The great fantasy scenario in the wild world of economics is the 'soft landing'.

Trouble is, I can't ever remember too many of them being achieved. Usually you are flying along on the crest of a market boom and the next thing you on the ground, with a very sore backside, looking up at the heavens.

The latest hoped-for 'soft landing' is for New Zealand's housing market, which was last spotted heading in the general direction of Venus.

This year the events in and around our housing market have reminded me a bit of one of those nature documentaries where a group of supposedly well-wishing scientific types round up a rhinoceros and bombard it with a formidable array of tranquillising darts till the thing finally keels over and can be safely approached.

Between the reinstatement and then (from May) the strengthening of the loan-to-value ratio (LVR) limits, the Government's extension of the bright-line test to 10 years, the removal of interest deductibility on investment properties and now the probable (though note it has NOT been officially signed off by the Finance Minister yet) introduction of debt-to-income ratio limits into the Reserve Bank's 'macro-prudential toolkit', the housing market has been shot up with enough tranquillising darts to stop a herd of rhinos.

Cheerful defiance

To this point the market has appeared to do the equivalent of giving a cheery wave and a cry of: "Hi! How ya garn! D'ya want ya darts back?"

But appearances, such as the continued strength in the May housing sales figures, could be a bit deceptive. Try stopping a train quickly. It ain't easy. And our housing market is a runaway train at the moment. Too much momentum.

The expectation is that the market will slow and once it starts to slow it will do so pretty decisively.

Having said that, I do think it's clear that the reimposition of LVRs, and particularly the 40% deposit rule for investors, is not having the same sort of impact that this particular measure had when it was introduced in 2016.

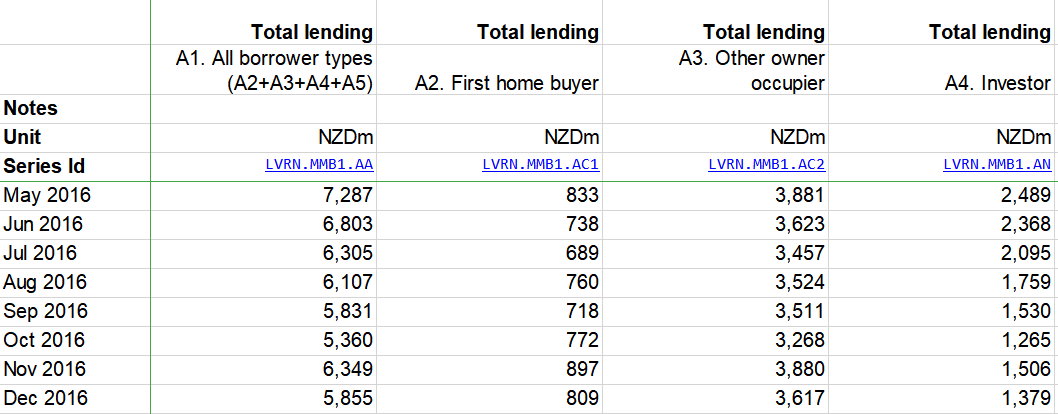

The market in 2016 was very hot (though nothing compared with now, as it happens) and in May 2016 banks advanced a record $7.287 billion in mortgages. That record stood till late last year when it was shattered by several months of new records, leading up to a $10 billion-plus month earlier this year.

In July of 2016 the RBNZ lost patience with the runaway market and hit the investors with 40% deposits. Officially that measure didn't take effect till October of that year - but the banks started applying the 'spirit' of the new rule straight away. And look what happened, according to this excerpt from the RBNZ's spreadsheet of the mortgage figures:

Just look how quickly the figures for the investors (far right column) fell - even before the official kick-off of the 40% deposit rule.

