How will the epic 30% rise in house prices we've experienced in the past year be viewed through the lens of history?

Potentially I think it could be a watershed.

Regardless of whether prices are now reined in during the course of the rest of this year, as I discussed in a column earlier this week, the massive buying spree seems certain to have an ongoing impact. More interesting than what happens for the next year or so (and I think the market over this period will be much more resilient than either economists or the Reserve Bank expect) will be what happens in the next three to five years.

We've seen a strong, I would say knee-jerk, reaction from the Government to the housing demand side pressures.

As I touched on in that earlier column, the concern is that by throwing so many restraining measures against a short term surge in the market, there may be a longer term effect that will be hard to quantify until it is upon us.

I wonder whether a lot of people have properly taken on board how far reaching some of the new measures will be, particularly those implemented by the Government in its March announcement.

Essentially, by making such big moves as the removal of interest deductibility and the extension of the bright line test to 10 years - to address a hot market in the short term - the Government is leaving a longer term legacy and maybe a toxic one for the housing market.

While the 'professional' property investors will be well up to speed with all the consequences, I do wonder if some of the more 'accidental' investors, such as those grabbing an extra house as a retirement plan, have as yet caught up with all of the ramifications.

The bright line extension, for example.

I've never been keen on the bright line test.

It was created by the last National Government as, I think, a fairly cynical measure to be seen as doing something about rising house prices while really only giving lip service. After all, given it was only for two years, there were few people likely to have been caught up by it. But 10 years is a bit different. Essentially this Government has used the existing bright line rules to construct a capital gains tax that dare not speak its name. But I think it's all been put together in such an ad hoc way that the unintended consequences have not been properly identified, let alone tackled.

I have to confess, it's only recently occurred to me that I many years ago was in a situation where - now - I would be 'caught' by this new 10 year rule.

Specifically, I travelled overseas for an unlimited period with my then wife, we rented our Wellington house - our main (only) home - out for a year-and-a-half and then found due to a substantial change in circumstances, including us splitting up, had to sell it. Because the house had been owned in total for only about five-and-a-half years, part of the profit on the sale relating to the time the house was rented out would have been taxable under the new rules.

Unpleasant surprises

Now, you have to believe that this kind of situation will occur in future. How many people are going to be surprised by it? Obviously one could avoid the risk of getting caught in this way by just selling the house before going overseas (which wouldn't be taxed because you are selling it as your main home so it's exempt) - but that does mean you've then got to start again and buy a new main home to live in when you come back. It is certainly another thing that people will have to think of. Inland Revenue's explanation of this part of the bright line test is here.

And then of course there's the interest deductibility question. Come October 1 this year then it's all change. No doubt those who own a few rental properties will be well up to speed with the requirements but, as I say, I wonder about those people who might have more recently bought a second property, lured to do so by the very low interest rates, and haven't yet worked out the sums and just what it will mean for them come tax time. I'm sure there's going to be howls of surprised protest.

I do think that as more people get their heads around these complicating factors, this could have at least some dampening impact on the housing market.

Already then there are some interesting issues and fishhooks surrounding the housing market that weren't there before.

On top of this we've then got, what I see as the keys - what might happen with inflation and what happens with migration once our borders properly open up again. These two issues between them (inflation and migration) - when put on top of the recent Government measures - are going to be vital, I believe, in setting the tone in the housing market in the next few years.

In terms of inflation, its most notable impact in terms of the housing market will be what it does to interest rates.

