Train wrecks and their financial analogues are a worldwide phenomenon. Europe, as I have written for several years, remains a giant accident waiting to happen—as Italy reminded us last week. You may have noticed the results when US trading resumed Tuesday. A wider crash may not be imminent but is certainly possible and will have worldwide effects if/when it happens. So now is a good time to review what’s already happened and what could be coming.

This letter is chapter 4 in my Train Crash series. If you’re just joining us, here are links to help you catch up.

Briefly, my thesis is that over the next decade, we will endure increasingly damaging debt crises that culminate in a coordinated global default—“The Great Reset,” as I call it. There are limits in how much leverage the world can handle, and I think we are already beyond them. And that is before we have a global recession. The only question now is how we will manage the collapse.

I previously quoted former BIS Chief Economist William White on how this will all unfold. Here’s his key point again.

… the trigger for a crisis could be anything if the system as a whole is unstable. Moreover, the size of the trigger event need not bear any relation to the systemic outcome. The lesson is that policymakers should be focused less on identifying potential triggers than on identifying signs of potential instability.

Bill says the financial system is so fragile that practically anything could trigger a crisis. Better to watch for signs of potential instability… and in Italy, instability isn’t just a potential. It is a probability at some point.

Messy Politics

Italy had been without a government since its March 4 election, which yielded a hung parliament with no party or coalition holding a majority. The Five Star Movement and Lega Nord finally reached a deal, to most everyone’s surprise since those two parties, while both broadly populist, have some big differences. Nonetheless, they found enough common ground to propose a cabinet to President Sergio Mattarella.

Italian presidents are generally seen as rubberstamp figureheads. They really aren’t supposed to insert themselves into the process. Yet Mattarella unexpectedly rejected the coalition’s proposed finance minister, 81-year-old economist Paolo Savona, on the grounds Savona had previously opposed Italy’s eurozone membership. This enraged Five Star and Lega Nord, who then ended their plans to form a government and threatened to impeach Mattarella.

Such acrimony isn’t new in Italy. Politics there are messy, to say the least. Savona’s possible appointment set off alarm bells because it suggested the new government might try to take Italy out of the eurozone. Neither coalition party had raised that possibility in the campaign. The main promises were to reduce taxes and introduce a kind of universal income for poor and unemployed Italians.

In fact, the polls clearly demonstrate that Italians still want to stay in the eurozone. Not as much as the Germans or the French, but a clear majority. At the beginning of the euro experiment back in 1999, 81% of Italians supported the euro and now only 59% do. (Some polls show as much as 66%.) Whatever the number, we can see a trend there.

On the flipside, only a small majority of Germans supported the euro at the beginning and now 80% do. France has seen a smaller rise in support, from 67% to 71%. And that pretty much tells you everything you need to know about which countries the euro helped. And in a few paragraphs, we will let those numbers instruct us as to the future direction of Europe.

The slowly disintegrating numbers in favor of the euro and Italy reflect the fact that the Germans and French are better off than the Italians compared to 17 years earlier. Germany, joined by the Dutch, Finns, and Austrians, runs a monster $1 trillion plus trade surplus with the rest of Europe and the eurozone. And that makes the workers in primarily Mediterranean countries increasingly less productive than the northern countries, which ultimately forces their wages down. So, the northern Italian business populist party (Lega Nord) feels Italian businesses are losing out because of the euro, and the southern Italian populist party (Five-Star), representing an area where wages are suppressed and unemployment high, have serious concerns about the euro.

My friend Louis Gave noted that Mattarella’s decision was “not a crime, it was worse—it was a mistake.” Even Mattarella has now acknowledged that. In a face-saving measure, the two populist political parties suggested a new finance minister, Giovanni Tria, who has some (let’s just say) interesting economic points of view, but at least he is in favor of the euro and thus allows Mattarella to correct his mistake. But then he approved Savona, whom just days earlier he had rejected as a potential finance minister due to past anti-euro views, to be the new Minister of European Affairs. If you are confused, remember this is Italy. Everything is confusing there, except the food.

