By Bernard Hickey

The Reserve Bank is expected to cut the Official Cash Rate by 25 basis points to 2.0% next Thursday, and some think it could even cut it by 50 basis points if it is serious about getting the currency down and meeting its inflation targets.

Normally the banks would just fall into line and pass on all of the expected cut to both mortgage borrowers and term deposit savers, but this time is likely to be different and that's a good thing.

The banks could choose not to pass on much or any of it to both floating mortgage rate borrowers and those re-fixing their mortgages or rolling over their term deposits.

They have already started doing this. The banks collectively have only passed on about 35 basis points of the 50 basis points of two OCR cuts since December. They have only passed on about half of the 70 basis points of falls in two year wholesale 'swap' rates to their advertised two year fixed mortgage rates.

They've done this for two reasons. Firstly, their borrowing costs on international wholesale markets have increased slightly. It's hard to tell exactly how much those costs have increased and how much of that cost increase can be justifiably passed on, but there has been some increase. Secondly, the banks want to increase their profit margins to build up their stocks of capital in preparation for some losses on dairy loans and because regulators both here and in Australia want them to hold more capital to back their mortgages.

This is bad news from a borrower's point of view, but could turn out to be good news for savers.

ANZ CEO David Hisco essentially called last month for a truce between the banks over their extremely intense competition for mortgage customers over the last three to four years, and in particular for rental property investors.

ANZ itself has been among the most aggressive, particularly in Auckland, but Mr Hisco called time on the battle when he said the housing market looked over-cooked and that he would actually like to see the Reserve Bank require all landlords have a 60% deposit, rather than the 40% one the regulator is proposing from September 1.

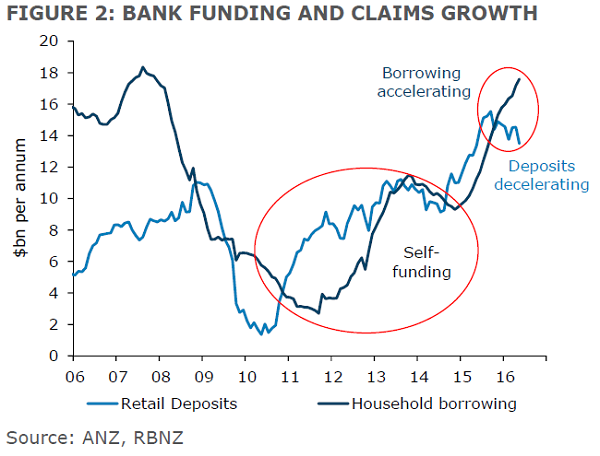

ANZ's economists also banged the drum this week about the potential for banks not to pass much of it on, either to term depositors or savers.

They pointed out that mortgage lending was now growing significantly faster than term deposits for the first time since the Global Financial Crisis. That means that banks are having to go overseas to borrow to fund the extra mortgages, which our credit rating agencies and the Reserve Bank itself are not keen on.

One way to encourage more saving and less borrowing is to not cut rates for either.

Right now the Reserve Bank is stuck between the rock of a housing market inflating at double digit rates, and a Consumer Price Index that is inflating significantly less than the Reserve Bank is supposed to target. CPI inflation of 0.4% is well below the 2% mid-point of the bank's target band and has been for over four years. This week's figures showing wages grew in the June quarter at their slowest rate in 6 years, which only reinforced the conundrum.

The Reserve Bank should be be cutting the OCR aggressively to get the currency down and get inflation back up again, but is worried that big rate cuts could worsen the financial stability risks building inside the housing market.

The banks could help savers and give the Reserve Bank some more breathing room by not passing on much or any of next Thursday's rate cut to both borrowers and savers. It will help them build up bigger buffers for the losses to come and reduce the risks that a future Global Financial Crisis could freeze a significant chunk of bank funding.

Borrowers will not love it, but the economy and the banking system would be better off if the banks chose not to pass it on.

A version of this article was published in the Herald on Sunday. It is here with permission.

51 Comments

Got a good laugh, out of your fourth paragraph. Especially the part about the banks' wants...

So, how much of the banks' lending is funded by the borrowing from RBNZ currently ? Is there a bank wise break up of these funding (local deposits, overseas borrowing, funds borrowed from RBNZ, etc ?) to finance the lending of each bank ?

Yes. It is freely available and has been for all banks quarterly since 1996 when the NZ General Disclosure Statement process came in. It is in great detail, in fact, more detail than the banks release to their own shareholders. Go to each bank's website to find this detail. It is quite esay to find. This is what we use when we do our analysis

Plus, the RBNZ publishes a summary, quarterly, by bank, here. (G1)

Plus, the RBNZ summarises this data in many ways. One (of 17) way is to look at bank funding sources (S3) which you can find here.

