By David Hargreaves

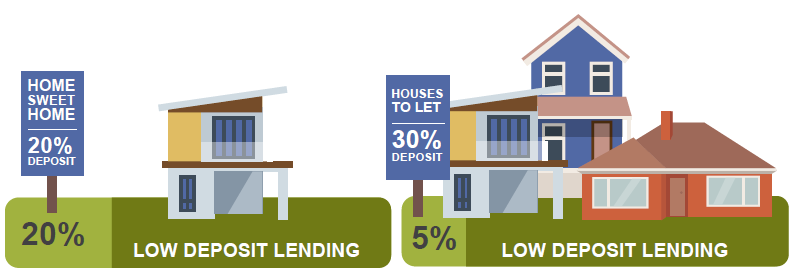

The Reserve Bank has decided to further relax the rules around high loan to value ratio (LVR) housing lending in a highly anticipated move that should provide a boost for the housing market.

The move was announced on Wednesday as part of the bank's latest Financial Stability Report.

From 1 January 2019:

- Up to 20% (increased from 15%) of new mortgage loans to owner occupiers can have deposits of less than 20%.

- Up to 5% of new mortgage loans to property investors can have deposits of less than 30% (lowered from 35%).

This is the second such loosening of the LVRs - which were originally introduced in 2013 - that the RBNZ has implemented. It's pretty much identical to what the central bank did in its FSR in November 2017, which then entailed raising the so-called speed limit for owner-occupier loans from just 10% of new bank lending to 15% from January 1 this year. The investor restrictions were eased from a requirement for 40% deposits to just 35% deposits.

The lending data in subsequent months after the January easing suggested that the relaxation of the rules did have a somewhat stimulatory impact on the market.

The moves to loosen the rules for owner-occupiers will be especially welcomed by first home buyers. However, the decision to also relax the rules for investors - which were a key part in reining in the housing market after they were introduced in 2016 - may be seen as more contentious and risky.

In making the announcement on Wednesday, RBNZ Governor Adrian Orr said risks to New Zealand’s financial system had eased over the past six months (since the last FSR), but vulnerabilities persist. In particular, households remain exposed to financial shocks due to their large mortgage debt burden.

"However, both mortgage credit growth and house price inflation have eased to more sustainable rates, reducing the riskiness of banks’ new housing lending.

"In response, we are easing our loan-to-value ratio (LVR) restrictions on banks’ new mortgage loans. If banks’ lending standards are maintained we expect to further ease LVR restrictions over the next few years."

ASB chief economist Nick Tuffley indicated he was a bit surprised that the RBNZ had also decided to loosen the rules for investors, as well as the owner-occupiers.

"The housing market has been at an interesting juncture recently. Sales turnover and listings rose sharply in October. A beat-the-foreign-owner-ban rush was one probable reason in some parts of the country.

"But mortgage rates have been falling for months, with sub-4% rates now available to borrowers with 20% equity. House price growth has been strong in a number of provinces and been accelerating in some.

"So relaxation of the LVR restrictions is not without some risk, even though Auckland risks are slowly dissipating through a sustained period of flat prices."

ANZ senior economist Liz Kendall said the LVR loosening was "modest".

"We anticipate that this easing will boost the housing market, but only a little, with the restrictions remaining 'tight' overall.

"...We expect that further easing will occur in time, but that the RBNZ will continue to tread cautiously. Household debt and house prices remain high and the risk of resurgence in the housing market cannot be ruled out, given low mortgage rates and still-strong population growth. Any improvement in vulnerability metrics will continue to be a slow grind, short of a fundamental change in market conditions."

This is the RBNZ media release:

Risks to New Zealand’s financial system have eased over the past six months, but vulnerabilities persist. In particular, households remain exposed to financial shocks due to their large mortgage debt burden.

However, both mortgage credit growth and house price inflation have eased to more sustainable rates, reducing the riskiness of banks’ new housing lending. In response, we are easing our loan-to-value ratio (LVR) restrictions on banks’ new mortgage loans. If banks’ lending standards are maintained we expect to further ease LVR restrictions over the next few years.

Debt levels also remain high in the agriculture sector, particularly for dairy farms, implying ongoing financial vulnerability. Balance sheets need to be further strengthened. In the medium-term, an industry response to a variety of climate change-related challenges appears likely, requiring investment.

While domestic risks have eased, global financial vulnerability has risen. Significant build-ups in debt and asset prices, and ongoing geopolitical tensions, overhang financial markets. This vulnerability is highlighted by the current elevated price volatility in equity and debt markets. New Zealand’s exposure to these global risks has reduced somewhat, as New Zealand banks have become less reliant on short-term, and foreign, funding.

The domestic banking system remains sound at present. We are using this period of relative calm to reassess whether the banking system has sufficient capital to weather future extreme shocks. Our preliminary view is that higher capital requirements are necessary, so that the banking system can be sufficiently resilient whilst remaining efficient. We will release a final consultation paper on bank capital requirements in December.

The banking system remains profitable, reflecting banks’ low operating costs and strong asset performance. While positive overall, banks’ low costs have been partly achieved through underinvestment in core IT infrastructure and risk management systems in New Zealand. This was highlighted in our review of bank’s conduct and culture with the Financial Markets Authority. We will be jointly reviewing banks’ responses to our review in March 2019, and following up as required.

CBL Insurance Ltd was placed into full liquidation by the High Court on 12 November. Aside from CBL, the insurance sector as a whole is meeting its minimum capital requirements. However, capital strength has declined and a number of insurers are operating with small buffers. The insurance industry must ensure it has sufficient capital to maintain solvency in all business conditions. Our ongoing review of conduct and culture in the insurance sector with the Financial Markets Authority will illuminate the industry’s risk management capability. The review will be released in January 2019.

