By Gareth Vaughan

New Zealand needs to deal with the "500 pound gorilla" of housing through a comprehensive capital gains tax among other things, if household savings are to be meaningfully boosted, ANZ New Zealand chief economist Cameron Bagrie says.

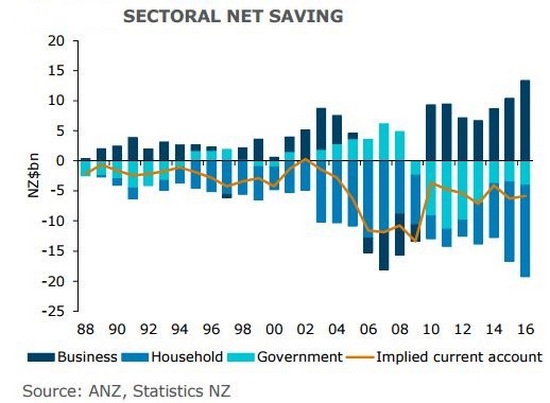

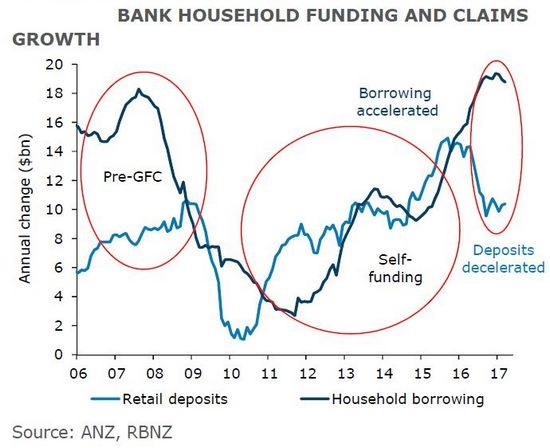

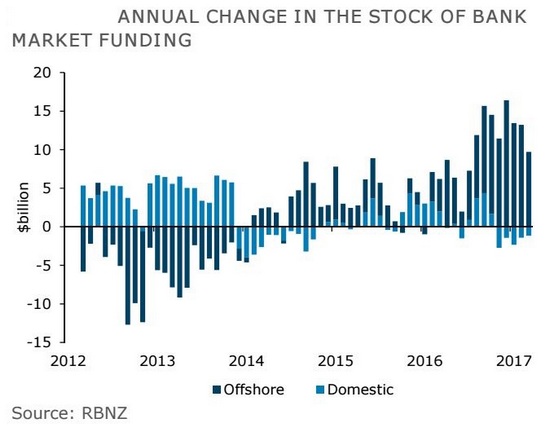

In their last two weekly New Zealand Market Focus reports ANZ's economists have highlighted a need for domestic savings growth to help fund the country's investment needs. This has seen them describe savings as the missing link from the Budget, and note that, on the evidence of the Reserve Bank's Financial Stability Report, the reliance on offshore funding by banks, given a significant gap between domestic debt and deposit growth, is coming under greater regulatory attention and scrutiny.

A key point Bagrie and his team are making is that if domestic savings is to increase significantly, more proactive savings policies will be needed. This, the ANZ economists say, will require "the finger to be pointed at the playing field between housing versus the rest."

"How New Zealand funds its future gargantuan investment needs remains at the forefront of our minds. Our previous modus operandi of back filling a domestic saving shortfall with offshore borrowing, and running a large current account deficit, is facing far more challenges in the current regulatory and global environment, which is all the more pertinent given a massive pipeline of investment needs," says Bagrie.

"It’s a basic accounting identity that investment needs savings, and the local pool is insufficient. The offshore tap can still be turned on, of course, but we just can’t be as dependent on it as we have been historically. Heavily indebted countries are under a brighter spotlight. We can run a current account deficit up to 4% or 4½% of GDP from today’s 2.7% level, so this lever can be pulled to a degree. But anything beyond that will see the stock of net external debt lifting as a share of GDP, drawing negative attention," Bagrie says.

