This week’s Top 5 comes from Jarrod Kerr, chief economist at Kiwibank.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

The outlook for global growth continues to disappoint. Our economic potential is fading, and output is failing to meet lowered expectations of potential. There are some very large forces at play, and some crazies in charge.

Our economic potential is being inhibited by the tectonic shifts in demographics (declining fertility rates and ageing populations), which lower population and participation rates. And our productivity has disappointed due to an underinvestment in infrastructure, and education.

We’ve revised down our growth forecasts. Because the risks we have been wary of are coming to fruition.

Here are the top 5 things wrong with the economic world right now…

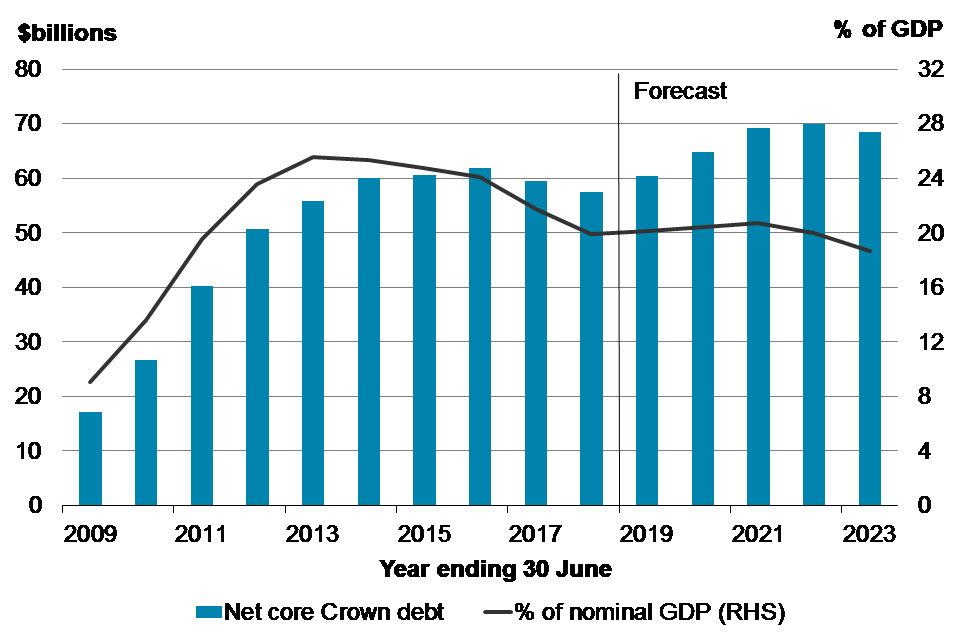

1. Fiscal austerity is our greatest mistake.

Fiscal austerity in the post-crisis world (since 2008) has severely limited the outlook for growth.

“The persistence of low inflation and low interest rates is not a surprise when, as has been true in fact, the low interest rates fail to generate substantial fiscal expansion.” (Christopher Sims, Fiscal Policy, Monetary Policy and Central Bank Independence)

Our obsession with balanced budgets and debt limits has created a burgeoning infrastructure deficit. We’re one of the 10 most highly rated nations in the world. And we have less debt than most nations in the top 10. Our Government has access to some of the cheapest funding in the world. But we haven’t taken advantage of our advantage. Our lack of investment has effectively choked our potential.

We should use the record low interest rates to invest and stimulate the economy for our children. We have to live with the poor decisions of the past. But it’s up to us to ensure the next generation has a healthy, vibrant, and efficient economy to grow into. If in 10-to-15 years from now, fresh graduates spend an hour commuting into the Auckland CBD, when it should take 20mins, to arrive late for their first job interview, we’ve failed them. And if their skills don’t match the job they’re after, we’ve also failed them. If we fail the next generation, then the bad news is they’ll vote for extremist parties that demand change. And so they should. Actually, it’s already happening.