167 Comments

"Risks to New Zealand’s financial system have eased over the past six months, but vulnerabilities persist. In particular, households remain exposed to financial shocks due to their large mortgage debt burden."

I know how to lessen the vulnerabilities to the NZ financial system that might come from a financial shock!

Let's increase the large mortgage burden that households are under by letting them borrow more!

Seriously. You couldn't make this stuff up. You have to leave that to the expert at the RBNZ....

Yea it seems to be a genuinely crazy justification, that one.

The only explanation is that they are just so utterly shit scared of house values dropping at all. LVRs are only really binding on the way up, not on the way down so their removal only signals an intention to stoke credit supply.

You're right, and I'm sure they are scared. But fear isn't going to solve the problem and making it worse sure isn't.

Facing the problem is the only longterm solution, and 'hoping' that tinkering with the LVR's will do it, is short-sighted; to put it kindly.

Change IS happening; the boat IS turning, and to change course now because otherwise, we might upset the passengers is delusional.

The contradiction is real. Another way they could bind the market is DTI ratios...

I think the reasoning behind this move is self preservation.

When the custard hits the fan, Mr Orr can hand on heart say "I acted as soon as possible." Rather than get criticised for leaving the restrictions in place longer and copping some blame for causing a crash.

"Self Preservation" is not what Adrian Orr is paid for.

Frankly, I reckon there's merit in your point, but what an indictment on the whole sorry state of affairs.

(Story !: When I was being trained up, I asked my Director "What do you actually do?" (He didn't seem to do much on a daily basis!).

His response was:

" I am here for when things go wrong; to make the hard decisions when they are needed; to be at the head of my troops when they go into battle, even if the chance of success is slim and my demise is probable. And if you do your job well, I will never need to do mine!")

Adrian Orr needs to step up to the plate because one way or another - he IS going to get the blame....

Career risk is all to a salary man.

Maybe Orr was reading all your comments that the housing market is crashing, so he had to act!

Particularly if he has a mortgage.

You really couldn't make it up.

The RBNZ is busy emptying it's clip before the bad guy has even popped his head around the corner.

As mentioned in a recent comment - they had to do it now or they will lose the opportunity. Once the market is falling you can't easily ease the restrictions.

The actual change is pretty minor, but it's the principle of it *face palm*.

Good reserve banking is preemptive not reactive. Would you want them to respond to rapidly rising inflation after the fact? Why is it face palm?

The lobbyists must have invested in some excellent lunches!

I think it's all because of your warnings that the housing market is crashing

WTH?? No actually WT*? Are you kidding me...., Mr. ORR, a lesson to be learned from the GFC , market forces always prevail and more intervention inevitably leads to a greater impetus for a drastic fall. Just look at Alan Greenspan's legacy. Today is a sad day for the uninformed consumer.

Man I can hear all the DGM heads exploding here. I also keep hearing "lessons to be learned from GFC", the lesson here is they are going to keep bailing out companies, keep the interest rates relatively low and keep the printing presses going. There is no "market" anymore. No matter how much you "wish" they did something to your advantage to crash/burn everything they won't, even though it may be the right thing to do.

No doubt you DGMs are all for capital gains tax as well? Do you realise the house prices need to appreciate for there to be taxes to pay? With that in mind how likely is the government/central bankers to purposefully crash the market as you've been hoping since 2009 especially with the current level of immigration? Especially if their sole goal is to be reelected?

Does anyone have an email address for anyone at the Reserve Bank? This article and stream of comments should be delivered to as many inboxes at the Reserve Bank as possible!

Immigration still at record highs? Still supply shortages? Definitely the time to bend over backwards for investors.

I will need to re-evaluate whether the next few chapters of life are viable in NZ. It seems people who want to work here and raise families are cannon-fodder for those who think the economy should be rigged so they can make money from property no matter what.

I'm starting to think that this needs to be spelt out to the RBNZ - they clearly have no comprehension of where this all leads.

Here is a very simple acrostic for them to consider...

Many

Over-leveraged

Retards

Are likely to

Leverage up even further now

Has

Adrian Orr stopped to think about the havoc that these

Zombies, who

Are

Recklessly taking on more

Debt, will wreak when the music stops??

I know who they will be expecting to pay for their super and rest home subsidies when it all goes tits up.

This is indicative of the brain drain thats likely to occur. Younger generation realise they're getting taken for a ride buy a bunch of self serving investors. The tide turns on immigration. We keep building, end up in an oversupply situation (does this sound like Ireland a decade ago?)

Couldn’t agree more. I’m 30, living in Auckland with my partner, both have good jobs and with near on $200k savings I could use as a deposit but even with that I don’t see a future here. There just is no upside, the boom has been had and for what? No political decisions have been made for the good of NZ, everything has been based around a certain generation to enrich them at the expense of everyone else (not just the young but pensioners as well). I’m getting pretty fed up but what options are there? The world is now in sync due to central banks colluding and creating a world wide credit cycle. Guess I’ll just be sitting on my hands waiting for the inevitable drop all the while our problems are continually exacerbated.

There we go, that’s my cathartic rant over with for the day.

You could have almost bought our place outright 14 months ago with those savings, put the rest on the credit card. 3 bedroom on 1/4 Acre only a 5 minute walk from the train station with a regular (but kinda shit) commuter rail service taking you into Wellington.

I've been considering moving to welly but I'm sure that there will be price falls in our fairly immediate future so I'll stay earning the big bucks here, living cheaply and saving for the time being just waiting for my chance to escape Auck!

I am shocked. The place is run by and for the Bureaucrat and Politician Party, who are "advised" by the New Zealand Chapter of the Society of International Bankers? Surely not?