'We've typically wanted to have our cake and eat it too'

Bagrie told interest.co.nz that whilst banks reining in offshore funding and starting to "swing the pendulum" away from borrowers towards depositors through higher interest rates is "jolly good stuff," people need to connect the dots and look at the downstream implications. If we're not funding our investment requirements for the likes of housing, roads, hotels to meet tourism demand, and broader infrastructure needs, through overseas money so much, then domestic savings rates need to increase.

"If domestic savings goes up then you have got to forsake consumption, which has not been within New Zealand's DNA. We've typically wanted to have our cake and eat it too," says Bagrie.

"I'd like to see more of the debate brought to the forefront because I think it's a big significant issue in the next two to three years," he adds.

"I don't think people have thought through what the natural consequences are of what is going on, what they mean in practice. We're going to borrow less money overseas because that seems like the right thing to do. [It] reduces the point of vulnerability. We give ourselves a little pat on the back and say 'we're going to do that.' But what does that actually mean? Because those offshore savings will be used to prop up domestic savings to meet our domestic needs. Where's plan B? Or what does Plan B, C, D or E even look like?"

"We've got to pull more levers and the big 500 pound gorilla here is the housing market versus everybody else. It's the untouchable one," says Bagrie.

'It's all a bit like eating broccoli. You don't like it but it's good for you'

That said, he argues there's more maturity among New Zealanders now than there was five or 10 years ago, noting that we're now talking about raising the retirement age.

"We're starting to think about the hard decisions that just need to be made. It's all a bit like eating broccoli. You don't like it but it's good for you," says Bagrie.

"You've got to look at ring fencing [tax losses on rental properties so they can't be offset against other income]. [And] I think the lack of a full blown capital gains tax is a weakness of our tax system."

"if we roll into 2018 and we're not tapping offshore funding markets, where's the money going to come from for that big investment pipeline? The corporate sector is generating cashflow, [and] the government sector's going from the red into the black. Where we've got a glaring savings deficiency across New Zealand is in the household sector. And it's blatantly obvious that the house is a big part of that reason," says Bagrie.

"The last thing we want across this economy at the moment is for the investment line to start nudging lower. We've got to keep that investment line up which means we've got to have a well articulated plan, strategy in regard to how we're going to drive more savings."

Household savings rate negative

The most recent Reserve Bank data shows a household saving rate of -0.7%, or -$876 million, in 2015. Meanwhile, the household debt-to-disposable-income ratio is now at a record high of 167%.

The International Monetary Fund recently suggested the Government ought to make changes so that the ring-fencing of tax losses on housing investments could only be applied against housing income and not all income.

"The incentives for buying real estate increase when real estate investors can write off interest payments against their other taxable income," the IMF says. "This ‘negative gearing’ encourages investment that would otherwise be loss making, and thereby acts as an amplifier of price movements in the real estate market. Ring-fencing housing losses to within real estate earnings would therefore weaken an important price driver."

Through its 2015 Budget the Government introduced a so-called bright line test to tax gains from residential property investments sold within two years of purchase. In addition to this capital gains can be taxed in specific cases, as detailed by EY's Aaron Quintal here. However, calls for the introduction of a comprehensive capital gains tax continue from others aside from Bagrie, including from interest.co.nz contributor Terry Baucher here.

Seven ways to boost household savings

Bagrie and his colleagues have listed seven potential ways New Zealand's household savings could be improved.

1. Stronger income growth. This is the obvious fix. But it is easier said than done, of course. A decent terms of trade outlook certainly helps, but the productivity story is not signalling much in the way of prospects for a decent lift in real wage growth. Education needs to be more of a focal point, but the pay-offs there are of the long-term variety.

2. Households lift saving of their own accord. That is possible, but arguably unlikely based on historical experience. The tendency remains to ‘save’ via the house.

3. More money is put in the back pocket. Tax cuts (driving more incentive to work and get ahead) or additional welfare payments could help, but we have to be mindful that sometimes this is just redistributing income, not creating it. You need to drive the right behaviours, which is why using tax policy is favoured. But if it just means an equivalent drop in government saving, then it won’t lift aggregate saving.