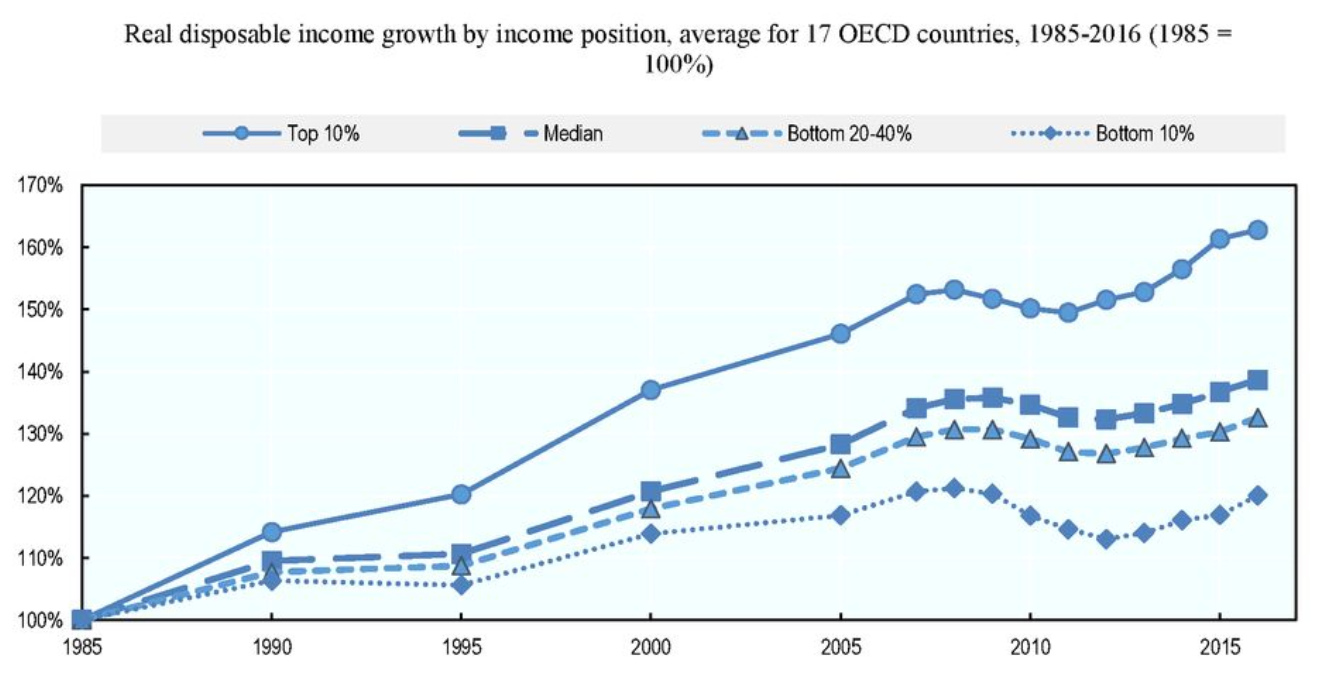

2. Widening inequality is a problem for everyone.

The worsening in inequality has many causes. Globalisation, technological disruption, and an underinvestment in education are key drivers. But the response to the global financial crisis in 2008 protected the wealthy more than the disadvantaged. Slashing interest rates, quantitative easing, and regulation have boosted and protected asset values. Therefore, the owners of assets have benefited to a far greater extent, in a world of very weak wages growth. Within the world of very weak wages growth, the incomes of the higher earners have risen much faster than the incomes of lower earners. The impacts of globalisation, technological disruption (think Amazon), and the disadvantages of poor education and wellbeing are seen clearly across income brackets.

Source: OECD

Rising inequality is the reason behind rising populism.

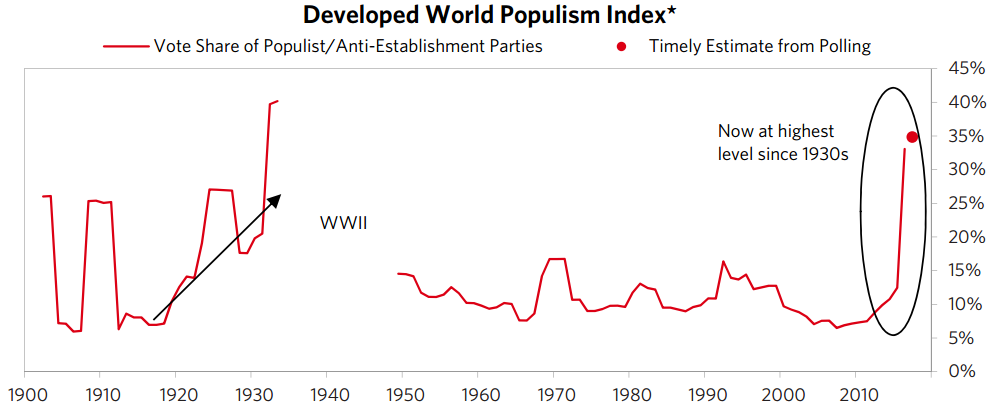

3. The rise of the angry voter, is popular in disbelief.

The sharp rise in populism has resulted in a sharp rise in protectionism. The rise in “anti-system politics” is a threat to global trade, and a threat not seen since the 1930s. Rising Inequality has produced populists in: Trump’s US, Italy, Philippines, Turkey, Brazil, plus Brexiteers, and Frexit followers. Trump’s tirade may be a tipping point.

