By David Chaston

It has now been 10 days since the surprise 50 basis points Official Cash Rate cut by the Reserve Bank of New Zealand.

This has allowed plenty of time for banks to react to the implications of a 1% official policy rate.

Markets have reacted by driving down wholesale swap rates. Markets have also driven down benchmark risk-free Government bond rates.

Locally these have shifted because of both the RBNZ signals, and the global risk aversion that is gripping markets.

Now we can assess how much has been passed through to the economy. After all, RBNZ Governor Adrian Orr was explicit that they are watching to ensure most of their policy action does pass through.

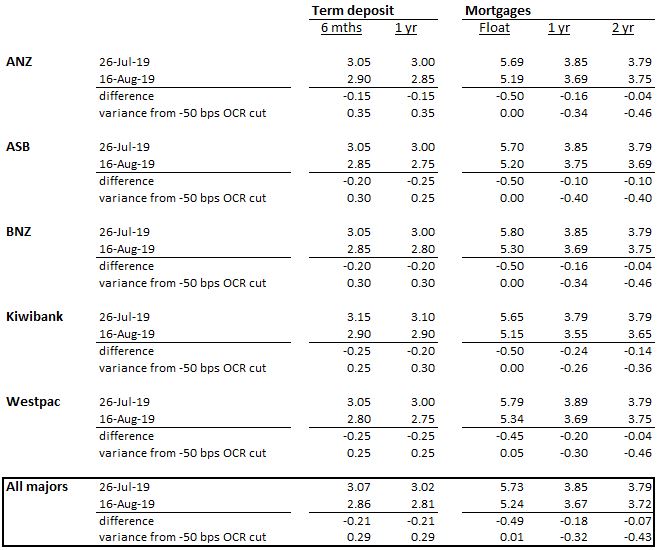

And so far the answer seems to be that a bit more than half the benefits have accrued for borrowers, and a bit less than half have been held back for savers. The banks themselves seem to have retained very little.

Of course, this can only be a crude assessment, but this is how we have made it.

On average, the main banks have cut their key term deposit rates by just -21 bps, leaving savers with a +29 bps 'benefit' from not suffering the full -50 bps OCR cut. That is almost 60% of the policy action.

All up, banks owe retail savers some $329 billion for the accounts they have.

These same banks, also on average, have passed on to floating-rate borrowers almost all the OCR rate cut. As we have previously explained, this is a benefit to borrowers who have 35% of the interest-paying debt in New Zealand. (About $164 bln of that debt.)

For home loan borrowers who hold about $223 bln of that debt as fixed-rate loans, banks seem to have passed on about 12 bps of the OCR cut so far. These borrowers hold about 48% of the interest-paying debt. Perhaps another 13% is held by businesses and rural lenders on fixed terms.

For personal loan and credit card borrowers, banks have passed on none of the OCR cut benefit, and this group holds about $17 bln of the debt (by bank and non-banks), or just 3.6% of it.

All up, all borrowers owe banks and non-banks $464 bln for the loans they have contracted to repay. Weighting the announced borrowing rate cuts in this way, we estimate that lenders have passed on an average -25 bps to borrowers across all borrowing. This is half the benefit of the official policy action.

Of course there is much more borrowing than saving (all loans amount to $464 bln while all retail (non-market) funding amounts to $329 bln). So you wouldn't expect the benefits to savers and borrowers to be equal, and they aren't. But there is enough to conclude that a bit more than half the benefits of the OCR cut have gone to borrowers and a bit less than half to savers.

Of course, this situation is dynamic. We will keep an eye on the situation as it changes over the next while and update it if the balance reported above changes materially.

35 Comments

This is an interesting read

http://sacred-economics.com/sacred-economics-chapter-12-negative-intere…

"There is little room in any highly developed economy for further domestic growth. The solution for at least twenty years has been, in effect, to import growth from developing countries by using the monetization of their social and natural commons to prop up our own debt pyramid. This can take several forms: debt slavery, where a nation is forced to convert from subsistence production and self-sufficiency to commodity production to make payments on foreign loans; or dollar hegemony, in which highly productive countries like China have no alternative but to finance U.S. private and public debt (because what else are they going to do with those trade surplus dollars?). Eventually, though, the solution of importing growth must fail too, as developing countries, and the planet as a whole, reach the same limits that developed countries have."

RBNZ signals, and the global risk aversion that is gripping markets. Yes it's a rates race to the bottom that includes savings rates they will be heading to ZERO! The RBNZ needs to restore public confidence in the NZ banking system otherwise Kiwi's will be looking for other savings/investment methods outside of the banking system (And no not property since that's too risky and needs to bottom out).

We at least need the Savings Deposit Protection Scheme of up to $50k per bank per Saver, which every other Western country has except NZ which is extremely poor. This needs to be implemented as soon as possible THIS YEAR!

