Low home loan interest rates have been here for some time. All banks offer rates starting with a "3" with many offers under 3.50% which are historically at record low levels.

But to get these rates you need equity in the transaction of at least 20%. And to get on to the 'property ladder' you need to start with a hard-to-save deposit.

Today's housing market data suggests that outside Auckland, a 20% deposit for a median house requires at least $105,000. For Aucklanders, that is a deposit of at least $175,000.

Data supplied to us by the Real Estate Institute of New Zealand shows that first quartile houses require a deposit of $80,000 outside Auckland, and $138,000 in the country's largest urban area.

Deposits at these levels are hard to accumulate. Committed and focused saving, probably involving KiwiSaver, is the only option - unless you also bank at the Bank of Mum & Dad (or win Lotto).

And if you don't have a 20% deposit, you are going to take quite an interest rate hit.

Typically, 'standard' rates are 50 basis points higher than 'special' rates. But they can be much more; for example at present the BNZ one year 'special' is 3.49% while its one year 'standard' is 4.45%, a premium of 96 basis points. Westpac has a one year 'special' of 3.39% and a one year 'standard' of 4.15% which is a 76% premium.

And low equity premiums are on top, adding another variable 25 to 150 basis points to the 'standard rates. (BNZ adds between 35 and 115 basis points for low equity situations on to their 'standard' rates.) How much depends on how far over the 80% loan-to-value ratio (LVR) you are.

It's an anti first home buyer situation essentially driven by the Reserve Bank (RBNZ) and its LVR policies. But bank policies take advantage of them in a way that the RBNZ isn't encouraging. The RBNZ applies 'speed limits' allowing some high LVR lending, just not too much. The RBNZ doesn't invoke interest rate penalties, they only limit the overall volume of high LVR lending that can be made. And they exempt new builds. But banks apply their 'standard' interest rates to all of them, plus they add low equity premiums. This is sort of a double hit given that the 'standard' rate is for situations where you don't have 20% equity, and the low equity premiums pile on higher rates for exactly the same condition.

Banks of course will point out the "higher risks" they are taking with this type of lending.

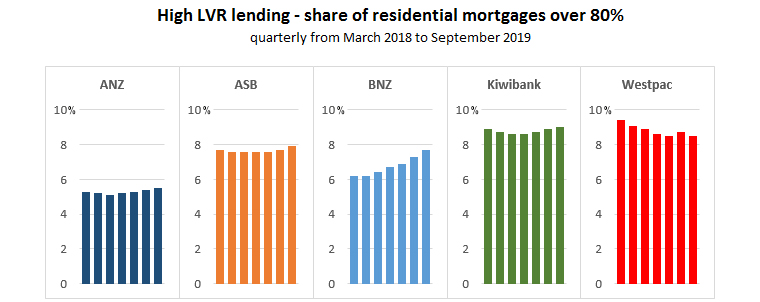

Some of them have a greater appetite for it than others. And others dip in-and-out of this type of lending.

ANZ, the nation's largest housing lender, has the least exposed on a weighted average basis. But ANZ is still lending about $4 billion to $5 billion into low equity housing situations. That is the same absolute level that ASB is committing and nearly the same as Westpac.

Kiwibank has the largest proportion of its mortgage book in low equity lending, but also the least dollar commitment. BNZ features in-between but distinguishes itself with a fast growing appetite for this type of lending.

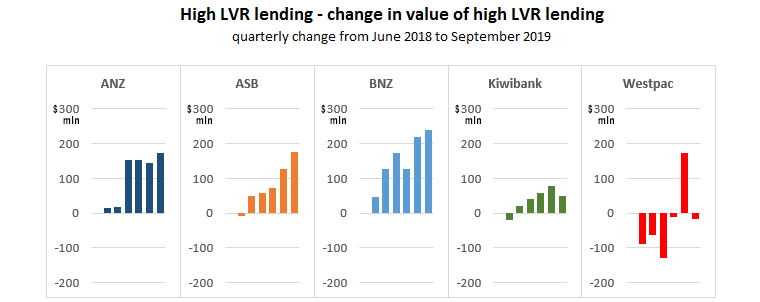

In fact, BNZ has added almost $1 billion in funding for high LVR lending between March 2018 and September 2019, half as much again as ANZ and twice the growth by ASB. Westpac has actually pulled back by a net $135 million over this period.