The populist protectionist president, aka Trump, is fighting on many fronts. The US-China trade tariff “war” continues without resolution. Mexico quickly succumbed to US trade threats over border protection to avoid a similar fate. But we suspect Trump has not finished with Mexico, or any nation with a trade surplus to the US. The populist protectionist Brexit ordeal is still unresolved, and the patience of the EU is wearing thin. The real concern for the EU, however, is the rise in anti-EU politics within. The epic recovery in equity markets since the start of the year has been halted in its tracks. Interest rates have fallen sharply as traders’ position for several rate cuts, by several central banks!

Source: Bridgewater Associates

4. The age of regulation continues to fuel uncertainty.

Regulation has played a large role in slowing growth. The repricing of credit (money was “too cheap” prior to the 2008 crisis) is ongoing. Regulation has impacted the price, by restricting the supply of credit. Credit is the oil in the economic engine. The ramping up of bank capital requirements has yet to play out here, and abroad. Lower rates of credit creation, lower nominal growth rates. Regulation in financial markets is designed to reduce the risks of future meltdowns.

Our financial systems are far safer than they once were. But the goal posts keep shifting. How safe is safe enough? Guarding against once in 100 year events, now need to be once in 200 year events. And we’ve had some dire financial market meltdowns over the last 200 years. “We specify that we want enough capital in the system as a whole to cover losses that are so large they might only occur very infrequently (for example once every 200 years).” RBNZ.

The issue from my perspective is not the intent, or even the endpoint. The issue is around the time it is taking regulators to get us there. We’ve had 10-years of post-crisis regulatory change. It looks like we’re in for at least another 5 years as the New Zealand banks build more capital. Credit growth is likely to be slower over the next 5 years, than it would be otherwise. And that’s despite the record lows in interest rates.

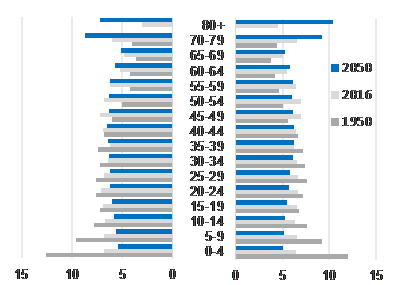

5. Demography is destiny for interest rates.

One thing is certain, global growth rates remain on a glide path lower. As economists, we talk of 3 Ps. We define potential growth as “An economy’s level of potential output is determined by the quantity and quality of its productive factors and the prevailing level of technology” (RBNZ). Potential growth has fallen, globally, for a variety of reasons. The drivers are split across the 3 Ps: population, participation, and productivity.

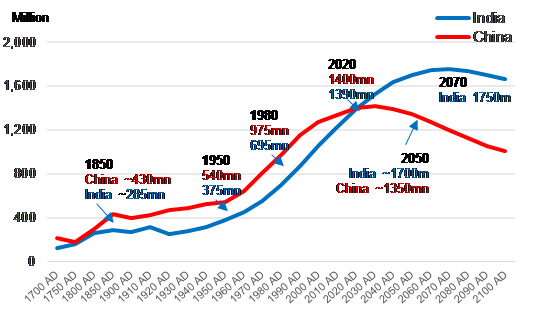

We have lower fertility rates, and now an ageing population. Population growth rates peaked in the 1970s, following the baby boom. Populations are peaking in large parts of the world – China’s population peaks around 2025, and starts to slowly decline for example. But we are not all created equal, India’s population doesn’t peak until 2070, and New Zealand’s population – along with the US and Australia – doesn’t peak in estimates out to 2100, given current immigration policies. BUT, we face the same ageing population issues. Which leads us to participation.

Participation has been lifted by the positive lift in female participation in large parts of the developed world. BUT, as the baby boomers retire, participation rates will naturally fall. How far and how fast will depend of migration (migrants are high participants) and keeping boomers in the workforce for longer.

In order to boost our potential, we need to look at policies to support population, participation and productivity.

