Two of the main factors used to justify the five OCR cuts Governor Wheeler has delivered over the last year will not have the impact on the economy assumed by the Reserve Bank and the economic forecasters in general.

Specifically, the negative impact of the fall in dairy farm incomes on economic growth is greatly overstated as is the relevance of the fall in expectations of future inflation.

The housing market has for some time been telling us that interest rates are too low while the labour market is starting to quietly ring the warning bell about future inflation risks.

With much of the boost from the OCR cuts still in the pipeline the labour market will head more into inflation risk territory before the governor realises his mistake.

The misguided OCR cuts pose a range of opportunities and threats.

When the main justifications for OCR cuts are flawed it is time to get informed

Since June 2015 Governor Wheeler has delivered five OCR cuts while some bank economists continue to argue that he should cut at least once more. The large fall in dairy farm incomes was used as a major justification for OCR cuts initially on the basis it would have a significant negative impact on economic growth. Recently the justification for cuts has shifted more to the fall in expectations about future inflation. Low inflation expectations are supposed to mean inflation will remain too low, justifying OCR cuts to boost economic growth and inflation. The problem is both these justifications for OCR cuts are flawed.

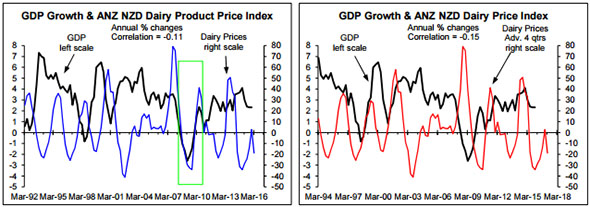

The historical experience says dairy product prices have little impact on economic growth. The left chart shows no clear link between the annual % change in dairy product prices and annual GDP growth. Falls in dairy product prices are more often associated with above average than weak GDP growth. This is the case even if I allow 12 months for changes in dairy product prices to impact on GDP growth (right chart).

Other factors generally swamp the impact of changes in dairy farm incomes on economic growth although in extremely rare situations, like the experience following the emergence of the financial crisis, the other more important drivers can line up with a fall in dairy product prices and cause a recession (see the boxed area in the left chart above). But this is the exception that proves the rule that dairy product prices are of little relevance to economic growth. With only a little over 12,000 dairy farms nationally there aren't enough of them to have a major impact on economic growth even if they cut spending significantly; especially in the current situation in which super-charged net migration is adding around 70,000 people to the population per annum and interest rates are at the lowest level on record.

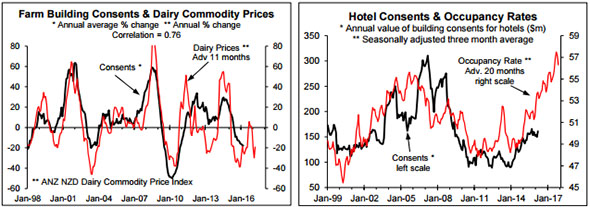

Certainly, the fall in dairy product prices is resulting in a large fall in consents for farm buildings (see the left chart below that shows the annual % change in dairy product prices leading or advanced by 11 months relative to annual growth in the value of consents for farm buildings). But why focus on this when the other contender for NZ's No. 1 export earner - tourism - is booming and the high occupancy rates in commercial accommodation point to further significant upside in consents for hotels, motels and other short-term accommodation after advancing the occupancy rate by 20 months (right chart).

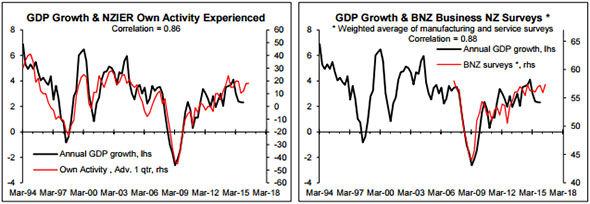

Rather than support the view that economic growth is going to slow more after the recent slowdown or remain low, the most useful leading indicators of near-term economic growth point to it running around 3.5- 4% although they aren't always reliable (two charts below).

