By Rodney Dickens

This report reviews New Zealand’s experience with an independent central bank since 1989. It provides an assessment of whether the Reserve Bank (RBNZ) has been more the cure or the disease from an economic wellbeing or human perspective. This question is addressed first for the Dr Don Brash era (1988 to 2002) and then for the Dr Alan Bollard era (2002 to now).

Having worked at the RBNZ and briefly been a member of the Monetary Policy Committee I have taken a keen interest in how well the RBNZ has operated monetary policy since it was freed from direct political intervention in 1989.

My conclusions are:

- Don and the RBNZ get full marks for achieving the first objective of taming inflation in the 1980s. It was a painful process for many Kiwis, but this meant it required tenacity, conviction and courage on the parts of Don and his predecessors.

- In the 1990s Don was only partly successful in the context of the inflation target he was supposed to achieve, but the strict inflation target he was held responsible for meant the odds were stacked against him. Once some lessons were learnt from his pioneering (i.e. Wild West) efforts, Don’s performance should be judged as being more than adequate in the context of the inflation targets he was set. And in terms of teaching politicians to operate responsible fiscal policy. But the experience during the Brash era raised wider concerns, especially about the impact of interest rates on the exchange rate and about the impact of monetary policy on the stability of economic growth. It isn’t entirely fair to do so, but when I look at Don’s performance in the 1990s from a general wellbeing perspective, monetary policy was as much the disease as the cure.

- In the context of keeping inflation within the 1-3% range on average over the medium term, Alan can be applauded even though in ten of the quarters between the 2005 September quarter and the 2008 December quarter annual CPI inflation ran above 3%. Compared to the Wild West experience in the 1990s, interest rates have generally been much more stable under Alan’s governorship in terms of how much they have been allowed to change from month-to-month or from quarter-to-quarter, and often even from year-to-year. Despite my initial (misplaced) skepticism in 2009, Alan should also be commended for how he has operated monetary policy since the arrival of the global financial crisis.

- However, in the context of the broader responsibilities Alan was given in the September 2002 Policy Targets Agreement he signed with the Minister of Finance (i.e. “seek to avoid unnecessary instability in output, interest rates and the exchange rate”), monetary policy under his governorship has been much more a disease than a cure from a general wellbeing perspective.

- The experience with an independent central bank since 1989 should teach us to be wary of what ill-conceived experiment the RBNZ will come up with next.

In the next report I will expose the fundamental flaw in the way OCR decisions are made by the RBNZ. The flawed approach used by the RBNZ means monetary policy will inevitably be a source of volatility in economic activity and especially housing market activity, in the incomes of retired people who often have a sizeable portion of their wealth in interest bearing investments and probably also in the NZD.

The Brash era (1988 to 2002) - Top marks for beating inflation

The Reserve Bank Act 1989 specifies that the primary function of the Reserve Bank is to deliver "stability in the general level of prices”. The interpretation of price stability has evolved since 1989 from an initial strict target of keeping annual Consumers Price Index (CPI) inflation in the 0-2% range continuously to the current more flexible target of keeping it in the 1-3% range “on average over the medium term”, although from the start it was acceptable that inflation could temporarily move outside the target range “in response to particular shocks” (e.g. terms of trade shocks, changes in GST or other government charges, a natural disaster). The original approach to assessing whether the RBNZ Governor did a good job was based on inflation outcomes relative to the official target for inflation. The target is agreed between the Governor and the Minister of Finance, as spelt out in the Policy Targets Agreement (PTA).