I believe these forces, particularly demographic headwinds, will have to be analysed and re-analysed for years to come. And I think I may have discussed this before, in a past life.

60 Comments

Excellent piece. BY FAR the best bank economist.

Apart from that it comes from the same thought process that has created the mess we are in. It is all very convincing on the surface, but look a little deeper and it is all based on assumptions that are often glib generalisations or, far worse, unidentified.

For instance he says that low interest rates have benefited the wealthy. To me it seems that it has rewarded those who by skill or luck have front run the capital flows this policy has created. The major benefits have flowed to borrowers. As the government is our biggest borrower, it has also flowed more strongly to government management and employees than to private sector employees. The major loser has been the profitability of the productive sector, causing a lack of investment in productivity across our society. In short we have favoured Auckland house price speculation by foreigners, new residents and well payed Auckland professionals (eg certified members of the Ancient Cartel of Olde Lawyers) over productivity.

Our social problems are the product of economists from this groupthink cartel. The solution we are presented with will result on a patronage based social structure. The Shane Jones Patronage fund is a great example. It rewards those who suck up to those in power and discourages all else. It encourages any independent minded person to go live in Aussie.

The same thought process that believes we can grow forever in finite biosphere.

This gentleman, together with almost all the other economists and politicians have no concept of the true problems confronting us.

I find the comments about needing to support population growth particularly ignorant. No understanding of overshoot.

Excellent post Roger.

Widening inequality. What a tired euphemism that is. The problem is serious. We are seeing it on the streets and breaking into our houses. Very simplistically, if A has not got it and cannot see how he or she can ever get it, but B has it, then A sees his or her, only way of getting it, is by taking it off B and after a while that progresses, to being of some right, because of some perceived social injustice. In Christchurch this week, an elderly man just escapes serious injury outside of a supermarket, from an assault by a beggar. Widening inequality has developed to the point that the streets in NZ are not safe.

For another perspective, just substitute NZ for UK:

The idea that a country automatically benefits from foreign investment is based on the assumption that productive investment in any country is always constrained by a shortage of capital. That is why when foreigners promise to invest in a country, it is assumed that this will lead to an increase in productive investment.

But like many other widely shared assumptions among economists about what is or isn’t good for the economy, this assumption is too rigid. Foreign capital inflows into any country can lead to an increase in productive investment only under certain circumstances. Under other circumstances, these inflows are more likely to lead to either more unemployment or more debt. What matters are the underlying conditions in a given country and, to a lesser extent, conditions in the country from which the investment originates. In fact, as I will show below, while Chinese investment can cause developing economies to grow faster, it is unlikely systematically to benefit the UK or other advanced economies.

https://carnegieendowment.org/chinafinancialmarkets/79261

Excellent stuff. Suspect zero impact on government here though as orthodoxy on borrowing dominates.

Inequality plainly inhibits growth of economy beyond a certain point on Gini co-efficient. That point was passed well in past for NZ and most of OECD. Governments have swallowed the Kool Aid form corporations that anything business wants is good for "the economy". So, stuff society or anything that sill voters not National, might want, here or in EU etc. THIS total abdication by governments is the reason we have populism. In my youth (1980s) cynics whom I argued with used to say that all Parties were same so not worth voting. Back then I argued against that view. Now with TTP etc, it is plainly right. We continue down a Neo-liberal culture de sac in which bottom 50% is offered debt instead of wage increases and government continue to be servile to business.

#1 Jarrod, you're not the only one advocating the Government borrowing when the interest rates are low. My questions is what happens when, burdened by huge debt, the interest rates go up?

Another; why can't the Government just create credit to build that infrastructure? why do they have to defer to the banks as to how much money/credit is in circulation?

#2 but mostly #3 I am concerned that populism results in sops to the masses. We can see that Trump, Macron, May/Johnson, the EU and so on are not fundamentally changing the very systems that the voters are frustrated with, so the endemic corruption persists. They are just throwing crumbs to the masses to appease them.

#4 The results of #2 and #3 but the wrong regulation, or regulation in the wrong area will not have the needed effect for the masses and might even make things worse. We need economists who are not driven by greed or a lust for power and who can see the micro as well as the macro, and are not overly wedded to theory to provide solid advice to Governments. but then the political winds will silence them - at great cost.

Finally I feel sorry for anyone with the initials JK, but whose first name is not John, working in the finance world, but it seems this one can stand on his own feet and won't be tarred with that brush!

