By Shane Martin & David Norman*

• Further, the population’s preference is for fewer people per dwelling (PPD) than in the past. This means that, all else equal, housing supply actually needs to grow faster than the population to keep prices stable.

• In slow-growing areas of the country, prices have remained subdued as house supply has easily kept up. But in Auckland, prices have risen sharply because too few houses have been built relative to the massive population growth, despite a large amount of land available to develop through the Unitary Plan.

• Simply, a slow response in housing supply rather than lagging technical land availability explains much of the house price growth.

A mixed bag of house price growth

Across all 47 cities and districts in New Zealand with a complete house price data set1, house prices grew significantly from the turn of the century until the Global Financial Crisis (GFC) in 2007. Still, growth varied from 75% to 190%.

During and after the GFC, however, widespread growth did not continue. In areas like Auckland, Queenstown, Selwyn, and Tauranga, prices continued to rise strongly. Conversely, areas like Clutha, Gisborne, South Taranaki, and Whanganui saw broadly flat prices between 2007 and 2016. What has driven this divergence across New Zealand post-GFC?

As always, supply and demand

As with any product, the price of housing is determined by supply and demand. We would expect that as population grows, the demand for housing would increase and put upward pressure on prices. Or if demand for housing is sufficient, as interest rates go down, prices will rise.

On the other hand, as housing supply increases, downward pressure on house prices is created. The interplay between these phenomena (and other unobserved trends) determines the market price. These are not profound insights, but our work has determined how much of the house price changes can be explained by these attributes.

By using an econometric model of house prices, we were able to measure the impacts of population, housing, and interest rate trends to help explain growth in house prices in Auckland and the rest of the country.

What’s the deal with Auckland?

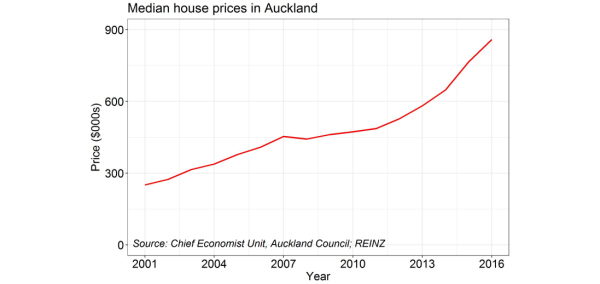

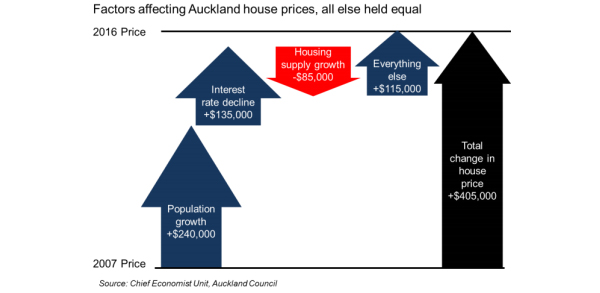

Over the past 16 years, Auckland’s median house prices have increased from the mid-$200,000s to over $850,000. Since the GFC, Auckland has had the highest growth rate in house prices in New Zealand, and saw absolute growth of around $405,000 in median prices between 2007 and 2016.

How much of Auckland’s house price growth can be explained by the three factors of population growth, interest rates, and housing supply growth? In Auckland, the population increased by 17% between 2007 and 2016. On its own, this would imply a $240,000 price increase, all else held equal.

Interest rates on mortgages declined massively between 2007 and 2016 – from an effective mortgage rate2 around 8.5% in 2008 to below 5% by the end of 2016. Our analysis shows that this fall in interest rates allowed a $135,000 increase in house prices without mortgage repayments rising, given the extent to which the supply of housing did not meet demand in Auckland.

The housing stock has risen, albeit not fast enough. Between 2007 and 2016, it increased an estimated 11%. This increase in housing stock reduced price growth by $85,000, all else held equal, in Auckland. But in summary, housing stock has simply not grown fast enough to keep up with demand from:

• a burgeoning population

• a preference for fewer PPD, not more

• higher bid prices due to lower interest rates.