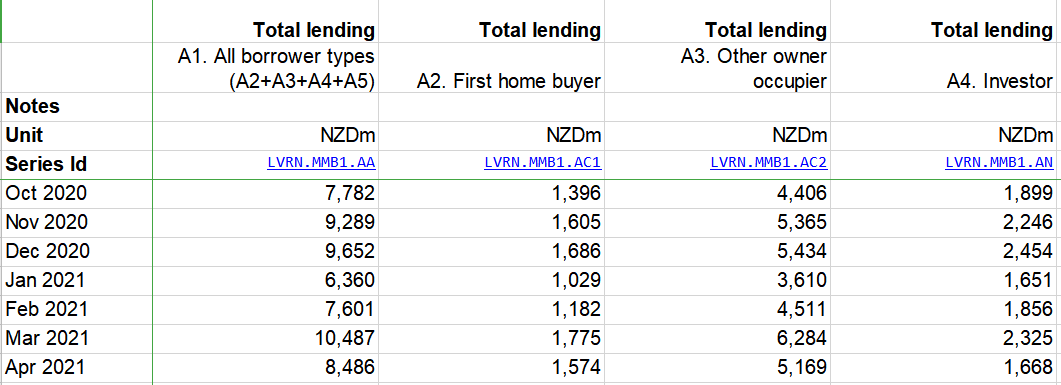

This time around the RBNZ signalled the reintroduction of LVRs and higher deposit rules for investors (though initially only at 30%) in November. And banks started implementing that soon after.

But look what has happened with the lending figures this time:

The fall-off has been a lot more gradual. The latest figures though do suggest it IS starting to happen. But those figures also suggest that the first home buyers and owner-occupiers are happily filling the gap.

The Reserve Bank is making fairly bold assumptions about what will happen to the market. Its latest Monetary Policy Statement projected annual house price inflation to be 28.5% in June of this year and then falling all the way back to just 0.4% in 12 months time. Within this, it's projecting that quarterly house price inflation will drop from an actual 7.9% in the March quarter, to an estimated 5.5% in the June quarter and then just 0.2% in the September quarter.

So, in other words the RBNZ's picking all the action (or perhaps I should say increasingly less action) to happen in the three months from the end of this month to the end of September. If the RBNZ is right then we should see some pretty sharp fall-off in activity and pressure from the July housing sales and mortgage figures onwards.

What if we don't? Already economists have been expressing surprise the market hasn't seemed to be cooling faster, particularly regarding prices.

If the market doesn't appreciably cool in the next couple of months, what then?

Plan B?

The RBNZ could of course increase those deposit limits for investor even more, to 50% or even 60%. But the interesting thing would be if FHBs and owner-occupiers appeared to be maintaining some fairly solid momentum in the market by themselves and without the input of the investors. What then?

DTIs are of course now on the horizon, but as my colleague Jenée Tibshraeny explained last week, they don't look like a priority. And the other point is, if the RBNZ has to water down the DTIs (perhaps setting them as high as debt being seven times annual income) this won't slow down the FHBs.

So, I don't really see DTIs as an issue. I think whatever happens we would be unlikely to see them for a year at least. I think the RBNZ has pushed and pushed for them because it realises they are ultimately more versatile than LVRs and our central bank did, let's face it, make a big mistake not pushing for them in 2013 when the 'macro-prudential toolkit' was established. At that time the RBNZ would unquestionably have been able to get the sign-off of then Finance Minister Bill English - but they didn't go for DTIs.

Anyway, nevertheless, I would have some concern at what might happen if the housing market doesn't appear to be slowing soon. The concern is that another hefty measure could be targeted at the market and it turns out to be the over-tranquilised dart that really deals to our runaway housing rhino. In which case, there goes the soft landing. Strap yourself in it could be bumpy.

Here's hoping not. I think the market will turn and I suspect that the RBNZ will be patient enough to wait for that. But strange things happen. Who predicted 30% annual house price inflation this time last year?

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

87 Comments

Well the problem is that we have not hit the housing market with everything have we ? Simply raising the interest rates will very quickly curb the problem but the RBNZ has been quick to drop them and clearly doesn't want to raise them. They are giving the train all the track it needs until February 2022 and by then the market will be out of sight and up at least another 10%.

Yes, we have hit it with a typical Kiwi wet bus ticket, then crowed about how much we have done.

A few things we could do.

1. Only Citizens can buy residential property

2. Cash deposits required for all residential property (no equity)

3. Increase interest rates

4. Remove the building cartels

5. Remove wasteful red tape

6. Build more (and better planned) housing. i.e. don't convert a paddock in the middle of nowhere.

May I add to that:

- IO loans only available for new builds

- Implementing DTI, hasn’t happened

- If a FHB under 20% pays higher interest rates why can investors with multiple properties get low rate? Investors rate as a business should be 2% more than standard home loans rate.