'My questions is what happens when, burdened by huge debt, the interest rates go up?'

My view is they won't go up much in the future. We are entering a Japan stage in our economic life (obviously there are differences, but fundamentally a lot of similarities)

We are entering a Japan stage in our economic life (obviously there are differences, but fundamentally a lot of similarities)

I disagree. Even during Japan's stupendous bubble, Japanese were on the whole far less reliant on h'hold debt relative to the country's productive output. Anyway, most NZers could not imagine 30 years of deflation. Ashley Church says house prices double every 7-10 years as if it's a religious phenomenon. If you asked him about the Japan experience, he would have a good argument as to the differences between NZ and Japan. A good argument in that it's a "narrative", not some kind of mathematical proof.

In Japan the trade surplus and fiscal deficits allow the private domestic sector to net save.

In NZ the current account deficit and the fiscal surplus push the private domestic sector to run up debt to sustain spending. Fiscal deficits are safe. Private debt is not.

G-T=S-I -X-M. Given a stable cab, if the Gov spent more it would allow households to repair balance sheets.

In NZ the current account deficit and the fiscal surplus push the private domestic sector to run up debt to sustain spending. Fiscal deficits are safe. Private debt is not.

Do you really think that NZ and Australia could run up huge fiscal deficits? I'm not so sure that we could. Theoretically I understand what you say but my intuition suggests that we couldn't manage huge public debt like Japan.

Why can't we manage public debt like Japan? We have our own currency, our own central bank, our own floating exchange rate, our debt denominated in our own currency? In NZ, it is unlikely we'd need such large ongoing fiscal deficits as Japan to reach full employment. But as long as inflation is under control why do we care about the particular level of public debt to GDP or the absolute level of deficit spending it does?. It's just keystrokes. It's the real economy effects on which the fiscal stance of the government should be judged. The idea that government spending is reliant on the whims of the bond market is erroneous. The central bank can control yields whenever it wants. Or buy any public debt the private sector doesn't want. Financial constraints on government spending are mere institutional convention. That does not mean governments should spend whatever they like. They should spend functionally.

I see you've got the MMT stuff down pat.

@JC. Well Ashley Church is religously wrong. Seen his stuff on Israel. Weird.

As I noted, there are obviously some social, cultural and economic differences.

And that is one of them - Japan's saving culture

But are there not similarities?:

- Slowing population growth, and an ageing population (albeit not as extreme as Japan)

- Permanently low inflation, and a permanently low interest rate environment, following a stupendous property 'boom'

- Stagnant economy

Interestingly, Japan has been able to diversify into non-tech areas like tourism that have been mainstays for countries like NZ.

Unfortunately, I doubt we'll be able to move much into Japan's high tech space.

I don’t think we have any of those do we? Maybe we have permanently low inflation, a bit too early to say for sure. I actually think our government could spark inflation if they had to.

What Japan shows us us that central banks in monetarily sovereign nations can control interest rates on the debt the government issues via QE. Which is just covert overt monetary finance. The Japanese government owes itself and finances its ongoing deficits. Yet no inflation or currency crisis or skyrocketing interest rates. Mainstream econ has yet to explain this.

"#1 Jarrod, you're not the only one advocating the Government borrowing when the interest rates are low. My questions is what happens when, burdened by huge debt, the interest rates go up?"

Issue 10 year bonds, interest rates are fixed, just have to stop rolling them over when interest rates demanded by buyers start rising. Gives you 5-8 years to budget for repayments to start.

Thank you Jarrod. A summation not unexpected from one in your position. Whilst economists seem to have all the answers, the reality at ground zero is somewhat different. Low interest rates are a curse. They are only low because no one wants to be productive at a time of declining demand, & after an age of huge transformation. This part of the curve has another 10-15 years to play out. Abysmal birth rates from among the western educated classes is a major issue, & one that is driving immigration trends globally. I've tried to get my head around this for years but I have to admit defeat here. This will mean our culture as we know it today, will essentially be gone within the next 100 years. The inequality thing is as much a problem from the dumb side as it is from the rich side. The dumb are busily breeding dumber while the rich are busily getting richer. Worse, the tax payers are sponsoring the dumb getting dumber. No wonder no one wants to pay their taxes. As for populism (a word termed by the liberal msm) I feel it is a return to traditional values in a new millennium. No more or less. It's the failure of the urban liberals, or the left, to lead us anywhere sensible that is behind the current backlash. Left of centre politics has no effective leadership that I can make out, nor offers any reasonable future that I can for see for the working people. And, as I've commented before, this does not end well. Sorry Jarrod.

