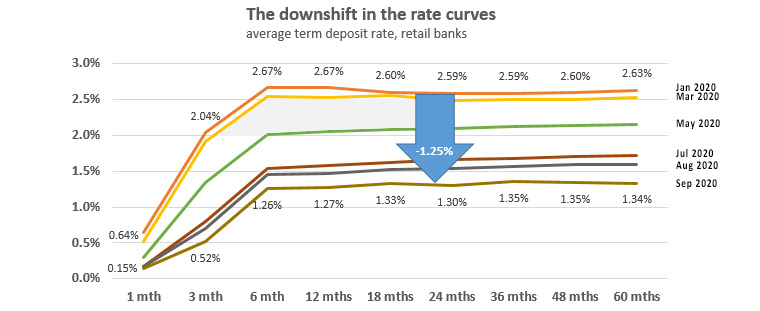

In 2019 we were able to make the point that banks protected their savings customers more than their borrowing clients when the central bank cut its official cash rate benchmark.

The year started with an OCR of 1.75% and ended at 1.00% and savers only felt part of that, especially those who invested in terms less than one year.

But the tables have been turned in 2020.

The OCR has fallen from 1.00% to 0.25% so far this year. But term deposit offers have fallen more than that.

In fact, the cumulative reduction has been more than the OCR change and banks have tended to pass on this to their borrowing clients.

Regular readers will know the underlying reason; banks are awash in customer deposits and have far more liquidity than they can lend out in the current environment.

Deposits from households are up a heady +8% in a year.

And the deposits-to-loans ratio is now its best at 83.5% and its highest since RBNZ records started. This is a growing problem for bank stability because customers only want their funds held in short and very-short term deposit instruments, whereas borrowers want to borrow for long periods, as much as 30 years. For a banker, to fund short and lend long is asking for trouble when economic stress is high and rising. We are in that environment now.

So banks need to find long term committed funding, and that comes from wholesale markets. Even so, they haven't been fast enough to lock that in as household depositors have been loading up their deposit accounts faster than the treasurers can find and lock in long-term money (most of which is sourced offshore).

In this environment, few banks offer deposit interest rates designed to attract funds. In fact, the reverse is happening and offers tend to be grudging, minimum offers out of 'sympathy' for depositors - and don't count too much on the 'sympathy'.

The latest to cut term deposit rates to very low level is ANZ, but even their reduced offers are not as low as some of their main rivals. There is no client reaction or downside risk to having the lowest offer in the market at this time.

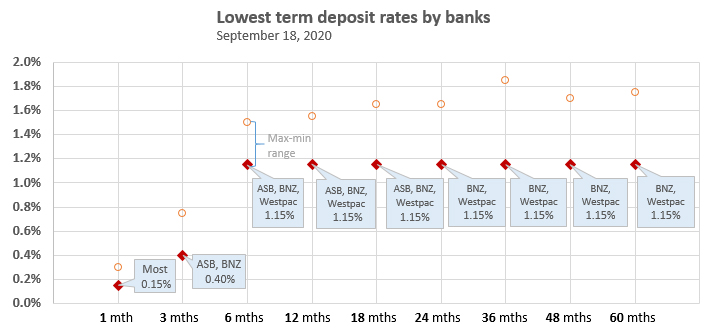

We have noted these levels before, but here are the mid-September updates.

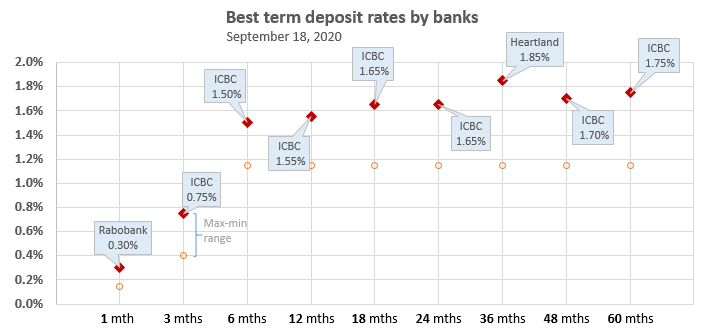

And the highest rates (even if they are high in the normal definition of the term) are as follows.

79 Comments

Soon the retail banks will start charging the RBNZ fees to do the RBNZ's bidding

And they'll pay us at the checkout, to take food away.