4. Well-targeted social investment. Improved prospects for the vulnerable mean the same for incomes, and higher incomes lift the ability to save. Some levers are being pulled but this is a multi-decade long investment.

5. Make it cheaper to live. New Zealand is not a cheap place to live, particularly housing-wise. The weekly wage gets whittled away pretty quickly. Construction costs are a problem. Local authority rates move up faster than inflation. Thankfully the electricity sector is functioning a lot better than it once was.

6. Interest rates rise. That is already happening given the funding pressures banks face, but if domestic saving doesn’t lift enough to meet our investment needs, then interest rates will need to keep rising until they do. That’s bad for the investment side of the equation.

7. There is a more proactive push on the policy front. This is something that we think is increasingly going to be necessary to drive the desired outcomes. And without getting into details, it is going to require the playing field between housing and other investments to even up. We have the new bright-line test but that doesn’t go far enough. Some tough, but necessary, discussions are in store.

*This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

78 Comments

Try measuring the debt to income ratio of just those with debt - but be seated first !!

That is the only relevant ratio - those without debt pose no risk to themselves or the banks. A classic case of the dangers of using averages.

I suspect there's a lot of mortgage fraud. Easy to conceal or exit the position when house prices are climbing. Not so easy when things are flat or falling. We're going to see what's been really going on over the next few years.

it’s a basic accounting identity that investment needs savings". Not quite. Using savings is an historical notion ( pre the end of the gold standard). What investment needs, is...funding. Funds, can be created at will by Government issuers. They do however need repaying or rolling over ( as we all do at the moment) and that just shift the burden of repayment onto future generations. But savings? Not needed as such.

He also doesn't clarify what this so called "investment" is for ... presumably to pour more concrete for the population/financial Ponzi.

"Both debt and equity are “pay you back later” systems. They depend on energy supplies actually being available, so that goods and services can actually be made, so that we can in fact, pay back the debt later.

Because of diminishing returns with respect to energy extraction, it takes more and more future promises, to obtain a unit of today’s energy. Thus, we need an increasing amount of debt, just to stay even with respect to energy extraction. We end up with a Ponzi Scheme, of ever rising debt. Then someone decides to raise interest rates, and the whole thing tends to fall over."

There was a great program on Aljazeera this week called "The debt machine" it was well worth a watch to see whats happened since the gold standard ended.

I think this is the one you are referring to if anyone wants the link

http://www.aljazeera.com/programmes/specialseries/2017/05/debt-machine-…

... Cameron : If a CGT is the answer , then the question is wrong ... seriously ridiculously wrong ...

We need a land-tax ... an across the board annual tax on the unimproved value of all land in this country .... simple , cheap to apply , impossible to avoid ... plus taxes on all of the nation's natural resources ... air and water included ... user pays !

... and perhaps , we need to look at the universal income ... follow Gareth Morgan's lead on guaranteeing an income for every citizen over 18 years old ...

I agree; a land tax is simple and easy. Also, a UBI would remove the colossally stupid way that being on the dole disincentivises working.

If I have a guaranteed income, then I don't have to do anything. I don't need to work, buy a house, save for retirement, pay off debt, buy insurance. I thought we were talking about raising the retirement age, clearly you are talking about lowering it right down to 18. Bravo!

If too many people are pushed out of the workforce it will not be something to argue the toss over, it will be pretty much necessary. And no, people in general would not tend to sit around doing nothing, they would get into other pursuits, that might otherwise not render a living income, mostly creative as that will be the one truly unique thing machines will not be able to replicate. We will be looking at a completely different world, come that day.

HAH most unemployed people will sit around drinking booze and smoking pot. It's already happening in Northland. It's a different world alright!

Only the pensioners in Northland are dopeheads? I mean, seeing as the superannuation is universal to the whole country, I would imagine that their would doped up oldies throughout.