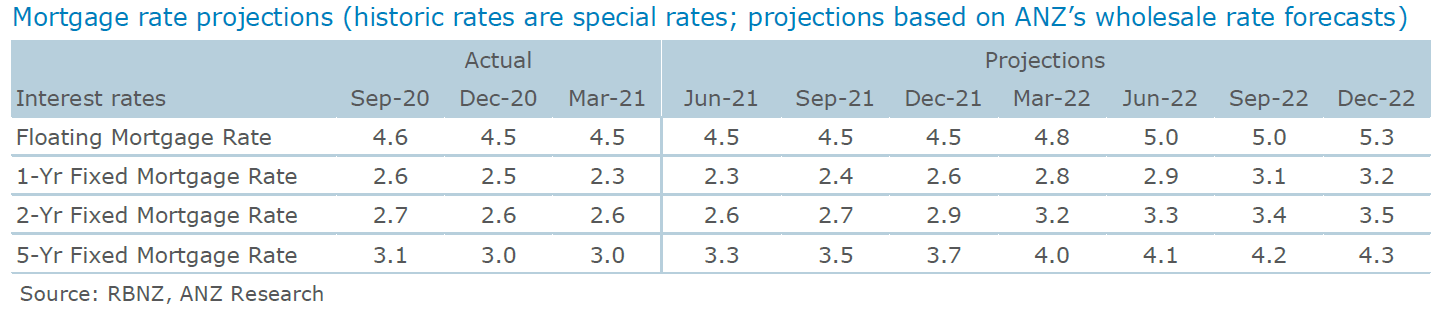

The Reserve Bank has already indicated it will start 'normalising' interest rates next year by beginning to raise the Official Cash Rate, currently at 0.25%. The RBNZ has forecast the first move potentially in the second half of 2022, though bank economists see it happening earlier. ANZ's economists now pick February as the start of OCR hikes. And in their latest Property Focus publication ANZ's economists have given their estimates of where mortgage rates may be headed as in this table:

Based on recent mortgage figures as collated by the Reserve Bank, the average-sized new mortgage is about $335,000. Running that figure through interest.co.nz's mortgage calculator and using the ANZ's examples of two-year fixed rates, both actual now and projected as of December next year, we can see that for a 30-year mortgage, someone with $335,000 outstanding would be paying $1341 a month now. If the ANZ forecasts were to prove correct that same mortgage would be costing $1504 a month as at December 2022, based on a 3.5% rate.

So, a 90-basis-points rise in the rate would produce a $163 a month increase, which equates to a 12% rise in monthly payments. And it would mean over the course of the 30-year loan someone with a $335,000 mortgage would be paying nearly $59,000 more in interest and fees at 3.5% compared with 2.6%. It's a big impact from what looks on paper like a fairly small increase.

But of course the low interest rates have allowed people to take up some heroic-sized mortgages. And while the low rates have made it affordable for people to get these big mortgages, the rises in interest rates, when they come, will have an at least noticeable impact on household budgets. This will likely crimp spending, which could have a dampening effect on the overall economy, and it will also unquestionably have a direct dampening impact on the housing market.

Then there's migration...

In recent years we've viewed this as an inbound issue, given the fact that far more people have been coming into the country than leaving. But what if the very high house prices do encourage waves of young people to start leaving the country once the whole Covid thing eventually starts to recede? It could happen - particularly since the most likely destination, Australia, is showing very strong jobs growth currently.

If the Government does stick to its current intentions with its immigration reset, then once the borders here are fully opened, a lot fewer people would be coming in. If a lot start to leave we could be looking at a reasonable outflow, which would mean less demand for houses.

The future

To me all these factors together suggest that looking a bit further out - say in a three to five year timeframe - the housing market here could face quite a few 'headwinds' as the economists like to put it.

Much will depend on what happens with inflation. If the current global inflation pressures we are seeing do dissipate as central bank leaders are hoping then concerted increases in interest rates won't be needed.

Then on migration, well, we just don't know what will happen. If large numbers of particularly young kiwis start to leave what would be the Government reaction to that? Would we see the borders opened up again to large-scale immigration like we've seen in recent times? It would be tempting for whichever Government might be in power. And it would certainly help bolster the housing market.

And then I suppose there's the question of whether future Governments may reverse either or both of the 10-year bright line test and the interest deductibility removal. There probably has to be at least a reasonable chance that a reversal of one or both of those measures could be a useful election campaigning weapon.

So, we certainly could see a situation where migration is used politically to stop the population dropping (thus helping out the housing market with demand) while, also politically, some of the recently installed barriers to particularly housing investment in the form of the deductibility move and the bright line extension could be removed. And that would pretty much revert the housing market back to where it has been and preserve its status as the investment of choice for Kiwis.

But there's plenty to think about for the future, I would suggest. Depending on which way the various moving parts do go, the housing market in the medium term might not be the sure fire one-way bet that it has always been assumed to be in this country.

84 Comments

You only pay the bright line tax if you made a profit so not really an "unpleasant surprise". More like getting a free Chocolate Sundae without the cherry on top.

