus of houses?

I would add that if you were a reader of this site and delayed buying a house - you are in hell right now.

Nice troll!

And yes I think we're on the way to hell, property investors being the devil :-p

were they in Ireland before their last housing bust?

Ptoleny, you forgot to mention that Karen is going to get lung cancer and that Irene will have a terrible car crash leaving her disabled for the rest of her life… Sooo let's not live now, because something bad could happen in the future, that's your life philosophy right?

Funny you should get that from my post. I was just telling a story of a possible outcome of the current housing bubble (and it is a bubble by any common definition). You may be interested to know that I have just bought another rental property but probably not for the reasons you would expect. I don't expect house prices to rise much past the middle of next year, probably the opposite. I do however think there is a pretty good chance of a banking crisis at some stage in the next decade and I want to have less money exposed to the banking sector. I am also slowly selling down shares as they look ridiculously overvalued. Managing risks at the moment is more about where am I least likely to lose a lot. Property even it goes backward 10-20% will still give me a positive cashflow.

But the crash, the crash, the crash! When will the looney lefties on here finally concede they should have just bought property like the rest of us and stopped obsessing over bubbles.

Let's say Peter can find a proper job and be a productive citizen instead of a parasite just because he has the equity to do so.

Peter, like the vast majority of mum & pop investors does have a "proper job", your hatred makes you blind, people with jobs and investors are not different people, they are the same people.

"The wealth effect will protect us from the risks of the rising wealth effect"

Que?

He's an economic genius...

Surely the big risk is actually inflation. If we get significant inflation from the extreme amount of money flowing around, Orr would have to increase interest rates and possibly quite quickly if its hyper inflation. If he does that the banking sector is toast. Is Orr confident that the settings in place won't lead to inflation or even hyper inflation? Are the small advantages of even lower interest rates worth that risk?

I’d say central bankers were far more worried about deflation.

I’m sure they are. But inflation has to be a significant risk. economics 101 would tell you that very low interest rates and money printing will cause inflation. Are we so sure that is wrong now? I don’t think they can be sure of anything anymore.

Given how slow they've been to react to house price issues, do we trust them to react in a timely way if inflation suddenly takes off from under us?

The answer is simply that he wouldn't raise rates. Running inflation over and above debt servicing costs is the least resistance form of dealing with the debt burden.

Central banks have been trying to generate inflation and struggling. (Of course the only methods they try are those that involve giving money to banks or pumping it into markets, rather than helicopter money or wage increases.)

The rational markets hypothesis is being proven wrong again. It turns out that a country can print money/debt in whatever quantity they want (cf. Japan) as long as there is psychological confidence. Zimbabwe and Argentina still get hammered, of course... It seems that fear of inflation (which begets actual inflation) is more about political stability/instability than how much money a central bank is printing.

You can print if you're trading partners print (and the US as reserve currency). Argentina's mistake was to issue US$ denominated debt - that is the single biggest trap.

So why not print us all $1 billion each if it doesn’t cause inflation. We could be the richest country in the world.

It appears to be more deflationary - see Japan...Europe...perhaps soon to be the Anglosphere....

Why the hell is he waiting till March ?

On an agenda to screw as much as before been forced to act.

While removing LVR it took a day to decide so.............

I'm assuming its because mortgage pre-approvals typically last for 3 months.

Like ASB bank, you could exclude current pre-approval- any new pre-approval must be assessed at new LVR.

Why were LVR's removed again?

Because Orr is incompetent

Both are incompetent, but a large majority of NZ voted in October and are now crying in November.

I guess because almost the whole country were predicting economic Armageddon and house price collapse due to Covid (including 99.9% of commentators on this site). Personally I was surprised by how bad some of the economic predictions from the likes of treasury were. They seemed possible but not the most likely scenario.

You could argue that the cost of rent is closely linked to house price inflation. It encourages both FHBs (who would pay less for a mortgage than for rent) and investors(seeking high returns from high rent) into the market thus creating a higher demand for property. Rent freeze for ten years would also help FHBs to save a deposit more easily, keep many investors out of the market and save Govt money on accommodation supplement.

Can't see any major downside unless you are a greedy speculator.

Adrian Orr: zero fucks given

Adrian "Honey Badger" Orr

hahaha that's right..."Adrian Orr don't care, Adrian Orr doesn't given a shit. He just takes what he wants..."

