By Gareth Vaughan

News that Australia's Westpac Banking Corporation is reviewing its ownership of Westpac New Zealand poses a couple of key questions: Why would you sell an oligopoly bank? And who might want to buy an oligopoly bank?

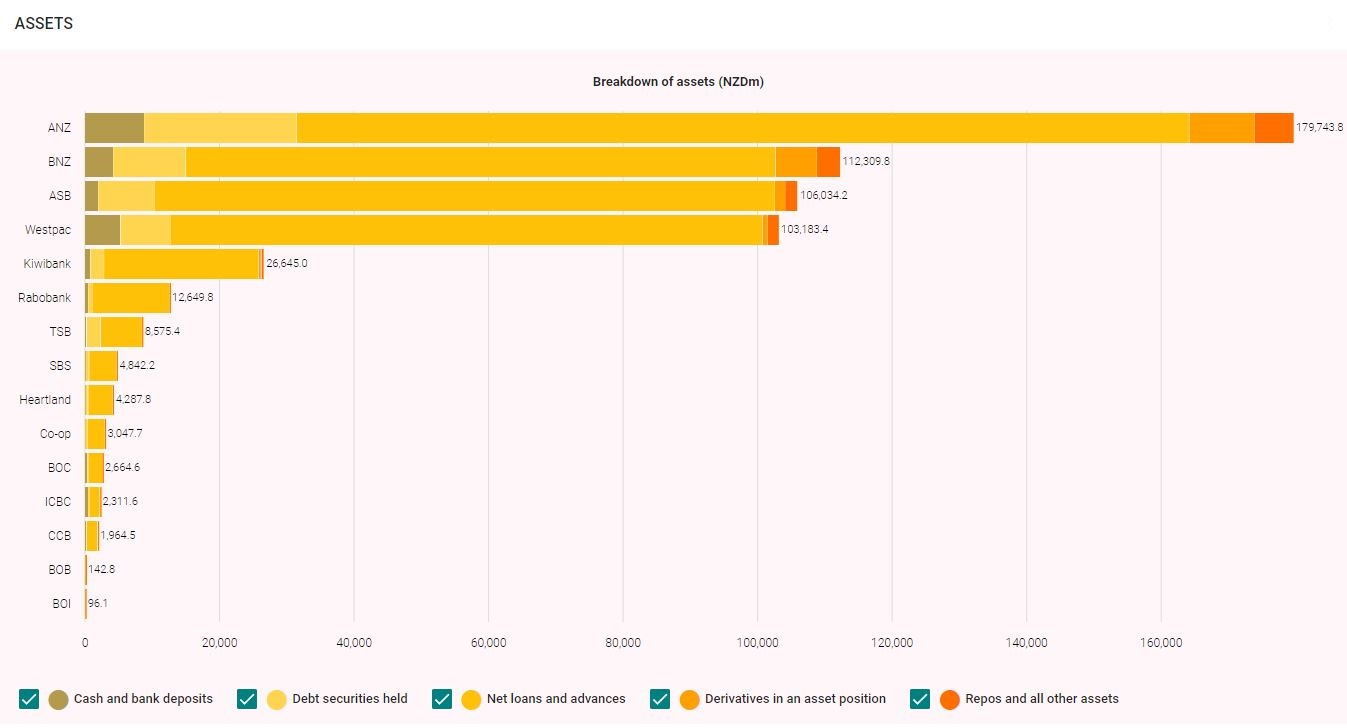

NZ's banking oligopoly, of course, consists of the Aussie owned quartet of ANZ NZ, ASB, BNZ and Westpac NZ. Between them they had total assets of $501 billion as of September 30 last year. That's 88% of total New Zealand banking assets. Westpac NZ, with total assets of $103 billion, ranks fourth. It dwarfs Kiwibank which is fifth with total assets of $27 billion. (See chart at the foot of this article for more detail).