If we enter a period of high general inflation will the bright line taxed profit be inflation adjusted? If not, does the bright line tax or any capital gains tax become a tax on inflation?

Tax on term deposit returns is not inflation adjusted either. I'd rather start with fixing that, if I had to.

HeavyG that kind of shows your mis understanding to the scenario put forward. That person is classed as a property investor due to the timing of a relationship split etc is then taxed on any profit. Unfortunately that persons ability to buy a home back in the same market is reduced by their marginal tax rate. I don't think the govt or public intention is to reduce peoples ability to move from one personal property to another due to relationships or working overseas / doing OE for a period. Understandable to want to modify or tax investor behaviour, but is this who they wanted to target or a negative unintended consequence that is being ignored because "that's not my situation". It is someone's situation.

"We've seen a strong, I would say knee-jerk, reaction from the Government to the housing demand side pressures"

Happy realisation.

Wonder, why interest only tool is not talked about. Many investors use it and almost all speculators. Why is it hard to impliment ban on interest only loan for house purchase as that will curb speculative demand.

Why is it hard....answere may be as both Robertson and Orr has NO INTENT but than question is, why is not talked about or raised by experts and journalist, like no mention of it in this article by David.

Also DTI was used to distract with no intent and both got away successfully.

I am pretty sure investors would prefer a ban on interest only loans rather than a ban on claiming interest deductions. Banning the deducibility of interest for investors shows plenty of intent to smash investors. The Government has effectively blindfolded investors and made them tie one hand behind their backs but you are wanting their legs cut off as well before you are willing to get in the ring.

If I buy an excavator or any other asset for a business and it's value rises; I pay taxes on it. Why should property be any different? Most other businesses and their assets make a far more positive and meaningful contribution to the economy and society, than property investors. The latter simply seeks to insert themselves between the occupant and the dwelling which they might otherwise be able to afford if it were not for the speculator.

The gain on sale of the excavator would be a capital gain if it was used in your business e.g. earthmoving business. The sale of the excavator would only be taxable if you were in the business of buying and selling excavators.

That's the distinction between capital (not taxable on sale) and revenue (taxable on sale).

I can firmly assure you that if a construction company sells plant at a price above it's book value, then the gain is taxable.

You need to find a decent accountant.

"If these assets are sold above their tax book value, then the seller must include the excess depreciation deductions they claimed previously as income in their tax return."

Direct reprint from IRD web site

If a house is sold above its book value it will be subject to depreciation recovery income as well. This no longer happens much as the law changed to make depreciation rate for buildings 0%. You're crying about a regime that benefits other capital assets by allowing unrealized losses to be deducted and then requires a square up when those losses will never be realized (when sale price exceeds book value). Stop playing the victim.

Chris-M you are being disingenuous. You are only paying back the tax deduction you previously claimed as a depreciation (tax refund) - zero sum game. Any increase in value over and above the original book value (purchase price) in your weird appreciating digger example, would be tax free.

Chris-M If you sell plant at above book value, the tax you pay is to offset the depreciation claimed against previous tax years that didn't actually occur, not because it is a true realized gain as in disposal price is larger than purchase price.

Correct.

You pay tax on deprecation recovered on the sale of the asset where the sale price exceeds the depreciated value I.e. book value = depreciation recovery income (DRI). This essentially returns deprecation deductions claimed previously on the basis the asset has lost value. If you elect not to depreciate an asset the sale will not be subject to DRI. DRI is capped at the amount of depreciation previously claimed, any gain on sale above this is tax free. Deprecation on residential property is now 0% so DRI no longer applies for houses bought after this rate was introduced.

Capital gains is not taxed generally… unless you are trading in the asset or when you bought it, your intention was to sale and make a profit. Depreciation recovered is taxable

I assume the same business offsets all of its costs too. Inconvenient not to discuss that elephant in the room.

I assume the same business offsets all of its costs too. Inconvenient not to discuss that elephant in the room.

Ban on interest only will target speculators / flippers as it is mostly used by all most if not all speculators to fund their speculative activity.

Mr Orr and Mr Robertson are aware and is the reason not banning as no intent and will be more than lip service.

So you would allow interest deductions in return for banning interest only loans for investors?

The prospects for a plummeting in NZ house prices remain bleak.