Many places already have a land tax, and it is called rates. Infact many councils rate just on the land value, while some backwards councils have moved from that to rating on captial value, which is actually more of a wealth tax. But this creates distortions and means that many who have invested in creating a nice large home end up paying significantly more, for the identical services. So really councils should move back to rating on land value, and this means that land banking developers also have to pay full rates on their undeveloped land, as they pay the same amount as someone with a house on their land.

I'm not a great fan of UBI, it still has to be paid for

http://www.oftwominds.com/blogapr17/idea-bankruptcy4-17.html

When you talk about a UBI you are talking a whole another world and system in place, you are talking a time when there may not be much of a choice due to robotics and mechanization. The answer to how it is afforded will come from either taxing the machinery or re-thinking how it is owned.

There is little point thinking about a UBI with today's systems.

The funding isn't the issue, it's implementing the options that would be difficult.

100% tax on capital gains. 100% tax over and above a certain wealth cap. A pollution tax. A greed tax.

Not saying I agree totally with a UBI but our current model is clearly not working. A UBI to me is just another band aid and doesn't solve the cause.

You could consider a UBI a way of implementing the social contract if private business doesn't provide enough employment and the state cannot or will not provide sufficient employment. Otherwise, the social contract is perceived as broken and that provides a breeding ground for disenfranchisement, crime, extremism, etc. A UBI may in effect partly be a payment to citizens to keep the peace.

The big issue I can see is that whichever countries first implement this on a large scale, they are going to have to tighten their immigration policies up. There will for sure be a huge surge in immigration, even if there is a multi-year stand-down period for new residents before receiving a UBI.

A land value tax - it's all too simple - all too fair - and all too unavoidable.

The undisputed, most economically efficient tax around - and the best part about it is, if we got really serious on it we could dispense with taxing labour.

What would accountants do for a living, eh?

I agree with a land tax

UI is tricky I think, it's a very nice idea but basically, it states that Joe who gets out of bed early and works all day has to pay for Pete who sleeps in and watches TV all day

I agree I think we should be drug testing pensioners. Drinking booze and smoking weed is sapping their motivation. I shouldn't be paying taxes so they just sit there staring out the window all day.

My understanding of the Big Kahuna UBI proposal was something along the lines of a 25% flat tax rate - where the first $50,000 of income was untaxed (equivalent to a UBI at $12,500 pa).

In other words, the UBI was not a substitute for working, just a safety net when not working but not at the level of super and/or other present welfare benefits.

1, 5, and 6 is all it takes.

Pay people more, drop their costs, and reward them when they save.

Wanting to implement a capital gains tax/land tax is all well and good, but it ignores the high-vis wearing elephant in the room; the toxic love affair New Zealanders have with residential property. Seriously. "Hurr durr, owning investment properties is the only way to make money. I don't buy shares or start a business because they're risky. You never lose with property. I don't care I have millions in debt. I'll never lose!" The sheer blindness and stupidity in regard to other investment vehicles and the lack of financial literacy in NZ is staggering. Simple and straightforward education on financial topics like investing, shares, debt, interest rates, OBRs etc are needed for school leavers, uni students and the general public. You could start with the muppets who harp on about 1987 as the reason they don't buy shares.

Well, yeah...it's either more Kiwis share a little bit of pain or we continue to shovel it all onto the young and upcoming generations, sacrificing them for the benefit of primarily boomers and Gen X.

Splitting the tax burden across land and income (instead of almost all on income) would rebalance things a bit, making land more accessible for many as it did in NZ's past by removing some of the motivation to land bank and speculate.

... also , the Rich-Listers have highly paid super clever accountants and tax avoidance strategists ...

In the end , as well meaning as the CGT may be , it'll fall most heavily upon small investors , Mom & Pop businesses , small landlords ...

.. the high rollers won't stump up a single penny ... as usual ...

There is a lot of talk about "Mom & Pop investors" being hurt. Basically claptrap. There is no need for Mom & Pop investors to get what is effectively a taxpayer subsidy.

If they faced a level playing field whereby no investment class was artificially advantaged over others, they would make their investment decisions on the rational grounds of what provided the best return, not what provided the greatest tax shelter.

