By David Hargreaves

I normally keep quite a close eye on the monthly mortgage figures by borrower type that the Reserve Bank has now been publishing since August 2014.

This month I kind of missed it, given that the figures came out less than 24 hours before the RBNZ announced a further tweak to its 'speed limits' on Wednesday. I was distracted.

And I missed the housing investors seemingly disappearing into a rather large hole. Well, that's a bit melodramatic, but in short the investors had their smallest monthly share of the mortgage borrowing in October since the RBNZ started publishing that data - and it was the smallest share by some way.

The investors share of the overall figures dropped to just 18.7% in October from over 21% the previous month.

I wonder about this and wonder whether when we see next month's figures it will appear to have been a glitch, or was something else going on? Were the banks anticipating perhaps that owner-occupier lenders would see their lending limits lifted by the RBNZ (as they did), but the limits for investors would be left the same?

Certainly, while I expected the RBNZ would tweak the LVR settings for owner-occupiers, I did think there was a fair chance the investor deposit requirements would be left the same. I think they should have been.

So, were the banks anticipating no change for the investor settings and holding back a bit, while loosening things up on owner-occupiers? And it is worth stating that the detailed October LVR figures actually show the highest portion of high-LVR lending advanced by the banks to owner-occupiers since the 'speed limits' were first introduced in 2013.

For the record some 13.7% of the total amount advanced in October was for mortgages with a deposit of less than 20%, while the total after exemptions (which include things like mortgages on new builds) was 10.3% - also a new high.

Anticipation ahead of the event

So maybe there was a certain anticipation on the part of banks of some loosening, even though this doesn't take effect till the start of next year. And of course it may well represent the increased competition for mortgages between the banks we have seen in the past month or two.

The other thought about the decline of the investors though is whether this is a delayed reaction to the extension of the bright line test, the capital gains tax that dare not speak its name, from two years to five years in March. Or was it in some way a reflection of the foreign buyer ban that came into effect in October?

The reaction of investors to the more relaxed deposit rules they face from January 1 - they will now need 30%, down from 35%, will be quite pivotal, I think, in how the housing market performs through and after summer.

Some background

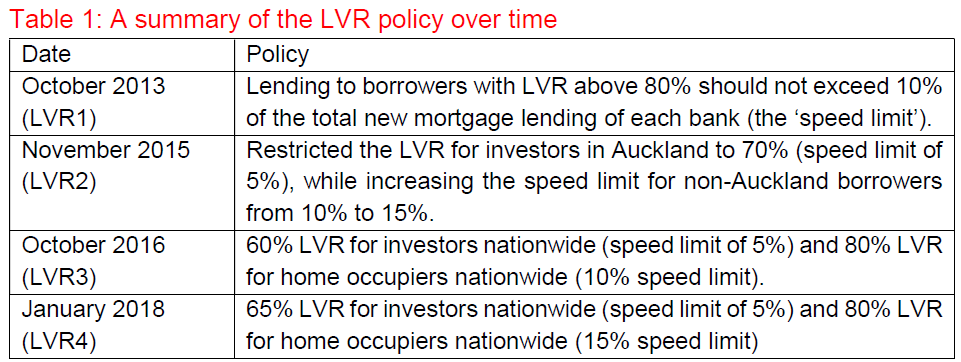

The new iteration of the LVR rule can be described as LVR5 (sounding more like a Hollywood blockbuster by the minute). I'll just reiterate what the new rules are from January 1:

- Up to 20% (increased from 15%) of new mortgage loans to owner occupiers can have deposits of less than 20%.

- Up to 5% of new mortgage loans to property investors can have deposits of less than 30% (lowered from 35%).

And now, courtesy of the RBNZ, here's this very helpful table of what happened with LVR versions 1-4:

I'll summarise the impact of those a bit. LVR1 was officially described as a success. A rampaging Auckland market DID slow. The great unknown about that first iteration though stems from the fact that it just so happens that it coincided with FOUR interest rate hikes from the RBNZ. Now, with or without the LVR measures those interest rate hikes WOULD have hit the housing market. So, while the RBNZ's always been quick to ascribe success to LVR1, I think you need to exercise a little caution around that. Personally I think the LVRs and the rate hikes probably worked 50-50 together.

The Auckland firestarter

Okay, then there was LVR2, the Auckland-centric one that just didn't work at all. Basically it encouraged Aucklanders with money to look outside Auckland for investments, and they did, and the housing markets in the rest of the country - which to that point had lagged Auckland in terms of price rises - then started to take off as well. I might say, I thought the Auckland LVR measures were a good idea at the time and was pretty astounded by how badly they failed. Unintended consequences and all that.