Hi Withay, my situation is very similar. Early 30s, a couple of career false-starts and on the back foot in terms of having deposit. I am torn as I have family in Akl/NZ but I am in a position where I simply can't afford to have one of my own as things stand. I don't want to have to leave a city I've lived my entire life in, simply because other people have seen fit to enrich themselves and pull ladders up behind them. Unfortunately the clock is ticking and time may run out for me. I hope these boomers aren't too attached to their grandkids, if their offspring can even afford to have them.

Hi GV 27. Sorry to hear that, it's not an ideal situation. Were holding off starting a family as well for the time being. Forgetting Auckland being your home and for what its worth, working in Melbourne was what put me ahead. Housing is cheaper than Auckland (and getting cheaper) and typically you will get paid more with a lower cost of living. All up, I feel your pain though.

Good to know its not just me on here. 30 with a partner, good deposit and jobs in Hamilton. Don't want to be a debt slave for the rest of my life on a home that will remove all my flexibility. Going overseas again is an option but really do want to start a family in next few years in NZ.....

...the banksters and rulers don't want you to start a family - much cheaper to import a fully grown unit from India, China, the Islands or the Philippines all ready to go.

Fully educated, compliant, won't join a Union, willing to work all hours at well under gazetted rates ...and happy to share a home with 15 others to pay the property class an exorbitant rent.

The inevitable end game of social democracy

While young Kiwis don't vote enough, and in their own interest.

It's left to the older voters to vote in their own self interest that is unfortunately too often at the expense of young Kiwis.

Who is there to vote for in my own interest, nobody wants to touch how we introduce money into our economy? I vote for the party closest to my ideals but they’re not spot on and unfortunately until the above is sorted we’re just trains on a track with alternating drivers.

We've now had both major parties campaign on means-testing super and then rule it out as soon as they got into power. Who, exactly, do we vote for to protect young people's interests when they're too busy feather their own nests?

First problem is not enough young people vote, such that there's not the motivation in the parties to actually do something about some of these critical issues. Second problem is that there's no other political pressure coming on to parties from young people to do something about these issues.

They don't listen because they don't have to, twice over.

dp

Errrgh, that is a tight deadline medically, although even looking at adoption options these days is pretty limited. I have known many in the FHB 20-30 gen. They faced either having a secure home for a few years, or children. They cannot have both. Along with any unlucky life events completely blowing chances of either. I have seen people who chose either one being absolutely miserable because of the cost of the choice. Yet there have been a few high flyers with good family help to put them in a position with extensive deposit assistance, guarantee and shared buying. But a few trying that now can no longer do so because the banks have already started considering DTI ratios even if the Reserve Bank is too chicken.

I say the same thing, move out of NZ if you have the skills, get the better career experience. Have a home and a family, then consider whether it is worth coming back or whether NZ has degenerated to zombies eating their own flesh just to get by, especially with the ageing population and pushing for increasingly low wage high cost living as well as little to no job security. Find if there has been any family or friends already blazing a trail and see if they can help or provide advice & network connections in their chosen area.

Yes, definitely sit on your hands for now, and keep saving. We are in a bubble and so is Australia, and it will return to closer to average affordability ratios. It might be Australia that does that first, given what is happening with the market there now. Awful to say, but when there are a huge number of mortgagee sales, and people are not buying, that would be a great time to use your $200K or more.

Yes keep saving and making desposits at the banks so that investors can risk your money on the housing market via a banking system with no deposit protection.

If it gets to the point that the banks need a bailout, real estate values will be dropping a great deal, so I don't see buying now as a better option than having cash on the sidelines.

Haha I don’t keep my money in a bank. Mostly for OBR reasons but it’s a nice bonus not making it available for speculation.

banks don't lend your deposit

Correct me if I’m wrong but it goes towards their reserve requirement which allows them to lend more.

That certainly has got me curious about where it's kept but I won't ask. I'm thinking cryptos (down about 80% for the year), non-bank deposit box (cash and gold), or buried somewhere...

Just wait for when the boomers start running out of money to fund their winter cruises around the med and they'll all start selling up their rentals at the same time, while they move into a retirement village and sell their own home. Suddenly there will be houses everywhere and nobody wanting to buy them because they're dropping in price.

You wouldn't remember but in the early 2000s Ian Wishart was on talkback and said the same thing about boomers selling their family homes will cause a glut. I like Ian, hes generally quite smart, not that time, he could not have been more wrong, since then there has been two major property booms and still strong.

Dp

Did he give a timeline when he made that statement of when Boomers would start selling their homes? Maybe he was making a long term prediction? If it does happen in the next couple of years does that make him wrong for calling it 20 years early?

Houseworks - you could be too fast jumping to conclusions. Give it 5-10 years as he might be right. Time will tell...Boomers don't need to sell yet, but wait til they're 70+ and the section starts getting too big and they need to downsize or their partner dies and they move into a retirement village...just at the same time as we get organised with high density housing and the younger generation get so pissed old with the cost of getting established in NZ so they leave in droves overseas (all possible). Could be the perfect storm...again time will tell..

I'm 32, live overseas and was planning on moving back in the near future. Now, however, I feel the same way as you; NZ does not seem like a good place for young families like us to set-up shop. We have enough now to buy a home in Dunedin, where I am from, but It just feels like such bad value. Our life savings gone for a damp old house in a place with little job opportunities. Looks like we will be putting aside our move back indefinitely at the moment.

Whoa, watch out about Dunedin most the houses coming on line have MASSIVE flooding & landslide risks and the DCC and insurance companies are washing their hands of the whole area. Do not go into Dunedin blind it will be a bloodbath, even those trying to offload dodgy properties in the past year outside but near marked flooding zones have flood damage and the communities will be brutally cut off. Not to mention the massive infrastructure debt of Aurora being cut like a pound of flesh from ratepayers. Oh and as a bonus the DCC is raising rates 50% over 10 years. Not for the faint hearted, or low equity FHB. The cheap house flips have been shockingly dodgy but buyers often only get 1-2 weeks to even see the properties & get all reports before it goes in a deadline sale. I.E. purchasers going in practically blind. Find a less flood prone area with a less incompetent council.