Who will pay us to take food away pdk? Who is 'they' and who is 'us'?

For as long as interest rates are low, people will borrow money to consume/invest......

And asset prices will climb.

TTP

If OCR turns negative, the banks will pay the RBNZ to offload QEed NZ government bonds in exchange for settlement cash.

On wholesale funding, the banks have been telling the world about how safe they are for well over 20 years. It was an easy 'game' to borrow in JPY and buy AUD and NZD. A carry trade play with currency risk. The banks would use wholesale funding for cheap mortgage debt funding. Money for jam if they hedged their risk properly. You never read about it anymore. What we do know is that some of the Japanese rural banks (Japanese farmers are notorious savers) have been scouring the work for investments (returns so low in Japan they can barely cover costs).

Post panademic economy / business / institution / Agencies will change including investment and saving pattern along with borrowing.

Good or bad only time will tell as are in surreal world where saving has been replaced by borrowing and fundamental of economy of demand and supply being replaced by printing and distribution of money where everything is Distorted.

Good or bad only time will tell as are in surreal world where saving has been replaced by borrowing and fundamental of economy of demand and supply being replaced by printing and distribution of money where everything is Distorted.

Hence the growing awareness and realization of Bitcoin as a currency based around being a 'store of value' as opposed to something that can be created on a whim. There is a certain irony here in that most people still look at Bitcoin as being the opposite of what it actually represents. Furthermore, those same people 'trust' their own national fiat currencies, even though it's manipulated to the point where it's wiping out any psercieved value that those people want to exchange their labour for.

So far panademic and lock down has been a boom for for speculators and so called investors with all the stimulus and money been thrown by government.

In stock market, experts and pundits like Warren Buffet has been sitting on sideline but amature and first timers have been lucky to hit jackpot for now and is it just a fluke being lucky or is the real norm which economist and experts have failed to understand.

Even reseve banks have helped in creating hyper bubble to super inflate asset class but can they sustain it for long as only way possible is to create more and mire money to buy bonds/distribute till the economy gets back to normal as once they walk the path of printing money, their is no turning back till things get back to normal even if it takes eternity as the moment is stopped niw will be bloodbath.

Like life cycle one should not be afraid of economy cycle but the fear of correction by the political class is doing more damage in tbe long run than good.

Strong dose of pain killer may help the pain in short term but is not the cure and if too much pain killer even that will be ineffective as body gets immune to it.

Now even small caps are following the trend just like other stocks and housing market.

It shows how distoterted the economy world is and can just hope that reserve bank knows what they are doing and long term outcome

https://stockhead.com.au/news/the-asx-small-caps-fund-managers-have-the…

Alittle, hear what Jim Roger is saying as he too is confused just like all experts except government and reserve bank

'whereas borrowers want to borrow for long periods, as much as 30 years' Keep asking an accountant that and sadly, he keeps saying no. Are there any possibilities to borrow for say 10-20 years fixed? how do they do it in the US? That's for residential or farm so say 0.5 to 10 mill.

Many are predecting that worse is yet to come but NZherald confirms that recession is over so good times ahead and worse is over.

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

Many are predecting that worse is yet to come but NZherald confirms that recession is over so good times ahead and worse is over.

Yes, but unlikely Liam Dann wrote that headline. Liam addresses things in an understandable manner for most people who're not interested in the hard, uncomfortable questions about how economics applies to the real world. Liam openly addresses the central bank's focus on house prices to not disturb the wealth effect. He does it uncomfortably but at least he's not afraid to dismiss its existence.

banks are awash in customer deposits and have far more liquidity than they can lend out in the current environment..... because customers only want their funds held in short

Of course! (And the 'lower they go' the more this rational behaviour will be reinforced)

But there's an easy answer.

What is the shortest of short date interest rates we have? The OCR - Overnight Cash Rate to fund banks if and when required. So....

Allow ALL taxpaying New Zealanders to open an OCR linked savings account with the RBNZ if they so desire.

It's a 'safe' alternative for those who worry about the soundness of the commercial banks; soaks up any cash retail banks would otherwise be 'awash' with - and allows them to tap it as needed via the OCR mechanism, and provides competition to the retail banks when the RBNZ needs to enact policy change.

Let us tack a suffix onto our existing IRD number; one that simply allows us to park At-Call funds with the RBNZ.