So, then we had LVR3, and it's from that point on that I will busy myself with here. That's where is all really got started and set us up for where we and the housing market are today. This is the one that took the blunderbuss to the investors - and boy, was there a reaction.

Some crunchy numbers

To demonstrate that, I'm referring to figures from October 2014 to October 2018, but also with the figures for June 2016 thrown in. While that table just above suggests the LVR3 iteration came into effect in October 2016, that's actually a bit misleading. It was announced in July by the RBNZ and the banks began to implement the 'spirit' of it straight away - so the impact was in fact immediate. Therefore you can say the June 2016 figures are the last ones before the investors began the retreat.

If, we look back to October 2014, investors represented 29% of the mortgage money advanced. In October 2015 it was 29.3%. By June 2016 it had climbed steeply to 34.8% (in dollar terms that equated to nearly $2.4 billion) but then, remarkably, by October 2016 it had shrunk to 23.6%. In October 2017 it was 22.7% and as stated earlier, in October 2018, just 18.7%. That's quite a retreat.

LVRs and distortion of buyer patterns

Good as the RBNZ mortgage data breakdowns are, it's a shame we don't have full figures available for pre-August 2014. One thing that would be interesting to get a handle on is the extent to which (and I suspect it was quite a lot) the first iteration of the LVRS in 2013 blocked off would-be first home buyers and encouraged investors. Did we end up with a distorted market because of the first wave of LVRs? Were investors effectively given a hand-up at the expense of the FHBs? You can debate it. I think, yes, they were. Those unintended consequences again.

Anyway, the situation has very much reversed since the investors were hit with the big deposit requirements.

The revival of the FHB

Going back again to October 2014, the first home buyers took just 9.5% (less than half a billion dollars) of the total mortgage money advanced that month. By October 2015 the share had increased a little to 11.5%, but by June 2016 it had shrunk to 10.8% amid the investor onslaught. However, the FHBs were not quite finished. By October 2016 they had 14.4% of the mortgage money advanced that month, then 15.7% in October 2017 and 16.6% in October 2018. And lest you think it's all about a bigger share of much less total money, the amount borrowed by FHBs in October 2018 was nearly double (at over $900 million) the amount borrowed in October 2014.

Put it all together then and what are we expecting when the new LVR5 takes effect from January?

Looking ahead

It's worth considering what happened as of January this year the previous loosening took effect, given that the loosening from next January onward will be of similar magnitude (IE 5 percentage point tweaks for both investors and owner-occupiers).

Here, I shall compare the first 10 months of 2017 (before the previous LVR tweaks) with the first 10 months of this year, taking account of the tweaks.

For the first 10 months of 2017 new mortgages averaged $4.867 billion a month. This year it has been $5.272 billion a month.

Within this, in the first 10 months of 2017 mortgages on homes where the deposit was less than 20% averaged $306 million a month. For the first 10 months of this year the figure was $431 million a month, which is an appreciable rise, but not enormous.

$100 million a month more in mortgages?

It does suggest though that perhaps a rise in new mortgages of somewhere above $100 million a month might be expected from next January, which would certainly help the housing market, but would not appear likely to set it on fire.

The first home buyers are likely to be in gangbusters. Over recent months about a third of the mortgage money advanced to FHBs has been in high-LVR mortgages, so, you would imagine the FHBs would be in for a fair share of the extra mortgage money wiggle room the banks now have.

Really, the key thing then is what happens with the investors. Will the reduction in deposit requirements for them be enough to encourage them back into the market in bigger numbers, competing again against the FHBs and maybe driving prices higher?

What will the investors do?

The answer to that question will be crucial. It may be that the problem for a lot of wannabe investors would not be the LVRs, but the bright line test. In which case, the obvious question is how many so-called investors were never there for the rental yield but were only thinking about capital gain? Specuvestors? And over a short period of time, it seems.

With interest rates set to stay low at least for a year (barring bad external shocks) the FHBs seem sure to stay out in the market buying up this summer.

The real test will be if there is a resurgence of investor interest. If there isn't then the RBNZ will have been right to loosen the LVRs. But if there is, the game changes, and that's also the time we might see our FHBs overstretching themselves.