This market dominance means the big four banks have enjoyed a stellar time of it in NZ for years. Deutsche Bank analysts Matthew Wilson and Anthony Hoo summed this up nicely two years ago, at a time the big banks were lobbying hard against Reserve Bank (RBNZ) proposals to increase their regulatory capital requirements.

"This unique market structure, we are yet to find another one, generates oligopoly-like returns. The four banks print an average return on equity of 15% and remit 65%, or NZ$3.25 billion, of earnings back to the parents as dividends," Wilson and Hoo said.

So why would an owner of one of these banks want to give this up?

Westpac's announcement of the ownership review came within hours of the RBNZ saying it had ordered Westpac NZ to increase its holding of liquid assets, cash or assets that can be easily converted into cash, after being non-compliant with liquidity rules for eight years. Westpac noted this, and the RBNZ's strengthening of outsourcing requirements - so Westpac NZ can operate on a standalone basis from its parent - and increasing bank regulatory capital requirements.

"Westpac NZ is a valuable part of the Westpac Group and has been for over 160 years. The business continues to perform well with a strong position in retail and commercial banking. However, given the changing capital requirements in New Zealand and the RBNZ requirement to structurally separate Westpac’s NZ business operations from its operations in Australia, it is now appropriate to assess the best structure for these businesses going forward," Westpac said.

Westpac said it was "assessing the appropriate structure for its New Zealand business and whether a demerger would be in the best interests of shareholders."

The increasing RBNZ capital requirements, which banks have seven years to phase in, will likely reduce the major banks' return on equity outlook. Albeit from a high base.

The citing of RBNZ regulatory moves in Westpac's statement shouldn't come as a surprise. Those with long memories will recall Westpac, even though it's the NZ Government's banker, isn't shy about throwing its weight around in politically charged situations. This certainly happened in the run up to Westpac NZ being registered as a NZ bank, a NZ incorporated subsidiary of Westpac Banking Corporation, in 2006. Until then Westpac NZ's business was conducted by a branch of the Australian incorporated bank. The change was made to bring Westpac in line with the RBNZ's local incorporation policy, and meant all systemically important banks (the big four) were locally incorporated.

Behind this dispute were concerns on the NZ side of what might happen to Westpac NZ depositors in a wind-up situation, and for Westpac whether the shift would see it slugged with a capital gains tax liability from the transfer of assets from the branch to the incorporated subsidiary.

What about its own backyard?

Westpac's statement didn't say much about its domestic Australian woes. These have included the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. In its 2019 financial results Westpac included provisions for estimated customer refunds and payments, associated costs, and litigation of A$958 million.

Additionally the Australian Prudential Regulation Authority (APRA) acted against Westpac breaches of liquidity standards in December. And prior to that Westpac and Australian anti-money laundering regulator AUSTRAC struck a deal for the bank to pay an A$1.3 billion penalty for 23 million contraventions of Australia's Anti-Money Laundering and Counter-Terrorism and Financing Act. The contraventions included transactions associated with possible child exploitation.

This scandal saw Westpac CEO Brian Hartzer resign in late 2019, to be succeeded by Westpac's former chief financial officer Peter King. Westpac's September 2020 year cash earnings fell 62% to A$2.608 billion. And in December Westpac announced the sale of its Pacific businesses, in Fiji and Papua New Guinea, to Kina Bank for up to A$420 million.

And not to be underestimated are changes that APRA is requiring the major Aussie banks make to the capital treatment of equity investments in subsidiaries such as their NZ offshoots. UBS analysts have noted that: "The implication is that small investments, below 10% of parent common equity tier one capital, can be leveraged further. But large exposures such as NZ subsidiaries require more capital to protect Australian depositors in the event of default." There's more on these APRA moves here and here.

In Westpac's own words, the ownership review of Westpac NZ comes as part of the banking group's "fix, simplify and perform strategy." And there's a whole range of reasons why Westpac might have decided now's a good time to test the market for its Kiwi subsidiary.

So who might buy?

