Interest.co.nz journalist Jenée Tibshraeny has written today's Top 5.

She has selected titbits from recent reports and government documents that have caught her attention.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 5s here.

1. Housing and transport disjointed.

Our commutes to work are getting longer.

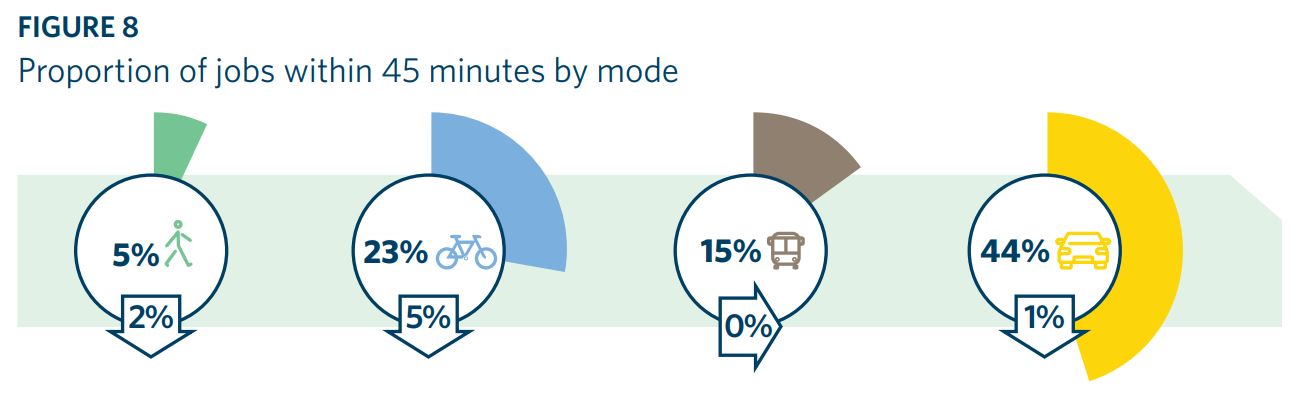

Only 44% of jobs are accessible by a car trip of less than 45 minutes, according to New Zealand Transport Agency (NZTA) research.

Meanwhile 15% of jobs are accessible by a bus trip of less than 45 minutes. Only 5% of jobs are accessible by a walk of less than 45 minutes, and 23% accessible by a bike ride of less than 45 minutes.

These 2020 findings are marginally worse than in 2019.

“This is possibly due to greenfield developments in Auckland and Wellington which have occurred away from central business districts,” NZTA said in its 2020 annual report.

Separately, research done by NZTA found only 9.5% of homes built in 2019/20 had access to frequent public transport services.

2. Treasury analyst questioned whether CPI adequately captures housing costs.

It turns out the suitability of the Consumer Price Index (CPI) as a target for the Reserve Bank's (RBNZ) monetary policy was discussed among Treasury officials earlier this year.

Emails released under the Official Information Act show a Treasury analyst throwing around some ideas with his colleagues. He said:

“I’ve been further pondering how housing enters the CPI and increasingly coming to the view that urban land is significantly underrepresented. The home ownership component only includes construction costs because the land is treated as an asset.

“To me, this unreasonably overlooks the significant consumption cost of urban land (whether measured as the direct land price, imputed rents, or mortgage costs), and inflation of urban land costs has been, if anything, the rising price of greatest social concern over the last decade.

“Urban land is included to a minor extent – it’ll be indirectly captured in market rentals and real estate fees (to the extent that these are correlated with house prices), but owner-occupied urban land costs are otherwise omitted…

“I’m wondering what the CPI would look like if it had, say, 5% weight on urban land (whether measured as direct land price, imputed rents, or mortgage costs).”

The formula for calculating CPI hasn’t changed. The above was purely a discussion that occurred following the RBNZ writing to Finance Minister Grant Robertson, opposing his suggestion for it to be made to consider house prices when setting monetary policy. The RBNZ said:

“When formulating policy, the MPC [Monetary Policy Committee] takes account of the impact of house prices on its objectives in a number of ways.

“For example, housing demand affects the demand for housing-related goods and services, such as property construction, rents, and property maintenance. Together these components account for around one quarter of the CPI weights.”

