This is a re-post of a World Gold Council article. The original is here.

The COVID-19 pandemic raised uncertainty by compounding existing risks and creating new ones. But by the end of last year, investors were optimistic that the worst was over. Looking ahead, we believe that investors will likely see the low interest rate environment as an opportunity to add risk assets in the hope that economic recovery is on the immediate horizon. That said, investors will likely also be navigating potential portfolio risks including:

• ballooning budget deficits

• inflationary pressures

• market corrections amid already high equity valuations.

In this context, we believe gold investment will remain well supported while gold consumption should benefit from the nascent economic recovery, especially in emerging markets.

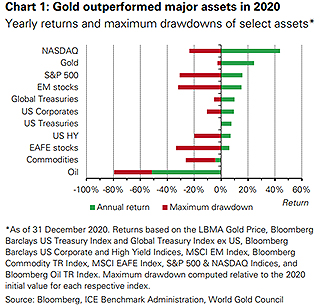

Gold gained from risk, rates and momentum

Gold was one of the best performing major assets of 2020 driven by a combination of:

• high risk

• low interest rates

• positive price momentum – especially during late spring and summer.

Gold also had one of the lowest drawdowns during the year, thus helping investors limit losses and manage volatility risk in their portfolios (Chart 1).

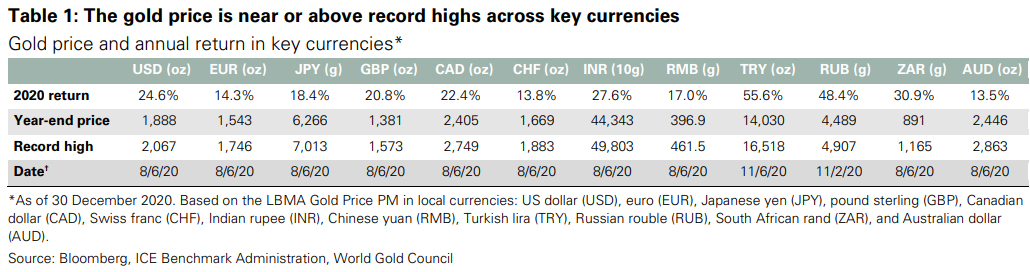

By early August, the LBMA Gold Price PM reached a historical high of US$2,067.15/oz as well as record highs in all other major currencies (Table 1). While the gold price subsequently consolidated below its intra-year high, it remained comfortably above US$1,850/oz for most of Q3 and Q4, finishing the year at US$1,887.60/oz.

Interestingly, gold’s price performance in the second half of the year seemed to be linked more to physical investment demand – whether in the form of gold ETFs or bar and coins – rather than through the more speculative futures market. For example, COMEX net long positioning reached an all-time high of 1,209 tonnes (t) in Q1 but ended the year almost 30% below this level. We believe this was due to the dislocation that COMEX futures experienced in March relative to the spot gold price, making it more expensive to hold futures compared to other choices.

Investors’ preference for physical and physical-linked gold products last year further supports anecdotal evidence that, this time around, gold was used by many as a strategic asset rather than purely as a tactical play

Gold investment to react to rates and inflation

Global stocks performed particularly well during November and December, with the MSCI All World Index increasing by almost 20% over the period. However, rising COVID-19 cases and a reportedly more infectious new variant of the virus created a renewed sense of caution. Yet, neither this nor the highly volatile US political events during the first week of 2021 have deterred investors from maintaining or expanding their exposure to risk assets.

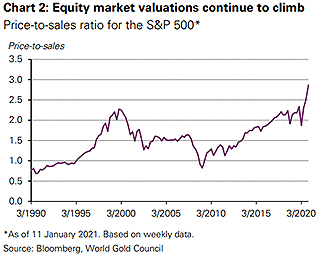

The S&P 500 price-to-sales ratio is at unprecedented levels (Chart 2) and an analysis by Crescat Capital suggests that the 15 factors that make up their S&P 500 valuation model are at – or very near – record highs. Going forward, we believe that the very low level of interest rates worldwide will likely keep stock prices and valuations high. As such, investors may experience strong market swings and significant pullbacks. These could occur, for example, if vaccination programmes take longer to distribute – or are less effective – than expected, given logistical complexities or the high number of mutations reported in some strains.