If you ever need to use a Savings Deposit Protection Scheme for that very same $50k per bank per saver, it will be worth - nothing. ie: If things ever get so bad that a scheme of arrangement cannot be figured out for any failing local bank, it's Game's over...

So bw, you're suggesting it might be best to move all assets off shore and abandon little NZ as a lost cause. Seem that way since we're the only country in the West that doesn't have a Savings Deposit Protection scheme.

CJ, property doesn't "need to bottom out" because you'd like houses be cheaper, that's not how market's work. Yes some of the money earning too little from term deposit rates will go into property (directly, through REITS, funds or direct shares), how much is hard to tell, this will of course provide some support to house prices

I think most people still recognize that the property market is still sliding downwards (Particularly Auckland, Queenstown and Tauranga) no mater how much you would like to think otherwise Yvil. Small drops in mortgage rates isn't enough to maintain property prices in comparison to the enormous amounts of foreign cash that was being pumped in to our main cities and the ripple effect that caused which has now gone.

So yes property prices here still have to bottom out.

CJ099 you are absolutely correct. From this level, fall of interest helps but is not decision changing as the amount to be borrowed is huge and for 25 or 30 years.

What will decision changing be, will be the fall and amount of moratge to be borrwed. Also such drastic cuts indicates the direction of the ecenomy and everyone has to Be Aware.

Yes so true Stuart. :)

Hi CJ099,

Note that all of the reputable data series for NZ as a whole show that median/average dwelling prices are increasing.

TTP

TTP sorry but you're trying to twist the facts again, no one is falling for it! Here's some recent facts for you: QV figures show property values on a long slow decline in Auckland, starting to head downwards in several other regions! 7th Aug 2019

QV quote: "Areas where average values are down compared to three months ago include parts of central, north west and south east Hamilton, plus Tauranga, Whakatane, Rotorua and Taupo, all of Wellington City, Christchurch's central, northern and hills suburbs, Timaru, Queenstown Lakes, and Dunedin central, north and south".

https://www.interest.co.nz/property/101060/qv-figures-show-property-val…

Go on show me the facts and figures that prove that Auckland's house prices are rising along with Queenstown, Tauranga and all the larger investment areas, I dare you and you know that the small provinces don't count. I'd be delight to see your so called data that you never EVER provide. :)

Do you have one showing year on year increases? Everything I've seen has been (as Bill English says) "flat to falling". Am curious as to what figures you're actually basing this claim on. Hopefully they're tangible.

REINZ Median and HPI show NZ up yoy. Median is up about 4.5% and HPI is about +1.5% for NZ. Auckland itself is about -3.3%.

Thanks for the pertinent article David

I would have put money into Govt kiwibonds at 1.5% if it wasn't so difficult/archaic to apply for.

Fill out the form and mail it to Auckland with a cheque. Really?

Cj99,the property market in NZ is not sliding down at all.

When interest rates are as low as 3.55 p.a. For one year, there are going to be experienced investors starting to buy up!

First home buyers are now seeing that it is cheaper to own than Rent and if they don’t buy now in ChCh then they probably never will.

Cheaper to own than rent. Crikey, better get those first home buyers to mop up all the rentals that people are flogging cos' our Dear Leaders don't like them in private hands. Squeeze the tenants into fewer houses. That should get rents rising again, so the bureaucrats and politicians can point and say:

"Look! GDP UP! Inflation UP! Wages UP! Aren't we clever!"

Meanwhile, as a nation we dig deeper on down into the debt pit and the Aussie banks look after the Debt Farm.

Roger, this coalition government has done absolutely nothing positive for housing in nZ.

We are still waiting for the KiwiBuild reset, which is a long time coming.

Reality is that they have no idea and by reshuffling Twyford and bring in Woods and Faafoi is just smoke and mirrors, and shows that they have got absolutely nothing.

Arderns halo is starting to get dimmer by the week.

Mr Cheap-seats, They actually have done quite a lot to reduce property prices (Foreign Buyer Ban) making them more affordable just because you have a very blinkered perspective doesn't mean you see the bigger picture. Hey they could reduce prices much further by introducing an empty homes scheme if you like.

But the national average price has gone up?

Fewer houses? that old chestnut.

One household of renters moves into one freshly purchased house. 1 In, 1 Out.

One of the big reasons there is a difference in OO vs renter occupancy is all the oldies living alone, widows like my grandmother with a three bedroom house all to herself. Something like 75 or 80% of over 65s live alone or with partner only, so that cohort of the population has a good chunk of houses with an average occupancy of <2. As tey move into rest homes, or shuffle off the mortal coil those house become available, and get occupied by higher occupancy youngr families, whether renting or owning. This so-called shortage is nowhere near as bad as some make out, and if a lot of immigrants decide to leave.. well, shortage no more.

Rentals are on average more crowded than owner occupied houses. Its not 1 in and 1 out. Shifting from rentals to owner occupiers slightly reduces supply.

Sometimes you need to look deeper than the overall number. All those old couples/single lower the owner occupier average, but they aren't representative of the ones buying houses to occupy.