Noncents and Passerby

. . . apart from your points 5 and 6, that is all counter to addressing the needs of the 1700 of people (1.5% of the population) in motel accommodation here in HB.

Look at the housing issue being a little wider that just housing affordability for FHB.

Indeed. Let's phase out the accomodation supplement so rents can return to reality.

Oh I agree, but the main article is about cost. I have ranted throughout the years on the poor state of overall housing, poverty, etc... but thought I would stick to the issue raised on this one.

Exactly, it seems that have done enough but are not even talking about interest only loan and DTI, behave just spoken to distract and have been successful.

How hard it is to ban interest Only loan to buy house and allowed in emergency situation. For DTI, as no intend will take months, years to discuss - No will - intent is clear.

Interestingly, Minister Robertson was the one whom mentioned 'stopping interest-only-loans'. He kicked off this interest-only-loan debate.

Though I cannot say, my imaginings lead me to wonder if during some bureaucratic consulting, someone let slip to Minister Robertson the extent of leverage/interest-only-loans in the system.. and how certain restrictions might smash demand over-night.

Irrespective off my imaginings, the political will appears lacking.

The problem with interest rates isn't that the OCR is too low but RBNZ is running simultaneous market intervention programmes - primarily LSAP and FLP.

Totally agree we haven't done enough. This should be just the beginning. Other things that should be done:

IO should be used short-term (max a year not ad infinitum).

Put investors on notice to start paying interest, especially if they are over the DTI threshold being introduced.

Tax empty homes (i.e. Canada) (or forcibly take possession like in Germany - can you imagine!)

Stop investor visas for residential property development for less than 10 properties. You can easily create a company, build two houses then sell it to your trust and promptly move in. I've seen that a lot in Auckland. That's not adding to the housing stock!

Register of ultimate beneficial ownership (just how much hot money is really flowing into NZ real estate? If prices start to fall those properties will not be sticky on the way down).

Mandatory for real estate agents to collect formal identification and evidence of money flow from buyers.

I agree - but if the RBNZ stopped QE immediately, raised the OCR to 1% now, and progressively to 2.5% by end of 2022, then the housing Ponzi would drop like a stone.

So would the economy as our exchange rate would rocket and our forward sales disappear. Housing would certainly come down but hard to buy one on the dole.

A resident or permanent resident have just as much right to buy as a citizen. Some people have been here 20 odd years as PR, but opt not to be citizen for whatever reason. There's already a rule that they have to sell if they leave for more than 2 years.

I believe its time we also addressed the fees that the RE industry charges for selling homes.

Slapheid,

That name suggests a Scottish background. I agree-when I sold my home in 2003 in Milngavie, I paid 1%. Competition had brought it down from the 2% I had previously paid in 1981.

Here, the RE market resembles a cartel, though Kiwis could sort this out in short order by simply refusing to pay these exhorbitant commission rates.

Sell privately. It's easy

Hi Linklater01. Dunedin born and bred, but lived for 15 years in Glasgow and Inverness. I miss Scotland dearly, but wanted to raise the kids over here.

Underestimated how expensive NZ is to survive in though!

When house prices can double every 10 years, as they have done over the last 40 years, then NZers don't mind spending these sorts of fees. It allows the house to be seen by as many eyeballs as possible to maximize the price it sells for. People can sell privately, and save on the commission, but they may not get the best price, which you often get from a multioffer situation. But it essentially adds on 4% + to the price of each house each time it sells.

Most IMPORTANT : PM of the country and reserve bank should stop assuring / promising that come what may, they will not allow the house price to fall.

Recent survey suggested that majority wants house price to fall - How wrong Jacinda Arden is and was.

I would be interested to see the wording of the question that produced the answer that the majority want prices to fall. Marketers (or pressure groups) can get whatever answer they want by managing the question asked.

I suspect its like the congestion charges, most want them introduced, but nobody wants the impact on themselves. If the question was "would you be happy to see the value of your own house fall to make houses more affordable", what do you think the answer might be? No

How do you force the FED to lift interest rates and blow up the world sharemarkets?