Source: http://rbnz.govt.nz/monpol/pta/3027620.html

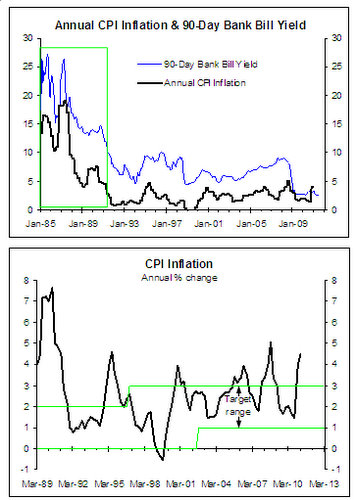

Dr Don Brash’s first responsibility after being appointed governor in September 1988, which was prior to the first PTA being signed on 2 March 1990, was to finish the job of getting inflation down from the double-digit territory experienced during most of the 1970s and 1980s. The black line in the top chart shows the history of annual CPI inflation back to 1985. Note that the temporary spikes in inflation in 1986, 1989 and most recently were GST effects (i.e. the introduction of GST at 10% in 1986, the increase to 12.5% in 1989 and the increase to 15% in 2010).

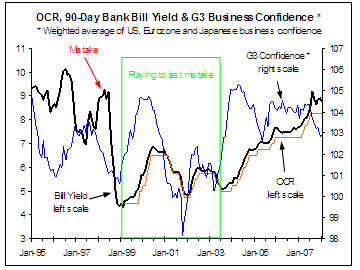

The RBNZ had been engaged in a battle against high inflation since soon after the Lange Labour Government ousted the Muldoon National Government in the July 1984 snap election. The RBNZ had made good progress when Don was appointed governor. This was achieved by a sustained period of high interest rates. Prior to the birth of the Official Cash Rate (OCR) in March 1999, the 90-day bank bill yield, the benchmark short-term wholesale interest rate, was the interest rate the RBNZ focused on most (see the blue line in the top chart). By the end of 1991 low inflation had been achieved, which Don responded to by allowing the 90-day bank bill yield to fall dramatically between 1991 and 1993.

Don and the RBNZ get full marks for achieving the first objective of taming inflation. It was a painful process for many Kiwis, but this meant it required tenacity, conviction and courage on the parts of Don and his predecessor, Sir Spencer Russell (and Dr Rod Deane who was heavily involved at the RBNZ prior to Don’s appointment).

During Don’s governorship from September 1988 to April 2002 inflation averaged 2.6%. But Don can’t be held accountable for the inflation outcomes in the first two years of his governorship because it takes around two years for monetary policy to impact on inflation. Excluding the first two years, inflation averaged 1.9% during Don’s era. On average he kept inflation within the strict 0-2% target range, but he did allow it to temporarily exceed 2% between the 1994 December quarter and the 1996 December quarter.

When Don’s transgression was to be debated in Parliament I was, by chance, discussing monetary policy issues with the Hon Max Bradford, who at the time chaired the Finance and Expenditure Committee that the governor has to regularly report to. Max had to be present in the House during the debate so his secretary seated me in the public gallery while Parliament debated whether Don should be sacked.

Jim Anderton and Winston Peters, politicians who had previously shown little interest in keeping inflation low, were baying for Don’s head on a plate. National was in power and the National MPs, who knew Don would not be sacked, had broad smirks on their faces and were baiting Jim and Winston. It was a farce (i.e. a normal day in Parliament). Monetary policy is too important an issue to leave the debate about what monetary policy should target and how it should be operated to them, or to them and government officials.

The lesson learnt from Don’s transgression was that monetary policy didn’t have a tight control on inflation in the short-term, so it wasn’t reasonable to expect him to keep inflation in the 0-2% range continuously. This was especially the case at the time because the CPI had an interest rate component related to credit services. The interest rate component meant that when the RBNZ tighten monetary policy annual inflation initially rose and when policy was eased inflation initially fell, which undermined what the RBNZ was trying to achieve.

So in the December 1997 PTA the target range was widened to 0-3% and the CPI was switched to the CPIX, which excluded the credit services component in the CPI. In the 1999 September quarter Statistics New Zealand changed the composition of the CPI to remove the interest rate component, so the target reverted to the CPI in the December 1999 PTA.