In fact, it is hard to imagine a more transparent system. Sadly, the RBNZ has found that very few people use the data available.

Thanks. The next question is how much would be the actual $ value that banks may benefit by, if the OCR reduction is not passed on ? Will the existing borrowings from RBNZ incur the lower rate or will only be the new borrowings be at the lower rate ?

Banks don't borrow from the RBNZ in the way you assume. The RBNZ doesn't lend to banks in the way you assume. It is a wholesale market signal. See here.

It does to pre fund NZD settlement cash (Section 10 - swaps) which is passed back by the banks to the RBNZ's liability ledgers, Memorandum items, together with lent out crown cash balances, rumoured to be costed at the OCR.

The swaps/memorandum items imbalance is one I have been asking the RBNZ about for many years without an answer.

In simple terms our local banks borrow USD to borrow NZD from the RBNZ via the currency swap market - the crown funds some of it's foreign reserves in this manner.

The official cash rate (OCR) is the term used in Australia and New Zealand for the bank rate and is the rate of interest which the central bank charges on overnight loans to commercial banks.

The most crucial part of the system is the fact that the Reserve Bank sets no limit on the amount of cash it will borrow or lend at rates related to the OCR.

So as a lender of last resort, the RBNZ will fund Banks at OCR. So technically, the Banks can go either to RBNZ or Overseas or to Local sources to fund their lending, whichever is profitable for them.

It would b intresting to know what would be the bottom line effect on the Banks on account of a cut in OCR, which Bernard thinks will improve the profits of the Banks, thus helping in shoring up their capital.

Not that simple - here is a list of eligible securities and the appropriate haircuts the RBNZ will impose on acceptable collateral in exchange for credit at each bank's respective RBNZ account. These trades will be conducted at the reverse repurchase agreement (repo) rate which will fluctuate according to arcane rules such as security scarcity etc - another long story. The haircuts are in place to discourage banks from leaning on state funding to support private lending operations.

"The haircuts are in place to discourage banks from leaning on state funding to support private lending operations."

hmmm, does the Accommodation Supplement/allowance meet that criteria?

The Bank of England has seriously exposed itself to the hindrance of bankrupt corporate debt securities gracing it's asset ledgers, not to mention the losses. Read more

What people should get from these documents is the very great depth of how our economies are so highjacked by bank dependency, and why every government policy & many media articles are so focused on encouraging borrowing to the max over saving etc; pushing borrowing for housing in particular like drug dealers.

It's quite disturbing how much productive human energy goes into pushing debt onto the masses to feed the gigantic parasites we call banks.

Ive said it before. It's such a waste of human potential to have so much effort put into monetary enslavement.

That's the big picture we never want to face. A life of being lead like farm animals to the slaughter house of banking and debt

It is 'alleged' (by some NZ families touched by suicide) that NZ's 'actual suicide rate is 3 times what is publicly released, due to coroner mis-reporting. I highlight this because I do wonder why regardless of whether this is true or not, NZ has such a high proportion of suicide? How much does the life struggle against DEBT play a role I wonder?

Honestly, this saddens me to the core.

Money Manager Capitalism: “The emergence of return and capital-gains-oriented block of managed money resulted in financial markets once again being a major influence in determining the performance of the economy… Unlike the earlier epoch of finance capitalism, the emphasis was not upon the capital development of the economy but rather upon the quick turn of the speculator, upon trading profits… A peculiar regime emerged in which the main business in the financial markets became far removed from the financing of the capital development of the country. Furthermore, the main purpose of those who controlled corporations was no longer making profits from production and trade but rather to assure that the liabilities of the corporations were fully priced in the financial market...” Read more

Great research David you seem to know your stuff on this.

Amplifying debt is what got the World into trouble, not out of it. Have you not heard.

Interest rates are not the issue, it is the issue of more debt, for little return. Even negative returns for negative reasons in most countries...these fine days. That is just the last resort, a bit like NZ,,,nice as it is, or was. It will be all fine...in the end.

If we can import our Dear Leaders bucket list.

Compounding problems, never solved anything. Especially when multiplied by increased stupidity.

I suppose we should all invest in Pokemon Go...do not pass go, do not get yer free Monopoly Money.

Eventually people will all see the light...when it dawns on them all at last.

But as usual...if you wear blinkers...full beam will hurt their heads, as they all blindly walk into it ,

Beam Me Up Scotty....We have a New World Order to discover....LALA Land.