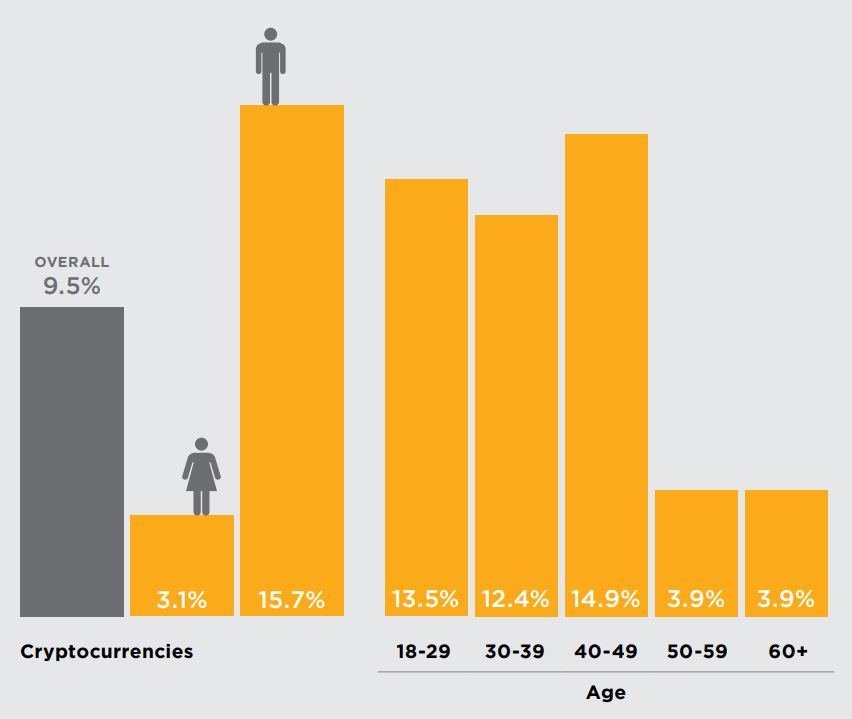

3. One in 10 New Zealanders may be crypto investors.

There may have been a tripling in the number of New Zealanders who have bought cryptocurrencies over the past year.

Of the 2,035 people surveyed in April for research commissioned by the Financial Services Council, 9.5% said they owned cryptocurrency. This is an increase from 3.1% in 2020.

According to the survey, men are the ones doing the bulk of the buying:

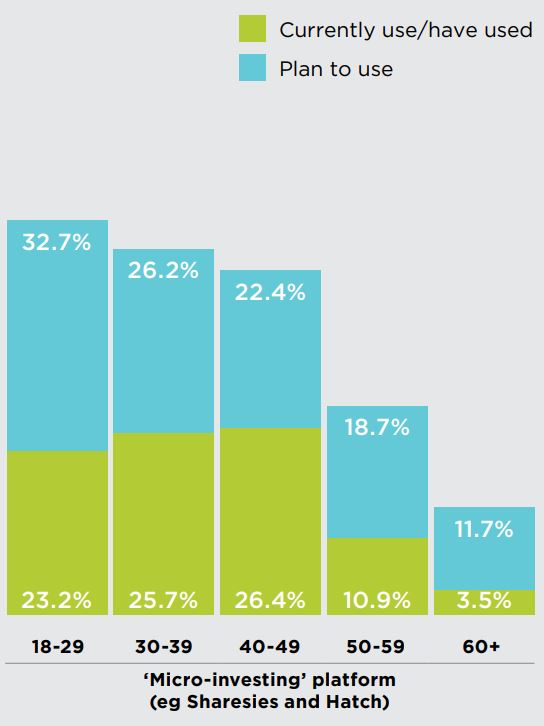

About a quarter of 30 to 49 years-olds surveyed also invest in shares and managed funds via online platforms like Sharesies and Hatch:

Low interest rates and improved technology are undoubtedly key drivers behind the push towards these investments.

4. RBNZ winds back bond-buying.

The RBNZ is continuing to wind back weekly purchases of New Zealand Government Bonds via its Large-Scale Asset Purchase (LSAP) programme.