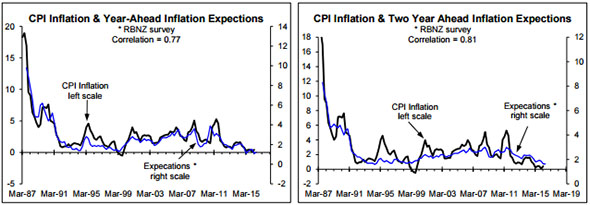

More recently the focus of those calling for OCR cuts has been on the fall in inflation expectations. The left chart below shows the relationship between the Reserve Bank's (RB's) survey of year-ahead inflation expectations and actual CPI inflation and the right chart shows the relationship between the RB's survey of two-year-ahead inflation expectations and actual inflation. Year-ahead expectations go up and down with actual inflation. Periods of low year-ahead inflation expectations have often been quickly followed by rebounds in inflation. The RB's survey of two-year-ahead inflation expectations is less reactive to the shortterm swings in actual inflation than is the one-year-ahead survey, but it still largely moves with actual inflation rather than being predictive of future inflation (right chart below).

Evidence the OCR cuts are unfounded and implications for businesses and investors

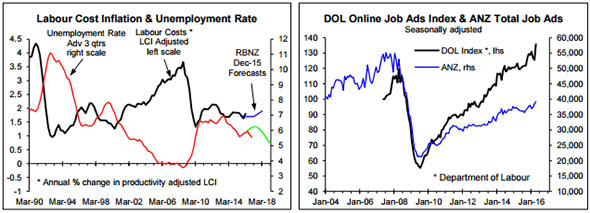

While the housing market provides the first indication if interest rates are too low, the labour market is where the more important inflation implications of excessively stimulatory monetary policy get confirmed. It takes several quarters for excessively stimulatory monetary policy to be reflected in a falling unemployment rate and several more quarters for it to be reflected in upside in the purely inflationary component of labour cost inflation (i.e. the increase in labour costs that isn't justified by productivity growth and will therefore boost unit production costs and encourage producers/employers to put up prices).

The left chart below shows that the unemployment has fallen in the last couple of quarters when a two quarter moving average is used to smooth the volatility in the quarterly numbers (red line). This contrasts with the RB's December prediction that it would increase (green line) and predictions of upside by most of the bank economists (use the following link to the October 2015 Raving that criticised the Westpac economists for predicting a rising unemployment rate). The fall in the unemployment rate is consistent with GDP having grown at a 3.5% annualised rate in the second half of 2015 (i.e. it shouldn't have been a surprise to the RB and other forecasters). While surveys of inflation expectations provide little if any insight into future inflation, the unemployment rate is a pretty accurate leading indicator for productivity-adjusted labour cost inflation. The peak correlation at -0.84 (akin to a 84% mark in an exam) is with the unemployment rate leading by three quarters, with this reflected in the left chart by the unemployment rate line being advanced or shifted to the right by three quarters.

In my assessment of the historical experience, if the unemployment rate falls below around 5.5-5.8% (i.e. around the current level) it will fuel, with around a three quarter lag but at times with a slightly longer lag, higher productivity-adjusted labour cost inflation than consistent with Governor Wheeler's 2% CPI inflation target. If GDP growth continues to run at around the recent rate of 3.5%, in line with what the leading indicators are suggesting, the unemployment rate will continue to fall. The somewhat volatile job ads indicators are suggesting employment growth prospects are strong (right chart above), which is vaguely consistent with what the leading indicators of GDP growth are predicting.

It takes around a year for OCR cuts to fully impact on economic growth and a little longer for them to impact on the unemployment rate. The obvious implications of this is that the fall in the unemployment rate that will occur as a result of the five OCR cuts delivered over the last year still lies ahead. The risk appears to be high that the OCR cuts will fuel higher productivity-adjusted labour cost inflation over the next couple of years allowing for the normal lags in the process. Having not predicted the fall in the unemployment rate, the RB and the economic forecasters are playing down the implications of the fall while some of them are calling for one OCR cut that will only drive it more into inflationary territory.