Moving onto the next question of who might want to buy Westpac NZ, we can expect plenty of tyre kickers. Why not? Investment bankers sensing a nice fee feed will be peddling the bank in all directions. And NZ institutional investors, gagging for a slice of one of the country's major banks, would love to see Westpac NZ listed on the share market.

The options likely to be under consideration by Westpac include retaining Westpac NZ, spinning it off to Westpac shareholders and listing Westpac NZ on the share market, or selling the NZ subsidiary to new owners.

From a New Zealand Inc perspective speculation will swirl over whether Kiwibank, backed by shareholders the NZ Super Fund and ACC, could make a play for Westpac NZ. Realistically, given the size difference between the two banks, such a deal would require some serious financial engineering. In their 2019 report Deutsche Bank's Wilson and Hoo valued Westpac's NZ business at NZ$13.7 billion.

Nonetheless, the idea of the Government potentially getting involved will also be floated. One suggestion on twitter, for example, is merge Westpac NZ and Kiwibank, retain a controlling stake and use the combined entity as a policy bank to grow business lending and fund developers of affordable housing whilst listing a minority stake on the NZX to allow Kiwis to participate.

The last ownership change at a major NZ bank was when ANZ bought the National Bank from Lloyds TSB for almost $5.5 billion in 2003. However, it's hard to see ANZ, BNZ's parent National Australia Bank or ASB's parent Commonwealth Bank of Australia seriously considering buying Westpac NZ today. They likely feel they have enough exposure to NZ, and face the same APRA subsidiary capital rules as Westpac.

The return of George?

Meanwhile, The Australian newspaper has touted Bank of Queensland as a potential bidder. This suggestion is interesting if for no other reason than because Bank of Queensland's managing director is George Frazis, the former CEO of Westpac NZ. A Bank of Queensland spokeswoman said the bank doesn't comment on speculation.

Bank of Queensland is currently acquiring ME (Members Equity) Bank, which may keep it occupied for the time being. The ME Bank acquisition will give Bank of Queensland 2% of total Aussie banking assets, or about A$92 billion worth. After leaving Westpac NZ in 2012, Frazis headed up St George Bank for three years, which Westpac had acquired in 2008. Thus he both knows Westpac NZ and has experience running a relatively newly acquired subsidiary.

Japanese interest in Westpac NZ can't be ruled out. The last sale of a major NZ financial institution, UDC Finance, was to a Japanese bank. Shinsei Bank completed the $794 million acquisition of the vehicle and asset financier from ANZ last year.

Bank of China, China Construction Bank and Industrial and Commercial Bank of China, the three Chinese government controlled banks active in NZ, could all certainly afford to buy Westpac NZ. But would they want to? Thus far they appear to be pursuing a strategy of incremental growth in NZ. And are New Zealanders ready for one of their major banks to be owned by the authoritarian Chinese government?

Banks or behemoth international private equity funds from elsewhere in Asia, Europe and the US can't be ruled out. And could fintech companies even play a role? Notably Westpac already has a partnership with buy now pay later service provider Afterpay. Afterpay is launching a banking app in Australia with Westpac to hold Afterpay deposits on its balance sheet and meet APRA requirements on Afterpay's behalf.

I'm sure plenty of names will be thrown around before Westpac's review of its ownership of Westpac NZ is done and dusted.

Should a deal with a new owner be done, a non-objection notice will be required from the RBNZ, Overseas Investment Office Approval will be required if the buyer's an offshore entity, and should one of the other oligopoly banks be the buyer, the Commerce Commission would need to give its stamp of approval. There could also be questions about whether the Westpac name would be retained, and if so for how long?

So hold on to your hats as there's plenty of water to flow under the bridge before Westpac NZ's 1.3 million customers and 4,500 staff find out if they're getting a new owner of their bank.