It only plans to buy $200 million of bonds this week - the smallest amount since the programme was launched in March 2020.

Last week, the RBNZ bought $220 million of government bonds. The week before that it bought $320 million, and the week before that, $350 million.

By way of context, there were weeks during 2020 during which the RBNZ bought well above $1 billion of bonds.

It’s been an active player in the government debt market to put downward pressure on yields, and thus interest rates. It has been doing this to stimulate the economy. It’s also helped the market function smoothly at a time it has been flooded with new bonds.

The RBNZ has clarified a change in weekly bond purchases doesn’t necessarily represent a change in monetary policy settings. IE, it isn’t tightening monetary policy by buying fewer bonds.

Rather, because the Government is issuing fewer bonds than it was last year, the RBNZ doesn’t have to be as active a player.

That said, ASB economists expect the RBNZ to keep tapering its purchases all the while Treasury ramps up its bond issuance to meet its forecast issuance of $30 billion in 2021/22.

The RBNZ and Finance Minister have also agreed the RBNZ won’t buy more than 60% of the government bonds on issue/become too large a player in the market.

Since launching the LSAP, the RBNZ has bought $52.4 billion of New Zealand Government Bonds and $1.7 billion of Local Government Funding Agency Bonds.

The RBNZ doesn’t expect it will hit the $100 billion limit on the programme by the time it wraps up in June 2022.

5. A winter read for the wonks.

National MP Simon Bridges has written an interesting review for Newsroom of former Labour Finance Minister Michael Cullen’s new memoir, ‘Labour Savings: A Memoir’.

Bridges concluded:

“Naturally I'm anxious that Sir Michael will use his famed acerbic wit in some right of reply on me. But I hope he sees my high praise for a man who led with wit and acuity, made history, and has then written about it, fairly and accurately, if not with enough personal insight for my liking. Political tragics, wonkish wonks, rush out and buy.”

Bridges also set his former colleagues a challenge:

“Much has been published extolling the great deeds of our Labour-led governments. Frankly, John Key or Stephen [sic] Joyce need to come off from the golf course or yoga mat and pen a warts and all tome on their government before they forget. I fear that if they don’t, the legacy from those three terms will not be remembered as well as it could be.”

24 Comments

The driver behind Point 1 is simple. Poor planning and poorer execution at both local and national level.

Our real problem is that it is getting even worse.

Nope - the driver is Growth.

We start from a centre - typically a small village or a useful port - and we grow radially (unless we run into topographical limitations. Thus Auckland is double-whammied spatially. And we wonder that the supply-lines get longer?

"This is possibly due to greenfield developments in Auckland and Wellington which have occurred away from central business districts,"

Where else can 'more' go but out or up? Spare me.

Growth in itself is not the problem. Unplanned/unrestricted/infinite growth is. i.e. Poor planning and poorer execution.

So if you expended a large amount of energy on ill-planned and ill-executed things, energy you will never get back, what have you got. Seems like a recipe for more growth to meet the real needs. That's growth for growths sake

Actually I believe that is called increase immigration to gain GDP ;-)

Poor planning? Someone actually planned this?!

Poor planning? Someone actually planned this?!

Wow I didn't realise traffic in NZ is that bad, I guess Aucklanders love their cars. Here in Christchurch you'd have to live in the second ring of satellite towns (Darfield, Rakaia, Leeston, Amberley, etc.) to have a commute into the CBD longer than 45 mins.

For me personally anything longer than 30 mins in the car is just not worth it. I have done a 45 minute cycle commute (20 km) but you're getting exercise too, whereas when driving you need to find time for that as well.

I tried cycling to work in Auckland years ago, it was suicide. Almost got run down at least once a week and finally got bowled after about 5 months.

I miss Christchurch commutes :(

To be fair, I would love to bike or take public transport to work but the service just isn't there. Public transport to my work would take 2 hours compared to a 35 minutes drive. Have also had experiences with regards to drivers trying to kill me when biking in Auckland that I didn't have in Christchurch.

Yep, I found those stats pretty stunning too. Why do people tolerate this? I commuted to work for ~30 minutes by car for a week 15 years ago and decided that was a dumb way to live, so I planned things accordingly.