Don was only partly successful in the context of the inflation target he was supposed to achieve, but the odds were stacked against him. These were early days and once some lessons were learnt from this pioneering period and the inflation target was adjusted accordingly, Don’s performance should be judged as being more than adequate in the context of the official approach for holding the governor accountable.

'But still more a disease than a cure'

But the experience during the Brash era raised wider concerns, especially about the impact of interest rates on the exchange rate and about the impact of monetary policy on the stability of economic growth. The two issues are related because if monetary policy contributes to volatile economic cycles it will also most likely contribute to volatile cycles in the exchange rate. It isn’t entirely fair to do so, but when I look at Don’s performance in the 1990s in the context of the stability of economic growth, monetary policy looks more like the disease than the cure.

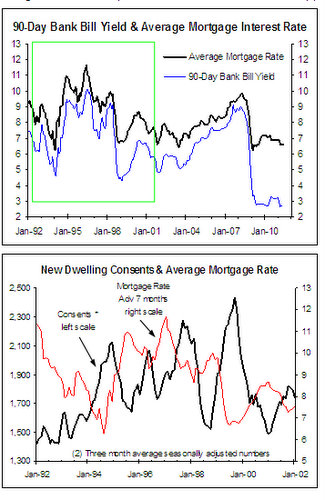

During the 1990s Don oversaw major short-term spikes and tumbles in the 90-day bank bill yield, which resulted in similar spikes and tumbles in the average mortgage interest rate charged by the major banks (see the period highlighted in the top chart).

In Don’s defense he had a strict target during much of his governorship. This contributed to him acting aggressively if it looked like inflation was heading in the wrong direction.

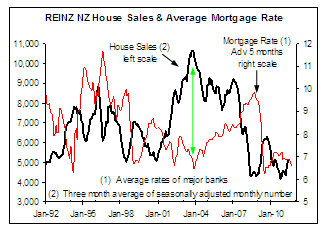

The spikes and tumbles in interest rates had major real world consequences. Interest rate sensitive industries, especially real estate and residential building, got whiplashed. The bottom chart shows that each spike and tumble in mortgage interest rates was followed roughly seven months later by a tumble and spike, respectively, in the number of consents issued for building new houses. This impacted on a wide range of firms and individuals in a wide range of industries and made planning for the future a nightmare.

'Housing market and GDP closely linked'

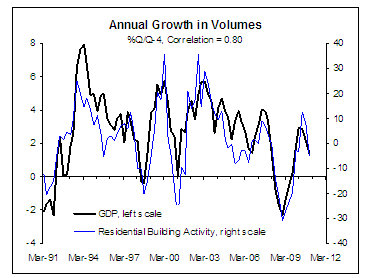

Housing market activity and especially residential building play a major part in driving cycles in economic/GDP growth, as shown in the adjacent chart. Every spike in residential building activity resulted in a sharp acceleration in economic growth. Every tumble in residential building activity resulted in a sharp slowdown in economic growth and in extreme cases recessions. The evidence clearly points to monetary policy having been the major cause of volatility in economic growth in the 1990s.

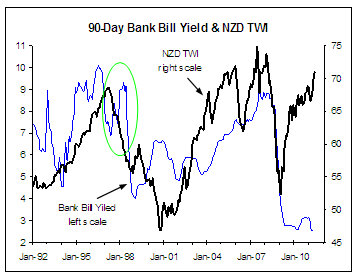

An excessive focus on short-term inflation outcomes at the time of the East-Asian crisis broke out in 1997 resulted in a recession in 1997/98. The crisis in 1997 had a major negative impact on a wide range of exporters and resulted in the trade-weighted value of the NZD falling significantly (i.e. the TWI). The RBNZ responded by forcing the 90-day bank bill yield to increase from 7% in June 1997 to a peak of just below 10% in June 1998 (see the highlighted area in the chart below). The RBNZ was motivated by concern about the inflationary consequences of the NZD TWI falling. At the time the RBNZ was using the Monetary Conditions Index (MCI) to as an indicator of monetary conditions and as a target for monetary policy.