Fatal Flaws

Italy is not Europe’s only problem. The big Kahuna is Germany, which spent years offering generous vendor financing to the rest of the continent to entice the purchase of German goods. The result: a giant trade surplus for Germany and giant, unpayable debts for those who bought German goods. Greece, for instance.

But a lot of that debt is on the balance sheet of European banks. S&P just cut its rating for Deutsche Bank to BBB+. That is only a few notches above junk status. And if there were Italian issues? A lot of German banks could see their ratings fall to below junk. Ugh. Will Germany let Deutsche Bank fail? Simple answer, no. But they may not feel the same love for Deutsche Bank shareholders.

Spain is not quite the basket case that Italy is, but its banks are certainly wobbly. Spanish lawmakers this week gave a no-confidence vote to Prime Minister Rajoy’s conservative government and installed a socialist prime minister. The Spanish economy is actually much improved; other issues are creating political instability.

The UK is still winding its way down the Brexit path, which doesn’t directly affect the euro but is disruptive nonetheless.

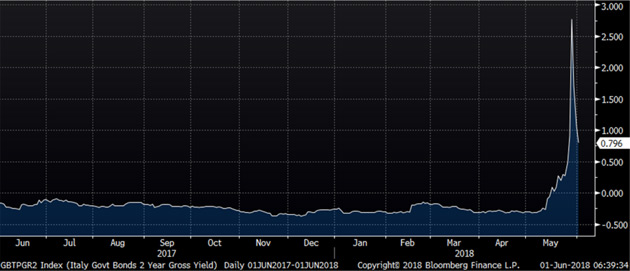

All in all, Europe is mostly stable but has problem spots like Italy. All it takes is one of them to bring the whole structure down. That’s why we see market moves like Italian two-year bond yields zooming from below zero to almost 3% within days and then falling below 0.8% the next few days. That’s some serious volatility. (h/t to Peter Boockvar for the chart.)

That’s not normal and doesn’t happen in a monetary union in which all the members share the same goals. And that’s kind of the problem: European governments have irreconcilable interests and thus don’t trust each other. By accident of history and geography, the continent is fractured into dozens of competing economies, languages, and cultures. Unity has long been a dream, but only a dream. Simply avoiding war is hard enough.

The Euro currency union is fatally flawed because it leaves each member state to set its own fiscal policy. There are good reasons for that, but it is not sustainable indefinitely. The Eurozone must get either much more centralized or fall apart. All the Rube Goldberg contraptions the ECB and others invent are temporary fixes. They’ve worked so far. They won’t work forever. And that brings us to the latest strange proposal.

Parallel Currency

Italy’s situation could blow up the fragile trust that keeps Europe together, and the leading parties may even be planning for it. The discussions between Lega Nord and Five Star included an idea called the “mini-BOT” that would effectively serve as a parallel currency.

The BOT is Italy’s Treasury bill, and as in the US, it serves as a kind of cash equivalent in electronic trading. The mini-BOT would be a government debt instrument, in paper form, that pays zero interest and never matures. The government would use it to pay social benefits and accept it for tax payments. Private businesses would not be required to accept it, but they could.

Private businesses and individuals would also, in theory, buy the mini-BOT as a way to pay their taxes. But they would buy them at a discount. So, traders would immediately set up an arbitrage where the person getting the social benefits payment could sell them for euros for, call it, a 5% or 10% haircut. Former Prime Minister Silvio Berlusconi, who is still a force in Italy, insists this would be legal. The Northern League sees a way to ease the transition out of the euro and the Five-Star Movement sees a way to increase spending without having to take on euro debt. And since the new coalition government wants to increase the deficit an additional $180 billion euros or so through a combination of tax cuts and increased spending, this is being seriously proposed.