Take my upvote. Exactly right, we've been dancing around one of the two main causes (interest rates being one, supply the other) trying everything BUT addressing the cause. Until they figure out how to channel debt to businesses rather than housing, the OCR will be subject to the (hopefully) unintended consequence of blowing up the housing market.

Exactly. Interest rates and DTI for investors will stop it immediately.

But they wont do the options that will work, they dont want to, its obvious.

We have not done a few fundamental changes that would have a real effect. One is not letting buyers use rolling equity on real estate to purchase real estate assets. This creates a vicious cycle that we are seeing right now. The second change we should be looking into is a temporary investment ban which could be applied and monitored on a per-region basis, letting investors back into the market once we can afford using housing as an asset and not as a means of accommodation for our families. Land price controls could also be something to look into, as long as councils don't release more land for development they could set a price cap depending on the characteristics of a given section. Land currently accounts for the larger price of the price of a home so that would have an impact.

The government have only just begun to start hitting prices. There's a vast range of options left.

I like Robinson's recent approach of hitting speculators with new expenses and road blocks one after the other until prices stop rising. It will eventually work if he carries on and then he has to pull of the rather more difficult task of keeping them from mass selling with net rental yields lower than TD in a few years time (I'd retired first).

The market has so much momentum and mass, that much like trying to steer a container ship I imagine the changes will take a while to manifest. Everything to date has been gentle. People can accumulate surplus property because the acquisition and holding costs are so low. Interest deductibility removal changes that, but gradually.

If we end up with an overshoot in building like we did in Christchurch, then vacant houses and rental properties? Just wait for the pent up demand to be satisfied. Even a backlog of 1k FHB can make the market appear to have a shortage if they're regularly turning up to open homes and auctions, until 1 month later when (according to RBNZ C31) those FHB take out a mortgage.

I don't think we'll see any slowdown until the Boomers see, with their own eyes, that there is something better to invest in. They only trust property and term deposits, maybe shares. Obviously term deposits are worthless right now. The sharemarket is overvalued, and everyone knows it. As a wannabe-FHB locked out of the market (no rich parents), I hate the situation, but I can't deny it's rational behaviour on their part.

The only thing that will stop investors is: a) interest rates rising, so mortgage rates are more expensive and TDs are more valuable; or b) the carrying costs of being a landlord on a leveraged property combined with a lack of capital gains make it seriously painful to hold property, for a prolonged time. They won't be budged quickly.

The RB is not going to raise rates. I really don't believe that it's even a possibility. They will 'warn' repeatedly, to lesser effect each time. So no generous TDs.

And neither they nor the Gov't want actual depreciation.

So for now, it continues.

brisket

A well reasoned comment. However, as you acknowledge, from a FHB perspective.

The big issue for many is actually having a home.Here in the HB 1700 are in motel and emergency housing; that’s about 1.5% of the population and there are now claims of an emerging generation of motel children. For these people, shutting out investors by whatever means and limiting investment in rental accommodation is not a solution.

Until the supply issue is addressed there is not going to be a solution and that supply needs to be both social and private housing.

Supply seems to be currently the most significant issue and despite FBB, reintroduction of LVRs (by banks last year), increasing the Brightline test, and stopping interest tax deductions the market continues to march on.

RBNZ raising interest rates may further cool the market but that is only going to increase servicing and affordability issues for FHB.

I agree that when us wannabe-FHBs are complaining about prices, it's a good reality check to think about the homeless... The same root causes are at play in both cases though.

One of the big questions for me is how much of this situation is actually about undersupply. If that's the whole story, why have prices exploded with borders closed? What if the demand is driven by price rather than vice versa? No one wants to miss out on an investment whose price is exploding, and housing supply can't increase as fast as demand, unlike financial instruments.

I wish there were someone both competent and motivated to do a thorough stock-take of NZ property, and find out how much of it is currently untenanted, being renovated, or under redevelopment. I suspect it would be an extraordinary, ridiculous, shocking percentage that would completely change how we think about this situation. But that remains a hunch, because at present there's no one properly counting.

You hit the nail on the head. All this talk about shortages and undersupply - yet prices go up the fastest when the so called fundamentals (supply vs demand) would dictate the opposite.

Property hoarding should be disincentivised. Yet we see the opposite.

brisket

Agreed; there may well be numerous empty properties.