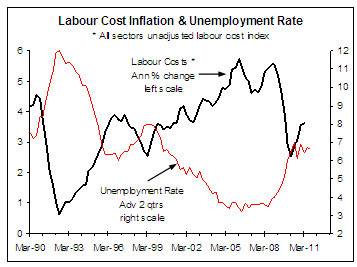

The MCI combined the 90-day bank bill yield and the TWI using a mathematical formula. It had some appeal, but it placed too much weight on the exchange rate. And it distracted the RBNZ from important issues, like the fallout from the Asian crisis and the impact of the severe drought during the 1997/98 summer. The large increase in interest rates had the normal negative impact on housing market activity and combined with the negative impacts of the East Asian crisis and the drought to result in a recession. During the recession the unemployment rate increased from 6.9% in the 1997 June quarter to 8% in the 1998 September quarter. The MCI was discarded not too long after the recession.

'Volatile interest rates'

I wrote a client report in December 1997 warning that the interest rate increases would result in a recession, but the RBNZ didn’t allow interest rates to start falling until July 1998. When the RBNZ belatedly realized that the economy was in recession, which wasn’t until the recession was all but over, it allowed the 90-day bank bill yield to fall from a peak of 9.9% in June 1998 to a trough of 4% in February 1999. This was the tail-end of the Wild West era in NZ monetary policy during which interest rates were often driven up or down aggressively in the name of achieving a short-term inflation outcome. To his credit, Don confessed to making two significant errors of judgment during his time as governor.

I have no doubt that the same average inflation outcome achieved by the RBNZ during the 1990s could have been achieved with much more stable interest rates and a much more stable economic environment. This is especially relevant to the large number of firms and individuals involved in servicing the real estate and residential building industries. But it also has consequences for exporters and importers because of the impact the volatility in interest rates and economic growth had on the exchange rate. Consequently, from a general well-being perspective, which is a broader perspective than Don was made responsible for, I conclude that during the 1990s the RBNZ was as much the disease as it was the cure.

Lessons learnt during the 1990s resulted in a change in the PTA signed between Don and Michael Cullen in December 1999. As stated in the media statement jointly released by the RBNZ and The Treasurer:

The one significant change compared to the previous PTA is that, with the new words in bold, section 4(c) of the PTA now states: "In pursuing its price stability objective, the Bank shall implement monetary policy in a sustainable, consistent and transparent manner and shall seek to avoid unnecessary instability in output, interest rates and the exchange rate."

Source: http://www.rbnz.govt.nz/news/1999/0092613.html

This change fits with my contention that the same average inflation outcome could have been achieved in the 1990s with much more stable interest rates, much more stable housing market activity, more stable economic growth and most likely a more stable exchange rate.

The Bollard era (2002 to now)

Don resigned as governor in April 2002. Dr Alan Bollard took over as governor in September 2002 after a brief period during which Dr Rod Carr was acting governor. The Hon Dr Michael Cullen, the Minister of Finance, took this opportunity to give the governor more flexibility. In the PTA signed by him and Alan in September 2002 the inflation target was amended from 0-3% to 1-3% “on average over the medium term”.

Setting aside the first two years of the Bollard-era because inflation in this period was largely the result of monetary policy decisions prior to September 2002, annual CPI inflation has averaged 2.8% if I rightly exclude the impact of the 1 October 2011 increase in GST. In the context of keeping inflation within the 1-3% range on average over the medium term, Alan can be applauded even though in ten of the 14 quarters between the 2005 September quarter and the 2008 December quarter annual CPI inflation ran above 3%, which begs the question of what is meant by “on average over the medium term” (see the bottom chart on page 2).

Like Don he allowed inflation to average just under the top of the target range, which in my book is acceptable.