The mini-BOT probably could be a practical alternative to the euro for many transactions. From what I’ve read, the other eurozone countries would have difficulty stopping it because the euro would still be the only formal “currency.” And other Mediterranean countries would watch this experiment and begin moving in the same direction themselves.

You see where this goes. Italy might be able to use mini-BOTs (or let’s be honest and call them the new lira) to finance deficit spending without breaking eurozone rules. This could ultimately debase the euro and blow apart the eurozone. Germany would have to leave. From there, you can draw your own map.

Is this what the Italian populists want? Some of them, yes, but I suspect their leaders know not to go too far. More likely, they see it as a bargaining chip—a plausible threat they can use to extract concessions from the ECB and other eurozone leaders. The Greeks threatened something similar in 2015 and it didn’t work. I think Italy has a stronger hand.

But it gets scarier when you think about how this could happen. If Italy’s new government decides to launch a parallel currency, they will probably do it with no warning at all. Tipping their hand would spark capital flight and reduce the benefits. We could literally wake up one morning to learn the lira (or something like it) is back and Germany is leaving the Eurozone. Imagine how markets would react.

I think this scenario is unlikely, but it points to something else. As the coming debt crisis matures, national leaders and central bankers will find their choices narrowing. I’m constantly amazed at their creativity, but it has limits. They can’t kick the can down the road forever. At some point, the road ends and then they have to choose. When your only choices are “impossible” and “terrible,” then you pick the latter. We are going to see previously unthinkable ideas be seriously considered, and sometimes chosen, because all other options are even worse.

The Mutualization of European Debt

Here’s the problem that’s brewing. Germany and the other northern countries, but especially Germany, have prospered tremendously under the euro regime. If the eurozone were to break up, German GDP would simply fall out of bed. Half its economy is comprised of exports. Further, the new German currency would get stronger which would even put more pressure on German exports.

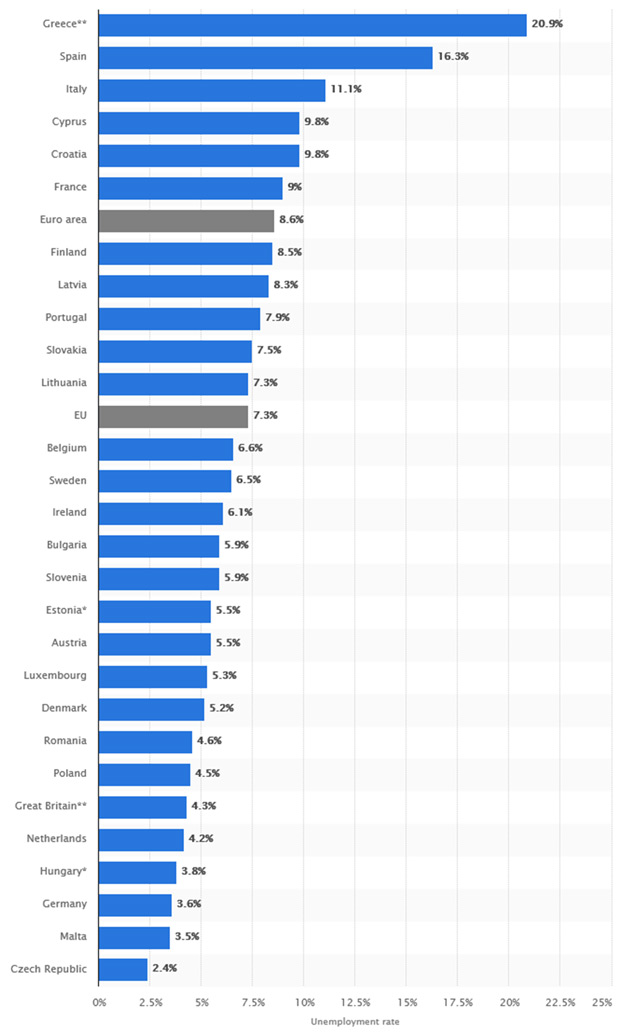

The Italians have no solution for their debt. Greece has been in a seven-year depression. And while some of the other countries are improving, unemployment rates in most of Europe are still lackluster to say the least. See the chart below and notice the high unemployment rates. And understand that the unemployment rates for young people (millennials) are probably double that. One in three Italian youth are unemployed.