Well this is good news isn't it? Economically everything is hunky dory just as I suspected. Things like dividends, profits, inflation and progress are not just chimeras like many on this site are wont to believe.

The changes announced today are marginal and won't change overall trends.

But it's the signal that the RBNZ can and will run this bubble until it and economy dies is concerning.

Take a close look at Australia's current trajectory and it will make sense.

It will stall or flatten the trend for longer. And this is what the RBNZ wants. They are sacrificing the FHBers of 2018/2019 so everyone that got a foot in earlier has a more capital buffer.

Kicking the can down the road to save the majority but screw over the few.... Problem is if house prices do start falling and less people start buying then this move matters nothing because lack of demand will win.

The quesiton we need to explore here is what does the self licking icecream cone do when there is no more icecream?

Zachary, defiance and denial won't make the approaching sh-t storm go away.

Oh wow. When there's a slightest hint of a credit slowdown - 'we need more debt'. Gotta love Keynesian Economics.

Question is, at what point will the Keynesian’s realise their system doesn’t work? Or will we get the whole “that wasn’t really Keynesianism as we didn’t print enough etc...”

At no point.

Correct, as the system is still working

thank you for that expression of faith.

Really? To what ends?

"Canada, the most affluent of countries, operates on a depletion economy which leaves destruction in its wake. Your people are driven by a terrible sense of deficiency. When the last tree is cut, the last fish is caught, and the last river is polluted; when to breathe the air is sickening, you will realize, too late, that wealth is not in bank accounts and that you can’t eat money." - Alanis Obomsawin.

How far down this road are we already?

We already have a perfectly good system that provides all our needs and only through our own insanity do we choose not to see it.

30% deposit for investors = 17% increase in borrowing capacity compared to 35% deposit.

Places already popular with investors (where investors maybe the marginal buyer/ price setter) such as PN at present have just been re-valued 17% higher across the lower valued investor friendly stock. Cheers rbnz

To be fair investors should make decisions based on the risk like any other business.

Who cares if investors get into deep water or fail, that's what separates the shrewd from the muppets

Well said and if an investor fails, don't bail him/her out.

Actually, come to think of it, same applies to a business owner, an employee, a wife, husband, a friend etc...

When markets turn into a frenzy emotion takes over - Spent time in share market? Dow worth 25k? (was 14k in 07 before the gfc). Humans are serial extrapolators as some dude on CNBC said referring to trend following in stocks-- property is the same but on steroids as the average 'investor' wouldn't know what CNBC is but they do know that horrible feeling of hearing prices rise 10s of thous every few months and all want a piece of the pie.

They go to the bank - get a max loan level - and see it as a target - spending right up to their limits. Servicability limits for salary earners kicks in only after the first 1 or 2 IPs , and the bank will let them know what rental appraisal is required - 10% yields if you want to do a G Fowler and buy 20 in a year, otherwise the thousands of mum and dad investors will get by picking up 1 or 2 at 5% yield, and likely make good money if they simply hold long term

The PMR 'investors' sound pretty retarded, to me.

"Yes! I can now pay 17% more for a property that has fixed yield growth and is cashflow negative at the trough of the interest rate cycle."

Sorry, I just need to decipher your usual serving of word salad.

What is PMR? Palmerston North?

What property are you claiming is going to cost 17% more all of a sudden? Palmerston North? Have you thought that claim through?

What is "fixed yield growth"? Yield that is fixed (for what reason is anyone's guess) yet growing at the same time...

Hahahahaha, he got the retarded bit right!

Can you answer any of my questions above?

No surprise!

The banks have been lobbying for this and of course, the best interests of individuals, families and investors is at the heart of the decision! NOT!!!

I really dont feel its too bad for the rest of NZ but in Auckland there are many that are slaves to their mortgage already, so why not add a few more.....

No one is forcing anyone to take on more debt, that decision is up to each person, if someone wants to be reckless then fails, too bad for them. I like freedom of choice and self responsibility vs nanny state.

Two key statements in your article to take from this:

1. "highly anticipated move that should provide a boost for the housing market"

RBNZ now have a very specific tool (not just OCR which has other consequences) to influence the housing market. RBNZ has a desire to ensure stability in the housing market for economic stability reasons. While some fall in houses may be acceptable for the RBNZ, they will not wanting to be seeing this to be of any significance impacting on the wider economy.

2. "vulnerabilities persist. In particular, households remain exposed to financial shocks due to their large mortgage debt burden"

For those with high mortgages including FHB, the explicit message is that there is a risk, and now is the time to be paying the mortgage down while interest rates remain low.

Just because the Australian housing market is in fall mode, this is unlikely to simply just transfer onto NZ as our historically high immigration rate and historically continuing low interest rates create some on-going demand - and it also seems that lending by our banks (despite their Aussie connections) has been a little more prudent in their lending.

Along with RBNZ statement one should note that RBNZ would likely be tightening LVRs if there was any sign of unsustainable increase in the housing market which would lead to increased risk to economic stability. So days of reliance on significant capital gains should not now be entering property investors' assumptions for buying additional rental properties - if it isn't cash flow positive now, then with a medium term outlook (three years?) for increasing interest rates, then it is unlikely to become cash flow positive and there will not be the capital gain to off-set this.

Thanks printer8. Informative post.