'More stable under Bollard'

Compared to the Wild West experience in the 1990s, interest rates have generally been much more stable under Alan’s governorship in terms of how much they have been allowed to change from month-to-month or from quarter-to-quarter, and often even from year-to-year, as shown in the chart below. The Wild West era was thankfully over. His cautious approach to hiking the OCR during the recovery from the global financial crisis has proved to be the right thing to do despite my initial skepticism in 2009. But in the context of the broader responsibilities

Alan was given in the PTA (i.e. “seek to avoid unnecessary instability in output, interest rates and the exchange rate”), monetary policy under his governorship has been more of a disease than a cure than was the case under Don’s governorship in the 1990s.

Bollard went for growth

Alan made use of the greater flexibility the September 2002 PTA offered by embarking on what at the time I labeled the “go for growth” approach to monetary policy. With no regard for what was learnt when interest rates were allowed to briefly fall to similar levels in 1993, Alan kept interest rates below historical average levels between September 2002 and late-2004 (part of the boxed area on the chart).

In Alan’s defense he had to do a lot of on-the-job training when he became governor in September 2002, although this highlights the flaw of allowing an inexperienced governor to have free reign over the OCR. He also joined the RBNZ when it was focused on trying not to repeat the major mistake it made in 1997/98, when interest rates were pushed up significantly in response to the shock to exporters from the East Asian crisis.

What the RBNZ learnt from the major mistake it made in 1997/98 was to pay much more attention to international developments. This was still the RBNZ’s focus when Alan took the helm in September 2002. The chart above first highlights the mistake the RBNZ made in 1997/98 and then shows the high correlation between the 90-day bank bill yield and the OCR on one hand and the level of business confidence in the major developed countries/regions on the other hand (i.e. G3 business confidence) between mid-1998 and mid-2003.

This was the “playing to the last major mistake” period. For the mathematically minded, during the first half of this period the OCR lagged G3 business confidence by eight months with a correlation of 0.97 (1.0 being the maximum possible correlation). In the second half of the period the RBNZ’s response time reduced, probably aided by the September 2001 terrorist attacks, and the best fit is with the OCR lagging G3 business confidence by three months, with a correlation of 0.75.

During the period highlighted in the chart the RBNZ put lots of emphasis on consensus forecasts of global economic growth and to a large extent adjusted the OCR in response to changes in these. So when Alan became governor the OCR was already low because near-term global economic growth prospects were reasonably weak. Continuing the preoccupation the RBNZ had when he joined; Alan cut the OCR from 5.75% in March 2003 to 5% in July 2003 largely in response to deteriorating near-term global growth prospects. The deterioration was signaled by the fall in G3 business confidence between January and April 2003.

'RBNZ slow to respond'

One of the problems with the RBNZ’s approach at this time was that the consensus forecasts of global economic growth the RBNZ subscribed to were slow to react to changes in global growth prospects (i.e. economic forecasters doing what they do best). These changes were picked up earlier by indicators like the G3 business confidence index shown in the chart.

This meant the RBNZ was always slow to respond.

But it didn’t take Alan long to stamp his authority. He ignored both the surge in G3 business confidence during 2003 (blue line, top chart) and the supercharged growth in NZ residential building activity and GDP in 2002-03 (bottom chart).

Alan was intent on trying a new approach to monetary policy. He experimented with a low OCR, which meant the 90-day bank bill yield and mortgage interest rates ran at levels that history had taught us would result in an inflation problem. The RBNZ forecasters and the bank economists played along by predicting that an inflation problem would not result from the sustained low level of interest rates. And many business people and others were willing to go along for the ride because they didn’t appreciate the ultimate consequences of the “go for growth” experiment.

But inflation takes no notice of economic forecasts based on wishful thinking. The experiment with low interest rates initially resulted in a period of strong GDP growth, which drove the unemployment rate to well below average or sustainable levels between 2002 and 2004. The tightening in the labour market resulted in labour cost and general price inflation heading to the highest levels since inflation was temporarily defeated in the late-1980s.