Source: Statista

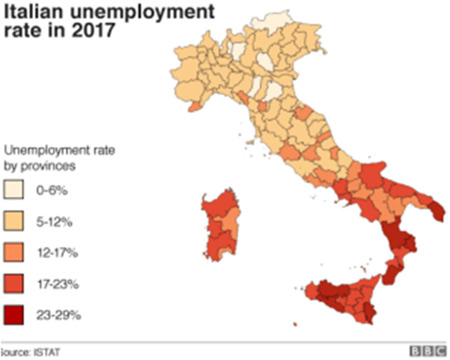

Let’s drill down on Italy’s employment data. Notice the further south you get, the higher the unemployment rate goes. That’s the Five-Star Movement’s base. The other part of the new majority is now called the League (formerly the Northern League) and is powerful in the low unemployment manufacturing regions of northern Italy. And for all the Italian problems we’re talking about, Italian manufacturing is a powerhouse. (Map h/t to Dennis Gartman.)

This is why you can’t entirely dismiss the notion of a parallel currency in Italy. The southern portion of the country wants to see more spending and the northern portion would like to ease out of the euro. Politics makes extraordinarily strange bedfellows in Italy. It’s not quite as outlandish as President Trump and Bernie Sanders forming a coalition government, but it was unthinkable just a year ago.

Germany and the rest of the export driven countries need to stay in the euro in order for their economies to grow and prosper. The southern countries need to figure out how to deal with their debt. Italy is around 135% of debt-to-GDP today.

I still think the most probable scenario is that Germany and the Netherlands reluctantly agree to let the European Central Bank mutualize all the sovereign debt, taking onto their balance sheet and issuing new ECB-backed debt for the entire zone. There would have to be serious constraints on running deficits after that point, but it would prevent a breakup, or at least delay it for another decade or so. Kind of the ultimate kicking the can down the road.

Market Fireworks

None of these dire possibilities appear to be in play right now. One way or another, Italy will slide through this. It could drag on a few months. But Tuesday’s market spasm ought to be a warning sign. Traders still know how to hit the “sell” button and will do it quickly if something surprises them. This time, it was manageable. At some point, it won’t be.

My friend Doug Kass, a brave soul who has been trading longer than most, actually turned bullish on banks following this week’s selloff, shedding his short positions.

After Doug wrote that, the Federal Reserve Board voted to loosen the Volcker Rule that had limited proprietary trading. Other agencies must agree, so it’s not a done deal yet. In theory, this should help banks and may also restore some of the bond market’s lost liquidity. I don’t think it will solve all our problems or prevent the larger crisis that I think is coming.

Charles Gave, who was also trading before today’s wizards were born, is questioning some of his assumptions. His longtime models say the time is nearing to sell US stocks and buy German stocks. But that model makes assumptions that are no longer true. For one, it assumes capital will flow to the place where it can be used most efficiently, and exchange rates will stay suitably flexible. Neither is necessarily true in an era of collapsing alliances and rising trade barriers.

Speaking of trade, with Trump once again getting ready to impose steel tariffs on the EU and lumber tariffs on Canada, things can get even more volatile. Since lumber is basically 20% of the cost of a house, a 20% increase in lumber prices (a gift to US lumber companies) would raise housing construction cost by 4%. Cars and aluminum cans would rise in costs. Not only are the countries that are paying the tariff being taxed, US consumers will be taxed with higher prices. This is not exactly the best way to stimulate an economy. Worse, it could all change again as negotiations continue, and businesses need policy certainty.