I'm not even going to attempt to pick which way this one will go. All I would say is that this situation is going to need both eyes very firmly focused on it. As they say, anything can happen, and it probably will.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

87 Comments

I'm seeing a few places in my area selling for high sums and then being rented out for reasonable prices. One house sold for 2.25M and is now offered for rent at $790 a week. 2.25M would earn far more than that in a term deposit after tax.

It looks like there is still confidence in properties in the leafy suburbs that have good sized freehold land.

Agree with Zachary.

Well-located property with good-sized freehold land will always be attractive to investors - and homemakers.

Add to that a northerly (sunny) aspect and drive-on and you'll be well-placed for the future - especially as NZ's popularity on the world-stage grows further.

TTP

rents reflect incomes.

nothing to do with what the recent sales price was

house prices reflect credit growth

nothing to do with incomes

Hi H_T,

Note that the unifying factor for both rents and house prices is the market: namely, the relative forces of demand and supply.

TTP

Agree, except rent (in NZ) reflects incomes plus the Accommodation Supplement. Something has got to be done about that market interference by the government.

In my area the preferred purchase at that price point is an older house on a 800m2 section. It’s all about the development potential, not the rent. Look forward a couple of years and there will be two new $2.5M homes on that site. An average quality home on an undividable site is far less popular and the price reflects that as it’s neither Arthur nor Martha.

Any update on your Corelogic price Expat?

Still the same as I posted earlier this week, 100% of CV as at 25/11

I missed that. Thanks for the update.

It depends. The margins on newer houses are very thin. So developer beware.

You'd need a CAGR of around 2.5% to break even, which seems easily achievable, especially in the longer term. Auckland averages around 7% in the long term.

Now premium property in Prime area may still fetch a decent price.

That's an abysmal yield of less than 2%

.Yvil

Agreed it’s a abysmal yeild

Abysmal investment at this time in the property cycle too

Lucky I sold my Sydney property when did

Sea change buyers on GC have yet to wake up It will hit there too eventually

Early Merry Xmas NZ from Bermuda

Sadly no longer has The America’s Cup but still great sailing

Enjoy Bermuda, I always wanted to go there. Glad they're not hosting the amerce's Cup though,cause WE ARE!

Thats a terrible return and the landlords will be bleeding money. How long will they want to do this for with no capital gains in site and a downturn on the horizon?

From an investment standpoint. Isn't that a terrible yield? Works out to 1.8%.

Way too many concerns around “disadvantaged investors “ . Let them invest in something else. Why there are not many stories about FHBs and other home owners challenges ??

andreas_od - Good questions. Just follow the money is all I can say ! But here is something to watch.

https://www.youtube.com/watch?v=3qiUN_lUw4c

While I don't have too much sympathy for investors, I think there are some issues brewing with the private rental market.

In many cases now property investing is a poor option. Yields are usually poor, future capital gains probably limited, and more onerous regulations present.

I think this means that moving forward we will see less investor interest in new housing. If that is the case, and if there is a limit to how many Auckland FHBs can buy, then I think the private rental market could get really tight.

This could well create a number of problems.

i think as the governments change you will see backwards and forwards on regulation, a bit like employment law is now.

so for investors they will need to factor that in as well as financial aspects of the investment.

where before both major parties sold down the state housing stock we will also see the left build the numbers back up and the right halt and sell some when they are both in power.

the BIG question for investors will be immigration, with the current level investing is still fine and long term looks good, if that changes then that could flip the whole market

Sharetrader - but do you think buying new build townhouses and apartments is a good investment? (generally speaking). You are lucky to get a gross yield of more than 4%, and capital gains may be muted when there is effectively no land with the investment.

i dont think rental housing is a good investment from personal experience, you need to put in time (which is unpaid) for a average return,

in saving that last 5 years was different all you had to do was buy hold a couple of years and sell for a nice return.

rental housing investment is the easiest to get debt for leverage from the banks, try them for a business loan much much harder, yet that business might take off and return 20% per year

Leverage is the key - if you can get a 1% yield after interest on a ton of money you don’t even own, that can work out a lot better than any other investment.

Just remember that leverage can take away as well as give. I know more than a few people that have erased their lifes savings via the wonders of utilizing leverage on investments that have risk.

On a more anecdotal level, I wonder how that guy is doing now that mortgaged his house to invest the proceeds in bitcoin last year... sometimes, one doesn't learn until too late that the final support level is at zero. On a more recent note, there is the guy that sold naked calls on natural gas via his limited partnership, just prior to the recent huge spike (see this video: https://www.youtube.com/watch?v=VNYNMM0hXXY ). Leverage is great until it isn't...