'Go for growth created inflation'

The chart below shows that the fall in the unemployment rate during Alan’s “go for growth” experiment resulted in Statistics New Zealand’s all sector annual labour cost inflation measure increasing significantly with a lag of 2-3 quarters.

The increase in labour cost inflation wasn’t based on higher productivity growth that justified higher real incomes. It was the bad sort of increase that was caused by too much stimulus to demand from low interest rates and resulted in firms putting up prices, which meant it didn’t achieve a sustained increase in real incomes.

Inflationary labour cost increases driven by a “go for growth” monetary policy experiment risk setting in motion a destructive and distracting wage-price spiral of the sort that was endemic in New Zealand the 1970s and 1980s. And even worse, it is just stealing economic growth from the future. This became evident for all to see when Alan responded to the inflation problem he had played the major part in generating by hiking the OCR from 5% in December 2003 to a peak of 8.25% in July 2007.

'He engineered a recession to solve the inflation problem he created'

Alan was effectively forced to engineer a recession to solve the underlying inflation problem, not that he would ever put it this way. But he needed to get the unemployment rate up to a level that returned balance to the labour market rather than the artificial tightness that was temporarily achieved by his experiment with low interest rates. The global financial crisis brought forward the recession NZ was heading for anyway and meant the economy suffered more than would have happened otherwise, but a recession was unavoidable at some stage.

This chart below shows that mortgage interest rates are the single most important driver of cycles in the number of house sales reported by REINZ each month. This chart shows that Alan’s experiment with low interest rates was a key factor driving the exceptionally high number of house sales in 2003-04.

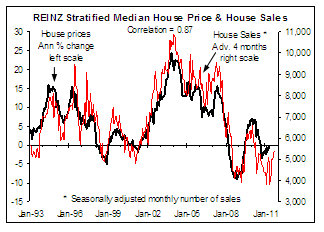

The chart below shows that the exceptionally high number of house sales in this period resulted in a speculative bubble in house prices, with annual house price inflation peaking at almost 25% in November 2003 based on the REINZ stratified median house price. The left chart also shows the major part the massive increase in interest rates between 2004 and 2008 played in slaughtering the housing market.

Alan could have achieved the same average inflation outcome without having fuelled a mega boom-bust cycle in the existing housing market, which was also experienced in the residential building market and by the wide range of industries that service the real estate and residential building industries.

The boom-bust housing market cycle Alan sponsored between 2002 and 2008 made the short-sharp cycles in the housing market during Don’s Wild West era in the 1990s look insignificant by comparison.

Unfortunately, the speculative bubble in the property market that Alan’s experiment with low interest rates played a significant part in fueling ultimately resulted in many casualties:

- People losing money in finance companies that got caught up in the property boom, which was particularly painful for a lot of retired people who had no ability to make up for the losses.

- Investors burnt directly when the speculative bubble in the property market burst.

- Small businesses that setup or expanded during the housing and economic boom between 2002 and 2007 getting hit hard when the bubble in the property market burst and the recession arrived.

- The large number of people laid off during the recession.

'Bollard's mega cycle failure'

There should be little doubt that during the Bollard era monetary policy has been more the disease than a cure. Yes, Alan did away with the Wild West era of interest rates, but instead of short-sharp cycles in interest rates he imposed a mega-cycle that resulted in much greater damage from a general wellbeing or human perspective as well as from the perspective of the stability of output. His experiment resulted in a protracted period of strong growth in output followed by the worst recession since the early-1990s. A major recession was an inevitable consequence of his “go for growth” approach to monetary policy. The global financial crisis made the recession worse, but we were heading for one even before it arrived.