In addition, many investors are concerned about the potential risks resulting from expanding budget deficits, which, combined with the low interest rate environment and growing money supply, may result in inflationary pressures. This concern is underscored by the fact that central banks, including the US Federal Reserve and European Central Bank, have signalled greater tolerance for inflation to be temporarily above their traditional target bands.

Gold has historically performed well amid equity market pullbacks as well as high inflation. In years when inflation was higher than 3%, gold’s price increased 15% on average. Notably too, research by Oxford Economics shows that gold should do well in periods of deflation. Such periods are typically characterised by low interest rates and high financial stress, all of which tend to foster demand for gold.

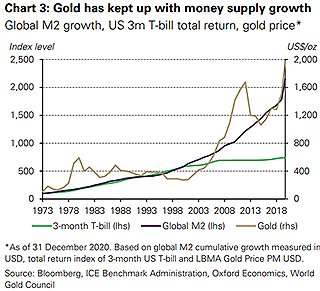

Further, gold has been more effective in keeping up with global money supply over the past decade than US T-bills, thus better helping investors preserve capital (Chart 3).

Emerging Markets economic recovery to benefit consumer demand

Market surveys indicate that most economists expect growth to recover in 2021 from its dismal performance during 2020. And although global economic growth is likely to remain anaemic relative to its full potential for some time, gold’s more stable price performance since midAugust may foster buying opportunities for consumers.

The economic recovery may particularly realise in countries like China, which suffered heavy losses in early 2020 before the spread of the pandemic was controlled more effectively than in many western countries. Given the positive link between economic growth and Chinese demand, we believe that gold consumption in the region may continue to improve.

Similarly, the Indian gold market appears to be on a stronger footing. Initial data from the Dhanteras festival in November suggest that while jewellery demand was still below average, it had substantially recovered from the lows seen in Q2 of last year.

However, with the global economy operating well below potential and with gold prices at historical high levels, consumer demand may remain subdued in other regions.

Central bank demand not going away

After positive gold demand in H1, central bank demand became more variable in the second half of 2020, oscillating between monthly net purchases and net sales. This was a marked change from the consistent buying seen for many years, driven in part by the decision of the Central Bank of Russia to halt its buying programme in April. Nonetheless, central banks are on course to finish 2020 as net purchasers (although well below the record levels of buying seen in both 2018 and 2019). And we don’t expect 2021 to be much different. There are good reasons why central banks continue to favour gold as part of their foreign reserves (see our Central Bank Gold Reserve Survey 2020) which, combined with the low interest rate environment, continue to make gold attractive.

Mine production likely to improve

Recovery in mine production is likely this year after the fall seen so far in 2020. Production interruptions peaked during the second quarter of last year and have since waned.

While there is still uncertainty about how 2021 may evolve, it seems very likely that mines will experience fewer stoppages as the world recovers from the pandemic. This would remove a headwind that companies experienced in 2020 but that is not commonly part of production drivers. Even if potential second waves impact producing countries, major companies have introduced protocols and procedures that should reduce the impact of stoppages compared to those seen in the early stages of the pandemic.

Putting it all together

The performance of gold responds to the interaction of the various sectors of demand and supply, which are, in turn, influenced by the interplay of four key drivers. In this context, we expect that the need for effective hedges and the low-rate environment will keep investment demand well supported, but it may be heavily influenced by the perceptions of risk linked to the speed and robustness of the economic recovery.

At the same time, we anticipate that the economic recovery in some emerging markets, such as China and India, may limit some of the headwinds the gold market experienced in 2020 caused by extremely weak gold consumption.

Using Qaurum, our gold valuation tool, we analysed the performance of gold as implied by five different hypothetical macroeconomic scenarios provided by Oxford Economics. These are:

• a steady economic recovery (their base-case scenario)

• a delayed recovery

• a deep financial crisis

• a rapid economic upturn

• a global second wave.

The results of the analysis suggest that, in general, gold may see a positive, though more subdued, performance in 2021. This may be driven primarily by a recovery of consumer demand relative to 2020 as economic conditions improve. In addition, gold’s performance may be boosted further by the prolonged low interest rate environment which would all but remove the opportunity cost of investing in gold.