Rents will rise, and accommodation supplement will have to rise because child poverty is a failure of capitalism, what else could you call it?

A failure of monopoly capitalism, perhaps?

Meaning the rise of monopolistic ownership type stuctures. There seem to be two sorts of these. The obvious type is the Facebook/Microsoft/Apple/Amazon/Netflix mega company that just buys up competitors, and effectively owns the rights to its customers.

The less obvious type is the monopoly cartel, where you have say, two supermarkets who are able to dominate both their suppliers and customers. This type is rampant through our housing market, as banks, building suppliers, councils and the central government have destroyed our ability to deliver housing at reasonable prices.

It's all darn complicated, but the banks have a monopoly on credit creation, which destroys the ability of people with equity to compete, thus driving up house prices with new money at absurdly low interest rates. This destroys the ability of a capitalist economy to allocate resources effectively as the pricing sends false information. It makes speculating in housing look like a more productive activity than it is.

Good points.

And then taxpayers subsidise property investors via the accommodation supplement and Working for Families, raising rent floors and holding back wage growth.

Add to that the RB throwing the banks a life line every time loan growth softens. It's a perpetual cycle no politician has the guts to break.

Houses, Kiwis, go together like a horse & carriage.

Nothing else stores value the same regardless of the financial & equity machinations in other investment areas.

Hi Mortgage Belt,

You make a solid point.

There's a deeply-ingrained culture of private housing investment in NZ. But this aspect of investment often goes unacknowledged or completely ignored. Nonetheless, like the All Blacks and fish 'n' chips it's a basic part of our society's fabric.

Housing investment is very multi-faceted: financial/economic, legal/regulatory, social as well as cultural.

TTP

...and speaking of Ireland, don't most unexpected things happen from time to time, just when they're least expected...the 'dead cert' loses...

Just because property is a NZ legacy doesn't mean it should remain that way forever and a day. There have been consequences as a result of our property obsession such as a long term decline in productivity.

I've seen lots of horses in the last week on holiday in the South Island.. not a single working carriage though (just static displays of days gone past). Maybe your analogy is more accurate than you realise?

What made you think the horses were on holiday there rather than residents? Trotting all over the road and veering over the centre line?

Heh, mostly standing round in a field eating grass... not a single one was seen breaking a sweat.

I would think RBNZ are feeling content at the moment; a relatively stable housing market contributing to economic stability, and FHB being a little more active in the market.

RBNZ is managing this not only through LVRs but also partially through a continuing low OCR. The historically low OCR is not only helping exporters by keeping the dollar subdued, but also FHB and mortgage holders with historically low mortgage rates.

As for investor activity in the market - the ones I talk to hardly mention the influence of LVRs, rather the current very low yields and downside risks to the market as the primary reasons for not investing further. Most of these investors don't have too many issues with compliance costs although they have concerns with changes in legislation, but more importantly they see this as the government that is anti-landlord and are increasingly concerned that this presents significant concerns for future investing.

While we mention the lack of FHB, I think that given the current yields, there is likely to be very few first time investors currently entering the market. There is no data seemingly available on this. If it is the case with few first time investors entering the market, then this is not positive for a sector - despite a love of many to slag them off - that is essential in providing necessary housing and accommodation.

I for one found the 40% deposit to be a bit much, but PI's love to pretend to be rich so it's hard for them to admit they can't afford it. Conversely the higher the deposit, the better the cashflow, but building the equity of a portfolio up to 40% when it was at 20-30%, is challenging, especially with slow growth in property values.

So if we assume that many investors are in this position, and the currently mild "negative growth" continues for a couple of years. What does that do to investors who want to get back in the market?

"Pretend to be rich" lol, others have a perception PI are rich and loaded. Being a PI doesn't feel like rolling in cash most of the time for us anyway. Some older investors may well have plenty of free cash though.

As regards borrowing the main issue for most investors is servicing the loan if solely using rents

Hi skudiv

It is not about pretending to be rich.

The investors I mainly talk to are those who are fairly well established in property investment having tended to been in the rental market for some years. Therefore they have seen capital values rise in not only their own home (which most leverage off) but also their existing rental property(ies) which commonly are a couple.

Due to significant capital gains - which upsets many - LVRs are not a significant issue as they can raise further capital through the equity in these properties.