Just because the Australian housing market is in fall mode, this is unlikely to simply just transfer onto NZ as our historically high immigration rate and historically continuing low interest rates create some on-going demand

This is not our first time to the Rodeo, it is not the falling of an Aussie market that hits NZ. It is recovery in the Aussie market, because then we tend to see large scale migration from NZ to Aussie. We may go from high inward to high outward immigration very quickly.

I agree with you totally uc

Immigration could change quite quickly and we could see increased interest rates sooner than expected due to an offshore event. Either or both of these would have an impact on the housing market.

Personally - if I was a FHB I would accept the stays quo (stable house market and interest rates) and take the window to get in, buy a house, but look to pay down the mortgage. A degree of uncertainty as to what will happen and to when; however I wouldn't be putting my life on hold to wait and see for which there may be no advantage and possibly some downside with interest rates rising and housing moving up by a couple of percent. Would I be waiting hoping for further fall in interest rates - well it is both highly unlikely and even if banks try to squeeze rates down slightly it wont be significant and probably at most by a half percent or so which is not going to be that significant in the bigger picture - I would take current rates while they last.

Rent and wages are on the rise .... it doesn't take a rocket scientist to know what way property prices will be heading ... eat your heart out doomers

Wonderful. More debt, less chance of FHB entering the market to have a stable roof over their heads and you celebrate this? How utterly selfish are those that wish for a future which would further increase inequality and further marginalise the youth of this country.

Yes, as those are the only two factors...

As long as they do not buy in Auckland or Queenstown, then yes now is a good time to buy. Auckland and Queenstown are over juiced currently.

Thank you printer8 for actually writing an intelligent post !

Thanks for your feed back ks and Yvil.

While we are talking of FHB, one hears a lot of talk about potential drop in the housing market. Of course that is a possible but one needs to really get their head around the implications of a drop whether it be 5% or 15%.

The future of the property market and potential fall in property values is extremely, extremely important to investors. A 15% drop in values will be on the value of the property, and if one has 40% equity, that equity will not drop by 15% but rather by 37.5%. (Think about it!)

However, for homeowners such fears are not that important and may be an advantage.

Why?

Buying a home is not a short term investment, rather it is an investment for one's life time. Yes, you are not going to keep the same house, you are most likely going to sell and buy a number of times as you either trade up or migrate.

If you are able to service the mortgage with either an increase in mortgage rates and/or a fall in house values, then the bank is most likely not going to "foreclose on you". The NZ banks aren't stupid; they are not going to lend to you if they think there is going to be a problem with either of these happening - they don't want the hassle and also risk losing money themselves. They are probably more astute about the future of the housing market and interest rates than you and I. So take a mortgage approval as a pretty good sign that the bank doesn't think that you are going to have a problem considering either a down turn in the property market or an increase in interest rates. (The experience of foreclosures in the USA housing market back in 2005(?) was due to circumstances quite different to NZ - unregulated US banks lent recklessly and considerable money to those who really couldn't afford it and on-sold those risky mortgages as sub-prime mortgages. It was not unsurprising that many lost their homes when interest rates increased leading to a collapse in house prices. Such a scenario is unlikely in NZ as our banks are highly regulated as demonstrated by the RBNZ shift in LVRs today.)

Remember, even if prices do drop - you have the same house and owe the same amount of money. In the longer term house prices are most likely recover.

In fact for any homeowner in for the long term, a fall in house prices could be be a great thing! Why? Well if you are trading up, the price you get for your property is far less important than the differential between your house and the one you want. In a market that is down - well that price differential is likely to be considerably less.

Bottom line. If you are a FHB, you are not going to be a property investor but a home owner. You will not become a property investor until you buy a second home purposely as as an investment producing a financial return. Think about both what this means and the implications of it.

Looks like we have ourselves our very own Plunge Protection Team....

When I bought my house those rules were extremely painful and essentially required me to put down 20% due to the imbalances on the bank's books. I could understand changing the percentage for new home buyers but I don't get investors being included. By putting investors in the change that just keeps house prices unnecessarily high.

Is the RBNZ the plunge protection team for house prices? Yes they definitely are. Who is to blame for continued high house prices? RBNZ.

It's entirely possible the RBNZ is already a long way behind the curve.

These changes come into effect on January 1, so the absolute earliest they could look at further easing the LVRs without looking like they are panicking is probably mid-2019 (allowing for an announcement in the first quarter and a lead time before implementation).

The problem for the credit addicted RBNZ is that once a negative feedback loop in prices develops it can be hard to stop, especially when interest rates are already very low.

This is exactly where the RBA is currently. They have been signalling rate hikes for so long, that by the time they slow down, engage neutral, and then find reverse (without looking like a stunt driver), the downward contraction already has a lot of momentum.

Adrian Orr knows what he is doing. Safe hands and a good track record.

BLSH, its battle stations in preparation for what lies ahead. If your market is so strong (stable-flat), why are they opening the taps now then?

The RBNZ are worried as hell.

They aren't "opening the taps" in my opinion. This is just a minor, well-signaled easing off of the restrictions. This is a perfect time to do so given that the Auckland market is flat and the restrictions were always supposed to be temporary.

I certainly don't think RBNZ are "worried as hell". To the contrary, I'd say Orr is cool as a cucumber at the moment - inflation close enough to sweet spot, economy ticking along well enough, housing market steady. There will always be global risks, but that's just par for the course

"Battle stations in preparation for what lies ahead" Classic RP

Classic BLSH denial. May 24th, 2018, "RBNZ says possibility of needing unconventional monetary policy tools 'higher than it ever was in history' meaning it needs to be ready just in case"

Since the media release in May, please factually outline how global risk has reduced? BTW, have you read the "Great Reset" series by John Maulden?

https://www.interest.co.nz/news/93891/rbnz-says-possibility-needing-unc…

The possibility of needing unconventional monetary policy tools is certainly higher than in the past. Good thing plenty of alternative tools exist https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Bulleti…

Global risk hasn't notably reduced since May. You just way overestimate NZ's exposure to risks in Australia, US and China. As a small market economy NZ absolutely will be affected if these global risks come to fruition . But you act like a downturn in China (or Aus or US) will affect NZ ten times worse than China itself. Simply nonsense. Now for Christ sake please don't go saying that I think that NZ has no exposure to global risk, because that's not what I think at all.