Put it in Kiwibonds. Repayable in 7 days with loss of interest earned, which is nothing. I just did that to settle on a Tesla. It’s clear that petrol prices aren’t going down and successive governments will kick the RUC can down the road so it’s a win win. I’d rather have assets I can touch than money in the bank.

Most cars lose a lot of value by driving off the lot. Even exotic so-called investment cars don't appreciate that much compared with opportunity cost, storage, insurance etc. Is there something about electric cars that I'm missing that makes the rule I mentioned not apply? I get less wear and tear, but instead of an engine wearing out you have batteries with finite lives.

Err, when it goes negative, as the wholesale swaps are pricing in, will you be happy to pay RBNZ as Retail banks will need to?

There seems to be a lack of understanding in this article as to how banking works. Banks don't lend out their customers deposits, these are kept in their reserve accounts at the Reserve Bank but may be used to buy government bonds or be lent to another bank. Banks create new money when they lend. This is explained here in this bulletin from The Bank Of England. They state, "Money creation in practice differs from some popular misconceptions — banks do not act simply as intermediaries, lending out deposits that savers place with them, and nor do they ‘multiply up’ central bank money to create new loans and deposits. It can be read here. https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

Its really quite astonishing. I tried to explain that to someone once and it sounded so ludicrous they didn't believe me.

Yes, this be true....and the housing market is the vehicle of choice to get new money into the economy.

Yes, and surprisingly, this is not what is taught in economics, even today! And, as MMT has noted, governments also create new money via government spending (which is extinguished via taxation).

Treadlightly you are correct. DC says banks lend deposits. In a previous retort he told a reader "think about it" if banks could just create money they would not go broke. That's misleading because banks create money buy purchasing securities and writing a premisory note.

So if someone wants a house then the bank creates a deposit backed by the security ie House. This is why house prices can't drop especially if leverage has occurred.

This can be explained by "stock flow consistent modeling' I think, where it states that for every asset there must be an equal and offsetting liability. Economist Wynne Godley had a lot of input into this idea. https://en.wikipedia.org/wiki/Stock-Flow_consistent_model

Treadlightly you are correct. DC says banks lend deposits. In a previous retort he told a reader "think about it" if banks could just create money they would not go broke. That's misleading because banks create money buy purchasing securities and writing a premisory note.

It's not misleading at all. Banks are able to lend more than they have in terms of they have in capital reserves. This is what is generally understood as the 'ability to create money'.

This is why house prices can't drop especially if leverage has occurred.

Nonsense

Nonsense

Explain then why they haven't dropped?

They have dropped recently in Oz.

In 2008 they dropped in US and UK.

That’s a little misleading. While the Extension of credit creates the money, the matching deposit doesn’t go to the bank, it goes to the seller. Banks have balance sheets, capital buffers and deposit ratios to maintain, so they do need matching deposits, whether by capital injection, wholesale or retail. Otherwise, there would be lending only banks ... do you know of any?

No you are correct I accidentally got confused in my explanation. I read a book called prince's of the yen that explained how it worked.

Question if house prices collapse 80 percent what happens to the price of money?

Cheers misterb

So banks need to find long term committed funding, and that comes from wholesale markets. Even so, they haven't been fast enough to lock that in as household depositors have been loading up their deposit accounts faster than the treasurers can find and lock in long-term money (most of which is sourced offshore).

And when those offshore wholesale markets dry up - then all the cash depositors will be in the box seat.

And I suspect, banks being banks, when they see this on the horizon they'll take deposit interest to negatives so as to claw back some of the pain before the event. I suspect that type of preparation has more to do with ANZ closing out Bonus Bonds - they were relatively risk free places to park cash that could not become subject to negative rates.

And when those offshore wholesale markets dry up - then all the cash depositors will be in the box seat.

No. The banks don't need wholesale funding. In the case of the Aussie banks, it was a useful source of cheap funding for mortgage debt.

But if that offshore wholesale funding dries up - what do you think they will do to roll over the long-term debt?

It's a good question. By the way, here's a good overview from the RBA about wholesale funding that was published in Dec 2019. Wholesale debt funding is much larger than I thoight it was.

https://www.rba.gov.au/publications/bulletin/2019/dec/the-nature-of-aus….

Sovereign secured lines direct to Fed.

Remember its the headroom in fx swaps that often is first governor on operations.

"Can we do the name" they cry.