37 Comments

What about the staff? What does this sort of public musings (by Westpac itself) do to morale already rather shaken by closures & cutbacks and all the uncertainty, like others, of CV19’s impact on life and NZ’s economy. If it transpires that this is nothing more than distant drums & smoke signals then it is petulant, high handed & reprehensible attitude & behaviour afflicting employees from bottom to top.

Not Many jobs come with guaranteed longevity these days.

I work in an industry where mergers are happening all the time. I've been in two companies that were purchased while I was working there, and I'm not a dinosaur. If you're good, they'll probably try and keep you and if they don't the rest of the market will be waiting for an opportunity to hire you.

It’s not me. ‘‘Twas long ago I worked for a Trading bank. But in any organisation staff morale across the board, especially at customer contact level, is vital.

If it was owned as a standalone entity, it could have a distinct advantage.

Currently all our banks are hamstrung by either lack of scale (kiwibank and below) or through kowtowing to both RBNZ and APRA (the bug 4)

Being large, and removing APRA from the equation would allow extreme efficiency gains.

There's also the not insignificant chance that we will be the buyer, just like UK citizens bought Royal Bank of Scotland and Lloyd's.

Time may not be on our side in that decision, and someone has to protect our economy - the mortgage market in other words.

Call me whatever you like, but this must NOT fall into the hands of the Chinese govt, which is what will happen if it is sold to any Chinese bank.

China has played its hand to perfection.

“The supreme art of war is to subdue the enemy without fighting.”

Further to mine above. If New Zealand finds itself in unmanageable economic turmoil, we no longer have the resources to assume any or all banks that fail. So will we be able to pick and choose who we want to be our saviour? No.

We could have de-risked our economy a decade back, at the latest, but no. We blindly stumbled on; doing what we had always done and assumed that next time the outcome would be different.

It's not like we weren't warned. Many, me included, could see exactly what the Chinese govt was up to, which became clear to us with the sale of the Crafar farms, they paid OTT money for them that no-one else would have seen value in, except them, for the foot in the door value.

It was clear then, to those of us who could see past the $$$$$$$$ that China would indeed gain the upper hand financially and once established that, apply the totalitarian screws, and hello, look what has happened.

Now we are in no position to separate ourselves from it, unless we want to feel some real pain, and I can't help thinking, it just might be worth it.

HSBC. Established & poised?

I’m not a huge fan of Government’s owning a lot of things and if you had asked me 10 years ago my answer would have been different, but I think the time is now for the Government to help Kiwibank scale and Westpac can provide that. In addition, the Government banking setup is bespoke to Westpac and no other bank can replicate that and manage the change successfully. Kiwibank would then have the scale to be a true challenger bank and hopefully create more competition in the market.

Hahaha. Kiwibank had a mission critical server at a domestic domicile during COVID and their IT infrastructure is held together with rubber bands and duct tape. You're dreaming.

Seem to remember a $90m odd impairment for an IT fiasco in the last year or two. Think a CEO just shortly before or just after the IT impairment resigning.

Kiwibank when first formed probably took up those who weren't quite up to it in the Ozzie banks. They definitely didn't want to lend me any money on two occasions a few years apart but surprise surprise my Ozzie bank were quite happy to. No special or onerous T&Cs either.

Typically when an organisation scales through LBO it's because they have the capability to improve the financial performance of the organisation being acquired. Kiwibank lags the industry by many return metrics and has done for some time. It would make more sense for Kiwibank to be viewed as an acquisition target by a bank with a higher level of management capability.

I want Kiwibank to do well, we really need more banks in New Zealand (particularly those with a focus outside residential lending and vanilla business banking), but Westpac is not that opportunity. That's not to say that there might not be another local buyer for Westpac of the price is right and RBNZ/Government can refrain from interference.

I always find it odd that so many kiwis are happy to bank with the big four and see the profits head over the Tasman.

We have little other choice now. (Yes, there are small entities to choose from, but they couldn't handle the scale of mass new customers. Their credit standing in international funding markets wouldn't allow it.)