I guess we should be careful not to attract too many more people to Chch or we might end up the same way. My 10 minute cycle could balloon out to 15 minutes.

4. RBNZ winds back bond-buying.

It’s been an active player in the government debt market to put downward pressure on yields, and thus interest rates. It has been doing this to stimulate the economy. It’s also helped the market function smoothly at a time it has been flooded with new bonds.

Hmmmm ...Central banks generally follow market rates down and up when an economy justifies and can sustain that outcome. The recent NZ government 10 year bond yield low was around 0.50% in May 2020, currently ~1.75%.

Every sovereign bond issuance exercise undertaken by the NZ government has been well oversubscribed. Globally banks are increasing the percentage of bond assets held at the expense of other loan categories.

Hiccups have only occurred when there have been severe collapses recorded in other markets which call for off the run bond sales to meet margin calls.

Indeed. RBNZ will buy as many or as few bonds as they need to to keep the long-term yield where they want it. Interest rates have become a policy variable.

CPI was only ever supposed to measure one type of inflation, good which are consumed, rather than be a broader indicator of household saving and spending. That's why you've seen Reserve Banks change the measure so the UK uses CPIH and in Canada/US they use an owner's equivalent rent component to weigh housing costs in. RBNZ used to use RPI which included houses but switched to CPI over 20 years ago.

Edit to add: Although changing the measure in the middle of a housing bubble is probably not the best idea.

From memory buses from the North Shore into Auckland City Centre costs about the same as a train from Osaka to Kyoto. A taxi from the airport to the North Shore costs similar to a bullet train ticket from Osaka to Tokyo.

“This is possibly due to greenfield developments in Auckland and Wellington which have occurred away from central business districts,” NZTA said in its 2020 annual report.

Auckland Super City has many urban areas big and small. The majority land around all of them (with two exceptions) are either zoned for future development inside an expanded rural urban boundary (RUB) or do not have a RUB. One exception are the Hauraki Gulf Islands, where residents took the council to court to reimpose a RUB. The other exception is Auckland City.

Michael Cullen. the man who gave us WFF instead of tax cuts.

What a balls-up that has turned out to be - pay your tax - sustain an army at winz- claim it back as wff.

Who out there now is not on a benefit, nat super, govt employee, council employee, ACC or other public jolly?

Not many if any.

Not to mention accommodation supplement and price supplements for investment property. Everyone's on a benefit except those who are working and don't have kids.

I can claim that. Worst is not having owned assets over the last few years so missed that subsidy.

In 2014 (the last time anyone bothered to ask this question in the house) it was determined the top 3% of tax payers pay 33% of the net tax. Distributive tax regime? Tick. Fair tax scheme? Well the rich do eat 10 times more than anyone else and live in houses that are 10 times the size of the average house and as for them driving those Belaz 75710's through town (https://www.mining-technology.com/features/feature-the-worlds-biggest-m…) it's just getting ridiculous!

Separately, research done by NZTA found only 9.5% of homes built in 2019/20 had access to frequent public transport services.

That is both depressing but oh so predictable. There is so much blame to be shared, where to start? I live at the Mount and regularly cycle to Papamoa which is rapidly heading towards Maketu and in time, will no doubt swallow up Te Puke. What do I see? A sprawling, shapeless mass/mess of small single properties on ever smaller plots-some under 300sm. It's depressing.

I agree. The eastern expressway acts as a catalyst. As papamoa expands and probably Paengaroa becomes a bigger satellite town in the near future it wont be much of an expressway for long. Same in Waikato with development springing up along expressway - Cambridge getting huge, pokeno, te kauwhata and now sleepyhead town - it's just outsourcing the sprawl from one council to another.

#3

Can you explain why anyone would waste their resources surveying 2035 people to find out their crypto-currency buying habits. They don't reveal why 10% of NZers are buying crypto-currencies.

Do we feel better informed?

Would prefer these drongoes go out and interview 5000 home-buyers and home-sellers and find out what drove the people to buy or sell

More people are getting into crypto and shares because desperate times call for desperate measures. What other get rich quick schemes are there if you missed out on buying a house in time. More disposable income will be going in other directions to try and make a buck because the government killed the saver with next to zero interest rates.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.