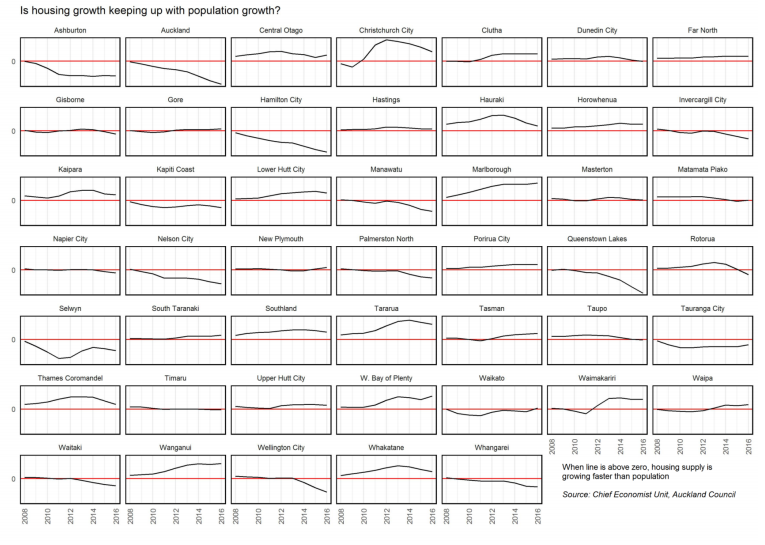

Where are enough houses being built?

Areas where lots more people want to live have not been able to raise supply fast enough, while those with weaker population demand have been able to cope better, slowing price rises. As of 2016, Auckland has the second highest gap between the rates of population growth and housing supply growth in New Zealand. Guess where it’s worst: Queenstown, where house price growth has been roughly as sharp as Auckland’s.

And the five areas in New Zealand with the largest price increases over the past 10 years have all seen house supply growth slip behind population growth. In contrast, four of the five areas with the lowest price increases have had stronger house supply growth than population growth.

Overall, housing supply has kept pace with population in 27 of the 47 areas we evaluated. In these areas, the average house price is about 20% higher in 2016 than it was in 2007 (suggesting unmet demand for fewer PPD). In the other 20 areas, the average price increased about 30%. It’s clear that the relative growth of housing supply and population significantly affects house prices.

You can’t live in a resource consent

Rapid house price rises in high growth areas like Auckland have led to debate about the root cause of the increases. Some have suggested that land use regulation may be the largest contributor to inflation in Auckland and elsewhere. But the evidence across the country supports the conclusion that land use regulation is unlikely to be the main culprit for house price rises.

To point the finger at land use regulation would imply that all the areas with the largest population increases have the worst land use regulations and those with the smallest gains have the best regulations.

Perhaps something else is at play?

Our findings in Auckland (which we can replicate for all 47 areas examined) suggest that population growth, housing stock growth, and falling interest rates explain about $290,000 of the $405,000 increase in house prices between 2007 and 2016. The other $115,000 is due to everything else.

“Everything else” may include land use regulation, but is also due to:

• unmet demand for fewer PPD

• household income growth allowing people to bid up prices due to unmet demand

• construction cost increases and capacity constraints

• changes in the relative productivity of land in Auckland compared to other areas

• all the amenities that draw people to Auckland instead of other parts of New Zealand. While excessive land use regulation no doubt puts upward pressure on house prices, land supply is not housing supply, as we pointed out here.

Council, the Reserve Bank and the Ministry of Business, Innovation and Employment have all estimated Auckland’s housing shortfall at between 43,000 and 55,000 and growing. The Auckland Unitary Plan allows for up to one million potential new dwellings. Yet the plan was implemented a year ago, and there is no evidence of decreasing land prices.