Nice bit of context there. Personally, I think the pendulum may have swung to the extreme and be about to swing back to an appreciation of the values that make our society work. Not sure how it will play out, but most things are cyclical. The cycles can vary in frequency and amplitude as they interact, transverse and longitudinal waves, not just fixed frequency. I'm half way through Mandelbrot's fine book on Financial markets and how there are three states of volatility, regular, big swings, and phase transition. All rather fascinating.

"Our culture as we know it will be gone in 100 years".. it always was going to be gone in far less.. no culture is immutable, they are constantly changing. The culture of a country with 3 million inhabitants cannot survive the reality of the same country with 6+ million people.

The top 5 things wrong with the economic world right now:

1. Politicians

2. Bankers

3. Economists

4. Accountants

5. Lawyers

Teehee. I have for soft spot for accountants though, at least bankers and accountants understand the mathematics of finance. Bankers just take the money that society throws at them and their success goes to their heads. You have to use the right maths for the problem in hand, and Luca Paccioli's maths works in finance and economics. I think the main problem in Economics has been trying to use Newton's calculus instead. A form of Physics Envy. If you use the wrong maths you end up in a Procrustean world where you make the conceptual framework fit the maths.

The irony is that Newton was a fine economist with a deep understanding of monetary matters. Having lost his shirt in the South Sea bubble, he later developed the monetary system that made the British Empire pre-eminent. It was based on the concept of measurement, that the measuring instrument should be consistent across time and space, rather than just giving the result one's political masters require, as we have at present. Technology does go backwards, too. They lost the knowledge of brickmaking in England for 800 years after the Romans left.

Appreciate your posts, Roger. If you want to educate yourself on economics I suggest you read Martin Armstrong’s blog and his writings. I learnt more in a week from him than 3yrs majoring in economics at Auckland university.

Thanks Ludwig. I have been exploring Martin's blog and Socrates for a couple of months now, after an earlier comment on interest.co, quite possibly one of yours. He is an original thinker, they are a rare and precious breed. I just try to follow people who have a habit of being right. So I try to avoid anyone who did not see the GFC coming.

There is to be true, a few angry voters. But I think frustrated is a more accurate adjective. Our national and local administrations are now corporates. Money is to be made and spent. The SOE’s created by Roger Douglas and co, are hardly accountable. The relative ministers hide behind “oh that is an operational matter.” It’s all about self interest, self reward, gaining authority but holding no responsibility. Even the tradies are at it. How exactly do you get redress for bad workmanship. Where is there any practical effective authority to go to.?Summed up by the popular catchphrase of the day. “See you in court then.”

You've forgotten to factor in an enormous war which will reset quite a few assumptions, much the same as WW2 did.

https://www.businessinsider.com.au/charts-the-limits-to-growth-2012-4?r…

I'd have put that in as No1. And I wouldn't have bothered with 2,3,4 or 5.

Amazing what blinkered education does. Jarrod, download a copy of Overshoot (Catton). Spend the weekend reading it. Then look around your profession and think. Deeply. I can give you a list of reading after that, the message is that we are at, or about, the peak of human activity. If you want future generations to thank you, try leaving them something real, something maintainable by non fossil-fuel energy. Convince your bank to only back such proposals. Of course, there isn't room for interest-charging in a reducing energy/resources paradigm, but there you go. Maybe sue your lecturer if that wasn't made clear.

The rise of anti-system sentiment merely reflects too many people and too few remaining resources - and those graphs are crossing, after which they diverge.

"we need to look at policies to support population, participation and productivity' Um, per-person resources is the only metric of real wealth. Less people means wealthier people. Your metric is fatally flawed, sorry. Participation? Sure - it's disenfranchisement is driving the rising angst and increasing refugee streams. Productivity, as in 'of labour' is about 200 years out of date. Given that FF do more than 99% or 'work', productivity gains are actually energy efficiency-gains. Second Law of Thermodynamics applies, as does 'diminishing returns'.

Good luck negotiating the next decade.

Banks have had cheap money and loose lending for a while now. Most of it has gone into housing, not productive endeavors.

And if the government was to borrow heaps more to spend on improved infrastructure the value of that housing will rise proportionately ( I couldn't name them but numerous studies show the correlation, heck, how else do you explain a house built ten years previous being worth double it's initial cost despite having 20% less expected lifespan) with that improved equity position the house owner can borrow even more. Money for nothing, how can that be bad.