If I am right in suggesting the OCR cuts were the result of excessive focus on factors that have little if any bearing on the medium-term inflation outlook Governor Wheeler is supposed to focus on, it will have major implications on a range of fronts. This includes house prices, residential building, interest costs, labour costs, consumer spending and the exchange rate. To find out what the implications are for these areas and others I suggest you enquire about our pay-to-view reports if you don't already subscribe to them. In my assessment the outlook on a range of fronts is significantly different to the consensus view meaning we can more than ever provide valuable insights to our clients; insights you won't get from the bank economists or the RB's forecasters.

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.

22 Comments

Without even looking at all your charts, I can tell you that it is unlikely that inflation is going to go much above the 1-3% target any time soon. And even if it did, the governor can very quickly stop it with just a small rate rise. And even if he couldn't, a couple of years of 'catch up' 4% or 5% inflation wouldn't be that bad. I wouldn't mind a pay rise this year!

The Fed is out after next week’s MPS, and their call will have a much greater impact on the currency and the long end of our curve than the RBNZ possibly could. We have two back to back MPS’s, so there is an opportunity in August to revisit the OCR with a full statement. Given this and the points you make above holding the OCR, with data dependant easing bias, would be the best call.

What inflation? Any inflation that will appear is not influenced by the actions of RBNZ at this time.

We have received this comment from a reader by email:

"The goose continues to lay its annual golden eggs of 'negative gearing' and 'tax-free capital gains (after two years)' for investors who buy houses. The Government pushes the line that immigration and lack of land have pushed housing prices to never-before-seen levels. This is disingenuous.

Recent reports indicate that 80% of houses in Otara were bought by investors and the figure throughout Auckland is close to 50%. Why? Because, for investors, it makes 'tax sense'. It makes very little sense for first-home-buyers or the vast majority of people who pay PAYE, or pay tax on their minuscule savings interest received, or who can't afford the now-excessive rents.

What are the chances of Government changing the rules, to remove negative gearing and impose say a 30% capital gains tax on investment housing - doing it immediately, not 'perhaps' at some future time? Parliamentary disclosures show that many politicians, especially National, own significant housing investment properties. Can they really be trusted to disturb their nest eggs or the nest eggs of their supporters? But change the rules they must to puncture this housing bubble, and media should be at the forefront of continuing pressure on the Government.

Removing the golden eggs will make many housing 'investments' uneconomic. Many, many homes will come onto the market - prices could fall dramatically. Banks will squeal - their $5 billion of annual NZ profits will take a hit - how sad - but they will recover (see Ireland) and might then reflect on the wisdom of lending huge sums at very low interest rates to sustain a housing crisis. The Government line of 'encouraging' the freeing up of more land and building more houses will take many years, perhaps a decade or more, and will do nothing for first-home-buyers now, or over the next few years. Prices have to drop, not just flat-line or rise more slowly.

Investors will squeal - tough - you have had it too good for too long. The vast majority of New Zealanders, though, will applaud, as house prices come back within their reach. Most of 'middle NZ' are not property investors, and lower income NZers are certainly not. There must be a winning percentage of votes here for a political party?

Mark Gilmour"

Unfortunately, I think this idea fails in understand that consumer spending is the single biggest driver of the NZ economy. To be able to quantify the impacts of a fall (say 5%, 10%, all the way to 30%) in house prices on consumer spending would be very interesting, but extremely speculative from an analysis POV. The govt is well aware that there is a relationship between house prices and consumer spending. They will be extremely concerned about the negative impacts of price falls for the sake of the wider economy but also for their own self preservation. I also think it's important to realize that falling consumer spending creates its own inertia, so a fall in house prices that impacts consumer spending will put further pressure on house prices. This may not be immediately obvious to some and you never read about the relationship in the media or hear it discussed by politicians or talking heads.