Put another way: If having already zoned to develop 20 times the current housing shortfall is not bringing land prices down at all, can land use regulation in Auckland be the major cause of high house prices?

In the case of Auckland at least, the answer is simple: You can’t live in a resource consent. It is because not enough houses are being built fast enough (for a range of reasons), rather than just the technical availability of developable land, that is keeping prices up. Land may be resource consented for development, but until houses are actually built on it, a premium will be placed on houses that are available.

How we did it

An annual dataset consisting of median house prices, population, housing stock, and interest rates for 47 territorial authorities (TAs) was created. A two-way fixed-effects model was estimated to assess the impacts of population growth, housing stock growth, and interest rate trends on house prices. This model controls for the named variables, idiosyncratic TA effects, and time effects.

1) Monthly house price data was available between 2001 and 2016 for 46 of the 47 Territorial Authorities (TAs) that had a population of at least 15,000 over that time period, the exception being the South Waikato District. Complete data was also available for the smaller Gore District, making an analysis possible for 47 of the 67 TAs in New Zealand, covering over 95% of the population.

2) It should be noted that whichever rate is used (floating first mortgage, effective floating mortgage, effective fixed mortgage, or effective mortgage), the trend is nearly identical.

*Shane Martin is an economist in the chief economist unit & David Norman is chief economist at the Auckland Council. This article is published with permission.

50 Comments

Let me suggest that an econometric model is not going to explain the real extent of drivers of house price growth, mainly because the model will lack the ability to quantify human behavior and the environment where a monetary paradigm / banking system enables money to be lent into existent (the idea that banks are mere “intermediaries” between savers and lenders is horseshit), quite often under the condition that the borrower is only responsible for returning the cost of funds. Furthermore, the supply-demand assumption is likely to be too simplistic. No disrespect to the economists. In fact, I admire them, but I firmly believe that the answer is not found among fixed variables. It completely ignores political economy and behavioral economics.

JC,

"mainly because the model will lack the ability to quantify human behavior and the environment where a monetary paradigm / banking system enables money to be lent into existent"

Ahh, what?

Surely the model does that very well, no? Okay, it may not forecast out of sample, well, but it is a fair representation of the observed data..

i.e. because the model is a function of observed house prices (growth) in a market equilibrium assumption the model relies, fundamentally, on some revealed preference, right?

They control for the marginal effects of, as you imply, interest rate changes (money lending) specifically. They even go so far as to explain the difference-in-differences result to you, from a ceterus paribus position, that interest rate changes (a proxy for money lending) is estimated to result in a given price premium.

Also,

"Furthermore, the supply-demand assumption is likely to be too simplistic."

What do you mean by that?

Again, it is observed data...

my "model" of demand is transactional.... simply, "money + credit = demand "

the supply side is measured in "quantity" supplied..

SO... of course the most easily influenced , and measurable variable in this model is "credit"..

Starts becoming hard work when one starts figuring out the different "players" and how they participate.. , in any particular mkt.

Unless you know that, it is hard to know, beyond generalisation, how interest rate changes might affect demand.

eg... in housing there are, Investors, first home buyers, homeowners, foreign buyers ...etc..etc

I learnt this from Ray Dalio..

Agree, Roelof.

My argument was more with the misunderstanding of the modelling by OP.

Surely the model does that very well, no? Okay, it may not forecast out of sample, well, but it is a fair representation of the observed data..

i.e. because the model is a function of observed house prices (growth) in a market equilibrium assumption the model relies, fundamentally, on some revealed preference, right?

Let me tell you. The model doesn't account for behavioral variables nor is there any indication that it accounts for lending volumes.

The model is built on assumptions about how people behave. It is not some kind of conjoint analysis, therefore it does not reveal anything about "preference".

Interesting.

What sort of 'behavioral' variables would you put in there?

Have you seen the report and methodology in full?

Can you share, if so?

