By David Hargreaves

A growing belief that an expected reduction in official interest rates next week will be the last for some time has been reinforced by results of the Reserve Bank's latest New Zealand Survey of Expectations.

The survey is a nationwide quarterly survey of business managers and professionals. The Nielsen Company conducts the survey on behalf of the Reserve Bank. Respondents are asked for their expectations of future outcomes of a range of key macroeconomic data.

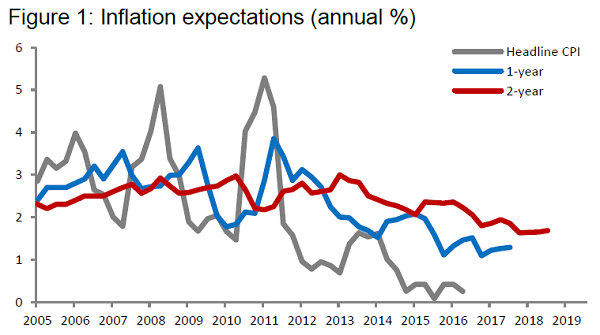

The key finding - and one that the RBNZ pays a great deal of attention to - is the expectation of the level of inflation two years into the future.

In the latest survey the expected rate of inflation in two years time has edged up to 1.68% from 1.65% in the last survey.

It's not a big rise, and it is still a figure well below the explicit target of achieving 2% inflation that the central bank has.

It is a rise, however.

Earlier this year, in February, a sharp fall in the two-year expected inflation rate from 1.85% to just 1.63% caused a good deal of commotion and appeared to be the single biggest factor in the RBNZ coming back to the table with more interest rate cuts when it had earlier strongly indicated to the market that there would be no more.

The RBNZ has broadly indicated that it will cut interest rates, through the Official Cash Rate, again at its next review next week (November 10). But the latest inflation expectation result adds to a growing sense that this reduction, to an expected new historic low of 1.75%, may well this time be the last.

The RBNZ's concern if inflation expectations settle at low levels is that these expectations then feed into future pricing behaviour. So, low inflation expectations have the prospect of becoming a self-fulfilling prophecy of stagnating and possibly even falling prices - the dreaded deflation.

The survey showed one-year-ahead inflation expectations have increased to 1.29% from 1.26%. The median also increased to 1.40% from 1.28%. The two-year-ahead expectations remained steady with a 0.03 percentage point increase to 1.68% while the median increased to 1.90% from 1.70%.

The changing mood in the marketplace in respect to expectations of future interest rate falls has been demonstrated by Kiwibank economists who have just altered their call. Previously they expected a rate cut next week and another in February. Now they expect next week's cut to be the last.

"..We now expect the [Reserve] Bank to remain on hold for an extended period," they said

"At next week's November Monetary Policy Statement (MPS) we still expect the Bank to cut the OCR by 25bps and to leave themselves the option of further reducing the OCR in 2017 if needed.

"The Bank is likely to change the September OCR Review commentary around 'further easing will be required' to 'further easing may be required'.

"While we have officially changed our central outlook for the OCR, we note that there remain several risks that could bring the RBNZ back to the easing table in coming months; including the US election outcome on November 8, the market reaction if/when the US Federal Reserve lifts interest rates in December, the path of the NZ TWI, and whether or not international price pressures continue to rise," the economists said.

ASB economist Kim Mundy, noting that headline inflation has been below the target band of 1-3% since December 2014, said the RBNZ had been concerned that ongoing weakness in headline inflation would begin to drag inflation expectations lower.

"However, today’s slight improvement will be a relief to the RBNZ, especially combined with the fact that the inflation outlook is getting a little brighter. Petrol prices have risen off recent lows and capacity constraints in the construction sector are pushing up domestic inflation.

"We do not think today’s result will have changed the RBNZ’s near-term interest rate outlook. Inflation expectations remain low and as a result, we continue to expect the RBNZ to cut the OCR to 1.75% next week.

"However, the fact that inflation expectations have steadied, combined with signs that inflation bottomed out in Q3, suggests the RBNZ is unlikely to feel any additional pressure to cut the OCR below 1.75% at this point in time," Mundy said.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.