A recent interest.co article looked at the new supply and population (including immigration) but the issue seems a lot wider.

Anecdotally;

Talking with a small group of fairly experienced landlords; with the new legislation last year they are now being very cagy about who they let to. One has just let a property; she was prepared to go well over six or seven weeks untenanted to get the right tenant and turned down over 70 applications even though many were able to guarantee rent through direct credit from WINZ.

I have a brother on a long-term (been there three years now) in Australia on work contract. His Auckland property remains largely empty coming home for family Christmas and the very occasional visit simply because no advantaged in being cashed up and whatever the property market does he isn't going to find himself shutout.

I have two lots of acquaintances in Wellington who have moved to the Wairarapa but have Wellington inner city apartments used during the work week.

I get the feel that these situations are more common than 10 years ago, so yes, "empty" accommodation could well be significant.

It's hard to stop that kind of activity, but I think there's a moral case to tax it. Something like a deemed 5% rate of return on any property other than the main residence, with married couples claiming separate main residences attracting IRD attention for an explanation. A tax rate of ~1.5-2% of the value of the second home will encourage more efficient use of a scarce resource - Maybe some with a second home reconsider, and those in your brother's position are more likely to rent out the property so it isn't going to waste most of the year.

Much simpler tax returns for investors too - ratings valuation of property * 0.05 = taxable income.

All very good points. My boomer parents have several residential and commercial properties despite not wanting to be landlords. The reason? They don't trust anything else. They've seen the stock market go bust several times in their lives. Bonds, TD's pay below inflation. Rent is a steady income that will provide them with a very comfortable 'pension'.

It's a 1-2 punch for the younger generations:

1. Money isn't going into productivity and creating employment opportunities,

2. Residential property is more and more concentrated in fewer hands, pushing up prices and widening the wealth gap.

Decision makers (politicans and central banksters) are the ones who could make a difference - but the status quo is just too lucrative for them.

At least rents aren't increasing at the same pace as house prices in NZ, but the number of empty homes is alarming. Along with the total lack of empathy.

What's the solution? Keep saving and vote for a party that openly wants lower house prices and hope for the best. This is why Labour is a bigger disappointment than National - they completely betrayed their young(ish) voters, big time. Would the Greens do the same if they got in power? Who knows. Are there any other options? TOP is dead and they seemed opportunistic at best (it's in the name after all).

Labour indeed has left all the young and youngish down. I know we are only 2 votes but how many of these ‘2 votes’ did they get on the back of their failed promises. I will not trust her again. I know it’s all virtue signaling with no real meaning.

Vote ACT to scrap the RMA. It does come with a few fishhooks though like unfettered immigration.

Exactly I do not see how our RB can raise rates if the RBA does not. They simply can not be out of synch with Australia.

Months of working group discussions, consultation and research goes into policies that benefit the average Kiwi but takes but a push of a button for programmes that effectively transfer wealth to asset-rich individuals.

A $55 increase for 'unproductive' welfare recipients is unacceptable but tens of billions in central bank printed money flowing into the pockets of asset owners without them lifting a finger at the expense of the have-nots flies under the radar of our mainstream media.

New Zealand isn't like other countries where a person can just purchase a plot of land and build a nice little house for their family. It's all about the zoning.

It's always been true that excess returns attract competition in the absence of a moat. In housing that moat is zoning that prevents supply from ever meeting demand.

Agreed. The current situation is deliberate. A conspiracy of the financial and political systems.

Efforts to slow the market are pantomime. The consumers must be appeased with the appearance of action or support. Often these efforts inflate the market further, obvious to anyone capable of second-order thinking but sufficiently complicated to avoid the scrutiny of the average consumer. For example - Kiwisaver withdrawals and first home buyer contributions.

I am waiting for some independent think-tank to run a stock-take on the broader socioeconomic costs of this housing frenzy.

For example, a recent study suggests 47% of Pacifika school students are living in overcrowded houses, emergency motels or battling homelessness by couch surfing. Then we are quick pin the blame of poor educational outcomes for our minority groups on policy failure.