Yeah, when I use the term "mom & pop investors" it's only ever facetiously, in recognition of the fact it's a farcical term that's roughly equivalent "won't somebody please think of the children!"

Employed by politicians of recent times when making excuses to do nothing, natch.

Well my Muppet Dad lost a large slice of his redundancy cos he took "professional" advice and invested in a managed fund that went West in 1987. He is now in his eighties has a smallish share portfolio that he holds directly. Yes he lost confidence, why shouldn't he.

But Russell - haven't you noticed how much 'professional' advice has been in circulation in this country for property investment the last 10 years - what average joe misses is that the pro's are closer to con men than professionals. So what's worse, '87 or now?

From what I have witnessed these days, people don't want their cake and eat it too, they want to eat their cake and then start eating everyone else's cake as well. The world is turning into an "It's all about me" place to live in.

Agreed. Sounds like a good number of housing investors.

"Ahh, give me some cap gains, double serving please, along with rental yield, and a double shot of tax writeoffs, with a generous drizzle of accommodation supplements."

Ironically it's ANZ that's been the single largest investment loan provider, and a significant enabler in this gluttony.

HERE WE GO AGAIN !!!!!!!!!

Who is going to supply housing rental stock if you discourage private investment through a new tax ?

The Government ( which cant do it) or Housing New Zealand which cannot cope with the backlog right now and is a drain on the taxpayer ?

Hobosn's Choice if you ask me

Capital Gains tax is a resentment tax and has never brought house prices down , ask our Aussie relatives if it worked there

... yes ... CGT is a massive disincentive to improve the value of anything ... land ... businesses ... houses ...

Whereas a land-tax , greatly incentivizes the better use of land , and discourages land-banking ... easy choice , if you ask me ...

... this CGT which Bagrie & others keep trotting out , is absolutely bonkers !

..I'd agree. The horse has bolted as the gains are all in (unless it were backdated to purchase date). Where has this guy been over the last 10 years.... and why has he only just woken up?

These guys have been fluffing around in denial for years. They need to do what the cannabis party have done...accept that TOP has already got the answer and get on with it.

..I'd agree. The horse has bolted as the gains are all in (unless it were backdated to purchase date). Where has this guy been over the last 10 years.... and why has he only just woken up?

Where's he been? Behind a desk at a bank. There are limitations on what is deemed relevant to his employee's interests.

Improving the "value" of anything or increasing the price of everything? It's only an issue if capital gain is the objective. What if we had a different MO?

Is capital gain not a form of income? Why not tax it under existing income tax rules? If anything, capital gains should be taxed at a higher rate as they don't arise from the effort of one's own labour but from a multitude of avenues outside the single individual.

Any and all cost get factored into any investment decision. If CGT is brought in ( it really is just tidying up the current practice of avoiding Income Tax ) it will too. If after all the sums are done, it makes no other sense than to take a punt on capital gains ( as many do today), that will still happen. Adding a cost won't change behaviour much ( your Aussie anecdote).

Anything that discourages property speculation will decrease house prices and mean that more people will be able to afford their own homes. Property speculation is mal-investment detrimental to the economy as capital is diverted from genuine business growth opportunities.

Other countries deal with capital gains tax and don't seem to have an issue with it. I think more people just look at the loss of their tax benefits and have an issue. Investors and developers would just incorporate the tax into the calculations. The ones that get hit are the speculators that aren't focusing on generating taxable income.

"Who is going to supply housing rental stock if you discourage private investment through a new tax ?"

Your assertion is absurd. Both Australia and the US have CGT and somehow they also have a healthy rental market.

"Capital Gains tax is a resentment tax and has never brought house prices down..." No, it's a fairness tax. I get taxed on interest, stocks sales, dividends and (my favorite) unrealized gains on Mutual Funds overseas. The only way that CGT is a resentment tax is that property investors resent paying their fair share.

Actually, Boatman, when it comes to addressing the mess we now find ourselves in viz a viz housing, the ONLY way it can be sorted is by government involvement, the private sector has no interest whatsoever in providing affordable housing.