Disagree, I think you obfuscating the subject. I think the original corespondent is fundamentally correct. an immediate tax on capital gains of investor housing of 30% would cause many "investors" to pause, but i also think it is not enough. Regulate to cap rents, but then another commenter has said it before, our political parties are too much in love with the "free Market" without realising that it is not free of manipulation.

Good comment, but I think it's slightly naive to believe any government will do enough on this issue. It's gone too far for too long now. So many people with vested interests that ignorance is bliss for them.

It WILL take a crash IMHO. My prediction for that crash remains as happening somewhere in and about 2018.

If they are too scared to tax a 2 year+ capital gain then bank term deposits for over 2 years should also be tax free ! ?? !

Good article Mark, you may be right but it doesn't change that it is wishful thinking. Also if house prices were to fall significantly, many many loans would default. You may think "good then I can buy a cheap house" but the loan defaults would lead to bankruptcies, business closures, staff lay-offs, there would be blood on the streets and you will still not be able to buy your cheap house when you don't have a job.

Yes, that is why bubbles are not good because of the externalities.

Brave & interesting contrarian article Rodney Dickens. I'm a bit dubious because of the sales pitch to pay your company to get more data at the end of it though

I was surprised to hear that Rodney reckons interest rates are too low when real interest rates have been on the up! He is wrong to concentrate on nominal interest rates when it is the real rates that are more closely related to the decisions made to invest in real assets. If NZ can expect to have high real rates relative to the rest of the world then New Zealand should also expect to have lower growth relative to what is possible and increasingly poorer per capita increases in incomes than the rest of the world. It is no very useful for Rodney to use historical graphs from periods of significantly higher inflation to somehow portray the current environment.

The problem with looking soley at whats happening in NZ , is it ignores the fact our interest rates are higher than elswhere , with no apparent reason. To not cut would magnify the difference with Australia.

The developed world has zero or near zero interest rates.

NZ is part of the developed world.

NZ is constrained by the interest rates elsewhere, unless NZ wants parity with the US or overshoot.

NZ interest rates are significantly higher than other countries.

The RBNZ wants to kickstart inflation and consumer demand, but the Govt have the floodgates of foreign property buyers and immigration etc driving up Auckland house prices

The OCR is only 0.25% lower than 2 years ago (raised 4x & lowered 5 x)

I think we'll still continue our OCR race to the bottom, as it's not looking good on the US job front so unlikely that the Fed is going to raise rates any time soon.

BBC article: US job creation in May falls to lowest in five years

http://www.bbc.com/news/business-36444516

Heaven forbid the thought of the masses possibly getting a pay rise, oh no we can't have that, meanwhile house price inflation is beyond out of control, with not the slightest being done about it, other than meaningless rhetoric, how did this country become so backward? oh that's right the nats keep getting voted in.

NZ is best to just enjoy the lower rates while we still can.

A crash induced inflation monster will run loose soon enough.

The housing market is no longer responsive to interest rate changes as other factors are overwhelming house price rises.

Wage rises are low to flat due to high immigration and generous work allowance rules for international students.

Yes, keep the peasants too scared to ask for a wage rise by bringing in plenty of cheaper labour.

OCR cut does not matter to overrseas buyer.

A year ago, RD wrote a similar piece for this column, so at least he is being consistent-and consistently wrong. He believes that interest rates are too low for the health of the housing market, completely ignoring the effect of investors, many from overseas, for whom our interest rates are irrelevant.

He should have read Bernard Hickey's article before talking up our growth rate. As Bernard and other commentators have pointed out, on a per capita basis, our growth rate is far from flash. Brian Fallow pointed to our poor labour productivity recently, where we compare badly with other OECD countries.

What would happen to our exchange rate, if we were to have, not a lower, but a higher OCR? He might just want to ask our exporters for their views on this. Tradable inflation would fall even further and the Bank would yet again fail to meet its target inflation rate.

I certainly won't be rushing to accept the invitation to pay for advice from his company, nor do I think it acceptable that he should use this column to spruik its services.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.