Regarding population, participation and productivity. Unending population growth is an environmental, social and in-the-end an economic disaster. There are some limits to participation (as we know it) but this can be improved. However productivity is effectively infinite - so that should be where all our energies should be focused.

I wonder if monetary policy is actually a thing that is helping to suppress birthrates (along with contraception and women's education)?

In other words young people not affording houses may put off having kids, having fewer in the long run.

This is definitely the case.

Read about this before, it's widely acknowledged I think.

The inability of younger people to buy houses until they're in their 30s has a lot of knock on effects e.g. later marriage, moving away from where you grew up, 'richer' areas becoming devoid of young families and so on.

I'm a boomer, and I couldn't afford to buy a house until I was in my thirties, and yes that was when i had my kids. so this phenomenon is not unique to these generations.

So the high house prices is not devoid of positive side effects then? We certainly couldn't afford to have everyone breed like the boomers did.

Of course this is a giant problem. Student loans and housing debt prevent family formation. As does insecure employment and low real wage growth. Letting them eat credit has reached its nadir. The economy stalls as the vast majority of people refuse to borrow even more.

1. Growth growth growth aye?

Import more people, make the motorways wider, import more people, make the motorways wider, import more people, make the motorways wider, import more people, make the motorways wider...

It's not a way to run a country. Totally unsustainable.

Make the women work, so they can't afford to have children. Import other people's to make up the shortfall.

Mr Kerr is right on austerity. And the need for fiscal stimulus. Smart capitalists should realise that it is far better to allow a good chunk of social housing to be built than have your house repossessed by a gaggle of irate pitchfork wielding millennials. You can have a nice safe asset to earn a risk free return on in the form of a government bond too.

So Jarrod thinks austerity is bad and the government should borrow and spend. Well if anybody thinks that, please demonstrate your view by taking on a large mortgage yourself and blowing it to 'stimulate the economy'.

I don't think the government has the right to do it on my behalf as well, so do it yourself.

compare apples with apples. The government is not like a household and can effectively create money. Windflow folded up over interest payments on 20 million of debt. that company was employing engineers, generating IP and overseas revenue. Imagine if they'd been given a 20 million interest free loan for 20 years from the government. https://www.nzherald.co.nz/the-country/news/article.cfm?c_id=16&objecti…

@ Fat Pat. I think you proved my point about stupid borrow ( and subsequent stupid handing out case) Windflow. " Imagine if they had been given 20 million interest free....." Well we ímagined" it and what we saw was a company that was still a dog.

but we're competing against nations who engage in state sponsored industrial espionage, and who're only too happy to provide financial support in the form of 0% interest to key industries. What happens when all the value add manufacturing shifts overseas. I guess we end up a simplified pastoral economy, similar to what Morgenthau had in mind for the Germans after WW2.

Jarrod thinks population stablisation is a problem. I don't see it. Just don't see the problem. Conversely I see continued population growth as an economic ponzi. And just nuts for our one planet. Its been well discussed here.

Sure a stable population means a higher proportion of older people. Lets just get used to it and organise accordingly.

I suspect economists attitudes to an aging population are like generals fighting the previous war (cavalry in WW1 etc). Yes in the past you needed young strong men to build your economy. True for hunter gatherers, true for farmers until recently and it remains true that an average young man in his twenties will shift more spadeloads of dirt than other ages and women. Especially true if he is strongly motivated to support a young family. It probably was still true when I was growing up but it sure isn't true now. Now we have a mainly service economy and the civil servant needs just the physical talent to sit on a chair and at the coffee shop carry a plate of food and a drink to a table (if they have table service!).

Admitedly a young person in their early twenties is generally capable of learning new skills quickly but honestly how often does that matter - maybe one person in ten thousand.

Most jobs can be done until you are in your mid-seventies and the soft skills and judgement needed for success means staff in their fifties are probably best.

So we don't need immigrants to fix our demographic aging problem; what is needed is deliberate encouragement for working longer - say reduced hours and more flexitime. The handful of manual workers may need to be retrained when they reach 50 assuming they are not already a team leader or supervisor.

A stable population fixes the housing problem and that significantly fixes the inequality problem.

Enjoyed this article. It would be interesting to hear what Economists think the future of interest rates and price stability will be, the long-term trend has been towards ZIRP but what actually happens when you get to zero and need more within a normal banking cycle. Would governments step in to promote growth as soon as unemployment ticked up fearing the electoral mood may swing rapidly?