BLSH, pleased us DGM's are getting the message through. Sensationalizing my comments by implying that I forecast NZ will be worse off is a tad desperate. With NZ house prices amongst the most expensive in the world, it won't matter what immigration numbers or interest rate arguments you throw at it, if there's a shock, it will all implode. So many jobs ride on this property boom, it will be a self fulfilling spiral. As of late you've certainly begun acknowledging the risks that are in plain sight. You've not had a choice. Now, it's just your insight that needs work. Papamoa prices will fall too. Have you seen how hard it is to sell a house on the North Shore lately?

BLSH, the RBNZ might have plenty of tools. It's a worry the same can't be said for countries much larger and globally weighted than us.

Good thing we aren't in those countries then ay...

...to which we trade with and greatly depend upon for earnings and employment.

Not enough for NZ's economy to "implode"

hopefully not. In such times, many unemployed will think it has. NZ house prices (including yours and mine) would certainly implode.

Na

Oh-ok, only mine and Nic's then :)

Hahaha

I don't sell houses, so wouldn't know.

Smart man. There isn't a single house or commercial building I sold in the last 20 years that is not worth more (generally significantly more) now than when I sold it, no matter how well I thought I did at the time.

Sounds like you did well out of those sales, so good on you, and no doubt used the returns to invest in other profitable assets/ventures!

The "plunge protection" squad armed and ready.

....so let me get this one right .....the general populace is up to the eyeballs in mortgage debt ....but those precious aussie 'big 4' banks need to keep those profits rolling in for their shareholders......property prices have either flatlined or reduced for whatever reason ....whhoahh !! that wasn't meant to be in the mix ....the punters will shy away from property as an investment ! ......and not take on anymore mortgage DEBT ! .....NO MORE mortgages for the banks profits .....HELP !!! cry out the 'big 4' to the reserve bank.....what can we do to help your Master ? ...... 'big 4' yells "reduce those LVR's" ! ......aaaaarrrh sigh the 'big 4' our mortgage books will get back on their upward track.....and the most important thing, the 'big 4' are much happier - true bliss......meanwhile at the coal face, the "property ponzi party" MUST continue .....at "all" costs ...... but at what 'cost' ? .....all I can hope for is that the NZ taxpayer does not "bail out" anyone .......including the 'big 4' .....talk about putting more fuel on the fire !

A lot of people think mortgage debt has been going through the roof - but they are wrong.

Household debt as a percentage of GDP hasn't really changed significantly since 2006 when it hit 90% of GDP. What has happened in that time is that interest rates have halved. So that fairly constant mortgage debt is costing us a lot less than it used to, in fact interest charges are nearing lowest they have been in a generation.

https://d3n8a8pro7vhmx.cloudfront.net/garethmorgan/pages/675/attachment…

{kind=link}

dp

Why do you think John Key went to work for ANZ, it is a revolving door and he served the Aus bank profits and foreign speculators so well.

Come on guys its really simple, we have to keep the status quo and everything keeps on ticking along as it has done for the last 10 years. Everything possible will be done to keep the housing market afloat and your just going to have to live with it.

There is a level of desperation that's showing in the RBNZ. There are plenty of people hitting retirement age, and giving the low interest rates they've poured their money into property. Now that many will want to downsize or sell off rentals the property prices are in danger. Of course this move entirely favours retirees over those hoping to buy a home for their family.

Essentially if you aren't near or at retirement age the RBNZ is telling you to get f'd.

We need to look after our old folk.

ZS it needs to be balanced rather than the one sided situation that exists. If interest rates were higher then house prices would be lower. We would have also seen less retirees moving away from term deposits but here we are.

Somebody has to fund the boomers retirement. May as well get the younger generation to take on heaps of debt to buy their rentals and fleece them via taxes as well to pay their super.

You aren't that young IO to be the 'younger generation' and btw you have to pay tax to jacinda and co for all their grand schemes ... cycle tracks and bikes riding lessons in school just one of the loopy left wonderful ideas

In our day we actually learnt to ride a bike all by ourselves instead of cost the taxpayer tens of millions.

Pay tax unless I have negatively geared property?

Oh and have I disclosed my age? You'll be aware I"m not a boomer but also haven't disclosed if I'm 20, 30, 40 or more....

You haven't disclosed that precisely but "reading between the lines" you are probably a lot older than what you seem by your naive comments

From the banking industry to the RBNZ:

(cue music)

"I can fly higher than an eagle...... because you are the wind beneath my wings"

I remember not that long ago a bank (think it was ANZ) TV commercial The theme music was Bittersweet Symphony by The Verve. Second line of the song is "Tryna make ends meet, you're a slave to money then you die"

On the 10th day of christmas, my reserve bank got me a ........ a judas goat !!!!!!!

Nic Johnson - That link on the Federal Reserve is the best one I have seen so far. Well worth the watch !

https://www.youtube.com/watch?v=lu_VqX6J93k&t=1614s

A massive message from the RB that we are in the shyyyyyyyyt. That's my read...but watch msm beat it up as great news...lets go shopping!!

Nope just positive news from the RB and a signal to go out spending. Just a coincidence its RIGHT before Christmas ? I guess we will see how many people open their wallets this year, Eftpos transactions and total spend it always very interesting as it shows an accurate picture of how people perceive the economy.