Alan will have learnt lots from almost a decade of on-the-job training and probably won’t repeat the ill-conceived “go for growth” experiment, or at least not on the same scale as he tried in the 2000s. But the history of independent monetary policy in New Zealand after it initially did an excellent job of breaking the back of an entrenched wage-price spiral in the late-1980s has been a minefield of misguided experiment after experiment. The human face of the experiments includes:

- Many businesses facing a much more volatile economic and industry environment than was necessary for the RBNZ to achieve its primary inflation target, which is especially relevant to the real estate and residential building industries.

- Retired people facing much more volatility in their fixed-interest incomes than was required.

- Employees experiencing unnecessary windfall gains and lose in the labour market.

- Investors facing an unduly volatile environment and one that tempted unwary investors to get caught up in the boom-bust property cycle that Alan’s “go for growth” experiment largely caused.

- Exporters and importers most likely facing larger variations in the exchange rate than was necessary.

The experience since 1989 teaches us to be wary of what ill-conceived experiment the RBNZ will come up with next. My concern is amplified because there is a fundamental flaw in the way the RBNZ makes OCR decisions. The framework the RBNZ uses makes it susceptible to delivering excessive cuts and hikes in the OCR.

'Bollard's great job after GFC'

I believe Alan has done a great job since the financial crisis arrived, but I see no reason to assume that he has learnt enough to avoid the major pitfall inherent in the approach used by the RBNZ to make OCR decisions. And even if he has, the next time we have a new governor the odds are probably high that new mistakes will be made or old ones repeated if a superior framework for making OCR decisions is not in place.

The fundamental flaw in the approach used by the RBNZ to make OCR decisions will be the topic of the next report.

* Rodney Dickens is the Managing Director Strategic Risk Analysis. See more detail here.

17 Comments

Growth doesn’t happen - and is the wrong goal anyway.

Everybody around the world is competing for less money, but with increased costs.

Where are the 170’000 decent jobs coming from - PM ?

A reasonable good NZeducation system, providing young Kiwis with the potential to compete internationally in many sectors is constantly abused by the government not supporting the private sector, but allocating well paid work to China and other nations. A government, which is to blame of wasting billions of taxpayer’s money by draining our national “Brain/ Knowledge Capital”.

As a consequence our ministers proudly explain their spending in the billions on infrastructure – HA – including more prisons, boot camps, welfare programs, the extension of the police force, etc. – what a “Mickey Mouse Economy” !!

Planning - YES !

Considering the worldwide economic/ financial, environmental and political circumstances and the severe consequences nothing is more important for a small, remote country then good central planning - now. The private sector and government sitting together planning (mixed economy) and executing actions for the future of this country.

The parties aren’t enough engaged in these processes, but disconnected - making regularly unwise, even stupid decisions against the wellbeing of the NZpopulation – the private sector – the NZworkforce. The results are obvious.

There should be little doubt that during the Bollard era monetary policy has been more the disease than a cure.

Amen to that. But the other disease that afflicts this economy (fiscal policy that encourages investment in non-productive assets) is probably even worse.

Thank You for the insights into the RBNZ Rodney.

Perhaps you could help me with a very fundamental question regarding our monetary system.

Looking at the RBNZ figures and historical data we see that the total debts outstanding have been rising for about forty years at about twice the growth in nominal GDP. If the debt growth drops a bit we fall into recession and the Government starts running deficits.

How long can this continue and can we ever reduce the total credit market debt to GDP ratio without a massive depression and mass debt write off or extreme inflation?

Your comments appreciated.

KiwiDave,

Good luck getting a central bank economist admitting to that. The banks have relied on the explosion of debt to provide their shareholder's with profits and fund employee bonuses. And they rely on the willingness of politicians and greater society to accept liability for their losses due to their negligent actions.

They're even now complaining about the increased capital that they have to hold to back their customer's debts.

Graham Turley, ANZ's managing director of commercial and farming lending, said the rules meant banks had to hold more capital. "That's an additional cost to our business so the immediate conclusion is ... eventually that will be passed on to farmers.

"You can't ask organisations to carry more capital and expect them not to get a return on it, and that's a fact."