That funding is unnecessary, it's a tribute paid to foreign banks. Moreover, NZ banks monetise the NZD hedge side of the trade, generally supranational Kauri NZD bond issuance.

Take a look at the RBA's view of deposit creation There are ways to address the funding mismatch with derivatives. Furthermore, retail bank deposits are not designated "sticky" by RBNZ without reason.

The mismatch ratios require banks to hold a certain stock of readily liquefiable assets to ensure that they can meet their short-term obligations. The CFR addresses their longer-term funding position by forcing them to hold a certain amount of more ‘sticky’ core funding, e.g., long-term wholesale debt with maturities of more than one year, or retail deposits.

Thanks for the clarification Audaxes

So, effectively banks will never need retail depositors?

Not in the sense they are saving to fund bank lending.

But from the point of view of the bank, it has acquired the security without giving up any cash; the counterpart, in its balance-sheet, is an increase in its liabilities. There is expansion, from its point of view, on each side of its balance-sheet. But from the point of view of the rest of the economy, the bank has ‘created’ money. This is not to be denied. Hicks (1989, 58)

We start with the idea of credit creation, specifically a swap of IOUs between a bank and myself involving a bank loan that is my IOU and a bank deposit that is the bank’s IOU. Nothing could be simpler, and yet the mind rebels, especially the well-trained economist’s mind, because this simple operation increases my purchasing power without decreasing anyone else’s. It seems like alchemy, or anyway a violation of some deep conservation law. Real productive resources are the same as they were before, and the swap doesn’t change that, does it?

Spending of the new purchasing power adds another layer of perplexity. If spending increases but real resources do not, then it seems logical that the increased spending must exhaust itself in higher prices—that is the intuitive appeal of the quantity theory of money. My purchasing power may increase, but everyone else’s decreases because their money balances buy less. From this point of view, the alchemy of banking seems like a kind of theft, something to be deplored in the name of economic science and if possible outlawed in the name of the general good. Link

Perplexing alchemy - no matter how much I try to make sense of it, I cannot understand just how the world of banking/finance got here. Ugh.

Will cash ever be king again? A good topic for a traditional yes/no debate.

What side would you take Audaxes?

Cash cannot adequately supplant the volumes of ledger money currently in circulation - too cumbersome, as is gold.

Our main banks should be seriously investigated for such a shameful lack of competition.

Regular readers will know the underlying reason; banks are awash in customer deposits and have far more liquidity than they can lend out in the current environment.

How does it look if one considers $56.657 billion HQLA and $38.274 billion deposited at the RBNZ

Potential FHBs getting shafted from both ends...deposits cant grow whilst low rates are inflating house prices...

Generational shafting

This is all going to make it harder for first time house buyers, as property prices get pumped up even more. I can't understand why the housing crisis in NZ isn't a bigger issue this election campaign.

It is an issue but they don't want to address it. It's too difficult. The politicians don't have any solutions or answers.

Any politician who tries to sort out the property price issue will be dealt to by the boomers who want prices to keep increasing. Their kids and grandkids futures do not matter. Jacinda stepped back from trying to implement CGT as she knew she could not win that battle.

Ever thought that the people you so disparagingly call "Boomers" might actually be attempting to provide for their children and grandchildren via something called a "Will". Maybe the "Boomers" are actually looking after their own family interests, as opposed to the "Me too" and "I want it now

" generation, who seem to want someone else to pay for their future.

Don’t buy your theory Hook. The boomers are downright greedy. Many have more than they ever will need. They have stuffed it up for the generations who follow them. And politicians won’t take them on as they want their votes. Who needs 20, 40 , 80 or more rentals?

it's nothing to do with baby boomers, it's a system that benefits those with existing assets and capital. Baby boomers are not a race of people or people who just happened to be born at the right time, they cover the full range of socio economic grouping.

The way our society is structured makes it very hard to compete in a capitalist world. The more the govt intervenes the worse it gets, ie, note the effect of govt trying to influence CB's to set a zero interest rate policy.

I am a farmer, the govt brought in Tenure review of the high country and made many many of those farmers multi millionaires, stopping those farms from ever being owned by genuine Kiwi farmers.

The govt introduced the Student loan nightmare, the accommodation supplement, which is little more than welfare for landlords, councils adding costs and regulation making housing an elite occupation, duopolies etc., I could go on.