House prices in the United States rose at the quickest pace on record in May, reaching new highs due to a shortage of stock and exploding demand. The median existing home price last month was $350,300, according to a report from the National Association of Realtors, up 24% from 2020.

The phenomenon is global. House prices in the Netherlands increased nearly 13% year-over-year in May, the largest increase since 2001.

NZ is just part of the trend. What's happening here is exactly as we might expect.

TTP

Car accidents (and dysfunctional housing markets) the world over are usually due to universally common factors, exactly as we might expect.

Why does the fact that rising house prices are a trend overseas as well make it less likely we will have a drop in values here?

Because it has less to do with microeconomic local policy and more to do with global liquidity factors such as world governments printing money to stimulate economies.

Because anyone leaving a country with higher house prices to come to New Zealand will have more money to spend on property here, thereby propping up our housing market.

There are very few countries in the world where, especially considering factors such as population density, job opportunities etc, there is worse value than in the NZ housing market, a market where an housing stock of very average if not appalling quality is so wildly overpriced as to be beyond the level of a bad joke.

You conveniently forgot that US house prices crashed circa 2008 so the comparison is moot. Also compared average salary to house prices in NZ and US and you'll find the US housing market is noway near the bubble territory NZ finds itself in

When the US housing market crashed didn't people owe a lot more than the houses were actually worth thus causing them to simply walk away? Wouldn't the NZ housing market need to crash by 20-30% before some people would be in the same position?

There is a difference, as in some US Sates, in being able to walk away from the property and the debt owing compared to walking away from the property but not the debt as in NZ

True...I guess bankruptcies would go through the roof in NZ if things ever got that bad. I like the LVR restrictions gives people a bit more interest in their property even in the bad times...I believe Australia for a long time allowed 5% deposits which is sailing close to the wind!

The choices are stark. Either house prices fall very significantly, we have galloping inflation to "depreciate' houses to an affordable level, or we lose a very large number of our children to Australia.

Probably some combination of all three not very pleasant consequences.

Thank you Jacinda Ardern. This will be your legacy.

Spot on, you can get twice the house for 1/3 of the price over there. Let the emigration commence.

Simply not true when comparing proximity to jobs.

No you can not!

Have any of you actually lived in Aussie? I have for many many years and statements like this are just absolute BS!

More like 30-50% cheaper for the same standard of housing in SE Queenland.

It is getting more expensive though.

Better weather, wine, women and song to boot!

Although id agree with this Brock. Though pretty much anywhere has better women.

Great, well why don't you both go over there, and improve the general standard of the men in NZ.

Did you just assume my gender?

Im offended.

Never would have pegged you as a snowflake!

Heh. No comment.

DP

Still single ah Lord?

DP

If the Government does stick to its current intentions with its immigration reset

This is going to be a rather tough nut to crack with our low wages, insane house prices and years of underinvestment in apprenticeships and internship/graduate programmes.

My mate can't seem to find 2 engineering grads (any from mech/civil/geo) for the past 6 months. No local in their right mind would move to Auckland or Wellington for 55-65k when there are plenty jobs paying similar rates out in the regions.

Give it some time. Last year the Government brought out the TTAF (Apprenticeship Fund). It includes funding the various level 6 engineering diplomas. I myself am doing the Diploma in Construction (Quantity Surveying).

https://www.tec.govt.nz/funding/funding-and-performance/funding/fund-fi…

He is probably talking about BE(hons) grads. The construction industry is very hot right now. Doesn’t surprise me there is trouble finding grads especially if the “mate” is a small business owner not one of the major consultancies.

I call bullshit on your mate. I know several in those areas and regions who have applied for every job they have seen listed and not got a word back. In fact in those regions we pump out thousands of grads every year and most cannot get jobs in those regions to hire them (hence most now leave for overseas or leave the field). Even those at PHD and masters levels with experience are struggling to find work here. Better to leave the country I say. If the employers are just planning on hiring from overseas then at least you might have a pathway back in a few years at less than half the wage companies are paying overseas.

Migration and inflation or for that matter anything will have no effect on housing as long has support of Prime Miniter and Reserve Bank Governor.

Jacinda Arden has already assured that under her, come what may house price will not fall.