No I haven't seen the methodology. As I said, to understand preference, you would need some kind of conjoint or behavioral components in their model. Building that it into a broad macro econometric model would be very interesting and would be very complex. I very much doubt that the economists would have the time and resources to produce anything of this scope. And if they did, they would most certainly be trumpeting that fact.

100% pure New Zealand, this is the only advantage kiwis has. Multi culture, more population are short gains, and will only destroy this image long termly.

Wrong it is all because of No capital gains tax and Chinese multi millionaires!

Wonderful stuff. Well done you guys.

Hopefully we can now all stop argueing about what the causes are and actually solve the house price problem.

Maybe high house prices are a combination of many reasons, but the biggest reason is high land prices, with an Auckland section costing in the region of half a mil.

High land prices are due to both demand and supply. Auckland council are restricting supply (both in terms of rural boundaries and density restrictions). Auckland council are largely responsible.

High land prices then flow on to large houses - why spend 800k on a section and new 2 bed house when you can spend 900k on a section and 5 bed house.

They certainly made a lot of excuses and their job is to protect Auckland Council. However setting aside the extreme cost of land they excluded any discussion of the regulatory costs of building consent as a contributor which appears to be a deliberate omission.

The tremendous costs of obtaining the building consent from a Council that is sensitive about legal claims for leaky buildings etc put developers off carrying out projects. There's too much cost and risk to justify enough residential construction to deal with demand. It's also a problem that's not just limited to Auckland, and MBIE share some of the fault through their incompetent work in managing the NZ building code.

I don't know why we continue to debate why the massively regulated housing market is performing so badly compared to most other markets which are unregulated.

Remove all the unnecessary regulation and I bet most of the problem will go away. The only required regulation would be the likes of height to boundary restrictions and some minimal health and safety building requirements (most of the building code is about longevity and quality which should be the owners choice)

And don't we still have trade restrictions on building materials like Gib! Ridiculous...

The way Council's work with their building and resource consents need to be reviewed. The Council's themselves need to be reviewed as the large Councils are completely dysfunctional, which is a sign that something is seriously wrong. Perhaps support from the Government and MBIE would help, something that has been sorely lacking and seemingly corrupt.

e: Also these economists are operating outside of their area of expertise and therefore no weight should be given to their opinions.

Yep, I've just been through the consent process.

By the time you have to pay the council, architects, engineers, surveyors, 'licensed' tradespeople, overpriced NZ standards complaint materials, etc, I think the need for a building consent probably doubled the price of my build.

Fair enough to have strict standards for multi story buildings, but for simple stand alone single/double story houses its just not necessary. Personally I think we should be able to build a house without even telling the council (other than asking watercare to hook up the services just like you would with the power company).

No mention in this article about Christchurch - the only city where prices are reducing in real terms.

The earthquake shook up the land regulations in Christchurch and forced the council to make ample new land available to build on. Land was plentiful and therefore cheap, builders could build a selection of different housing sizes profitably and supply kept up (even outstripped for a while) with demand. Result: stable to gently falling house prices.

So $240k increase if prices is caused by population growth offset by only $85k due to housing supply growth. So not enough houses have been built to meet demand resulting in rising house prices. All sounds good until we get to:

"The Auckland Unitary Plan allows for up to one million potential new dwellings. Yet the plan was implemented a year ago, and there is no evidence of decreasing land prices.

Put another way: If having already zoned to develop 20 times the current housing shortfall is not bringing land prices down at all, can land use regulation in Auckland be the major cause of high house prices?"

So freeing up land under the unitary plan should be expected to have a near immediate impact on Auckland house prices..??? How long does it take to get a building consent, let alone build a house and then make it available to sell (increase in supply) and then have that flow though to a slow down in house price growth? I would say at least 3 to 5 years.

So the unitary plan might help but it is too early to say. Definitely no evidence is presented that land use restrictions have not been a material factor in rising prices.

Simply, a slow response in housing supply rather than lagging technical land availability explains much of the house price growth.

Thats right... and the slowness of supply response has more to do with "red tape" , than anything else.