Or is it that the "boomers" are the most afraid of being poor, the most afraid of future security?

It shows in many comments - "what about my wealth", "we'll all be poor", "I worked hard for this, it's all mine".

The fear is totally understandable given the prior generations history of survival in a new colony and two world wars.

At what point though do we attempt to break the chains of fear?

Ex agent we are responsible for ourselves. Stop blaming others. The moaners need to live within their means. Everyone wants the latest iphone and pays for netflix and spotify and the latest clothes and car and 4k tv. If they learned about investing and compounding and the important rule of 72 then they would be better off. But from what i have researched delayed gratification cant be taught. A wise mentor of mine told me the saying of get rich slowly and anyone can to do it by saving and investment and living within your means.

Agreed 100%. Millennial Lifestyle Inflation (I'm a Millenial), I see it with my peers regularly. Nice lounge suites, big TVs/flash appliances/cars/phones etc but cant get that deposit together for a house in Christchurch/Rolleston.

In 3 years my salary is up with a 60% reduction in mortgage rates but my discretionary spending is unchanged. I've increased my mortgage payments (13 year schedule down from 25) and saving the balance. Have a 10 year old 32 inch LCD TV, our 1 family car is 20 years old, $200 Lounge Suite from TradeMe etc. Oh wait I lie, we bought a brand new Dishwasher a few months back.

Well done. The more you can save to get ahead in the early years the better off you will be. Its a long time ago now for me in cars but my first one I managed to do 258,000km in it. Things have moved on a lot from there but I wasn't unhappy driving a manual corolla back in the day and saving cash to invest.....

I think it's great that you are minimising consumption and environmentally unfriendly fast living. And there are certainly people that live indulgently who need to learn from their mistakes. But I think there's danger in that mindset when the surplus fruits of frugality are funnelled into property owned by a powerful social class. That feels like a society moving back to feudalism.

Frugality should be a reward for the individual and we should have a country where people can aspire to live a comfortable and healthy life.

You don't seem to grasp that the meritocratic methodology of frugality and conservative investment is immensely less effective in 2020 New Zealand than 2000 New Zealand.

That's precisely the problem, Hook. It used to be the case that you didn't need to have rich parents in order to do buy a home. Now the vast majority of people have to rely on parental help to get a house because deposits (and prices) are so high.

As for being the "I want it now" generation, that's just factually incorrect. Millennials have later marriage ages, first home buying and first child having ages- and the delay in those things is explained by the fact it takes a lot longer now to achieve financial stability. This is despite the fact that millennials have higher savings rates than boomers did at the same ages.

As for 'someone else paying for their future's its actually the other way round, really. Boomers have had the benefit of generous social services (including education), super, and rising asset prices (which essentially functions as a wealth transfer from young to old). Millennials are likely to see none (or at best, diminished) versions of these things, on top of the sacrifices made for the Covid response.

Why would anyone able to help their children now, hoard their money instead until they die and ruin family relationships post their death. I hardly know any estates that were settled with all the children coming out of it speaking to one another.

I agree Kate. My wife and I are gifting our children regular cash every year. And not modest amounts. We get great pleasure out of seeing them be able to live without being slaves to the Banks. One of them is debt free and the other will be when they buy their next home.

I suspect that a number have a non-liquid asset that they cannot or a scared of cashing in on at this point of time.

Most people live into their 80s or 90s now. So younger generations can settle down in their own property and start thinking about having kids when they’re nearing 60. Yep, works well. Also brilliant for those with poor parents, or parents who decide to spend it all on travel (as many Boomers do), or who have several siblings such that the inheritance is shrunk. What a great way to run a country.

You are so right and I'm sick and tired of this 'greedy boomer' theory from young people. We have done everything right, as far as saving for our family is concerned. We have one house that we live in, have helped our daughter into a house and trying hard to hold onto our savings (in term deposits) so that we can help our son into a house when he's able to get back from overseas. There may be some greedy people who want to spend on luxuries before they die, though I don't know of any, but we know we only have around 10 years left on this earth (if we're lucky) and we can't take our savings with us. Most people work for their family and to make things a little easier for them, and that's what we'll continue to do.

100% agree. The moaners need to live within their means. Everyone wants the latest iphone and pays for netflix and spotify and the latest clothes and car and 4k tv. If they learned about investing and compounding and the important rule of 72 then they would be better off. But from what i have researched delayed gratification cant be taught. A wise mentor of mine told me the saying of get rich slowly and anyone can to do it by saving and investment and living within your means.