Aren't the tightened bank lending criteria over debt servicability calculations using verified household expenses, and stress test interest rates the more constraining criteria over credit growth for the banks?

The lower LVR will help those that have more than adequate debt servicing capacity? i.e those on high household incomes.

This guy over at Property Talk will be stoked with the announcement, hopefully the bank agrees with him and makes his dream come true. He wants to take the plunge and recycle the equity in his Home up to an 80% LVR so he can purchase an investment property.

Sounds like he's been spending too much time lurking in the PT forums and not enough time on this site.

Current House value - $735k

Current Mortgage Balance - $465k

Figure 2.2 of the FSR shows that 50% of lending is at LVRs greater than 80%, and/or DTIs greater than 5. This is hardly constrained responsible lending.

Perri,

Not sure where you are getting that 50% number.

Just looking at Fig 2.2 of FSR (as of new lending in the 12 months to September 2018)

1) lending greater than 80% LVR is 9% (last column)

2) lending greater than DTI of 6x is 25% (top row)

3) lending greater than DTI of 5x is 43% (top 2 rows)

Edit:

I think I see now that you added top 2 rows and the bottom left squares in LVR 80% and above column (totalling 6%) . Added this the total is 49%, and you rounded up to 50%?

Correct post, 0 thumbs up

Incorrect post, 9 thumbs up

Doesn't say much for the readers/commenters

I think the message is that we have been a little complacent and exuberant in the past and things could be a lot worse. We have dodged a bullet. This time instead of gorging on cheap credit work on deleveraging and raising your equity level somewhat. Sell some properties, take less of a profit than you had anticipated. A steady hand is on the tiller and there will be plain sailing for awhile giving everyone time to get their house in order.

By all means buy a property if the figures work out but don't over do it, don't bank on capital gain, rather work on being a proper landlord. And banks need to be sensible too, imposing their own criteria as responsible lenders.

ZS - were you a manager at Enron?

Auckland has insanely high costs to overcome (thanks to Goff Sprawl) and therefore building growth requires either:

1) an increase in debt accrued on purchase. Happening very soon.

2) greater access to foreign capital via increased immigration. Happening later.

3) building cost reductions as promised by Labour prior to the election. Will never happen.

High (p)raise to the bubble.

Looks like this Adrian Orr guy is firmly in the bankers pockets. The cure for too much debt is apparently more debt.

New Zealand is pretty hopeless for the young and the unpropertied.

But the economists told me it's great that central banks are independent from political interference. It must be for the greater good. They must have our best interests at heart.

What was wrong with a flat housing market for a few years so prices could have eventually eased of 9X income?

It is very clear now why RBNZ has been making dovish remarks and keeping the OCR too low.

Ok RBNZ, re light the property market but if it does we will clearly know who was responsible.

The winners are the speculators who have made hundreds of thousands tax free over the last 6 years,

now the savers are the mugs who have to prop this up the stressed home owners.

Unbelievable.

WoW this tells me they see a huge slow down in credit growth fed by the banks and house prices reducing

How will relaxed DTI's support prices if buyers anticipate house price reductions? Lets be honest the DTI's were only there to knee cap locals trying to compete with foreign buyers. I'm guessing boom time for the provinces and Minsky moment time for Auckland.

There are no DTI's in place

LVR's I meant to say

So put this in perspective of the Titanic. Is this lowering the LVR similar to starting the water pump to pump out the water in the hull?

although I fundamentally agree with this move, you would have to question the rbnz independence.

This decision was one made behind closed doors with the banks executives in Orr's pocket. It is also in complete contrast to what is going on across the Tasman. (Although I note that the rba governor came out recently and actually criticized the Royal Commission there, actually stating that the Australian banks "should ne a bit looser with credit"?).

Adrian Orr is looking more and more like a property spruiker, and in cohorts with the sector that he is supposed to control .

"The RBNZ loosens the LVR restrictions"

No surprise there

I want to thank RP, Nic, PP2F and all the other commenters on this site who have helped the RBNZ loosen the LVRs by their relentless claims that the housing market is crashing

Yvil, you're most welcome :) But, who said houses were crashing right now? (link please) Are they crashing in Sydney? Will it follow onto Auckland? Loosening the LVR's in line with much tighter lending conditions coming, is logical and demonstrates vigilance. I personally doubt it will change anything.

Do you still stand by your comment that were riding a slow spiral to another Great Depression? "So be brave and let the great depression happen, it's the purge the whole system needed. It's much better than the long slow downward spiral we're on now, which will still lead to a depression" 04 May 2018 @ 1:36PM

Auckland property prices only follow Sydney on the way up.

This announcement is a Clayton’s one!

Really nothing to write home about, and won’t make it any easier for people to get money at all.

LVR still at 35% for investors as a general rule. If you had a good case then with 30% you would’ve got it thru anyway.

Investors are generally sitting on the sideline in Auckland anyway I would’ve thought and would blame them with this Leftie government that prefers to build State houses for people that contribute bugger all to the country by way of working.

Michael Cullen in regards to the TWG entioned too much inequality in NZ so we should tax the people that have the money more!

What a pathetic thing to say Cullen.

I could say it is something coming from someone past there usedby date, but then Cullen was never useful!

He should be tucked up in bed in a resthome at his age and usefulness and yet this coalition put him in charge of a working group!!!!!

It will be intetesting to see how this plays out, I am seeing it as a nod to the investor class to go forth and subdivide now that the FOB is in effect, there might be a bit more space in the market as a result.

Yes, I know it has all been said but I just need to voice mine-What is AO thinking, oh that's right -he's not.Give me strength has history taught him nothing!

In my humble opinion his decisions do not reflect the general concern of the indebtedness of current mortgage holders. Interest rates are low -what happens in 12 months when China/US economis have dived, Russia invade Ukraine and Italy goes belly up?