"For example, a recent study suggests 47% of Pacifika school students"

Link to that study and who it was done by

Read the educational claims about the Pasifika and the following responses

https://www.kiwiblog.co.nz/2021/06/how_this_government_is_keeping_the_p…

https://www.kiwiblog.co.nz/2021/06/how_this_government_is_keeping_the_p…

In addition

2 Years ago TVNZ did an interview of 5 ladies in South Auckland who were captive of the Truck Shops and Pay-Day-Lenders

4 of the interviewees were Maori, 1 was Samoan

The Samoan Lady a welfare beneficiary who was going into debt and borrowing at exhorbitant interest rates to send remittances to her family in Samoa

During the the early months of the Covid-19 Pandemic we were bombarded by segments on TVNZ1 where school duxes in South Auckland were complaining how too many Pacifika students were being forced by their parents to leave school and get part time jobs to help their parents. Don't hear much about that now. The campaign now is about compensation for the "Dawn Raiders" including MP Sio whose family were overstayers including SIO himself who was born in Samoa in 1960 but resident in NZ from 1969

The sad part about the "dawn raids" of the 1970's is our Maori were being picked up for being brown and interrogated, thanks to the selfish actions of the pacific overstayers. Dont hear them apologising for that.

I don't think there are many that argue that housing holds back New Zealand from fulfilling it's economic potential or solving many social issues.

What motivation do the incumbents have for solving these issues? The issues are the source of their power. The victims of these issues are their electorate. Prolonging (and even exacerbating) these problems, with the appearance of trying to solve them, works in Labors favor.

That's exactly my point.

The government's idea to pour billions into several other symptoms of housing (nurses' and teachers' strikes, falling education standards, skill shortages, growing social housing waitlist) is just them distracting the public from the actual cause i.e. failure to address NZ's accommodation crisis.

I doubt any political establishment will self-inflict damage by getting an independent group to expose their own creative destruction of NZ's current and future prosperity, etc.

They have barely lifted a finger to stop the idiocy and it was clear there was an urgent need to act by last September.

Like most things in New Zealand there is no substance. It's all about virtue signalling and lip service and appearances.

At least it's killed off almost all of the desire I had to raise my kids in this country.

The damage to the economy and to society are going to linger for decades and decades to come.

I just find it so frustrating that Jacinda, when in opposition screamed across the parliament floor then to state that her generation are being locked out of owning a home and what has she done now in government? The situation went from extremely bad to absolutely dire. I’m so mad about this. She got my vote on housing.

She is lower than a cockroach.

Mine also and only on housing. It does appear that the mechanics of government are at least some of the problem, perhaps 10-20%. The mental health debacle makes this painfully clear.

Learn your lesson. Don't vote for socialists.

Don't fret. The PM, Labour (and the Greens) will be elected to govern on or before the 13th January 2024. The people know best, and they'll tell you the PM has their best interests at heart. The big issues of the day will be addressed, such as legalizing cannabis and other feel good schemes to be rolled out later in their term. To massive public approbation!

This is true and very likely. There are only fringe parties to vote for. National are beyond bad and are absolutely unable to be voted for currently. (I had previously been a National supporter).

It is not that Labour are any good but who else to vote for? Those that are able to leave should leave.

She had better hope the whole country takes up smoking it because there is no way she will get in otherwise.

We did barely minimum and waaaayyyy to late! In my view IF people are owning 80+ properties, IF investors can buy house no 25 without the money - the system is broken. Anything after your family home should be heavily taxed. OK maybe chuck in the bach as well but more than 2 properties should be taxed to the maximum.

So more homeless then?

Yes that's right. If investors don't buy them they just disappear. Its not magic, its reality.

Housing investors are a gift to humanity, buying up houses that would otherwise have gone to FHBs or even when failing to outbid others end up jacking up the market price.

Without all that money floating around!

You need investors, without them where would alot of people live and please don't say we would all be fair and even and own homes, reality is there are haves and, have not, that's life, never going to change.

Not "hit" market with "everything" at all I am afraid.

Market is driven from top end of people with a lot of money, who made a lot on markets in 2020-21 and are looking to offload into something safe as an asset class b4 it hits the fan on world markets. If want to choke that off, need to stop QE and raise rates and stop leverage and even that won't do much

Also, price rises are driven by banks lending. Set them limits and that will curtail it.