And it's getting people back into home ownership that is the goal NOT more landlords and rented housing unless we are prepared to look at a complete gutting of our tenancy laws and creating something more akin to Germany's and other countries where renting, probably for life, is the norm. Our tenancy laws are completely unfit for purpose for lifetime renters, they evolved in a time when people rented for a few years between starting work and getting married and starting a family, and little else.

Two things. yep. Increase New Zealanders incomes. Which strangely has not seemed a government priority. And yep. Decrease living costs. New Zealanders are not wise consumers and accept too much of the overpriced non service we get. Government accordingly does not make much (any?) effort to protect citizens from the rorts that extract cash out over our border. (Banks, etc etc)

How do you increase people's incomes? Also that will only push houses prices higher, as it will mean people can afford to borrow more. Increasing interest rates will bring down house prices.

Wellington agrees that there's a housing crisis and is trying to encourage development. As compared to Auckland Council that just wants to increase rates on hotels to put them out of business.

http://www.stuff.co.nz/business/93410105/council-asks-developers-to-con…

If rental costs actually came down people would have more money to save.

I see nothing wrong with chucking a dollar or two on top of each paid night's accommodation, but charging a blanket rate increase regardless of occupancy seems to make little sense.

My view Rick is that the tourism industry is doing a new version of privatising the income but socialising the costs. Including the non monetary cost.

Just look at Queenstown - what a mess for locals - what a way to destroy a tourism asset - really having a feast on the golden goose there.

I would be quite happy to see 50 dollars a day ( or 100) on the hotel bed to pay for general infrastructure. Or perhaps what could be collected at the border is a 50 dollar a day tax for the length of the stay.

Other stuff also, like compulsory travellers insurance for those coming in across the border.

Agree completely. A generation of old politicians who are happily sacrificing the lot of the younger folk to pad their own feather beds and those of their older voters. Young people are having to give up the idea of a clean environment and the prospect of home ownership to prop up these net-drain-on-society folk.

Hotels and Motels just add another line to their bill charging you for the tax that they are collecting. It happens all over the world, I don't see how this is a big deal.

Another factor that strongly favours spending and speculating for capital gain and discourages saving, is the effect of inflation. The playing field can be levelled by making the inflation portion of interest received on savings, tax deductible and the inflation portion of interest paid on borrowings, non tax deductible. Should be nearly fiscally neutral for the Govt.

Interesting to note that this is the second article from the ANZ recently bleating that we need to save more. They must be a bit worried. Serves them right, as the banks have poured money into the housing market borrowers irresponsibly for years and have played a significant part in creating the housing bubble. You can't blame savers looking at them sideways now that these loans may well look dodgy as prices cool. besides which savers are receiving next to nothing back for what is now looking like a not insignificant risk. From this point on things could unwind rather badly. - Banks can't attract savings so have to raise interest rates and mortgage rates = more risk of mortgage default and selling pressure on the market and the banks risk profile = savers less inclined to save with them (OBR losses) = banks have to raise interest rates further - and so on.

A very simple solution is @ 6 interest rate rises until saving becomes more attractive than borrowing. The market will take care of its self. We need a few broken eggs to change behaviour.

Agree that this will help rebalance investment from equity/bond markets back into banks, but country risk, OBR risk, and company risk remain strong disincentives for those who look at the details. I'd rather hold senior bonds in a bank than cash these days, because bondholders are nearer the front of the creditors' line should the bank run into difficulties.

It also doesn't solve the fundamental problem of making a larger percentage of disposable income available for saving/investing, after housing costs (either rent or mortgage) are accounted for.

1. Australia has a capital gains tax. Have you noticed that their housing bubble is even bigger than Auckland's? So fat lot of good a CGT has done in regards to cooling the housing market.

2. A CGT would be the final nail in the coffin of the NZ sharemarket.

3. How does taking away 1/3 of someone's investment returns improve their savings rate? Not only is it a cost in terms of the tax paid, its also a cost in terms of the loss of return on those funds if left in the investment and compounded. The less money you end up with in retirement, the more of a drain on the taxpayer you will be.