The LVRs will be a bit tough for both potentially new property investors (and as I have posted - a concern) and those who have been in property for a relatively short time and have just their home and the one rental property. For both of these groups, leveraging to raise money to meet the LVRs is likely to be more of an issue especially - as you point out - there is slow (flat) property market.

So potential and relatively new investors are being affected by the current LVRs. Within the next few years I can see a time when these two groups become more active in the property market - that is when there has been some growth in their existing equity and increasing yields make it more attractive. In the meantime - like long term investors - they are going to be relatively inactive in purchasing property at least until yields start to improve which could be due to either falling property prices (some likelihood), but more likely, continuing increases in rents.

As for property investors being "rich", a group of us were discussing this a year or two back. The conclusion was that despite most owning two or three rental properties, none of the investors considered themselves rich - "comfortable" and "secure: were more significant descriptives used and were the main goals for property investors. All agreed that property investment meant quite a bit of hard work especially bookkeeping, consistently monitoring payments and tenants' behaviour, a degree of nous (read as "having a bullsh*t filter"), and taking some risk.

Nous equals "having a bullsh*t filter"

The best part of your comment, cheers

I think most property investors are by nature cautious, even slightly paranoid and tend to be Scrooges. There are notable cases of people jumping in and buying sixteen properties or something but this is rare. Most will know that the lower the equity in the properties the greater danger of a complete wipe out.

They will factor in a 30% or more drop in prices and ensure they will still be able to operate and hang in there. Having many properties and only 10% equity would be considered foolhardy in the extreme. They will count pennies and let the pounds look after themselves.

So they rarely feel wealthy. Reserves are not for spending frivolously. Revolving credit is an emergency fund not an ATM. Spare cash is used to increase equity and goes into the mortgage and not on expensive cars and holidays.

After quite a few years of managing the portfolio and as equity increases the purse strings are loosened a little but old habits die hard.

If someone suddenly inherited a typical portfolio along with mortgages they might feel wealthy and splurge out but not someone who has spent decades building things up. They didn't get into this position by spending money on depreciating assets!

Most housing investors are typically asset rich and cashflow poor unless they've been in the game for 20+ years

Yvil

You’re right again

Asset rich cash poor

Working a job

We only have a certain amount of time & that’s your most valuable asset Time

The millennials understand this best & seek experiences over assets like cars

Enlightenment

NL: "Yvil, You’re right again"

You're quickly becoming my new best friend. LOL

Sorry, how is a new home buyer entering the market not doing the same thing; presumably they are freeing up rental accomodation somewhere else.

Also, the reality of being a FHB is that you're trying to get it over the line before you go from two incomes to one and start a family. That's not something you can put off forever. These are real world consequences for people of a housing system that prioritises investors over people actually trying to get on with their lives.

Hi GV 27

". . . the reality of being a FHB is that you're trying to get it over the line before you go from two incomes to one and start a family. That's not something you can put off forever."

I agree with the above sentiment. I have posted many times that FHB need to look to get into home ownership asap and not put their life on hold in anticipation that the property market may or may not experience a correction. (I have also posted how any correction is irrelevant to a long term home buyer as it is a long term commitment and in fact if looking to sell and trade-up then a correction can be a good thing as the price differential will be less!).

I understand your frustrations but your comment "a housing system that prioritises investors over people actually trying to get on with their lives" is clearly not correct. In fact it is the opposite is true - the system favours home owners including FHBs with lower LVRs compared to those for property investors, plus KiiwBuild as part of the system also clearly favours FHBs.

Corrections are pretty relevant if it you get laid off. Given how much of our national balance sheet is tied up in housing and mortgages, the spread of a contagion to employment is a valid concern.

Also, LVRs being a singularly thing that works in favour of FHB on paper ignores the massive untaxed gains that investors have built up on and can realise in a market with a large shortage and continued high immigration. So yes, while investors may have to deal with LVRs higher than FHB, FHBs by definition do not have existing portfolios of homes that they can take realise gains in to take advantage of better opportunities as they come up.

As for Kiwibuild: Again, housing shortage, and Kiwibuild has delivered, what, barely 20 homes? We're undersupplied by tens of thousands. It's also not adding new housing stock on top of what was already planned as things stand, just buying out developers, and even then that's taking FHBs out of the rental market and freeing them up for someone else (to your original point). In eight years maybe, but the economic cycle may well have come to a halt by then anyway.

And again, you ignore a decade of untaxed capital gains, mortgage interest deductibility/negative gearing etc that FHBs do not have open to them. We preserve these at the expense our children and grandchildren, and investors and lawmakers need to accept they bear responsibility for this.