The inelasticity in supply response + the locational value of land has alot to do with rising house prices.., in my view.

Is using the term .."technical land availability" , kinda meaningless, within the context of the discussion of house price rises,..??? Should the focus be on the "cost" of that land..

eg...the price difference between farmland prices on the urban limit and the price of a section , as a monetary metric for measuring the "tightness " of land availability ..??? etc..etc

High section prices vs farmland prices imply constrained land availability

After all... New houses do not get built unless developers can make good profits.It is not just the "technical land availability" , but the cost of that land that is a determining factor in whether a developers numbers crunch out into a profit...or not..

So let me get this 100% clear. In a time of QE and globalised low interest rates that has seen sustained asset price inflation, Auckland Council have decided that there is nothing wrong with their land use regulations because house prices are being subjected to asset price inflation?

Wow. Auckland Council may have figured out that low interest rates highly impact house prices. But here is the problem, having now figured out the bleeding obvious, why is land use regulation given a pass?

Put another way: If having already zoned to develop 20 times the current housing shortfall is not bringing land prices down at all, can land use regulation in Auckland be the major cause of high house prices?

Nope, the major cause of high house prices is low interest rates.

The question we should be asking Auckland is why are houses being built so slowly in Auckland? And the answer is, because of Auckland Council and their insane land supply policies.

My thoughts exactly. Absent economic pressures to develop buildable but bare land (such as, f'rinstance, a swingeing differential rate), land prices are sticky on the downside. There is little to no disincentive for land-banking.

But given that past, economically clueless, land-zoneration has most certainly lead to crazy plot prices in Awkland, those prices are what foobars everything on top.

And the article is certainly incorrect in averring that NZ-wide observed data backs up their conclusions.

In Christchurch, the post-earthquake response was to effectively toss zoneration rules under the bus, by opening up land development to all comers. And it was helped by intense competition as between TLA's, each eager to attract residents, businesses, and economic activity to their patch. So despite the typically woeful performance of the Christchurch City Council, neighbouring districts (Selwyn, Ashburton. Waimak, Hurunui) had some of the highest build rates per head of population in the country, for a number of years.

So the article is more than a little deceitful in neglecting to point to this rather unique real-life case study.

Christchurch plot prices start with a 1, house+plot in the high 3/low 4 bracket.

Christchurch had four major drivers of this happy outcome:

- A destructive natural event which shook up the existing institutions and led directly to a ground-up re-examination of what needed to be done to recover. In MBA Change-management jargon, this was the 'unfreezing' of the existing order.

- A flow of insurance, Gubmint and investment $$$ into the construction industry which lubricated the rebuild

- Land use regulatory changes (the LURP) driven by a determined Minister (Brownlee) who had no compunction about calling out stupidity in TLA rules and staff attitudes

- Intense competition at TLA level for the fruits of the recovery

This happy combination cannot be modelled elsewhere. But the AC economists are remiss in not understanding that their Models clearly do not 'model' the Christchurch situation at all well. They certainly neatly avoid the core argument that Hugh P (much missed on this site) used: that if the land price is wrong, so is everything on top.

And, to top it all off, the article has not one mention of the Productivity Commission's report, which nails land price growth, due primarily to regulatory constraints: see Chapter 3 for the full glorious story. Figures 3.8 and 3.9 give the lie to the AC economists' happy-clappy view of their culpability......

The "locational Value " of Land is a very unique economic study.

Location + utility = value.

This is a field of study , on its own..

I dont see any mention of this in the above report..???

eg.. How did the new unitary plan impact on land values..?? ( unitary plan became a massive revaluation of land )

What impact did allowing intensification while still limiting urban limits , have on land prices within the urban limits..???

Yea, there should be some important references in this report. (For the Auckland case, at least)

Namely Greenaway-McGrevy (2017) (An interest article was produced for this last year) and Grimes and Zhang (2009) which answer both of your questions.

The Auckland Council have an extremist position on the concept of locational value of land. Auckland Council disagree with just about everyone on planet earth as to where to allow development of housing.