On one end of the spectrum (as you have mentioned) you have the old couples/widows living in 3 or 4 bedroom houses, at the other end you have students who would never be in a position to buy renting in "student type" accommodation (4 - 5 + bedroom houses). In the middle is the life stage where young couples settle down and start a family, they're the ones being trapped into renting due to the hurdles of home ownership, and they're often (and i speak anecdotally) the ones who are renting 3 bedroom places without flatmates. If they leave their 3 bedroom rental to buy a 3 bedroom house, it's a zero sum.

Yep, and when those young people in flats pair up and save enough to buy, they move out, the flat acquires another young couple or single to replace them keeping the flat occupancy relatively stable. And the couple that paired up and got a place of their own ,sure, they are a lower occupancy house, but from what I've seen that only lasts a year or two before the basinet and baby clothes appear. If they are happy and committed enough to sign up for a mortgage kids usually aren't far away.

@ The Boy 2: Perhaps when mortgage interest rates hit the 1.5% for a fixed rate deal then you may see residential property prices bottom out in the more expensive cities particularly in Auckland. Remember you are see property prices from the cheap seats with ChCh being much lower in value and it was not effected by foreign buyers since they were more focused on Auckland. Your property prices were simply pushed up by rebuild costs from that massive earth quake you had and are still recovering from. Not sure how any investor would take the risk of buying property in Christchurch considering the very high earth quake risk. I have to admit that put me off Wellington as well, even though I think it's a nice place apart from the windy wet weather and regular earth tremors.

Earthquakes are not a worry for Christchurch property investors.

Everything is insured and ChCh has had that many shakes and we have not had a single property written off.

The fact is that property investment is the safest investment by far, and positively geared property is only going to get better in ChCh.

cJ, if you worry about things like you clearly do, you would be better just being in Term Deposits and not getting ahead financially.

"Earthquakes are not a worry for Christchurch property investors". You've got to be kidding me! Earthquake and flood zones are a risk and a high risk at that! Next you'll be saying that your happy to build an investment home under an active volcano. I just don't take silly risks and pay more expenses in thousands of dollars for extra insurance which may or may not fully cover you.

Re Term Deposits - Nahh I would sooner leave NZ than go for Term Deposits here, that's an even bigger risk than property investment in an earth quake zone. Not until they bring in the Savings Deposit Protection Scheme that all Western countries have except NZ!

CJ you are absolutely correct. There is a huge question mark over the integrity of the second hand housing market in CHCH. Any house that suffered serious EQ damage, whether declared or undeclared, is highly suspect. This is why this government is having to revisit thousands of shoddy repairs by the previous government under the mantle of EQC/Fletchers. On top of that there are the dud and insufficient repairs by the Insurers. And on top of that there are the dodgy repairs by certain opportunistic scavengers who have bought “as is.” There have been several publications of purchasers getting “respected” building inspectors surveys only to find, down the track, that serious damage has been completely missed. Moral of the story, stay well away from houses in areas of widespread EQ damage, at the least.

That is why successful investors are successful.

Because they do invest, and don’t over analyse everything!

ChCh market is just fine, we have done very nicely since the quakes and many people have made a heck of a lot of money since then.

As for dodgy repairs, we haven’t had any because we have employed our own subbies.

Humm I like to stick to the facts not just march in blindly. And I don't think you understand how insurance premiums go up when you're in a high risk zone. That's a headache I can go without thank you. I'll keep to safer more lower risk areas, lower insurance costs and less hassle. Just common sense really. Plus according to the latest QV data it looks as though property values in Christchurch are declining in the Central, North and hills areas. Might be due to people not wanting to take on more risk factors, with little to no capital gain.

https://www.interest.co.nz/property/101060/qv-figures-show-property-val…

This in from a Remuera Real Estate Agent

“It looks like home buyers are back in the market enforce. I have a large number of clients who would rather buy some real estate than leave their money in the bank.”

How will this effect the banks cash reserves? This is a very affluent area so it would not be unreasonable to expect many of these purchases would be for cash.

Large cash withdrawal + No mortgage lending = Distressed bank ☹️

Pretty much what I said a week ago about pent up FHB demand when interest rates have fallen further. The banks cash reserves are FALLING and the banks may come to the point where they need to raise TD rates again to try and stem the outflow. Now looking at property again myself as my TD's come out at the end of this year on now what look like were great rates.

Well it depends? Are they buying with cash from Foreign Owners? If it's a locally based vendor, then the funds will likely be debited back into the/a bank.

with the foreign buyer ban surely it means the odds of the seller being a foreigner haven't decreased, but the odds of the buyer being a foreigner have been reduxed to near zero, so the flow of funds from residential house transactions has changed direction, from a net inwards cashflow to a net outwards cash flow.. just a question of magnitude. We know it was huge inwards flow a few years ago, is it now a trickle out, or a torrent?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.