Mr Turley said it was impossible to argue against the Reserve Bank's aim – to reduce vulnerability in the financial system – but ANZ disagreed with the risk models and had argued for the changes to be delayed.

"Their view is, as an industry, we're not holding as much capital as we should be if there's an armageddon situation. So based on their models ... we should be holding a little more. Are they right? Possibly. Are they wrong? We think so."

http://www.stuff.co.nz/dominion-post/business/5139450/In-debt-farmers-face-more-pain

The really interesting issue is: is central planning of the interest a good idea?

Central planning of the interest rate is not a free market feature, it's a socialist feature. And as socialism has never worked, this won't work either.

Abolishing the reserve bank is the only cure.

abd Capitalism dies at the top of the Gaussian. (Needs growth, fails at the mid-supply point).

oh dear.

Maybe we have to come up with something else.

I agree that central planning of the interest rate is a kind of socialist feature and that it has negative outcomes, but I would argue that your claim that socialist doesn't work is empty rhetoric, the West has employed differing degrees of socialism in governance since the 17th Century with varying degrees of success. To argue socialism doesn't work is just pure ignorant drivel.

Under a central banking system, the price of money (interest rates) that banks outside the central bank charge is not set by competition between these same banks but by the monopoly authority of the RBNZ to raise (or drop) the OCR at will. Then there is fractional reserve banking...

Socialism never worked as it was outsepent (debt) by Capitalism....funny.

All being equal in access to resource etc., whichever economic/political system out performs others may very well dominate eventually. It seems China is doing so at present. Time will tell of course.

Sadly, most 'system' failings relate to the human foibles especially greed of those in control. In this current world, I do not see capitalism being any better than communism in this regard

Both are forms of establishing dictatorships, particularly when the free market is not free of monopolies.

Very interesting analysis.

And on the Fed/corporate welfare and other matters - this from Ron Paul;

http://www.zerohedge.com/article/complete-ron-paul-highlights-last-nights-new-hampshire-debate

Is it going to be a Ron Paul win at the 2012 US presedential election? I bet you can say goodbye to the government bond market if he does. Just imagine, the US government wont be able to increase the amount of debt the nations taxpayer has to pay simply by creating a new number. Now only if we could learn that one here in NZ...

When Rodger Douglas became finance minister he deregulated the banks who immediately created billions of dollars. With all of this money the banks were desperate for borrowers (ask Olly Newland, they were trying to get him to borrow millions, he got a shock, that's what he and others said in the doco at the time). Further it created many high flyers with many millions of borrowed dollars to buy out companies both here and in Australia. This massive growth on the money side of supply and demand, caused an explosion of inflation, which led to the extraordinary high interest rates that were imposed at that time. To blame all of this on Rob Muldoon is a cop out and a cover up for the cowboys in charge at that time. You either believe the supply and demand theory or you don't. Avoiding truth can put even a good article into disrepute.

Brash and Bollard might have failed but the banks scored big time...here's why...

"More than any other industry, large banking has the guarantee of high profitability and success. The bankers know that the government will not allow their banks to fail. So, they can take enormous risks based on the discrepancy between short-term rates (at which they borrow) and long-term rates (at which they lend).

When the spread reverses, which it always does at some point, driving up short-term rates and driving down long-term rates, the result is a recession. If a very large bank faces bankruptcy, the central bank intervenes and lends to it at low rates until the old yield curve (spread) returns: low short rates and high long rates. If central bank intervention is not sufficient, then the government intervenes and uses tax revenues to offer more bailout money to the biggest banks.

This arrangement has created a class of super-rich people. The arrangement is ideal for them. When they win, they win big. They do not lose, except when their bank is judged not quite too big to fail. Then the bank gets bought up at a discount by a TBTF bank. The government arranges the terms of sale"

http://www.marketoracle.co.uk/Article28689.html

NOTE: "created a class of super rich people"

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.