Alternatively, our valuation model suggests that a global economic relapse from COVID-19 or any other unforeseen risks could result in weak consumer demand, thus creating a headwind for gold’s performance. However, a risk-off environment such the one captured by Oxford Economics’ “deep financial crisis” or “global second wave” may result in strong gold investment demand, which could offset low consumption as it did during 2020. Historically, this behaviour has occurred as investors look for high quality, liquid assets, such as gold, in these risk-off environments.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis (restarting for 2021 on Monday) here »

Precious metals

Select chart tabs

22 Comments

V committed conclusion. Not

You need to have the real thing, paper gold is wordless if you buy it as save investment. https://www.rt.com/shows/keiser-report/512358-inflation-level-bitcoin-m…

Anything on the Kaiser Report, whilst amusing, should be taken with a large block (not just a grain) of salt

Anything on the Kaiser Report, whilst amusing, should be taken with a large block (not just a grain) of salt

Max Keiser has been bullish on BTC since 2011. Would have been the best block of salt (and easily the most profitable investment) you'd ever have taken if you followed his advice and bought and hold BTC. His year-end price prediction prediction for BTC in 2020 was one of the most accurate among BTC celebrities.

Keiser is insightful and smarter about economics and the monetary system than most. The fact that he's also an entertainer is kind of beside the point. Furthermore, Max would be among the first to suggest people need to educate themselves and make their own decisions.

So he's an advocate of BTC and crypto.. good on him and his acolytes that follow. Doesn't mean his general financial advice is anything but entertaining. It's a free world.. believe who you want.

Max is also a large holder of physical gold and silver. He has skin in the game so he's worth listening to for an informed perspective. He is not a financial adviser. He's a broadcaster.

Interesting you have such in-depth knowledge of his holdings. Ever stopped to think .. If he's got so much how come he's still working??

If he's got so much how come he's still working?

People have different life goals. Wealth doesn't mean people stop working if they enjoy or love what they do. Peter Thiel, Bill Gates, and the late Steve Jobs are good examples of those who prefer to work than do nothing.

So Keiser would rather get up, go to a cheap nasty studio, spend his morning performing, and go home, all for the enjoyment?? As opposed to buy some land, a yacht, get a supermodel girlfriend and spend his days travelling the world - what a trooper.

BTW the three you mentioned are in a completely different league from Keiser and they are/were significant owners of their companies which in all cases rely/d on their names as a branding exercise

Getting back to Gold - realistically, from '08 on it hasn't been that crash hot especially if you work in inflation. In 13 yrs it's barely doubled (gross in USD). History would suggest that Keiser's suggestion isn't that hot.. especially with current commentary about an impending oversupply (which admittedly may or may not be accurate)

So Keiser would rather get up, go to a cheap nasty studio, spend his morning performing, and go home, all for the enjoyment?? As opposed to buy some land, a yacht, get a supermodel girlfriend and spend his days travelling the world - what a trooper.

Max Keiser lives in southern France and broadcasts from his home. He's married to Stacey Herbert. Accept that people's lives and dreams may be different to others.

Accept that people's lives and dreams may be different to others. - J.C. fundamentally every human wants the same thing (unless they belong to a cult or a convent). To dismiss or discount that is either naïve or delusional. Unless you're talking about Mother Teressa or the Pope that's just how it is. Some disguise their ambitions well, but the ambitions are there nonetheless

This is the most outrageous hot take I think I've ever witnessed! Awesome

Getting back to Gold - realistically, from '08 on it hasn't been that crash hot especially if you work in inflation

Your interpretation of what inflation is likely to be different to mine. In the way that I view inflation (expansion of the money supply), gold has performed as a store of value. It is not a speculative instrument.

I was talking about inflation from '08 to now.. not future inflation. The whole "store of value" argument is being tested recently and imv the jury is still out. Who knows?? perhaps the old saying "buy land 'cos it's in finite supply" actually is on the money.