Try establishing a new bank here, call it whatever you like that isn't Westpac (in this case) and see how many Letters of Credit; FX facilities and Lending Lines you get to establish.

Next to none will be the answer.

So your business model will be a non-starter from day one.

(NB: Note how even the new banking upstart in Aussie, Barrenjoey, is really just Barclays Bank in disguise.)

https://www.barrenjoey.com/

Often think if it was worthwhile and/or necessary for the Clark government to bail out a dire AirNZ situation then the preceding Bolger government should have had more cause to do the same for the BNZ. Then again there was a large scale black cloud hanging over the outfit at the time, some things perhaps needed to be kept buried?

Point taken, but what if people just moved to Kiwibank? Surely they have the ability to scale up and overtake the big 4?

we moved to Kiwibank shortly after it opened - no complaints. However retail banking is not the same beast as the wholesale side

"This unique market structure, we are yet to find another one, generates oligopoly-like returns. The four banks print an average return on equity of 15% and remit 65%, or NZ$3.25 billion, of earnings back to the parents as dividends," Wilson and Hoo said.

We are on an express path to a centralised rather than decentralised economy. Authoritarianism vs Liberty. In 2018 @ProfessorWerner explains how & why, while there has always been an alternative way, except no economic commentator on #MSM will tell you. Link

The Werner video is such a clear and well explained summary of where we are and why, it beggars belief that those like our RBNZ Governor either don't understand it or worse, do, and still choose to stick to Plan A.

A couple of years back, Westpac moved their IT infrastructure from Wellington to Auckland. In the process they let go most of their Wellington based technical staff (about 140 people IIRC). Once they got to Auckland they struggled to hire those specialist staff back. So they came back to Wellington looking to hire. Good IT people are hard to find, and understandably all those staff had moved on. You can't run a bank successfully without good IT infrastructure and I expect they're seeing the fruit of their actions about now. A complete failure on behalf of management, and an inability to read market conditions. I would put money down, that this is a big part of the reason they're looking to sell.

If they get bought by a larger bank, the IT delivery and merger has an 80% chance of being a complete shambles. If it's an SAP based system, those odds go up to 100%. Long story short, When it comes to where I put my banking business in the next 5 years, I wouldn't touch them with a barge pole.

I understand from the horde of ex Westpac staff that have left in recent months that something in IT fails every two weeks.

They honestly have no idea what they are doing in IT. They think they do, but sadly you they do not. Years behind cutting edge. They must be busy with harvesting spaghetti https://bit.ly/3sSAyi6 and I am thrilled since after that they learn about some core Enterprise IT concepts.

I was heavily involved with implementing the IT infrastructure for a SaaS payroll product for a number of foreign financial institutions in Japan, and I can tell you that 80% of the effort was defining, documenting and testing the processes. Crossing all the t's and dotting all the i's, not only for ISO 9004, ISO 27001 and Japanese Privacy Mark requirements, but also specific security needs for particular customers.

The hardware/software was simple by comparison. 80-odd virtual servers running on VMWare across 2 data centers - one in Tokyo and one in Okinawa - with immediate failover and 99.999% availability. Dell made a decent amount off us at the time, even with the sizeable discount we negotiated.

We had twice-yearly failover tests, penetration tests, QA and security audits, and yearly disaster recovery walkthrough where we simulate the total failure of the Tokyo data center and operations offices as part of the Business Continuity Plan.

I just have a suspicion that many corporations think the solution is mostly tech, but in reality a robust and reliable IT system is making sure the business requirements are met, and that everyone is trained to do the right thing when needed, and can handle it if they don't.

The time and money to ensure that you have a scalable solution that will continue to supply your business needs in the event of a disaster, whether natural or man-made, usually exceed what companies are willing to pay in capital expenditure and ongoing costs, so invariably things are pared back until the budget is met, usually leaving you with something that is hardly better than putting all your critical information on a laptop you take home every day.