If you need a high LVR loan, it seems that BNZ is the most receptive. Mind the interest rate gap, however.

23 Comments

And there's another challenge; in a rising market bank valuations don't keep up with market value. To seal the deal you'll have to offer a higher price for the property than what the bank determines to be fair value. Guess where that extra money needs to come from? In most cases: a higher deposit.

If you're buying an existing property with under 20% deposit the bank will require a registered valuation anyway.. so that will be what the bank uses as a basis for it's valuation.

had a friend just buy, needed a valuation for more than what he already had approval for from the BNZ,

The Valuer asked what he needed to purchase and surprise surprise valuation came back at that figure so the BNZ lent him the funds and all is ok

purchase went through

"The Valuer asked what he needed to purchase and surprise surprise valuation came back at that figure so the BNZ lent him the funds and all is ok"

That is a very interesting observation, despite banks supposedly selecting the valuer to obtain independent valuations (& to stop buyers from selecting optimistic valuers.)

How many valuers are taking this approach?

What if that valuation is not reflective of current market conditions & is overstated?

Overly optimistic valuations potentially give rise to positive price feedback loops in the market, as higher valuations allow borrowers to borrow more, especially for those engaging in deposit recylcing / equity release financing techniques.

Having said that, the key constraint currently appears to be bank debt servicing calculations.

Buyer can still select the valuer, just has to be one on the banks list. And fat chance of the valuer not finding out what number the bank needs to see.. who lets the valuer into the house to value it?.. The RE agent that wants their commission, or the seller that wants their money.

Is it Normal at this time of year or is it unusual that in the last 7 days over 500 properties have been listed for Auction just in Auckland region.?

It's actually less than I would have expected. There's usually a huge rush of listings at this time. This rush is looking a little smaller, perhaps.

Quite normal as mid Feb through March until Easter is the main summer season. Majority of sellers wait until after people are back from their summer holidays, Auckland anniversary weekend, Waitangi day long weekend and have got the kids back to school which was late this year (7th Feb at my local primary school).

I was particularly interested in the listing share at Auction, as opposed to just Listed properties. I don't know any way to find that as a % share of listings.

Edit.....

Actually i just found a simplistic way, as shown in TradeMe anyway, there are 1128 new listings in the last 7 days, over 500 of which are Auctions, that's over 44% going to Auction, does that seem normal.?

Going back in 7-day steps it seems the % has increased since the week beginning 28th Jan. from 40% to 43% and latest 7 days 44%

These are new listings and will not have come to Auction date yet so cumulatively that 3 week period brought at least 1300 new Auction listings in Auckland alone to the market, all of which will actually be Auctioned in the next 3 to 4 weeks.

“Banks of course will point out the "higher risks" they are taking with this type of lending.“ To which they have a higher interest rate which means higher servicing costs and ironically increases the risk.

If the banks had true risk mitigation in mind, they'd impose higher principal repayments rather than interest rate premiums. But hey I suppose the competition is in the carded rates, if they can make a buck elsewhere by squeezing every last dollar they can out of a "scraped together" borrower then good on them??

The RBNZ doesn't invoke interest rate penalties, they only limit the overall volume of high LVR lending that can be made.

What about the higher RWA capital imposition for higher LVRs?

{kind=link}

It seems that you've forgotten to mention that more capital is required to be held for these loans. That capital is also increasing. The exemption for new builds is only relevant to speed limits not capital.

Also, I presume the charts are from the RBNZ Financial Strength Dashboard, which is an entire portfolio view. It does not necessarily indicate current appetites. There are on's and off's here - including when people drop to a lower LVR as they make payments.