So do not be negative Bernard, keep up with the times., they can print and be damned...We just have to follow suit.. I think it is a house of cards....zeros and ones.

And we can all work ourselves to the bone. And bitch about it..as we are cut to the...Quick....reduce the rates,, some bloody more.

Beggar the savers.

Follow my f..leader...

Stuff that for a game of soldiers. Brexit....NZEXIT...It is a brave new world...out there.

Live long and prosper....But don't save for your Enterprise...borrow some f...ing...more.

Now where did I put that 3d Printer. My turn.

Since the RBS cut a few days ago, Aussie banks have RAISED deposit rates. Interesting article on the topic here: http://wolfstreet.com/2016/08/04/australia-big-four-banks-housing-bubbl…

Yes, they have. But it might just be a PR move. They did the same thing at the previous RBA cut when they also retained some of the benefit for themselves by not lowering their variable mortgage rates by the full amount. They raised term deposit rates then too - and waited till the hue and cry died down, then cut them again. The raising of TD rates then was about a 4 week temporary benefit.

Whatever happened to The Core Funding ratio, the only useful thing the RBNZ has done in the last 6 years? Oh, I know, it worked, so no need for more. Need to do more of the things that don't work. Silly me.

How sticky is core when a huge chunk of the funding ledger is O/N cash? View data

Silly me, I thought the words meant something. I was thinking that simply putting up the Core Funding Ratio from 75% of one year liabilities to, say, 100% of 2 years liabilities, over a suitable time period, might be rather effective. The RBNZ doesn't want to get the blame for being effective, of course.

I suspect the RBA has fewer qualms and has been telling the Aussie banks to pull their heads in, hence the bank CEOs finding religion.

Not passing on rate cuts may well help to stabilise our current property binge but does it not further exacerbate is the issues around moving ever closer to deflation? There is the risk of consumers delaying purchases in the future. Which is worse? It's matter of deciding on which is the lesser of the two evils.

Australia’s WTF moment

Why did the banks raise the interest rates on term deposits when the RBA cut rates?

http://blog.australiaboomtobust.com/2016/08/australias-wtf-moment/

All of the debt market reform and regulation going on must surely be a contributor to the lackluster performance of the US economy since the GFC.

Here is another article on the Oz house prices.

I reckon it applies to NZ just as well.

Hedge Funds Are Betting Record Amounts on Meltdown of Australian Banks and Housing Bubble

http://wolfstreet.com/2016/05/23/hedge-funds-bet-meltdown-australian-ba…

Another reinforces yours.

In other words, a number of buyers are now faced with a sudden increase in interest rates from 4% to between 8% to 12% – regardless of the administered interest rate of the RBA. It is of course possible that the effect will once again stay local (i.e., confined to Melbourne and condominiums), similar to what happened when commodity prices collapsed.

The downturn in commodities led to sharp declines in property prices in regions and towns close to mining activities. However, house prices in the big cities continued to soar – not least because the RBA cut rates in order to offset the impact of the commodities bust. Read more

[ Silly personal abuse, deleted. Stick to the issues. Ed ]

IMF came out last week with latest global housing numbers. Of course anyone can argue with their methodology. However , New Zealand sits at number 2 in real house price increases over past year, real credit growth in top 4, house price to income at number 1 (at least we get one gold), and house price to rent at number 5.Overall New Zealand was number 1. Of course by giving the national figures , the true concern( Aucklands debt and house prices) is simply numbed down .Looking at RBNZ figures last week, credit growth has most definitely slowed on all stated measures., Without ever increasing credit , then Auckland house prices have topped. There will be a realisation over the coming months that there will be no soft landing, that the housing shortage never was. The reality is the RBNZ , could address interest only loans ,or cap mortgage to income tomorrow ,but it knows it would be game over sooner. Yet it was the same RBNZ that allowed cash back mortgages, IPADs and indeed grocery vouchers to be dished out over the past five years to enrich our Australian banks , as Aucklanders in particular went on a credit binge.The RBNZ may cut by 0.5 basis points, it will have nothing to do with the CPI, but all about maintaining the housing market. The next problem will be the currency .New Zealand has simply deluded itself for the past 15 years , at some point , we hit the windscreen.

So Bernard. Are you asking for interest rates to remain high for borrowers in a deflationary environment? That seems cruel wouldn't you agree? Are you a neo-liberal now? Et tu, Bernard?

Bernards heart is the right place, he just hasnt thought it through.

The banks are already OVERSEAS OWNED BANKS! That is where the money ultimately comes from and where the all profits are ultimately going to. Bleeding the average NZ mortgage borrower of even more floating margin is not at all clever for NZ. It just fills the pockets of the banks.