Most property investors have 1 investment property, they leverage equity in the family home to buy a rental for retirement, and the first rental is always easiest to fund as by banks conservative measures unless you're getting a net 10% yield then each rental negatively effects cashflow from banks perspective so eats into salary and eventually you'll fall short of their servicability calculations after 1 or 2 rentals.

I think lowering to 30% will see a big portion of mum and dad investors being able to buy that first investment property, yielding something average, but fairly safe provided they maintain their day jobs.

take a look at the Orr video

https://www.rbnz.govt.nz/financial-stability/financial-stability-report…

the market is in the hands of borrowers / those who wish to be borrowers "stepping up"

see also the dependence on jobs/incomes being made.

Bernard's question also seemed to have them searching for a diplomatic answer - regional house prices taking off since January this year after investor and fhb LVR loosening - same measures again happening next month - know palmy later 2017 had growth rate tapering down, falling to 8% year on year, now back up around 13% and climbing every month, 150 odd sales October is big (180 listings on tm nearly up on the 170 during winter, no one sells today when they know it will be worth so much more tomorrow) - 24 days to sell, fastest around.

Add the extra loosening palmy is truly off to the races -

Deputy governor agreeing last loosening had positive effect on regional markets, and next months loosening will likely do so too - but that's not what they're watching or concerned about, as overall, thanks to as Auckland and Chch flat lining, the growth in credit and nz prices overall is what they watch and they seem happy enough with that (given nz banks can handle stress tests of very large magnitudes, and new lending is prudent eg servicability considerations which are now toughest in recent memory)

Simon: "the first rental is always easiest to fund as by banks conservative measures unless you're getting a net 10% yield then each rental negatively effects cashflow from banks perspective so eats into salary and eventually you'll fall short of their servicability calculations after 1 or 2 rentals"

??? can you explain that statement?

Seems pretty clear to me.

Banks policy varies between banks, but general they take a % of rent income only eg 75%. They then use something like 7.5% as an assumed interest rate.

So a 300k investment all borrowed against existing equity returning 440 a week (4 bed PN for eg) might actually be putting money in your pocket each week after interest, rates, insurance, maintenance - but once the banks run there assumptions over it they'll have you well into the negative.

440 a week = 22880

2500 rates, 1k insurance, 1k maintenance, 300k @ 4% = 12k = $16500

6380 profit, $122.69 profit per week.

BUT: banks think that for 3 months, a quarter of the year, all your rentals are vacant!

So 22880 rent becomes $17160.

AND interest expense becomes 300k @ 7.5% = $22500, $27000 with rates, insurance, maintenance.

Loss of 9840, or 189.23 per week imaginary loss as far as bank is concerned.

And that's on a gross yield of 7.6% which would be considered high these days.

Agreed with your maths but why do you say the 1st rental is the easiest to fund, your maths (bank criteria) apply to every rental, 1st, 2nd or 10th

Most start with a job/salary ; every rental you buy yielding under 10% eats into this... generally an average salary can easily support 1 investment; maybe 3 or 4, but unless they yield 10% or more you'll soon run out of cashflow in thur banks eyes

My point is , buying decent 7% yielding rentals, the banks view them as about 10k a year cashflow negative. So you earn 80k , have a family, net 30k cashflow positive after running thr household, you buy 3 rentals at 7% and you've exhausted your cashflow in the eyes of the banks - so yes , the 4th 5th .... 10th are now not happening until debt is paid down or income is increased significantly

More seasoned investors are likely well over 35% equity across the board anyway and like bigger yields or great development opportunities - I don't see this having much of an impact on them unless they're earning a lot (well clear of servicability limits) and are wanting to buy a dozen more rentals fast in which case recycling equity has just become easier for this strategy

well seasoned developers/projects are done "no-money down"

bank funds the lot

any equity money is pulled out pre construction.

I think you crossing the beams

getting mixed up between a developer and an investor

- you can also speculate in development sites and investment properties (surprise renter).

At around 40 min in 'future of housing market in the hands of those wanting to step up and borrow' - in NZ, first home buyers and mum and dad investors guaranteed to be stepping up and will keep stepping up while banks allow.

20 min in interesting question around investor v owner occupier relative risk. Really no evidence in NZ for this and if you look hard enough overseas ofcourse you will find some evidence to support this.

And Australia markets being over built being different to NZ and not considered to flow through to nz market.