Your first mistake is thinking government has a clue where to spend anything and would make the correct infrastructure investments. They will back there own political agenda as Labour has already indicated in there preferential sector treatment.

Milton Friedman hit it on the nail "If you put the federal government in charge of the Sahara Desert, in 5 years there'd be a shortage of sand."

It was human endeavour created a lot of that sand. And is busy creating more. You visited Sumer lately, for instance?

How would you explain Singapore then? Huge state sector involvement? It's simply not that simple. South Korea? Government has a massive role to play in economic development. But we need to rediscover the art of this after years of running down planning capacity. The Freidmanites had their go at running the show. It hasn't ended well for the majority.

Yes and it’s not like the private sector has done any better unless you think “investing” in existing houses somehow makes us richer.

I'd explain Singapore simply, a key trading hub position built by using super cheap imported slave labour.....is that really good model for us.

Thoughtful article, Jarrod, even though your point of view is assailed by the usual suspects. My experience in assessing tertiary education is that, far from being a key to productivity, it has largely become a credential-production line with little real added value. Unfortunately for the participants, it contributes directly to wasted years, wasted earning potential, foregone family formation and bye-bye-FHB. There are notable exceptions (STEM, which has the advantage of being reality-based) but much of the rest could be deep-sixed and no-one would notice. Secondary education is if anything worse, hailing as it does from Prussian army concepts rooted in the mid-19th century. None of this does much for Productivity....

The demographic changes are frankly intractable: as China is discovering. Keeping workers well into their 70's is a stop-gap only - eventually the attractions of the RV, the cruise and the rest home outweigh the cash flow advantages of continued work. And importing migrants needs a great deal more selectivity than Gubmints seem to be able to devise, more especially so when they are refugees with varieties of PTSD caused by their recent past: they will need pastoral care for years if not decades before becoming Productive in any wider and measurable sense. And we seem to produce enough home-grown souls with similar conditions.....and have in place perverse incentive schemes to ensure that this is a Growth Area.

There are those who believe the scattered thorium in seawater can be gathered, the gathering taking less energy than that obtaind therefrom. There are also those who believe in the omnipotence of the human mind, despite the example of all those magnificent minds on the Titanic, succumbing to a paradigm-change. The common denominator is 'believe'.

We are overshot, grossly. We are drawing-down, unsustainably. And we are betting on ever-more of both happening, using bank-issued betting slips. Go figure

What he advocates for in point one causes point two and correspondingly point three. The world is nuts

Sorry which austerity is that now?? Record low interest rates could hardly be called austere. Why the pendulum swinging? Why not just let finacial markets discover the true price of debt independent of central banks. We are all free market economies in the west, except in practice.

Great commentary everyone. Surely the best read of the weekend. PDK is right, we are finite. That is not factored into capitalism currently. It could be, but would require a change of attitude but so far no one's been brave enough to try. Although Japan is living with its population limitations, it is also selling like hell to the rest of us to keep up, so, no real points on the board so far. The planet will give what the planet can give & no more. Once the energy is gone it is gone. There are alternatives, but at this stage we think that less people is sustainable for longer, rather than the almost 8 billion we have, is the better bet. No, it can't last, but everyone's scared of the new reality & so the conversation doesn't change. But it will. When it has to.

Thanks - Japan isn't living within it's population limitations, though, far from it.

https://www.footprintnetwork.org/2016/02/21/origami-japans-ecological-f…

Frankly,i find it hard to take most economists seriously. This guy was presumably trained in classical economics;you know the one,that failed to say anything about what caused the GFC. The one that promoted the Capital Asset Pricing Model,the Efficient Market Hypothesis,the Arrow Debreu Theorem,the absolute rationality of agents and so on. This is a Social Science that was desperate to be treated like a hard science-physics,chemistry etc-so came up with impressive looking equations,but garbage in,garbage out.

Fortunately,the work of those like Kahneman and Tversky and added to by behavioural economists like Thaler have begun to expose the shaky foundations of classical-neo-liberal economics

Yes, lets spend, spend, spend, like the trumpeter that is running the USA into horrendous debt, all the while touting how magnificent everything is. Moronic thinking. IT HAS TO BE PAID BACK, something the trumpeter does not understand as he just files bankruptcy when things are unsalvageable. Lump the next generation with huge debt in the same way as USA???,awesome....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.