"the money ultimately comes from and where the all profits are ultimately going to" - yes all profits (and increasingly retained earnings) go to the overseas banks, but NZ depositors are the ones ultimately funding the banks and taking all the risk via the RBNZ OBR scheme. There will be no money coming from the overseas banks. And the covered bonds sold overseas will take many of the performing NZ mortgages prior to NZ depositors funds being protected.

So depositors to put their cash into kiwibank or other NZ owned lenders?

The Reserve Bank could and should ensure this outcome by lowering the OCR and concurrently require the banks to increase their capital reserves to match. As you say this capital may be called on to protect the banks and depositors in the events of farm and property price crashes. Both are a real possibility. If they do not anchor this money into the capital reserves the risk is that it will go back to Australia and lost through dividends or be used to prop up the Australian branches in the event of a crash.

ANZ's economists also banged the drum this week about the potential for banks not to pass much of it on, either to term depositors or savers.

They pointed out that mortgage lending was now growing significantly faster than term deposits for the first time since the Global Financial Crisis. That means that banks are having to go overseas to borrow to fund the extra mortgages, which our credit rating agencies and the Reserve Bank itself are not keen on.

BIS claims: Deposits are not endowments that precede loan formation; it is loans that create deposits. Borio Page 17 of 38

Hence every new loan creates a deposit for an agent selling an asset to a debt financed buyer, possibly just not a term bank liability, since the selling agent may credit a business financing account. Farmers selling holiday homes would fall into this category.

Collective bank liabilities always match their assets, but the breakdown of each participating borrower /lender cohort does not necessarily have to match.

Please point to evidence beyond RBNZ tables S6(bank funding) and S7(bank claims), after mutliplying claims by 21% (foreign funding) and adding this back to S6, where there is substantive evidence of a claims/ funding mismatch.

OCR is a paper tiger, increasing or lowering it is just a signal. It doesn't really affect the bottom line of the Banks as they have other funding sources available at different costs, especially in a world awash with money on account of successive QEs. Banks' pricing of their loans and deposits is a complex game. Each Bank has to approach it differently.

A OCR reduction does not necessarily mean more profits for the Banks, does it ?

It is just not positive to attack property investors and people making money out of the property market. The culprits are our inept councils over the past decades, the RMA which is a joke and has choked supply. They might think their consent processes are short, but the amount of people you have to engage with to build or develop is not only costly but incrediblt time consuming. In my view the majority of fault lies with the RMA and I have developed so am better equiped to have an opinion. Property investors should be given a medal, they provide a free service to the government, they know that and that is why they are trying to stay out of it. Otherwise it would be up to them to purchase, manage and provide discounted housing which would cost us all an absolute fortune. Investing is not as easy as people think, it only looks so in the good times and they are few and far between.

Blame supply and the RMA! Making rental property more costly for tenants is not the answer.

.

Obvious troll is obvious.

If the banks don't pass on the cuts by the reserve bank, then the reserve bank is a waste of time and should be wound up. The reserve bank purpose is to maintain the stability and security of the financial system and to maintain inflation between 1 and 3%. It is currently .4% and has tracked well below the target rate for some time. If you want to slow down the housing market why not curb the amount of cheap funding banks can arrange overseas and require more to be sourced locally.

Gold for house prices relative to income... congrats National looks like doing nothing is a winning strategy after all.

Would be interested in understanding how often the bank rates are not lifted when RBNZ increased rate?

Currently if you have a cash deposit you earn some interest. It shows up on your bank account, but what !, tax is deducted by the bank and sent off to the IRD. Meanwhile ïnvestors"get a tax deduction for the interest they pay

Now apparently we want to encourage those saver and we are starting to think debt needs to be discouraged.

The mechanisms are all there so why don't we reverse it. Should be simple.

Put the tax requirement on top of the interest that people pay, and remove the tax on interest on deposits;

(let the howling begin)

a medal ...lol....that made me laugh out loud...

Property Investors and foreign buyers are part of the problem, not the solution. The only property investors that deserve medals are those building new builds. The rest are effectively just trading existing homes which simply pushes up the prices. This also reduces home ownership rates thereby making more people tenants in the long run.

You blaming the council is like john key blaming supply ... both completely ignore demand. Where is the demand coming from exactly ? Investors & foreign buyers. Just like Australia, Canada, Singapore, Uk , etc etc NZ is no different.

The only difference is the NZ government, unlike those other nations has yet to act.

NZ Government is just trying to win the next election at any cost.

46% of the market are investors

13bn NZD a year is spent by foreign students and temp visa workers on housing

13,500 houses bought by foreign students and temp visa workers. That is 260 houses a week. Per LINZ.