The entire world (apart from Auckland Council) thinks that new suburbs should be built on locations directly proximate to existing metropolitan areas to allow utilisation of existing infrastructure creating environmentally efficient compact development.

Auckland Council believes that new suburbs should be placed everywhere except directly proximate to existing metropolitan areas. And the reason given by Auckland Council for spreading suburbs as far away from Auckland as possible is to create a "compact city" - Auckland Council planners are very weird.

"Auckland Council's economists argue that evidence from across NZ supports the conclusion that land use regulation is unlikely to be the main culprit for house price rises"................Surely........instead of of the lengthy production of so many graphs and information these economists could have gone about their appraisal with a far more effective and simple analysis.........a simple bareland plot with NO land use regulations upon it vs bareland with land use regulations upon it and then price for the exact same house to be built upon both bits of land.

There is a graph in the latest Demographia report that shows house prices in cities with restrictive land use and those with non restrictive use. Very telling.

And in spite of what that authors claim, Auckland, and NZ in general have restrictive land use polices.

Which cities don't have restrictive land use? Is it just a handful of not very interesting cities in Texas?

While I am not a fan of restrictive land use, I don't believe that is the only reason why Houston is cheap...

Houston might have been cheap once, but it has had a price boom over the last 5 years and is now rocking historic highs.

Looks like its boomed from cheap to still cheap:

"As such, the single-family home median price rose 4.4 percent year over year to an all-time high of $235,000, and the average price increased 4.3 percent to $302,362, the second-highest average ever."

Yes still as cheap as chips, in spite of low interest rates and high immigration..

Houston is one of the most cosmopolitan cities in the States, Austin the music capital of the south west etc. and there are other states.

Read the 2018 Demographia report.

And before anyone says it is because Texas is flat, if that was the case, then Australian housing should even cheaper.

It's about policy. If you have a restrictive growth policy then you have expensive housing, and non restrictive cheaper better value housing.

Gotta love the Auckland geographical "constraint" fallacy. Auckland is a city on an isthmus - a strip of land between two large land masses - and therefore as the city gets bigger land becomes more available. Right now Auckland is facing the least geographical constraint it has ever had and land should be inexpensive.

"Interest rates on mortgages declined massively between 2007 and 2016 – from an effective mortgage rate2 around 8.5% in 2008 to below 5% by the end of 2016. Our analysis shows that this fall in interest rates allowed a $135,000 increase in house prices without mortgage repayments rising, given the extent to which the supply of housing did not meet demand in Auckland."

Auckland Council economists and bank economists have, previously, made the mistake of looking at nominal interest rates rather than real interest rates (important as inflation causes the burden of home loans to reduce over time).

It looks like that's been corrected in this piece, but interest rates at 8.5% were a spike and not typical of the 2000s. It seems improbable that a small drop in real interest rates has had much impact on the market. Even if this aspect is mathematically right, isn't it more accurate to say "there was a brief period where people had to have an additional $135k to prevent mortgage repayments increasing"?

Their conclusion does not to accept the reality of the world, where low interest rates drive house price increases.

In the case of Auckland at least, the answer is simple: You can’t live in a resource consent. [] not enough houses are being built fast enough ([because Auckland land supply polices are insane]), [it is] the technical availability of developable land, that is keeping [supply down, but this has minimal impact on prices compared to ease of monetary supply]. Land may be resource consented for development, but until houses are actually built on it, a [shortage of houses will exist].

I agree, they are a factor. But only one in the face of many.

If you read the report, they are not denying the impact of interest rates.

I assume you mean that they are the main positive driver, though?

"Their conclusion does not to accept the reality of the world, where low interest rates drive house price increases."

If your assertion was to be correct, do you mind explaining the Labour/Clark era, then?