I haven’t written yet about the housing markets in Canada and Australia, both of which are in worse shape than the US was ten years ago. Especially Australia. You can just go around the world and find Bill White’s “pockets of instability” everywhere. One or two here and there is not an issue. The world typically just shrugs it off. But we are now beginning to see problems in a much larger geographical space. Argentina? Mexico electing a radical socialist? Where does it end?

------------------------------------------

*This is an article from Thoughts from the Frontline, John Mauldin's free weekly investment and economic newsletter. This article first appeared here and is used by interest.co.nz with permission.

- Credit-Driven Train Crash (May 11)

- Train Crash Preview (May 18)

- High Yield Train Wreck (May 25)

35 Comments

...the size of the trigger event need not bear any relation to the systemic outcome...

That's the exact definition of a systempunkt, to use John Robb's neologism. Small investment or input, massive payoff or result. JR coined the term to describe early-aughties terrorism thinking, but I've always thought it applies equally neatly to geographical, tectonic and other physical configurations. NZ, an irreducibly pluvial country to steal a phrase from Sir Geoffrey Palmer, viewed in this light, is a long chain of systempunkts....as the weekend's rain events demonstrate. SA's electricity grid is another.

And Interesting, innit, that Mauldlin uses Australia to illustrate another 'pocket of instability'. Has the guy never heard of Awkland?

And Interesting, innit, that Mauldlin uses Australia to illustrate another 'pocket of instability'. Has the guy never heard of Awkland?

Much as we may have heard of Kentucky* but don't bother mentioning when talking about the US, I'm sure Mauldin is aware of the existence of Auckland, but also its irrelevance in the grand scheme of things.

*Fun fact Kentucky's GDP is pretty much as large as New Zealand's.

"Canada and Australia housing markets are in worse shape than the US was ten years ago". True, but NZ is Australasia's housing utopia! (extreme sarcasm on my part)

property never crashes in NZ, maaaaaaaaate!

Fritz, Thank you for that, brilliant.

lmao

Lol, so good!

Priceless!

Europe is definitely showing signs of imminent catastrophe.

Greece is not in the MSM anymore, but is nowhere near resolved.

While the current focus is on Italy, it shouldn't be forgotten that both Spain and Portugal are equally destitute.

Brexit will happen, and if anything is more popular now than at the time of the vote.

The "new" nations are really just draining the dregs from the German Keg, rather than supplying their own one.

The last point is the key to everything really. The EU survives solely because Germany is keeping it's wallet open.

Once that is closed, it will be more than the EU that goes down. After all DB has effectively spread the debt globally (among Western Nations)

Once the first domino goes, well....

Germany caught screwing over other EU member states on gas. Brexit can't happen fast enough.

"The report suggests that Germany has been enjoying a sweetheart deal with Gazprom, gaining a competitive advantage in gas costs at the expense of fellow EU economies and leaving front line states at the mercy of Moscow’s strong-arm tactics.

Hundreds of pages leaked from the European Commission paint an extraordinary picture of predatory behaviour, with Gazprom acting as an enforcement arm of Russian foreign policy. Bulgaria was treated almost like a colony, while Poland was forced to pay exorbitant prices for imported flows of pipeline gas from Siberia."

https://www.telegraph.co.uk/business/2018/04/12/leaked-eu-files-show-br…

Yes, Italy is quite likely the powder keg that blows up the Eurozone - and how can it be any other way? Politically you simply can't go on with the status quo in the face of the cold hard economic facts: On joining the euro GDP per capita in Italy was 20% higher than the average in the euro area. Today it is 20% BELOW the average. Unemployment in Italy is 11%. In Germany it's 3%. What is telling is that it isn't just the disgruntled working and middle classes that are angry. It is the local elites. Throw into the mix an influx of migrants via Libya thanks to the West's destabilization policy in the area with little EU assistance and you have the recipe for some neo-fascist, nationalist, populist politics. Alas, we all knew this was coming. The Eurozone either has to change big time and start funneling northern surpluses into Club Med and writing off sovereign debt OR it has to go.