By way of reasoning - I bought 40acres in '06 for 500K. It's got a GV now of 1.1 mil. I just today looked at a 5 bedroom+pool house that'll go for about 1.1-1.2 mill but was valued in '06 for 550K.. is that not a value store?( the land)

I was talking about inflation from '08 to now.

So am I, but I am likely to have a different perception of inflation compared to you. As a 'store of value', gold has proven its worth over time. As for the emergence of BTC, they share similar properties, but it doesn't mean BTC replaces gold. And just because my BTC holdings appreciated in fiat value by 200% in 2020 and gold holdings only by 15%, it doesn't necessarily mean that BTC is overtaking gold.

You need to have the real thing, paper gold is wordless if you buy it as save investment.

As someone who owned the GLD ETF for almost 16 years, I think this is not correct. While the premise that there is more paper gold than physical gold is correct, there are now different options that I believe these people are unware of:

1. PMGOLD--'Rights' to gold ownership that is 100% backed by physical gold under Perth Mint custody and guaranteed by the Western Australia govt. I sold all my GLD holdings to buy this.

2. Gold digital tokens--Who needs paper at all when gold can be owned and exchanged via a blockchain with gold tokens? Perth Mint issues digital gold tokens, which I have also bought.

I don't mind gold, I've owned gold, it's probably tending up..

However Gold is also very financialized, aka 'paper gold'. Many billions of fines have been issued for gold manipulation too.

Due to the financializaton of gold, Gold Bugs are largely dependent on central banks adding (physical gold) to their balance sheets.. central banks in cahoots with the likes of PJ Morgan and Goldmen could drive the price up some.. probably wouldn't be looking good for the greenback at that point.

If I was to get back into precious metals, I'd probably dollar-cost-average into unallocated SILVER via the Perth Mint.

The strengthening NZD prompted me out of gold, also storage fees and its illiquid nature. Probably volatility to trade if your into option trading.

Re the suppression of the gold price, JPM is the main culprit. They are the largest owner of physical gold and derivatives in the market. Central bank purchasing is largely irrelevant. The non-Swap countries accumulate for a reason and that is largely about the demise of USD. NZ is tightly connected to this as a Swap nation.

I have exposure to silver through ETPMAG (yes, I know I'm a hypocrite because of my scorn for JPM) and exposure to junior miners through SILJ. For a real wildcard, you could check out Myanmar Metals who have access to one of the best (if not the best) high-grade deposits on Earth.

I'm quite the 'lunch-money-investor' - I'll take a stake in something, then dollar-cost-average up my stake. I had some 'lunch money' in New Talisman Gold Mines too, but liquidated towards the end of the lockdowns - think I was up about 30% - very much a penny stock. Gold mines tend to have a high failure rates too.

I'm probably staying away from gold in all its forms this year. Will be the first time in 5 years I've owned none.

Newbie here re QE causing inflation vs deflation and how that affects gold. But if the QE stops however, hypothetically, if markets correct, does everyone jump to cash out, and seeing as cash is still somewhat tied to gold, does gold/silver go up? Due to demand.

Or is the cash/gold link totally gone (in a market behaviour manner, not the technicalities of non gold standard).

Or is the cash/gold link totally gone

The 'cash/gold link' is totally gone in the sense that in 1971 Nixon stopped backing the US Dollar with gold. So you could no longer wonder into a bank and exchange your cotton notes for physical gold. The purchasing power of the US Dollar has gone down since down.

But if the QE stops however, hypothetically, if markets correct, does everyone jump to cash out

Your presupposition is that people have jumped into the Gold Market and the physical market at that. Central Banks have been known to sell gold, on mass. Putting aside what counts as QE, it would depend on why QE stopped. If people have confidence in dollars they are less likely to buy gold. If stopping QE crashed the US economy people are likely to buy gold and Bitcoin.

Gold is also priced in USD, so you have to consider the price movement of the NZD/USD pair. Gold is probably more akin to an insurance policy/store of value - gold was what.. $20 in 1971 ??

You cant have an article about gold and not mention Bitcoin. Not only does it do a better job than gold at storing wealth, but it also significantly outperformed every other major asset class illustrated on the above chart.

Check out the following article for reasons why Bitcoin is better than gold:

https://danheld.substack.com/p/bitcoin-vs-gold

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.