House prices increased by over 100% during their reign, except that, if anything the drift of interest rates was upwards, with an (loose) average of around 8%.

https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-mortgage-rates

The interest rates were low during the Clark era and now they are lower still. Look at the longer history of mortgage rates. Both eras had low rates and prices went up.

https://teara.govt.nz/en/graph/23100/interest-rates-1966-2008

If the study by Auckland Council is to be believed, the main driver is population growth. And yet during the Clark era house prices went up by 100%, whilst population growth was much lower.

Why didn't house prices skyrocket after inflation targeting smoothed the volatility, then?

It took them around 12 years to double, despite both interest rate level and volatility substantially dropping in historical terms.

Like I say, interest rates are definitely a driver.

Blindly assuming they are the main driver is stupid, though.

In the case that supply was perfectly elastic, they wouldn't at all matter would they?

Have a look at Fig. 5 Real House Values in the attached. There is an upward step change in property pricing trend from about then onwards. They did seem to skyrocket and housing is not able to be a perfectly elastic market.

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Bulleti…

Yes, upward slope.

That difference over 12 years is 0.25 on a log scale.

From 2003 to 2008 the difference is about 0.6 points.

That is not comparable.

There is a simple, sad explanation for Fig 9 in the Bulletin: the Universal Pricing Signal issued to every sentient being in NZ via the introduction of Welcome Home Loans in 2002-3.....This had the immediate effect of sliding a price floor into the market at whatever the current WH loan limit was.

The message to sellers was blunt:

"Don't even think about selling that borer-riddled fibro shack in Ranui for less than the WH loan limit".

The 'market' duly obliged.

The Good Intentions Paving Company, Version 1.0.....

nymad... In 2005 credit growth was 15%.. so the demand for credit was there.

Obviously %rates were low enuf to sustain the demand for credit..??

https://www.interest.co.nz/charts/credit/housing-credit2

In the end the transmission mechanism is not just interest rates, per se , but also the "gap" between investment returns and interest rates.. and the existing debt burden ...etc.., within the context of whatever the economic climate is...

If you start of with the wrong premise, then you may arrive at the wrong answer, eg they state:

'a large amount of land available to develop through the Unitary Plan.'

This is only true if the land had the same competitive ability to be developed and brought onto to the market at the same time.

In non restrictive boundary jurisdictions, any developer could do this, but in Auckland, this land is still drip feed onto the market, so the true amount of land is extremely restricted.

All a consent is, is another type of restriction. Those jurisdictions like NZ that have very restrictive land policies also have restrictive consenting policies, they go hand in hand.

And if you don't understand this basis concept, then on it goes:

'We would expect that as population grows, the demand for housing would increase and put upward pressure on prices.'

This is ONLY true if the supply cannot meet demand. If supply is elastic enough then the price stays the same. And will also stay the same if the reverse happens, ie if demand drops, then supply switches off almost as quick so no bust either.

And there are plenty of housing jurisdictions were this steady state happens, ie low house prices irrespective of demand pressures.

And of course the rest of NZ is the same, as previously posted:

Prices going up in the regions only shows that the same dysfunctional housing policies that make Auckland what it is, are nationwide. IE it is not a size thing, it is a policy thing.

Every town in NZ is just an Auckland cluster$&%@ waiting to happen, take Tauranga for example as mentioned in the latest Demographia report (Which Interest.co.nz have failed to cover?)

The inability of these authors and their employers ie ACC to understand that land restrictions are the root of the problem, and how they greatly effect all the other variables in the system, including consenting policies, developer and builder decisions, etc. is the main reason we have high land prices and therefore house prices, and low quality builds, compared to many other jurisdictions.