Still very high interest rates for global standards, do not forget this.

For deposits too... not sure of many other countries where you can get 2.8% for 6 months.

And...it gets worse for lending at LVRs over 80%... some lenders impose a Loan Fee of $150, a Registered Valuation of the property being purchased is pretty much the norm and the Low Equity Margin applicable is not adjusted down automatically by the lenders when loan balances ( or property values increase) reduce. It must be customer driven AND..in most circumstances, Bank Customers must wait until the end of their current fixed rate period before any Low Equity Margin is reduced to the margin that then applies.

We are hoping to build at the end of the year and the high LVR margins and fees on top of standard rates is brutal. The arguments of risk etc are bull. The banks have insurance on high LVR debts so once that insurance is paid for it is just taking advantage of those who are already on the back foot. We intend to go with ANZ as they will knock 0.7% off a standard fixed rate if we build a Homestar 6 property and charge a high LVR fee rather than margin so it isnt an ongoing cost that people inevitably forget to follow up as their equity builds to ensure the margin is removed from their mortgage ASAP. ANZ will also give first home buyers (even high LVR) a $3k cashback and wave the application fee if you ask. Even though we are building we are going to have to get a registered valuation on the plans as well as a follow up valuation before the final payment is made on the build. We were also given the wrong advice by the banks that you can't access Kiwisaver for your deposit because an agreement has to be unconditional for Kiwisaver to release it - that isnt true! We were then told by that bank we would have to borrow our deposit at a casual overdraft rate of 19.95% until Kiwisaver released our funds! There is an undertaking available on most provider's standard solicitor's certificate where the funds will be held on trust until the agreement goes unconditional and if it falls over will be returned to the Kiwisaver provider. We were also given conflicting advice on whether Kiwisaver can be used to just buy land - one bank saying no and the other saying yes - it can by the way. Then we were told if we bought land with Kiwisaver we would have to build on it within 12 months. That also isnt true because there is nowhere within the Kiwisaver terms that stipulates a specific time period in which to build. First Home Grant does but Kiwisaver doesnt. You just have to have the intention of making the property your principal place of residence. These are the further problems first home buyers and high LVR borrowers also have - even the bank's expert advisors do not understand all the bureaucracy and conditions surrounding Kiwisaver, First Home Grant and First Home Loans. If you arent used to researching and understand the legalities you will be given inaccurate advice to rely on which will continue to set you back and earn the banks more money!

Lenders Mortgage Insurance (LMI) is only in Australia. I do not believe the NZ market operates this way .. Banks do not have insurance, the risk and extra capital loading by RBNZ are covered via margin. The other advice you received though is pretty poor.

Yeah you are correct on most of this. I took out my Kiwisaver a few years ago and banks/solicitors were all giving conflicting advice. My circumstances changed shortly after purchase and I had to rent the property. Some told me I could not rent it within 6 months as I had used Kiwisaver, so I requested a waiver from HNZ and they responded that only the Homestart Grant required you to live in the property for 6 months before renting, it did not apply to Kiwisaver. Since I had originally intended to live in it as my PPOR and didn't use the Grant, I was all good.

3 years later it has increased by 71% in value and I've been able to buy a new PPOR with the equity. Good times.

You were lucky that HNZ got it wrong: "You must have been a KiwiSaver member for three or more years. You can only withdraw money to purchase your first home - not an investment property", although they probably took the intent for it to be owner/occupied.

I went and double checked the email - it was the Financial Markets Authority, not HNZ who advised me.

The KiwiSaver Act does not stipulate you must live in it for six months - the advice was correct.

Just purchased a turnkey off the plans and the bank required a valuation. Valuation came back at exactly the price we paid. Thanks for that.

We mustn't forget that banks do not proactively check to see if your capital payments have reached the 20% LVR threshold where low equity premiums are removed and the special rates can kick in. You have to force them to check. If you find you've ended up paying 5.5% instead of 3.5% for 3 months, the bank won't pay that back to you.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.