Oh sorry, cannot do that in a 'free" market

Plan B?

Put an end to this nonsense:

Banks have migrated away from lending to productive business enterprises because the risk weights can be as high as 150%.

Thus around 60% of NZ bank lending is dedicated to residential property purchases for one third of already wealthy households because the RBNZ offers them a RWA capital reduction incentive, to do so.

{kind=link}

Bank lending to housing rose from $50,788 million (48.36% of total lending) as of Jun 1998 to $307,871 million (63.13% of total lending) as of April 2021.

NZ bank depositors face more risk for virtually nil rewards while banks reap obscene profits with virtually no capital risk exposure.

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

Furthermore, remove the bank right to place a lien on residential property when a signed mortgage agreement is purchased for said collateral and most of the asset price dislocations we witness would be extinguished.

Last point is a great one.

1 person over 18 1 house max.

So investor with 5 houses with spouse and 2 children aged 4 and 5. 1 house each for investor and spouse and 1 year to sell other 3 houses or else forfeited to the Crown. That will free up supply for FHBs. No houses owned by companies or trusts.

Oh no, they can have it all but pay heavy tax on property ownership. 1 person owning more than 1 home, each year they need to pay property tax worth 20% of the home value on every additional property they own. That will teach them about paying tax for a change.

Why not 40% to capture any unpaid tax in previous periods?

Property markets are always very slow to respond to changes especially once they have gain momentum. Significant sales by investor/ landlords are coming as they start to bail from the market. Ultimately it's about supply and this may surprise over the coming months.

They are delusion if they think it will go down to near growth in 12 months, at worst I would say 10%, Labour can't deliver on anything so how the hell do the fix a complicated thing like this. Interest rates will rise more steady from next year for a few years, but even then its still cheap money, 5% type stuff

They are peddling the soft landing myth. When the New Zealand property market stops going up it's more likely to land like the Hindenburg.

I disagree, it is to large now. Would take another world wide finical crash to create even half that

It's a Minksy bubble. The fundamentals just aren't there for these valuations.

When the capital gains dry up, mortgage rates increase and the impending flood of supply comes to the market it's going to be squeaky bum time.

Nothing is too big to fail.

People have been saying this for 60 years, but here we are, I agree a slow down from these 20 plus % but 5 to 10% year on year will continue on average over 10 years. Bank on that

That's not true. Nobody was saying we had a Minsky bubble in the 1990s and 2000s.

It's only relatively recently that chasing capital gains took over from cashflow.

I agree in theory. But I think that our institutions will be willing to break anything to preserve the housing market in this country if we face a crash. Massive unemployment, total devaluation of the currency, absolutely any consequence will be chosen in preference to a housing crash. And that will be the wish of the majority of voters, too. Much like Ireland, our only escape valve for the consequences of rule-by-property-owners is emigration of the young and frustrated when times get tough.

What I miss in these commentaries is an international systems analysis. Yes house prices have grown here, but they have grown at similar speed in many other countries such as Oz, Canada, the Netherlands etc. What do countries that do well economically yet are able to stem dispropotionate house price growth, such as Germany, do differently ? Could any NZ political party, including the current one, adopt those policies without alienating NZ voters?

What do countries that do well economically yet are able to stem dispropotionate house price growth, such as Germany, do differently ?

In fact the Bundesbank has noted residential real estate accounts for 80% of total fixed asset valuations in Germany - a country once noted for it's prodigious industrial output.

NZ is not growing at a similar speed to other countries, our growth is huge when compared globally.

"The Knight Frank Global House Price Index shows that, in the first quarter of this year, house prices globally were up 7.3 per cent in the year to March 2021. New Zealand hit 22.1 per cent."

https://www.stuff.co.nz/life-style/homed/real-estate/125348365/nz-numbe…

https://uk.finance.yahoo.com/news/global-ranking-20-countries-where-hou…

What we have here is a housing market resembling a full pot of water on the boil. Where this Labour govt's 'interventions' are akin to sitting on the lid of the pot, to stop it rattling around. Whilst at the same time turning up the element.

There's still much room for upward valuation.

Be quick.

Honk Honk.

Well data or no data but a house with CV of $960000 and agent feedback was between 1.1 million to 1.25 million on higher side went for 1.525 million.

