ASB's dramatic mortgage rate hike for one and two year fixed terms is accompanied by some term deposit rate changes too, all increases as well.

Banks have been tweaking their term deposit rates in a minor way for the past few months. But with them at very low levels saver interest in these offers has dissolved away.

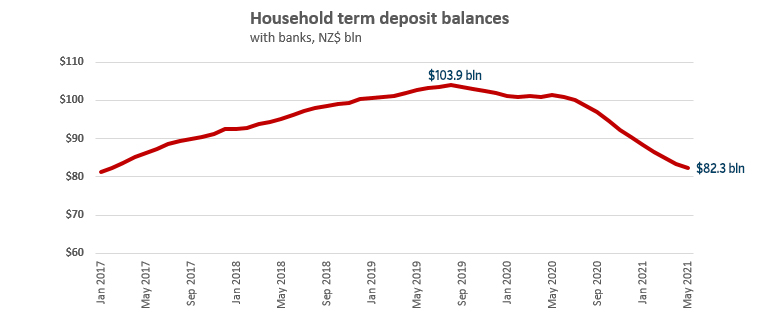

We can see that in the overall level of the banking industry household term deposit book.

On Wednesday Kiwibank raised its 200 day term deposit rate offer to 1.20%.

And ASB raised its six month offer to 1.00% along with all its offers from 18 months to five years. In fact, ASB's new five year offer is now 2.00%, the highest for that term for any bank. However, in a rising market (?) it seems very unlikely that many investors will be tempted to sign-up for such a long fixed term.

ASB also offers the highest market term deposit offers for 18 month terms and longer.

The highest short term rate is from Heartland Bank at 1.10% for a four month term.

The highest rate for any bank for a term about six months is now from Kiwibank with its 1.20%, 200 day offer.

The highest bank one year rate offer is from Rabobank at 1.35%.

Savers have been rejecting term deposits as a way to hold their savings. In the latest (May) household data from the Reserve Bank (S40), the level of funds held in term deposits fell by 18.8%, or $19 billion, from the same month in 2020. That is an accelerating decline, and the total in household term deposits is back to 2017 levels - and back then, they were growing at 14.7% pa.

It is not as though savers aren't saving at the bank - they are. Total household bank deposit balances rose 5.1% in the year to May, up to $204 billion, and at about the same year-on-year expansion we have seen for the past several months, up $10 billion. Only term deposits are being rejected.

One problem for savers is that the Reserve Bank offers banks money at the Official Cash Rate, currently 0.25%, and in theory banks have no need to pay savers more than this. But the hikes by ASB, and earlier by Rabobank, Heartland and others suggest that banks may be looking to retain their term deposit books and not let them atrophy further - because in the future they may need them when the Reserve Bank withdraws the Funding for Lending Programme.

Not in the table below are four and five year rates. Only ASB is now offering a 2.00% rate and the only bank to offer at that level.

One easy way to work out how much extra you can earn by switching is to use our full function deposit calculator. That will not only give you an after-tax result, you can tweak it for the added benefits of Term PIEs as well. It is better you have that extra interest than the bank.

The latest headline rate offers are in this table with the markings for changes this week so far.

| for a $25,000 deposit | Rating | 3/4 mths | 5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mths | 2 yrs | 3 yrs |

| Main banks | ||||||||

| ANZ | AA- | 0.45 | 0.80 | 0.90 | 1.20 | 1.20 | 1.30 | 1.40 |

| AA- | 0.45 | 1.00

|

0.90 | 1.20 | 1.25 | 1.40

|

1.70

|

|

| AA- | 0.45 | 0.80 | 1.00 | 1.15 | 1.20 | 1.30 | 1.40 | |

| Kiwibank | A | 0.45 | 1.20

|

0.95 | 1.15 | 1.15 | 1.30 | |

| AA- | 0.45 | 0.80 | 1.00 | 1.20 | 1.25 | 1.35 | 1.50 | |

| Other banks | ||||||||

| Co-operative Bank | BBB | 0.40 | 0.90 | 1.00 | 1.20 | 1.25 | 1.35 | 1.45 |

| BBB | 1.10 | 1.05 | 0.90 | 1.35 | 1.15 | 1.20 | 1.35 | |

| HSBC Premier | AA- | 0.45 | 0.80 | 0.90 | 0.80 | 0.90 | 1.10 | |

| ICBC | A | 0.55 | 0.95 | 1.10 | 1.10 | 1.10 | 1.15 | 1.30 |

| A | 0.40 | 1.25 | 1.10 | 1.35 | 1.25 | 1.35 | 1.50 | |

| BBB | 0.50 | 0.90 | 1.10 | 1.15 | 1.00 | 1.20 | 1.35 | |

| A- | 0.45 | 0.80 | 1.00 | 1.20 | 1.20 | 1.30 | 1.40 |

Term deposit rates

Select chart tabs

13 Comments

About time the worm turned, deposits have been bleeding out from the banks. More rises to come I think and may have to go for a short term special come August.

I will look at term deposits again when they are at least 2.5%.

Dont forget inflation for the next 12 months will be at the very least 2.5%, probably over 3%

I see the US is mulling its 4.5% inflation this week.

In a financial position where I don't really care about inflation unless we turn into Venezuela. You get to a point where your money no longer needs to be going up, its a hard thing mentally to see it going down but nobody lives forever so start spending it.

Correct. I will wait and sit while banks bleed more and more term deposits, the OCR raises (which are a certainty) start biting in the next few months, and term deposit rates finally realign with inflation again.

Depositors should have a pit of patience and wait a few months, as rates will increase at a faster and steeper rate than many wish or expect, or go really short with the duration of new term deposits.

Don’t believe there will be much appetite right now , from discerning investors at least, for any of the longer terms?

Nobody in his right mind would go for a longer term deposit, in this environment that will see rapidly appreciating rates. Too much risk on the upside.

I think TDs are rapidly losing its attractiveness especially for retirement planning. Real estate seems like the way to go moving forward.

Property prices may flatline. Plus more compliance costs in the future unless buying new. Plus dealing with renters, maintenace etc. Can be a lot of work

Low term deposits have attributed to this property boom. Reverse the trend and it’ll help bring prices back down to earth. Need more options again for people to invest.

Kiwis are typically lazy investors. "Here, finance guy in a cheap suit, take my life savings and earn me a 10+% return." That's why TDs and property are popular - they're simple.

Some of us like to sleep at night with no worries. Yes could have been in an even better position than I am now but it came with risks but I decided to sell a property years ago rather than rent it out, couldn't be bothered dealing with tenants.

That isn't helped by both 87 and 07-08 . NZ investors were badly let down by both the sharemarket crash, and finance company failures where NZers lost billions. Infact the 87 sharemarket crash was probably worst in NZ than anywhere else in the world which turned people off it.

Property can be a lot of work, so often not a passive income like dividend stocks etc. ALso it may rise, but it also may flatline, or fall shorter term. IN the 90's property prices fell. NZ TDs historically have given a reasonable return, but not over more recent years. We were getting 8 - 9 % around the time of the GFC. But the fact that our banks still don't have a government guarantee is pretty poor, and the planned $100k guarantee per bank is also not great when compared to Oz whose GG is nearly triple per bank

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.