Its defitely a different landscape thanks to the changes from this govt. If bulk appartment come online in good transport locations many will move into them for better security and amenity. One look at the cranes tells you they are coming.

Finance rates in the next ten years will really dictate outcomes on the buy and hold for speculation crowd. If rate do end up rising thwre is no blood left in the rental stone to be squeezed. The only thing I am sure of is that that out come will be driven by offshore events, not which party is driving the bus in NZ.

Most investors who have been in the industry for awhile will be considered wealthy in terms of asset position.

It depends on where your rental properties are and you debt loading.

Providing you have bought well and are positively geared then yes they will be extremely comfortable.

Most seasoned investors are probably not bothering to buy any at the moment due to the hassles that this coalition are causing and the Banks lending servicing criteria.

Personally we are asset rich and cashflow great and we are still able to borrow more due to the personal factor.

However for most there is a problem with the servicing as the Banks are doing their servicing with a ridiculous interest rate of over 7%.

Indeed. Some have. Many have not.

Yes if you have rentals in Auckland and Queenstown and have been in them for a while you have done well. If you have rentals in poor areas such as Christchurch you made a bad decision and have done yourselves and your family a disservice. Not all property investors are smart.

Not really gordon, I used to live in Chch and immediately after the EQ I took a chance by buying written off houses for land value (where the owner had been paid out by their insurance for the building). At the time it was a bit of a gamble as I didn't know if I would have to demolish these houses but I thought, with the shortage of houses there was a fair chance the council wouldn't request that. Then, over time "as is" houses became very popular and I ended up doing really well out of them (I sold out 2 years ago)

Yvil, peanuts compared with capital gains in Auckland. Maybe a great percentage increase but peanuts compared to hundreds of thousands in Auckland.

Hey Gordon, I like your style, only gains of hundreds of 000s (and millions) will do.

Well gordon, I do live in Auckland now and yes, the capital gains have been insane 2012 - 2016 but personally I do not count on average price appreciation to make money (it is of course a great bonus). I look at an area that I like, get to know it really well and I look at properties until I find one where I can extract an immediate 20% value, if I can't I just keep looking.

As an example I bought an EQ damaged house (perfectly livable) at 123 Upper Sumnervale Dr in Sumner for land value of $189k in 2011, the owners had been paid out for the building and they just wanted to leave Chch asap), I rented it out for $500 pw = yield of 13.7% and sold it in 2016 for $400k.

Good cashflow Yvil, we haven't ever invested in chch but have had similar high yield props which helped us build a portfolio. Then it's not just the capital gain on the one property but those that followed as well.

The property market has been "constructed" as a a framework where "nobody loses" (the punters, the banks, and the govt). The current framework appears to be reaching (or reached) the end of its use-by date and there has to be "added incentives" and / or tweaks to the system to enable floods of money to ensure that it continues on a path of price growth. Somehow the "spin offs" of the bubble economy are not really anywhere to be seen. The consumer economy is largely flat to falling; unemployment is low but so is wage growth; and the vast maojority of h'holds are living paycheck to paycheck, including both low or high income.

Investors probably need to think how sustianable it all is and whether or not they can manage the associated risks as the "bubble" grows larger and larger.

We all lose. Our national surplus goes out the country to the owners of the debt farming banks. In a better functioning economy it would flow into the pockets of those who are best able to allocate our resources in a productive manner. The current system makes property speculation look like productive investment. It is a form of monopoly capitalism that enriches the banks, the politicians, bureaucrats and property speculators. We are a deluded nation.

Interesting all. Thank you. I learn a lot reading the posts.

We've got 2 freehold properties, one we live in the other is for a family member. No 2 house returns nothing as they pay nothing. Let's call it an early inheritance, although we still have good cash flow through the small business we've created/had for over 20 years now.

Looking forward I'm more nervous about CGT than I am about house prices & I wonder whether it's a factor in other's thinking going forward. Not much of it mentioned above.

The cost of building a house is daylight robbery, from land development right through council & building to finishing. The building industry needs more bigger players, more choices & more creative ideas about how to halve the cost. If KB does anything I hope it is this. Lowering the build costs is a biggie. It could boil down to concrete, steel & glass with the glass being in the roof for light (no need for windows & better security). The less wood the better (that'll also help with potential fire damage). The other option not really considered much is caves. Create cave houses below ground level on selected semi-elevated sites so the water doesn't run in. Although you could create natural water falls internally for features & other uses.

I hope we could muster some building/consenting/migration reform before we have to completely revert to hobbitry.