I don't understand your reasoning about the bright line test. If houses prices go up you're always better to hold it, bright line test or not. If prices were to go down you're in the same position bright line test or not. So there's no reason for the bright line test to change your decision making in the example you mentioned.

This government has shown time and time again that it's not willing to do anything to curb house prices.

The one hope is that the US and other major countries have a much better Covid vaccination rate than we do, hopefully leading to increased inflation/interest rates overseas.

With that in mind, it will be out of our control whether interest rates rise later or not. Better that it's out of our control and forced on us, than not doing anything at all.

??? The March announcements were quite harsh and a bit of a surprise for investors. So yes they have acted. I assume you are referring to actively reducing house prices rather than stagnating them. The risks are just too big for the entire economy. No sane government will do this. The best outcome for many non home owners may be for prices to stagnate while inflation slowly erodes them.

Headwinds? House prices double every seven years. You can bank on it. Property 'expert' Church has spoken.

Do you mean the self-proclaimed, unqualified, property "expert' , and failed Nat party candidate ?

I think it's entirely predictable what will happen:

-Interest rates will not rise.

-There will be an outflow of young NZers.

-There will be a resumption of massive inward migration to compensate.

No concrete action of Labour, National, or the Reserve Bank has suggested otherwise, for a very, very long time. This is what they do.

I think the most likely scenario is a little different...

- There will be an outflow of young (and not so young) NZers.

- There wont be a resumption of massive inward migration (the political worm has been turning on that)

- Mortgage rates WILL rise because that's what is happening on international money markets

Should be interesting to see what happens when boom turns to bust.

I don't think the Gov't has enough control of the civil service to reduce immigration numbers once borders reopen. They were certainly failing to do so pre-Covid despite their own stated goals, and I don't think that relationship has changed.

As for mortgage rates; I can imagine the cost of overseas funding might rise, but the RB will step in if that happens. The bond vigilantes have been taken out the back and shot some time ago; the RB can own the bond market, a la Japan, and they will do that long before they consider serious interest rate rises. If I were betting with my own money, I'd wager that we see the RB buying >90% of gov't debt before we see RB rates rising more than 2% from the present level. There's no political incentive to end the party.

INZ is moving towards a new work migration regime starting next week. Employers will need to provide evidence that the job in question was advertised at 'market rates' for similar jobs before deciding to hire from overseas.

All this while, tens of thousands of economic refugees will come in through the student visa category, obtain automatic open-working rights and continue to undercut Kiwi workers.

It seems pretty easy to game though; placing a job ad is a small tax to pay. You can simply not call anyone back when they apply, and then tell INZ that there were no suitable applicants. Then give the job to your cousin's cousin, who's agreed to work for $10/hr in exchange for the visa... business as usual.

Agreed - easy to drive a horse and cart through this requirement. The foreigner wanting to work in NZ lists his/her work experience and identifies whatever odd quirks they possess then use it in the advert along with specific narrow restrictions. So if David Hargreaves was foreign and wanted a NZ work visa he finds an NZ employer willing to advertise for a journalist specialist in financial markets and economics preferably with European experience who also has news editing experience, specify a salary a smidgen too low and add some further requirement such as 'must be willing to publish articles online for breakfast readers at weekends'. That last requirement will get you David Chaston but you get the idea.

Agreed. All banks are having spurts of low rate specials to attract high equity house owners to try to balance their portfolio. As some point one will start a purge of it low equity leveraged clients as the one that does so first will have the lowest risk. Watch for this as a signal.

& with our aging population & a struggling pension system. Losing young kiwis will be something the govt lives to regret.

A generation decided some time ago that their capital gains were more important than a functional society; I suspect they'll regret it over coming decades as they realise they live surrounded by strangers who'll only take an interest in their well-being in exchange for cash.

...

Once border is open, the government is clearly looking at importing highly skilled migrants. Young kiwis will be moving overseas. But would massive highly skilled migrants be flooding into New Zealand? Based on the pay, living cost, living standard here, what makes you confident enough to say so? What makes NZ so attractive for them? Yes, we managed the Covid situation pretty well. But how about the progress of our vaccinations? We are lagging behind which means once we open border, other developed countries are also ready to open their borders.

But would massive highly skilled migrants be flooding into New Zealand?