Crazy nastyass

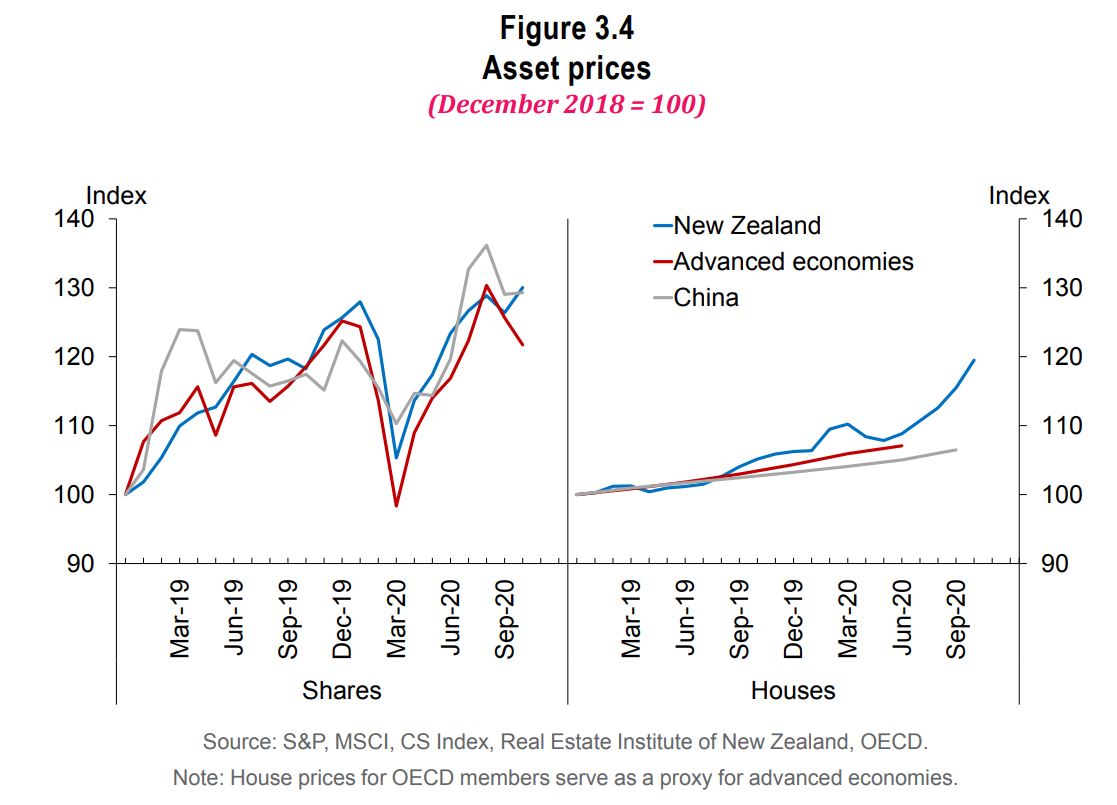

Fig 3.4

Mr Orr, please describe what you see in this chart.

Sure as heck glad to say I didn't vote Labour.

Transformation and reducing inequality my ass!!!!

ABSURD.

Orr should be sacked. The LVR restrictions should have never been removed.

Figure 2.10 clearly indicates investors are the main driving force.

Absurd, yes.

Kafkaesque.

Short memory. Are you saying you didn’t predict a house price collapse at that time?

Orr just doesn't get it, he doesn't want to get it, he just hides behind his "remit". There's plenty he could consider like DTI, excluding the FLP form housing, including housing in the CPI… His claim that low interest rates don't drive the housing market up is absolute rubbish!

He thinks peiple can be fooled all the time either he is..... OR...........

Not allowed to swear

They can't really introduce a DTI, because they are already too late to do so. The DTI would prevent far too many people buying.

They are always too late. Stopping overseas buyers was too late, as he damage had already been done. They are reactionary instead of being proactive. NZers pay for it, and there is much greed going on.

I have recently seen a pretty ugly 60's house initially on the market a few month ago , and they were asking nearly a mill for it. It didn't sell and now every few weeks it is dropping in price by 100k. Now down to offers over 700k. GV under 500k Although who is going to offer more than the minimum offer price?

Are RBNZ still pushing ahead with their cheap (tax payer subsidized) loans to banks which in turn will be lent to punters on the property market ?

I nearly threw up watching the TVNZ news tonight. Orr was on there saying that the NZ economy was doing better than anywhere else on earth and went on to imply it was due to his shrewd idea to move the interest rates to near zero. In fact it is due to Covid not being present here in any significant way - which in no way was due to the efforts of the reserve bank.

The RBNZ looked better media trained today and looking to make statements that would hit the news. Orr also looked alot calmer than the last conference.

Perhaps RBNZ policies are being auto-piloted by the BIS along with all the other central banks. The path to "zero" or negative rates and the ultimate destruction that will eventually cause is a question of ethics for Adrian Orr. Is there nothing he can do, or nothing he wants to do to change the outcome for the better??

All we can do in the meantime is watch his necktie-knot get ever bigger.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.