Quote from the Productivity Commission report (unreferenced in the AC article, quelle surprise): Overview Page 1:

The price of land is increasing, reflecting a constrained and stressed planning system

A number of factors affect the supply of housing, but one of the most important is the availability of land and the land use rules that determine the capacity of land to carry dwellings. Land values have grown more quickly than total property values over the last 20 years. This suggests a shortage of residential land in places where people want to live. The problem is particularly acute in Auckland, where land value accounts for almost 60% of total property value. However, in many high growth councils land is approaching 50% of total property value, compared with about 45% in the rest of New Zealand.Planning systems and land use regulations imposed by central, regional and local government affect the speed and efficiency with which land is made available for residential development, including the more intensive use of land within existing city boundaries. Decisions about the amount of land to be released, the timing of when this will happen, how it can be developed, and when it will be serviced with infrastructure all

directly impact on the price of land and, in turn, on the price of housing. Constraints on the release of land and development capacity (within and on the edge of cities) create scarcity, limit housing choice, and

increase housing prices. These impacts are disproportionately felt by people on lower incomes.

This entire argument can be demolished in two letters and 1 word: "U.S. South".

Throughout the entire period of throwing more or less free money at anyone who wanted a house loan real house prices in the US South region barely moved. Why? Because supply moved seamlessly with demand. And this region experienced growth rates in places much higher than Auckland has ever known.

This "research" is a more than a little fragile shall we say.

"Not I", said the horse.

I wasted 5 minutes of my time digesting what Auckland Council was trying to propagate. Bias research goal, wrong premises, wrong use of hypothesis, abrupt conclusion. Any level 7 student would had done better with an average supervisor.

Never listen/read any opinion from an 'employed economist'. The vested interest, in this case my $300K PA job,

dictates I present a report which exonerates my employer from all and any blame..

Put another way: If having already zoned to develop 20 times the current housing shortfall is not bringing land prices down at all...

...it might be due to Auckland having some of the worst spatial urban planning in the world.

Auckland is nuts.

We are facing a housing crisis in Auckland City and our idiotic regional authority (Auckland Council) has decided to open up huge over supply of land to all parts of the region EXCEPT Auckland City.

Taken as a whole region Auckland is doing most everything DEMOGRAPHICA might like in terms of supplying land and freeing up regulations. If someone wishes to develop land around Wellsford or Oneroa or Waiuku or Kaukapakapa the latest version of the Auckland UP has eliminated a lot of restrictions including any hint of a boundary. If someone wishes to develop around Warkworth or Kumeu or Pukekohe the council will provide extensive funded infrastructure within a very generous boundary expansion. Consequently, today Auckland region has more land available than ever before and probably much more than it could ever need. The council is so committed to overspending on land development, it is probably going broke soon.

Virtually the only part of Auckland subjected to suburban housing restrictions is land bordering metropolitan Auckland. If someone wants to develop around Greenhithe or Swanson or Takanini/Ardmore the council will not allow them. The allowed expansion of metropolitan Auckland is tiny.

Auckland is both indulging is a massive sprawl project at ruinous cost over the region and restricting city land supply jacking up land costs.

Auckland is nuts.

We have a perfect storm

- worldwide low interest rates

- high immigration rates (one reason for Auckland's increased house prices - most migrants stay in Auckland)

- restrictive land use zoning.

I agree with many of the comments above.

If the housing supply was completely elastic (i.e. I could add a marginal floor on any section in Auckland and keep adding those floors (i.e. no land zoning) until there was no profit left) then the only increase in prices would be the asset value change of $135,000 due to interest rate changes & possibly some of the "other" constraint costs.

Assuming the +115,000 covers "everything else & all other constraints" then the $240,000 reflects the inability of the housing "zoning" to elastically meet the increased demand without a lag.

Giving (240,000-85,000) / 405,000 or 38% on the price rise is simply due to land use regulation (which may well include infrastructure ("funding") supply constraints).

Well done. Not many people are studying the whole issue (apart from us property investors).

Of course similar arguments could be made about health and say it is landlords causing hospitalization of children due to poor housing rather than planners being responsible!

It is about time we applauded changes in our market. Change can permit and encourage financial, health, educational, and social advances. By the same token if we attempt to restrain growth nasty unintended outcomes can result.

Two thirds of my QV is land, but land supply isn't part of the equation? Say that again?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.