4. Not having a CGT is one of the few advantages NZ offers residents over other countries, lose it, and we might as well all go live elsewhere.

5. Why should we be penalised with higher taxes for the Govt's decision to flood the country with immigrants? If you want to cool the housing bubble, stop issuing visas. Simple as that.

"How does taking away 1/3 of someone's investment returns improve their savings rate?"

You mean like taxing deposits on savings in the bank already is ie: Capital Gains Tax on Interest Earned?!

Capital Gains Tax is simply Income Tax in other words. If, as property investors believe, costs can be deducted from personal income ( negative gearing) why should any gains made that is income ( capital gains) not be taxed?

Capital Gains Tax is not a new idea developed especially for New Zealand; it is widespread ( as you note it exists in Australia without much harm?). Enacting it here would bring us into line with much of the rest of the World.

Why do we want to be like the rest of the world? As I said, its one of the few advantages NZ offers over the rest of the world. Making everyone poorer just so we can be like everyone else is not a valid argument. Especially in a country with low wages and high living costs.

At least investment into housing provides a benefit to society in the form of rental housing. Would you prefer that everyone sink their money into US index funds instead? What benefit would that provide to New Zealand? In a country that's extremely limited in investment options, there needs to be incentives to keep your money here.

If CGT is implemented the first thing I would do is start investing in overseas markets. At present, I accept the lower returns from the NZ (and part of the Australian) market in return for it being tax free rather than subject to FIF taxes. Remove that advantage, and if CGT makes all investments equal, my money would go to the highest returning market, which is the US or EU markets. How do you expect NZ companies to raise capital to grow when no one is interested in buying shares on the NZ market?

".. if CGT makes all investments equal, my money would go to the highest returning market, which is the US or EU markets.. And so it should? What's wrong with all investment options being 'equal' - being treated similarly for taxation purposes? If you see advantage in foreign economies and want the exchange rate risk etc, then by all means go for it!

Singling out one market segment ( property) should not be the domain of Government. As you suggest, it should be the market that decides where we all put our money. But to have the Government stand aside, it requires equal treatment of ALL asset classes, and not the encouragement of one - for whatever purpose that is ( you suggest rental accommodation as the purpose. Guess what? That would happen anyway! That's how markets work.....)

Not sure you've fully picked up K.W's point that an absence of CGT is a major incentive to remain in NZ equities, without which you'd see a significant movement of capital to other markets. Thus defeating one of the purposes of a CGT. The only attraction left would be imputation credits and they would not be enough to offset the small economy and currency risks of staying in NZ. I for one would significantly alter my country weightings away from NZ if a CGT were introduced on NZ equities.

Good points, and in many countries the CGT is adjusted for a nominal amount of inflation. In the US (as I understand it) Cg is taxed at half the rate of other income. As Chris M has pointed out, the savers pay tax on the full value of interest received with no adjustment for loss through inflation. That makes no sense and is morally wrong as well - paying tax on illusionary income. Is it any wonder we are lacking a decent pool of savings - you would think the successive governments have deliberately set out to sabotage savings with a regime like that. We seem to have this belief that capital gains are not income; chuck it in with other income and we look like a very different country. Combined with wage suppression through mass low skilled immigration and runaway house price inflation we now have soaring inequality. We are a lot more unequal than we like to pretend.

The latter is a good point.

Research on the Panama Papers in Sweden indicates that the average income earner pays 3% less tax than they should. But the top 0.1% pays 30% less than they should. So the metrics regarding inequality (eg Gini coefficient) don't actually reflect true inequality.

I guess in NZ, the rich will be using property as their preferred vehicle for avoiding tax, as covered in this article.

"1. Australia has a capital gains tax. Have you noticed that their housing bubble is even bigger than Auckland's? So fat lot of good a CGT has done in regards to cooling the housing market."

A CGT is not a silver bullet for the housing bubbles. Never has been and never will be. CGT is simply taxing housing gains from investment housing just like all other gains. The only ones who think it's unfair are those getting the free tax ride.