(NOTE GREAT HEADLINES HOWEVER INTEREST.CO.NZ GAVE US THE 3% OFFSHORE HEADLINE)

Once the government control these two groups by applying a 15% stamp duty (on existing homes only) the quicker house prices will come down to more affordable levels. This would encourage new supply also which should help the issue. Once demand is reduced and supply increases prices should settle.

Prices are already Number 1 in the world relative to incomes people.. we are already at crisis level. This is the biggest threat to NZ's economy at the moment. Little wonder the ANZ chief called it that also.

Forget your medal and start saving for your stamp duty.... it is coming. You had a great run be thankful for that. Zero purchase tax, zero capital gains if sell after 2 years and not trading in a company. The circus needs to end one day.

LINZ REPORT

refer the table on page 12 for my statistics on foreign buyers 13,500 homes. (8751 + 4707)

http://www.linz.govt.nz/system/files_force/media/doc/prs_property-trans…

Joe Public is wrong is stating that property investors are just trading "existing homes" Property investors keep huge numbers of people in business up and down the country.

Every day plumbers, painters, electricians, concrete workers, kitchen and bathroom fitters, landscapers, chippies, etc etc are making a good living from investors as upkeep, repairs and maintenance grinds on keeping the "existing homes" in good repair, or in many cases renovating for resale to those who have not got the time or skills to do it for themselves. In fact most investors are little different from developers who build new houses, as they recycle and renew existing stock thus taking substantial pressure off the building industry. That can only be good.

Those are the exact same people that home owners keep in work. Next excuse.

@Bigdaddy - yeah and homeowners don't spend a bean with any of those exact same service providers?

Seriously...what planet do you guys live on?

I'm an owner occupier and a land-lord but c'mon... you cant be this deluded or narcissistic to think you are doing "gods work" .....................or are you? (and many others..)

When professional "investors" build new stock solely to help the needy I'll start agreeing on your intentions - until then at least be honest with yourself.........

Great post and agreed new stock is where they can provide a service if that is what they want to do.

Average house probably costs minimum $15k a year to maintain and pay rates etc...

PocketAces. No they don't. Home owners are not obliged to install smoke alarms, keep their places warm and dry, meet certain standards, provide sanitary conditions, or worry about over crowding, tenancy tribunals, and a myriad of other regulations. Home owners can live like pigs and not have the PC brigade hounding them morning, noon and night.

Indeed they do.

Which is probably why it is best if just about all do own their own house so that sensitive folks like you don't have to be on the receiving end of such tribulations. And you would be surprised how lots of nasty wee habits would vanish if people had a stake in the ground, had something to call "home" rather than the tenuous and precarious renting situations we have allowed to develop in this country. You might want to consider that if some people use houses in this country to, for all intents and purposes, farm people, then it should not come as a surprise that those that are farmed, end up acting like pigs.

Our home ownership rates are going down the toilet and our tenancy laws, which give no sense of permanency for people, are crap.

That's the thing about being in business. When you're selling a product to the customer there are standards to be met which don't apply if you're consuming the good or service yourself. If you're making sausages for your own consumption, nobody cares what goes into them. You could be putting dead mice through the Kitchenaid, and the regulators won't give a damn. So what, you're eating them, your business. But if you make sausages to sell to the public, there are all kinds of standards to be met in terms of ingredients listings and cleanliness and permits.

If landlords are incapable of reaching the standards required of the business, and frankly they're currently pretty low, then GTFO. Can't claim to be a business when it comes to tax and mortgage advantages, then bleat that it's too hard when the product is required to meet minimum commercial standards.

Great replies pocket aces.

No one is saying don't use the plumbers electricians painters gardeners ... just use them to make new homes !!! If anything because they are working for investora on existing homes this means they can't work on new builds. So you buying a place holding for 143 days and adding 140k to the price isn't helping anyone.

The big problem is that journalists have so much power these days to persuade people and the general public are usually cannon fodder for them. Good example is the foreign buyers.

Nz journalist quote 3% foreign

Completely ignoring foreign students and temp workers who buy 13billion worth of property or 13500 homes a year roughly.

This piece is another example. Somehow trying to persuade us that the banks not cutting the rates is a good thing. Hahaha... only in NZ could you print that. How many billion again do the banks make at the moment in NZ?

We saying they need more ?

What we need is

-loan to income restrictions of 4 to 1 on investors,

-require banks to hold far more capital on investors,

- 15% purchase tax stamp duty on investors and foreign buyers (include students and temp visa)

- stamp duty exceptions for new builds

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.