Nope, the sheer majority of those coming in will continue to be lower skilled. We have nothing going for us that will allow us to compete for that kind of talent with UK, US, Germany, etc.

Our universities have been sliding in ranking & reputation and high-value employers are being chased out of the country due to high running costs.

We once had decent living standards to offer but we ended up overusing that card to cash-in on importing low-skilled migrants.

We are getting more from poor countries and fewer from wealthy countries. They are not so much wanting to live and work in NZ but to avoid living in their country of origin. It is a little embarrassing when my Turkish neighbour had his kids here and then took his family back to live in Istanbul. It isn't that NZ is going backwards but we are standing still as the rest of the world catches up and passes us.

"Highly skilled migrants" is only correct on a paper. When such people arrived they are often not allowed to work at theirs skills level. And after (meny even before) obtaining NZ citizenship they move to AZ. Benefit to NZ Inc big 0.

"What makes NZ so attractive for them?" - 1).permanent residency without an expiry date; 2).pathway to enter other anglosphere countries such as Australia and Canada. If you remove one of them (especially the first one), people will stop coming.

Do I detect trolling for comments from the author? Given what we know about interest commenters..

OK I will bite

The brightline test is a messy one but then again for every person surprised to be caught out by it, they have also been certainly surprised by the capital gain achieved when they sold that property (no doubt the RE Agent exceeded all expectations). In your anecdote were you not surprised and happy to have held that property??

The "Accidental" investors of the last 2 years were taking a big leap and they knew it. There is no right of recourse that their big play in such a time of property-market-extremes doesn't (potentially) pay off. If it gets messy then FHBs might have a right of recourse and I hope our government is able to target them for support to restore the confidence of the under-30s of NZ.

If we get inflation and a rates increase, and an average mortgage increases by $163 per month, or $1956 a year, then perhaps the owner on $70,000 salary would require a $3000 salary increase (5%) to cover that. Inflation raises other living costs too so yep it feels like a bit of pressure onto mortgage holders, who haven't had any increase in pressure on them since 2008. Bless their hearts. I think however that maybe the fomo-ridden FHBS of the last decade might have been under more pressure with the ideal 20% deposit goal going up every single month in a much more significant amount than your $163.

If the drag on the market does eventuate... well I hope we will find some voices out there to articulate that this drag is necessary, just, and positive for NZ.

Well put. The rest of society is being held hostage to protect debt farming on housing. Its has to change.

The "unintended" consequence of moving to a 10 year brightline test is to make it easier to sell a switch to a proper CGT sometime down the track. Good job I say.

And how any increase in any tax will make any product cheaper is out of my comprehension. Thing gst. Is a pair of shoes cheaper with gst?

Well, there are quite a few differences between shoes and houses. There is not a shortage of shoes; your owning a pair of shoes does not prevent me owning a pair of shoes that is exactly similar in all respects; people are not out-bidding each other to buy shoes. Whether it will happen like this is unclear, but it's certainly plausible that an increase in tax could make houses cheaper if it dampens demand.

Even our own people cannot afford to live now. In 10 years time I'll be drowning in debt to buy a house, meanwhile, Auckland boomers cycle back and forth along their prestigious bridge all day.

Can't wait for the bridge!

What a time to love on the shore.

you will be waiting for a loooooong time.

People have always been able to love on the shore.

The housing situation sucks, no doubt about it.

But the bridge is such an obviously good idea. E-bikes are game changer for commuting. Would be good if we could re-discover some of that legendary kiwi ingenuity to reduce the build cost. It shouldn't take 5 years to build either.

just curious..I remember years ago when I used to live in Auckland and drive on the bridge that there were many days you could hardly keep the car in the lane because of the winds up there...a bike???? Good luck with that.

Inflation is rampant.

Restriction of Freedom of movement is the consequence of the bright line tax. No one will risk renting their family home if moving city or country for a job or other reason. So less rentals available and higher rents.

Restriction of movement is a favourite tactic of socialist governments. The next step is citizen zone cards needed for permission to move.

As a property investor it's the supply dynamic I worry about most. We have a vast amount of demand and an anemic land supply, that's essential to supporting current valuations. If the government ever opens up zoning it's game-over for us.

Tax changes are really a very peripheral issue. My guess is most investors will be able to pass through those additional costs to tenants given the tight market.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.