This is not exactly slow motion anymore.

In Greater Sydney, Australia’s largest housing market, the housing bust, after a terrific housing bubble, is gaining momentum. In November, according to the CoreLogic Daily Home Value Index:

Prices of single-family houses dropped 9.2% year-over-year.

Prices of “units” (condos) fell 5.5%;

Prices of all types of dwellings combined fell 8.1%;

The overall index for Sydney, after dropping 1.4% from the end of October to the end of November, is now down 9.0% from its peak in September last year"

https://wolfstreet.com/2018/12/01/update-on-property-price-declines-syd…

The article above discusses the RBNZ's LVR limits and its potential consequence on NZ lending, not the value of house prices overseas.

thats odd, look on right margin for this heading.

Update on the Housing Bust in Sydney & Melbourne, Australia

https://wolfstreet.com/2018/12/01/update-on-property-price-declines-syd…

Thanks Andrew, is it just below that one?

Perhaps lax lending standards had more to do with the housing bubble than I thought, now banks are tightening standards prices are falling.

"During the course of the 1980s three major 'anomalies' were observed in a number of countries, including in Japan, which threw doubt on the traditional macroeconomic models: 1. The apparent velocity decline in the quantity equation and the resulting instability of the money demand function; 2. unusually fast rises in asset prices that often came to be referred to as speculative bubbles and which could not be explained by standard asset pricing models; and 3. capital exports from Japan, which reached historic proportions in the mid-1980s, but collapsed in the early 1990s, and which could not be explained by traditional models. In this article I present a simple model that encompasses the standard theory as a special case and which simultaneously can account for the above three 'anomalies'. It is based on a 'quantity equation' of credit creation, which is disaggregated into credit for 'financial circulation' and credit for the 'real circulation'. It is shown that excessive credit creation for financial circulation is responsible for all three 'anomalies'. The model is supported in empirical tests using the general to specific econometric methodology and using Japanese data. The article concludes with a discussion of the implications of these findings for monetary theory, future research and economic policy.

You're correct, Yvil.

But there are plenty here who will seize any opportunity to preach doom and gloom......

TTP

Gordon, you really haven’t put much thought into too much that you write!

No we haven’t purchased property in Auckland.

We have found that we are able to get far better yields from property that is far more affordable than Auckland and enables us to leverage totally without ever putting a cent in.

Our returns average around the 9 to,10% on purchase prices.

As for capital gain on paper, I consider making many millions as being not too bad, when the only money we put in was a few thousand initially.

The Boy you are just an old grumpy boomer who got lucky with timing and inflation. Nothing special or spectacular. That is of course if what you say about yourself is true.

As for capital gains on paper, I consider making many millions as being not too bad, when the only money we put in was a few thousand initially.

Especially tax-free, while hardworking Kiwis making wages pay for the infrastructure and services society provides around them, which produce those capital gains.

A jolly good lark indeed.

That's how a productive economy works isn't it Rick? One part of society does abolutely nothing and expects to make millions?

Interesting that there is no mention in this article of the upcoming changes to the HHGA and RTA as potential contributors to the reduction in borrowing.

from across the ditch

"Sydney property values have now fallen 9.5 per cent since they peaked in July last year and will likely surpass the largest downturn on record, according to CoreLogic's head of research Tim Lawless.

The slide in prices accelerated in November, with national dwelling values falling 0.7 per cent, the weakest monthly result since the global financial crisis, led by a 1.4 per cent decline in Sydney and a 1 per cent drop in Melbourne, CoreLogic's latest home value index showed.

"For Sydney, 1.4 per cent is the biggest monthly fall we've seen so far this downturn. The last time we saw a bigger monthly fall was back in 2004 but that was only one month and otherwise you'd have to go back to 1989 to see values falling faster than this," Mr Lawless said.

"If you look at Sydney's largest downturn on record it was 9.6 per cent during the recession between 1989 and 1991. It's likely Sydney will set a new record in terms of the magnitude of price decline and the length of decline," Mr Lawless said."

Interesting re The Economist of 10th Nov, which shows Auckland house prices as 73.8% overvalued relative to income that could be derived thru rents. So the economic incentive isn't there, unless you factor in favourable tax treatment etc. It is one of the most over-valued in the OECD, compare the ratio of Sydney 47% over, and London 61% over.

I think that the Reserve Bank has actually done all it could, the problem has lain with governments, especially the previous one (tho the previous Helen Clark one was supine)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.