The issue seems to be with executive management just looking at IT as a cost centre. A big black hole they pour money into. They don't see any revenue from it (generally, unless supplying IT infrastructure is your business), so they are loath to spend anything on it, but you turn off the Internet router and all hell will break loose.

Or worse, find out that all your company email has been compromised because you were using an unpatched version of Microsoft Exchange on Premise, and when the blaming happens, the IT department head points to the paragraph in the 2018 department report that says that software needs to be updated so it can continue to receive current security patches, and then points at the meeting minutes where the CEO and CTO say "it's working fine, and we have more important things to budget for. We'll update them when we can."

Funny attitude for people to have about a critical part of doing business.

The first half of the article is a sad indictment of the banking industry as a whole as practiced in NZ and elsewhere.

Why do we tolerate this?

If a China bank takes over Westpac NZ a few customers may choose to move.

https://www.canstar.co.nz/banking-satisfaction/

But then again, there is a big lock-in effect with banking customers as moving mortgages, credit cards, accounts, KS, etc is a hassle.

I believe the government use Westpac for their banking?? You'd hope they'd move.

I would love to see Westpac NZ listed on the share market. In more general terms, we need much, much deeper capital markets in NZ: the current situation is abysmal.

We have to move away from the 19th century mentality of focus on residential property, and start channeling resources and focus towards the real economy, especially the export-oriented part of it.

Warren Buffet should buy it and add to his Banking portfolio. Would be nice entry for him into Asia-Pacific.

But seriously, Westpac should hive off the NZ operations and sell 75% of the shares in the market, with due reservation for NZ staff and may be some percentage for ACC, NZ Super fund, etc. The Aussie owners can be allowed to keep 25%. Fair Dinkum.

"From a New Zealand Inc perspective speculation will swirl over whether Kiwibank, backed by shareholders the NZ Super Fund and ACC, could make a play for Westpac NZ. Realistically, .." Maybe Kiwi Bank could be that NZ bank that handles all the intra-banking btw the government and other parties, as well as the central bank to receive funding from the RBNZ for the funding of all the infrastructure, works to come online. All it would take is the Kiwibank to employ the expertise from Westpac?

A few observations (assuming Westpac are actually up for sale which I very much doubt)

1) If Kiwibank don't acquire it in some capacity then we should shut them down. NZ needs a real NZ owned banking alternative and this is a defining moment for Kiwibank.

2) Not a snowflakes chance of BoQ acquiring, they were lucky to survive the pandemic and Westpac NZ dwarfs them.

3) No one is going to pay much over book for this, if Westpac really want out they'll need to be realistic.

Public service announcement: you can be your own bank with blockchain. 3rd party custodial financial services will cease to exist within 5-10 years.

Any NZ govt, must have to economic/housing stability in minds.. no matter what. Hence, the plan is for W/Pac NZ branch to be gobbled up by CCP sponsored bank/s - The only easy, silent way of fund transfer in legit way.

From mainland, to the land/RE operator in NZ. Plain simple. - So, it's never been a good time for residential housing investor .. to buy more, to 'invest'.

Kiwibank should be kept out of the conversation. They have their own issues at the moment and it's unlikely a tie-up would benefit either.

WBC (NZ) is probably too big for the NZX to swallow alone unfortunately. Relative to the size of our economy our stock market is very small.

Westpac just happens to be the smallest of the four Aussie banks so is it a signal to "Don't try and push us around or we will quit the NZ market" The banks are clearly not keen in holding such reserves. Just imagine if it was bought out by a Chinese bank, almost unthinkable a few years ago. New Zealand should have never sold out all the banks in the first place, we only have ourselves to blame.

CCP sponsored banks, will need to push. All stars aligned, NZ need to cover the cost of C19, watch the space.. the capital injection from mainland China to come via formal channel, but as usual not many in NZ & OZ are aware the modus operandi, the land must be able to be acquired first and those that purchase it/capital movement=to it's people movement. Try to do as such in India or any other countries that forbid by law for the land acquisitions.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.