"The Eurozone either has to change big time and start funneling northern surpluses into Club Med and writing off sovereign debt OR it has to go."

Yes, the Euro Bureaucracy will be all for the funneling.

The average person on the other hand... Well that's how brexit happened.

I watched an old documentary about Black Wednesday and the UK's over night exit from the ERM. How quickly things can change eh?. The supposedly unthinkable happened in a blink of an eye. I was not a fan of Ms Thatcher - but on the Eurozone and its perils for national democracies she was spot-on. What works in terms of monetary and fiscal policy in Germany simply is not right for Italy.

Who remembers the phrase coined a few years ago ......." kicking the can down the road " when describing all manner of fancy economic polices to avoid a recession / depression etc, and who even remembers the name Bernard Benancke ?

The US had QE , the Europeans had something similar which was simply printing more money , even China loosened monetary policy ... all just playing football with a can in the street .

So what happens to the can in the street game when :-

1) You run out of road

2) Its gets dark

3) the Cops come out and tell you to stop and confiscates the can

4) Everyone loses interest and goes home and simply carry on as if there is nothing wrong

5) the can owner wants his can back

5) the can falls apart

6) a key player ( Italy ) gets annoyed with the ref and storms off the field .

For almost 10 years now I have said that QE would eventually bite us on the backside when we turned around or were not looking

I assume you mean Ben Bernanke?

I remember that guy, in fact some of his papers are quite interesting and well considered. However when he was the Fed Chair is seemed to forget everything he knew.

I'm not sure that Italy will be the trigger event. There are so many issues everywhere and it's a matter of which one will create a cascade effect on failure. We can determine the cause of the failures after the event but I don't recall anyone discovering the exact point where the first failure occurred.

I also wouldn't treat Italy in isolation. All EU banks own a proportion of each others debts. If cashflow from one stops it will create cash flow problems for the other banks. That said a bank failure to bring down the EU would need to be large well networked bank involving a lot of euros.

It's called Deutsche bank!

Deutsche Bank having only 0.01% capital to support their loan book and the trillions in derrivatives what could possibly go wrong?

Iran feels to me like a ticking time bomb for instability. Massive youth population, and plenty of economic issues.

Northern middle east / Mediterranean feels a bit of a flashpoint.

I guess Maudlin thought he’d best join the chorus about GFC2

I’m just amazed there’s no attached link to send us for a subscription to his services as per usual

This guy was one of the greatest stock market spruikers

Guess he’s short the market these days

You are good man , I do indeed mean Ben !

Just checking to see if anyone remembered Ben

I do find it amusing, as a Pom, to see feedback on this site which is very easily convinced of a crash in Eu but not nearly so easily of one in Australasia (i.e. incl NZ) Australia and NZ are FIRE economies and with too narrow a base. USA is a service economy but only 14% of economy is exports. And self-suff in most kinds of oil needs. EU is primarily industrial - the make things, unlike NZ. As NZ did not have a crisis in 2008-11 but rather a slow down in housing market (still had 6% growth in those years, total) NZ folk do not really know what a depression size drop is like (except for older - who remember 1987-94) NZ has been in a sweet spot thanks to China spending and printing, since 2009. This is now ending. NZ demographics peaked for spending, in 2016 and next increase in that age group (40-47) is not due till 2023. Til then GDP will shrink. Treasury 3.3% for 3-4 years - yeah, right.

Pretty fair points but there is a difference with NZ, their exports are food which is not optional like a BMW/Washing Machine/TV etc so food demand is unlikely to vanish but may decrease in volume & value, the manufactured goods however may shrink in demand & value to almost zero. NZ & Australia are also more self sufficient than many EU countries so survival is assured and was a reason Ieft the UK over 20 years ago when I saw the direction the SSRE (Soviet socialist republic of Europe) was headed in, I hate the EU bur love Europe and especially my country of birth that will once again prosper and regain its independence after March 2019's exit from the evil empire.