Another unit with CV of $820000 Went for 1.310 million.

Above are not cherry picking but reality.

"...... do think it's clear that the reimposition of LVRs, and particularly the 40% deposit rule for investors, is not having the same sort of impact that this particular measure had when it was introduced in 2016."

How could it, when in a year house equity has gone up by 30% to 60%, which easily covers up the the 40% LVR for many investors - No rocket science and RBNZ and so called experts should stop hiding behind such excuses.

Tax change is good but most investors, specially now buy for capital gain and not for passive rental income. Again all experts should shut up and realise that it has been over three months and still the latest data / news suggests that housing market is as hot, if not more.

Still as no intend to take action, doing wait and watch.....for how long...earlier said will have effect on 3 months, now 6 months than a year....so on keep on wait and watch.

Even world accepts now that NZ is leading in housing ponzi with the blessing of Jacinda Arden and supported by Mr Orr.

The problem is that the best that they can hope to do (politically) is stabilise prices. A lot of people have been suckered into huge amounts of debt for lousy housing now because they refused to take appropriate action much much sooner.

Unfortunately, you can't taper a ponzi and the laws of economic reality can't be held at bay forever.

Still a coin toss if we get a housing crash or extreme levels of inflation. What a choice eh?

"Hit the housing market with everything."

Really?? No more tools in the toolbox?

I think Neve might donate her Tommee Tippee Squeaky hammer to the cause.

The horse has bolted. A crash of 40% will take housing back to where it was a few years ago. It was unaffordable then!

We really need to go back to basics. State Housing built by a new State Owned Corporation - Social Housing NZ. Money has never in this history of the NZD been cheaper. Perhaps we can put a hold on Bike bridges?

What I would say is that cannot be a new department of government. Government departments, how they are run and governed is deeply broken at the moment. A state owned corporation set up to operate at arms length with a commercial board and one shareholder. Use the buying power to build a pre-fab and civil works industry.

"We've hit the housing market with everything ...."

WRONG David.

We have just talked about DTI to distract and have not implimented nor planing to do in near near future.

"We've hit the housing market with everything ...."

WRONG David

Main Silver Bullet - Interest Only Loan, which if implimented will crush speculative activity is not even talked about.

Mr Orr and Mr Robertson's are playing to distract and experts like David also gets distracted - Otherwise if do serious thinking and not fall to Orr and Robertson's distraction will realise that are only tweaking for effects only, if serious, not very hard to control speculative demand thereby controlling FOMO leading to sanity in the market BUT DO THEY ACTUALLY WANT TO ?

Builders are buying sections off the plan with settlements up to 18 months away, plus more supply to come online with the Govt. billions just released.

100% off the plan sales required by banks to developers, which are then on sold off the plan to investors and FHB to settle at same time as sections settlement obligations at a future date. Yet banks won't confirm finance until a few months prior to settlement.

Basically a lot of this extra demand is tomorrows and next year's sales up to 18 months plus ahead being brought into the present, creating an even greater supply imbalance.

Over the next 12-18 months could see even more stock coming online, all at even higher prices due to the extra costs of the artificial land supply shortage, Covid supply issues of other materials, and extra energy efficiency material cost inputs.

But how many buyers will be around at these higher prices, when many of them have bought of the plan prior?

And how many of those purchasers who bought off the plan will not have their funding confirmed by the banks?

These supply imbalances can be problematic. The "tsunami wave" effect. When all this future demand piles into today, the market reacts by ramping up and extrapolating out this surge in demand for program planning. Demand can turn at short notice, but supply is a much harder ship to steer once it's in motion.

B-b-b-b-but we thought we needed to build 10k houses per month because 18 months ago we had 10k buyers per month, what are we going to do with all this land we've just finished installing all the pipes, internet and roading for???

Japan once had a system called ‘window guidence’ where the commercial banks had a restriction on lending into the non productive sector. This system was also called a ‘war economy’ because instead of producing weapons for ww2 they switched to consumer items. When this banking system was ‘liberalised’ in the 80’s Japan consequently experienced a massive realestate boom and bust that it’s never recovered from.

A Capital Gains Tax on all but the family home. 30% should do it. You get to keep 70 cents in the dollar still.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.