"That makes no sense and is morally wrong as well - paying tax on illusionary income. "

ha ha ha ha. You have clearly never heard of FIF, a yearly tax on unrealized gains. And what exactly is moral about paying tax on interest or stock gains here in NZ but letting the property investor who holds something for 2 years, get away with zero tax? Me think your moral compass needs an adjustment.

Try reading what I said again.

I'll put it another way; taxing the INFLATION component of interest received OR capital gains is wrong IMHO and there is no moral justification for treating them differently, as the current regime does.

CGT does not tax unrealized gains , nowhere is this the case

It's immoral that I have to pay tax on my income - yet we're placing a massive burden on income and none on land. Tax used to be applied to land too.

Most of the country gets more handouts from the government than they will ever pay in taxes, and it's immoral that I have to work hard and pay, so that they can get all their free stuff. I'll just have to work even smarter, make even more money to stay ahead of the ever growing number of parasites feeding off my income!

(Inappropriate and libellous comment deleted. Please see our commenting policy here - http://www.interest.co.nz/news/65027/here-are-results-our-commenting-po…, Ed).

1. The government could reduce taxes elsewhere, it's about rebalancing tax to encourage diversified savings, not raising funds necessarily.

2. The best way to encourage savings in all forms would be to discourage particularly favoured vehicles so that money is redistributed more evenly

3. I'm really struggling to see how calling for higher incomes, tax cuts, social investment and lower cost of living could be considered unpatriotic. Am I missing a particularly heinous detail?

4. Play the ball, not the man if you want to be taken seriously as anything more than a clearly vested interest defending their patch

Please tell me you're not Nikki from Propellor Property Investments

"At various seminars, Nikki has also been a guest speaker alongside the ANZ’s Chief Economist, Cameron Bagrie" (http://www.propellorproperties.co.nz/about-us).

I don't think the ad hominem helps your argument much.

I wonder how much Cameron Bargie has put down on term deposit?! Earning 3.35% Har har har!

Why not make interest from savings tax free to encourage ppl to save more?

I note, with amusement, that the Gorilla has been subject to Swingeing Deflation.

Useta be '800 pound gorilla'.

Now seems to be '500 pound gorilla'.

I suspect Animal Abuse - starving gorillas - where's PETA when ya need 'em?

What is it with my fellow New Zealanders? The first notion to solve any perceived problem is introducing new taxes. IT'S PERVERSE! Perhaps you think it will impact other people more than you? Uncontrolled envy is destructive to any society. Also, there's a common view that you have to be rich to invest in property. You don't - Anyone with limited income can invest in property through listed property funds etc. if they choose to.

Its clear that many commentators dont have the first clue as to how Capital Gains Tax works .

The devil is in the detail , and its so full of holes that you can swim right through it , and thats why it generates so little income for the taxman

FYI the tax is only paid on the sale of the asset , it is almost always inflation adjusted , and allowances are made for losses , interest and costs of repair , capital improvements are offf-set .

It is not triggered on change of use , so the batch can become your primary residence after you retire with no taxable effect .

Quite simply CGT is a disaster for all

The logic of implementing a CGT at the tail end of a massive property bull market escapes me. It would have a genuine chance of being revenue destructive, as the claimable tax losses would pile up in a property crash or correction. It's too pro-cyclical a tax in that it reinforces the tendency to hold an asset forever.

Look at the taxation that was going on in the 80's during the Wellington building boom. The Government was taxing the life out of everything they possibly could. In the end there were a lot of people who had massively overpaid their taxes to the tune of millions of dollars because the Government got really greedy.

A capital tax or wealth tax would be a less foolish option but as pointed out above people will find plenty of loopholes.

More taxes - the answer to everything. If you really believe that governments and local councils can spend your money more effectively than you can then you are beyond all help. Auckland Council wants a hotel bed tax and road charges and many seem to want additional general taxes on water. GBH wasn't far off when he jokingly (I think) suggested (above) a tax on the air we breath. That would seem to reflect the attitude of some.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.