I have a friend who is a landlord he has just under 20 houses, he was talking to other investors last week, they have all called the top of the housing market, are all looking at selling before Christmas.

So with lowest interest rates for 5000 years these guys think the housing market has tanked, my friend has been renting houses for 30 years. They are all rushing for the exit. New rental regulations have not helped.

Popcorn time?

Andrewj your friends is smart who is able to see what is comming specially at time when their is so much euphoria about housing market and that is one reason that he owns nearly 20 houses.

Either fundametal have to change/go up to meet the high house price or the house price has to come down to meet the fundamentals as equibilbrium has to be maintained and fundamentals (govt and reserve bank managed to hold by monetary and fiscal measures for now) moving up at this stage sems doubtfull, as all stimulus and printing of money has to end at some time.

I think it's always best to listen to real people, people with skin in the game, not conjecture ,speculation etc. Zero interest rates signal the end of Central bank significance in the economy.

Be fearful when others and greedy....people are attempting to be greedy while the real economy doesn’t support it. Might work short term but long term someone will need to pay the debt and if wages aren’t rising - well it doesn’t stack up.

Exactly right. There is only so much that the Central Banks can do to cheat the system, and only for so long. Once interest rates have reached the bottom, and the housing Ponzi has reached its peak, things will become very "interesting" indeed.

If you read the commentaries of asset owners and the financial articles in some papers in the late 1920's, and the comments of many speculators in 2007 just before the GFC, the resemblance to the current situation is starting to become positively disquieting. There were commentators in the US who were claiming that the housing market was completely rock solid just a few weeks before the s##t started hitting the fan. Moreover, there was no global pandemic at the time, global imbalances were probably not so pronounced as they are now, and the risks to international trade were not as high as now.

A lot of brand new builds (2-3 story row houses) going onto the rental market - and sitting.

I will beleive it when I see it. They will not sell until they see a fall and the conclusion I have finally come to is that there wont be one. The government stepped in and started bailing everyone out this time because it's now to big to let it fail. What I finally had to get my head around is that money doesn't actually exist. It's now just numbers created out of thin air so the total debt can go up and up as long as the computers have enough digits. Computers are pretty easy to change you know when you say need to go to a negative OCR you just make it happen.

maybe prices don't have to fall, perhaps just being stagnant is enough for people to want to reduce exposure?

And National will move the bright-line test to 2 years and restore the ability for landlords to ring-fence losses. Paul Goldsmith justified that on the basis that NZ needs more rental homes. Translation: the oppressed will continue to be oppressed forever and their numbers will grow.

Well it is good to see that the blind panic has abated.

these guys think the housing market has tanked

Yet right here and right now it clearly hasn't. This is a very weird comment. Also a landlord with almost 20 properties and in the game for 30 years should have considerable equity. Perhaps it is a good time to rationalize things, pay down some mortgages by selling a few, but having rent coming in will be better than bank deposits by a long shot. Landlords like this are generally not too keen on selling up and buying shares either. So what are they going to do with the money?

The comment doesn't make sense and I'm calling BS. He's just a bit salty about new tenancy laws I reckon.

Na, he has found opportunities offshore and thinks the property market here is going to fizzle. Tax could be a hurdle for him.

That is interesting Andrewj as I heard this same thing a few months before the GFC. They were right then and I believe they are right now. I still think we’ll see plenty of positive market news until around Christmas but into 2021 I can see mammoth problems for people with large debt levels. A recession and the long term issues around covid have not really started yet as the government assistance and friendly banks are holding up the system and households. For Granny Herald to say the recession is over is ridiculous. But there are people who will just read it and accept the headline news without any further in depth research of there own.

Was listening to Jeff Booth being interviewed this morning. He’s a Canadian entrepreneur. He was discussing whether we are heading into a deflationary period which will mean unemployment, and really bad news for people carrying high debt levels. It’s well worth a listen. https://youtu.be/kGsp45JbvnU

Thanks, really enjoyed listening to that guy.

You can lend to my business at 5%. According to our credit rating agency we have a 0.04% chance of failure. Our growth rate has been 100% p.a. every year for the last 5 years, Covid be damned.

Greatest recession and boom of all boom both here at the same time.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.