"Un Zul'n us duff'runt un spusshull!"

Every damn time, without fail.

The European Union always was a CIA project, as Brexiteers discover

It was Washington that drove European integration in the late 1940s, and funded it covertly under the Truman, Eisenhower, Kennedy, Johnson, and Nixon administrations.

https://www.telegraph.co.uk/business/2016/04/27/the-european-union-alwa…

Well...yeah...but WW1 and WW2 were pretty strong incentives to try to create a more unified community in Europe than had existed there in the previous 100 years.

I don't see the next crisis starting in Italy, the situation in Italy has been bad for long time, the Italians have been poor and put up with a lot of shit for a long time. However like the rest of the pigs they like the spending power of the Euro, yes their economies are in a shambles but at least the Euro is still worth a Euro, backed by the Bundesbank with all the might of Germany behind it.

In 2008 the local Porsche dealer in Rome had special on cars with € 500 down, something that should never happen in Italy, so yes a crisis was coming but it's been held back by the EU.

I think it's Spain where it will start, exposure to German and French banks will crank up the pressure, a lot of people in Spain are looking for a fight, too many immigrants keeping wages low and times are very tough for many. My French friends openly talk of the next revolution, Europe is a powder keg and no one can control the out come.

Viva revolution?

It’s revolution rhetoric every day in French Italian Spanish etc households

Italy Spain Portugal whatever they’re all up the creek

As for speculating on what will be the catalyst for GFC2 it’s clear corporate debt is at the very least a factor

Please don’t use the “S—-“ word Andrew

It’s so unbecoming of you

Or maybe it explains a lot ?

I had to replace the S word, it would be with corruption.

I think the EU is accelerating the demise of the euro. Remember that when they converted into euros back in the late nineties, many of the southern countries saw their debts double in real terms with the appreciation of the euro, Greece being a case in point. They have in fact gone backwards with the EU. EU banks are in big trouble and there is no consolidated debt behind the euro, so it was never going to compete with the usd. Add to that the fact that the ECB is the only buyer of EU govt debt at the moment and you have the trigger for a collapse in the euro and all the spending power that it once had. A dangerous time to have savings in euro accounts...

Emerging markets face a dollar double whammy

https://www.ft.com/content/e193381a-64c1-11e8-bdd1-cc0534df682c

Fintorque 20 hours ago

We witnessed peak Eurodollar a few years ago as a direct consequence of the changes in global bank regulations that were implemented post Global Financial Crisis.

Not only are there now less offshore dollars available but they are also less fungible. For instance the main international financial centres have tightened restrictions on banks deploying funds around their networks overseas. The dollars become trapped and have to be deployed locally.

This means that overseas sovereign, financial institutional and corporate borrowers of dollars are more vulnerable to changes in the US monetary and fiscal policies. Both taper and Tax (TCJA) will increase price and availability pressures.

This is unlikely to hold much sway in the US but it may well prove a harsh and costly experience for offshore dollar borrowers. The fallout will be a further bifurcation of borrowers and for those whose offshore dollar access is either restricted or too costly, accelerated use of non dollar funding alternatives.

Recently a friend told me about a conversation she had with two kids behind the counter of a Subway sandwich place in a South Island town. They were giving her all kinds of advice about investing in residential property due to becoming experts as a result of buying a couple of local houses with a view to on-selling for a substantial profit.

The above is only a very small part of a frightening global whole, but I think it's safe to say the Joe Kennedys of this world definitely would have cashed out of the market by now.

when debt is thrown around like confetti to anyone with a pulse it's time to worry. Oh dear NZ

And why wouldn't you? With an OCR of 1.75, the RBNZ obviously wants everyone to go into the marketplace and take huge risks.

They don't want people to save.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.