There are some very smart people here, however if they had just got into housing and put as much effort into that, instead of being so negative and spending what must be hours dragging up old posts to quote, spending hours on research and posting links and doing worthless math to try and prove their point they would have made a fortune from their effort.

Carlos - I'm going to call you out here and say that's a rediculous opinion and attitude to have. Its like telling somebody to be born earlier.

Yes its the young peoples fault for not being born earlier and now having missed out on the capital gains in the market. Its all their fault, they should have been born earlier.

Anyone who has bought a house as little as 3 or 4 years ago is not regretting it. I think it is pointless that people in their 30's with good jobs and a huge deposit already saved, continue to rant on here about house prices.Its pretty clear from the number of thumbs up to various comments here that there is a disproportionate number of pissed off people that missed the boat that just like to vent here and get support from others that are also still waiting in the dock. Buying a house can be less about the money and more about your mindset and expectations. Its a big jump of faith, been there and done it. Stood on the driveway and we had 10 minutes to put in an offer. Your either in or your out but don't continue to whine about it.

Do you think people might not be pissed off about missing the boat and just don’t want to get on a boat that’s going to run aground.

The majority of capital gains have been due to lowering interest rates and money creation since the 70’s, how much more is there to be had?

Or perhaps you've missed a shift in sentiment across society? i.e. the comments on here are a reflection of that change?

I O I'm sorry but you really, really, really don't get it. Where you are at in your life has nothing to do with when you're born or any other exterior factor, it's got everything to do with what you do, the decisions you make and the actions you take in your own life.

Do you have any care for others, a sense of community?

Actually it has a lot to do with when and who you are born too. If you are born with any disability say you have a 90% of being in poverty, not affording basic medical and housing needs because of reduced job opportunities. No one hiring with a hint of any physical disabilities even if the role is just tech skills. Seriously most cannot even find an employment opportunity at all, literally. Yet it depends highly because some disabilities instead of crippling a person's future from the start creep up late in life like Bill Moss with FSHD. Hence in no way is it the choices they make. The disabled get no choices and in fact many are just lucky to survive long enough to retirement. Now before you start claiming they are a drain on society because who wants skilled smart people who are incredibly loyal to any job they can get, I will just casually put out there that it was your attitude to discriminate in the first place, lay the Nazi reference down to invoke Godwin's law and torpedo the debate on it being non existent choices when house prices are over 25-30 times wages and rising faster than non existent wage growth when even inflation invalidates any wage increase.

Carlos67 - Oh my you said that so so well a thought I often have ! LOL !

I think we are in a new era with the RBNZ, with other tools than just the OCR I think the RB will do a better job.

The LVR's have proved very effective, neither a large drop or rise in house prices are good for the economy so a balanced approach is refreshing. The LVR's could just as easily gone up today if prices were rising to fast.

Maybe the boom/bust cycles are past as normally the OCR has been raising to control house price inflation at the expence of killing the economy !

Carlos67

POST OF THE YEAR

Is it a new rule on this site that if you become over stimulated by confirmation bias that you're allowed to post in capital letters?

Interest.co.nz should try optomising for mobile...

Second that.

I made a comment the other day about the addition of ads making it difficult to browse on a mobile. Each time I would load Interest, just as I am about to click on a link the page would resize and an ad would magically appear under my thumb.

Thanks for getting in touch David, I don't know whether you've done some magic behind the scenes but now the 2 page full screen flash ads are gone. I fully support this site using ads, I'll try make a conscious effort to click on a couple each day.

Another thing on Mobile for some reason the "New" comments flag that you see on a PC has gone. The 'x' New Comments link under the article from the home page does take you to the first new comment which is nice, but any further comments are a bit more tedious to look out for. Maybe I'm just lazy!

Agree, on holiday so only accessing on tablet/phone, and it's horrible. Tried to open the mortgage calculator tool last night to check something and after five attempts gave up.

The image issues and buggy design is the mobile optimised design. Quick fix I would recommend selecting request desktop site in your browser menu or switching away from the main default browsers where for some it just drops back to the nicer responsive desktop design that is at least still functional. Same image bugs are present on the herald site design in mobile which was so butt ugly I swapped to using the rss just to get the news without being reminded of all the terrible horrible bugs with their CMS. I am really sorry interest, I like your desktop design a lot, but the separate mobile design is both unnecessary, buggy and very very wrong, especially on tablets and in rotated views... it just makes me sad... like kicking a puppy. Oh god the contagion of the mobile design bugs is spreading... I'm finding more... noo.

I see a quite a few people here in their 30s (or younger) itching to buy a house in Auckland, with a decent deposit, but not being able to afford to. All I can say is stay renting for now, keep saving, and wait. Affordability will return, and you will save yourselves a lot of money not buying in a bubble - especially if you are able to buy with their is the proverbial blood in the streets. If you keep saving, the deposit you are saving might end up being most of the cost of your first place. That is they way it was for us in Australia (yes, before the bubble expanded too much).

I agree but danger is underestimating politicians and bankers. I don’t think we’ll be done until we are at zero rates. Maybe one more cycle to go?

Would not surprise me if we and Australia go to zero or near rates if there's a market crash. That's what happened in Europe and the US.

Exactly. Whoever is telling you rates are going up they are just lying, in a market like this banks won't meet their expectations so they'll lower the rates as much as they can to attract new clients.

I find it absurd that some salaried bureaucrat thinks he can make the market. Going to end in tears.

Bought and paid for......The term, may be used...as one sees fit. Debt is self perpetuating a Stated policy, as is Taxes.. Cough up.

To sum up: Let's make it easier tor home owners to buy overpriced property but more difficult to investors to loose their money.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.